BKD - Brookdale Senior Living: Margins Asset Utilization Hitting Capital Productivity

2023-06-20 10:40:40 ET

Summary

- Brookdale Senior Living has had a difficult time producing returns on tangible assets above the market return on capital.

- BKD's market value has eroded from 10-year highs in 2015, and the company is currently trading at a discount to peers across key multiples.

- The company is not investment grade in my view, and does not pass my investment criteria on fundamental and economic grounds.

Investment Summary

Despite a strong pattern of mean reversion since my January publication on Brookdale Senior Living ( BKD ), the investment case remains largely unchanged in my view for the senior living colossus.

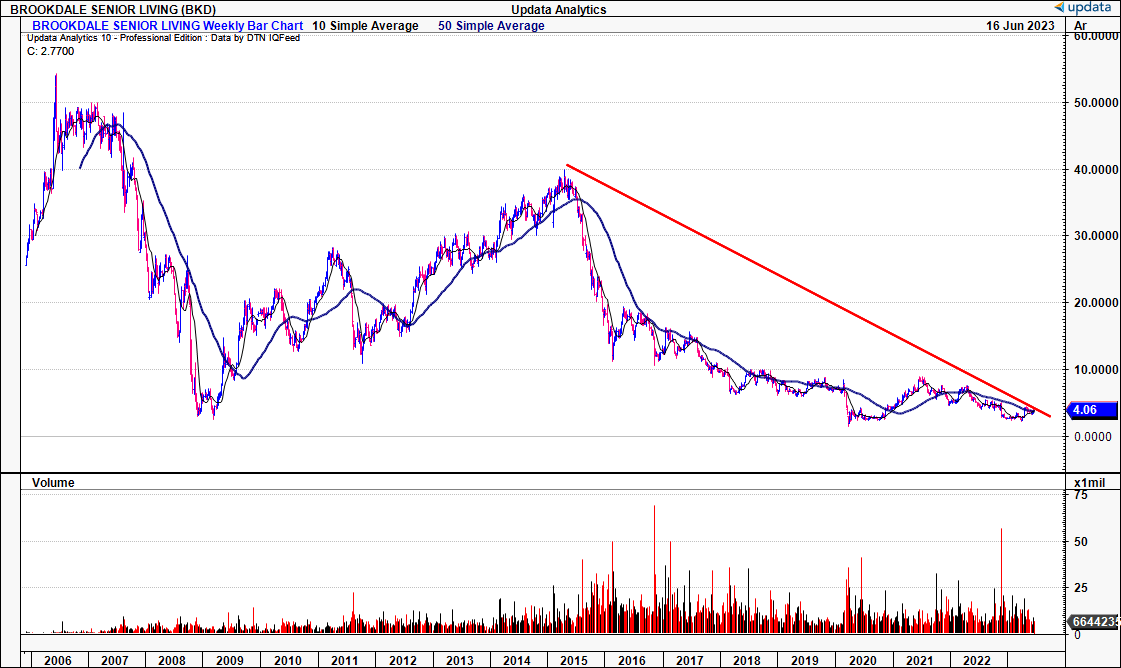

I say colossus, a representation of size, in terms of operations, not in terms of market valuation. BKD's market value has eroded off 10-year highs of c.$38 in 2015, only to trade at near 10-year lows as I write. Note in Figure 1, the sequential glide to the downside over this extended period, indicating the market's change in expectations for BKD each year.

Whilst the company has embarked on a significant capital reorganization scheme over the last few years, the economic returns on its tangible assets are still light, reflected in the company trading at a discount to peers across key multiples. Net-net, reiterate hold.

Figure 1. BKD long-term gradual sinking of market value

{kind=link}

Key investment drivers

In my own investment view, running money successfully involves a thoughtful analysis of the future. A thoughtful analysis of the future involves thinking in first principles. To think in first principles, one must also think in terms of combinations and permutations. That is – understanding what are the likely set of outcomes, and what are the probabilities each outcome will occur.

BKD is a hold for reasons of fundamental and economic origin. The company has a hard time producing a return on tangible assets above the market return on capital. The reasons for this are plentiful, ranging from capital structure to profitability. Alas, thinking in first principles, the investment debate is consolidated to those critical facts in my eyes.

1. Fundamental drivers

Much is gleaned from the company's latest results.

Senior housing revenue was up 12% YoY in Q1 , driven by a 290bp rise in occupancy, and an 8.6% growth in Revenue Per Available Room ("RevPAR"). These are the 2 critical elements underpinning BKD's unit economics.

Whilst BKD has clipped an additional $127mm in turnover since 2013, pre-tax income has shrunk by $166mm (TTM figures are used for 2023). This, on a far lighter capital base, as discussed later. With the financial performance exhibited to date, the economic result is a negative 1.3x operating leverage – the more revenue it makes, the more losses it generated over this time period.

Table 1. $127mm revenue gain matched with $166mm loss in operating income

Note: 2023 is shown in the TTM. All other figures are annual. (Data: Author, BKD SEC Filings)

- Unit economics

- Resident fees increased due to the Revenue Per Occupied Room ("RevPOR"; not to be confused with RevPAR) and the occupancy improvements listed earlier. As a positive, the gain in RevPOR came from the company's execution over in-place rate increases, adding growth to turnover.

- Despite the above, there was an 80bp decrease in weighted average occupancy, from FY'22–'23, but I would note this appears to be consistent with historical seasonal trends.

- Furthermore, the company recognized ~$2mm in other operating income from state grants during the quarter. It is expected to report modestly higher grant income in Q2.

Figure 2. BKD Q1 FY'23 resident fee revenue

Data: Author, BKD 10-Q

- Margins and asset utilization

- Moving down the P&L , facility operating expense clipped $531mm. Same community operating margin showed was also up 640 bps over the prior year, reaching 26.1%. Again, that growth in RevPAR was key in driving efficiencies in the quarter.

- It pulled this down to $9.1mm in operating income, and $94mm in core EBITDA. That's not a bad growth number actually, up $53mm YoY.

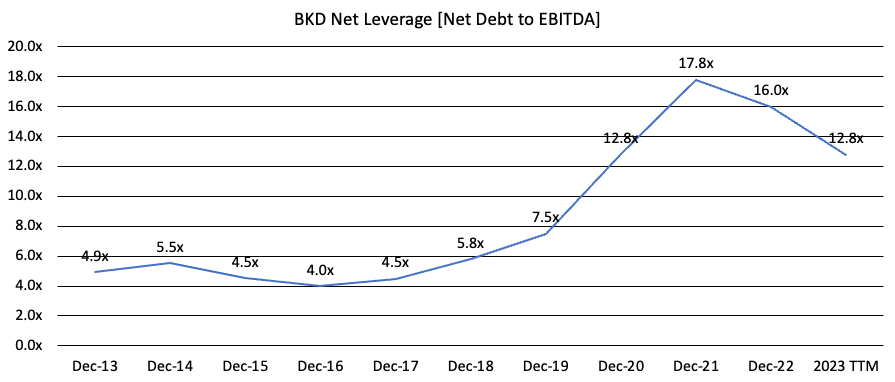

- As a potential risk, as of Q1, $540mm in equity held up $5.88Bn in assets, demonstrating the wide contribution of leverage to the company's balance sheet and financial results.

- You're looking at $3.7Bn in long-term liabilities, up from $2.16Bn 10-years ago, up from $3.34Bn 5-years ago.

- Around 60% of the debt is fixed and ~90% is structured as non-recourse asset-backed mortgage debt. Additionally, >90% of the variable rate debt is hedged with interest rate caps or swaps on a weighted average fixed rate of 4.14%.

- BKD's annualized leverage decreased from 19.8x at the end of 2022 to 15.0x at the end of the first quarter and is ~13x in the TTM.

- These are tremendously high rates of leverage in my view. Regardless of all the [potentially costly] derivatives hedging to ensure there is not too much pain to the balance sheet or income statement if things go wrong.

Figure 3.

{kind=link}

2. Economic factors and earnings power

The company has made a difficult time of meeting its cost of capital on a rolling basis. The profits BKD has generated from its tangible assets haven't accumulated at a rate faster than the market return on capital (defined here as 12%, long-term average). In my view, the following analysis does a good job in partly explaining the market's valuation of BKD.

Consider the following:

- Pre-tax earnings could be lighter in FY'23 on the smaller amount of business, continuing a longer-term trend. There's been some reprieve this year, we will see if the trends prevail. However, the issue is that BKD hasn't beaten the market's return on capital since 2020 [rolling TTM figures]. This is telling. It is unlikely sophisticated investors – those willing and able to pay higher market prices for the company – will be attracted to BKD with these undesirable economic characteristics.

- It tells us of a number of things – first, is the capital intensity of the business. The company has $5Bn at risk pushing just $261mmm pre-tax, 5.2% return on capital employed . Even with the $1.11Bn divestitures and write downs, this hasn't helped earnings. Second, is that BKD has not compounded its intrinsic value at rates above the market return on capital. Just remember, the market is a fairly accurate judge of intrinsic value in the long-term.

- That BKD has compounded incremental capital at rates below market rates means that investors have either (a) sold their BKD stock, or (b) profited from adding BKD to the short account – short interest in the stock is at a tremendously high 12.1%. This investment channel does not run a short account at this point in time, but sophisticated managers and investors may have food for thought there.

- With the movements in capital, there is reason to believe the sub-par returns on capital will continue in my view. For example, the company sold one of its entrance fee community assets, 306 units in total, last month It booked cash proceeds of $12.3mm, net of $29.6mm in mortgage debt repaid and transaction costs.

Figure 4.

Data: Author, BKD 10-K's

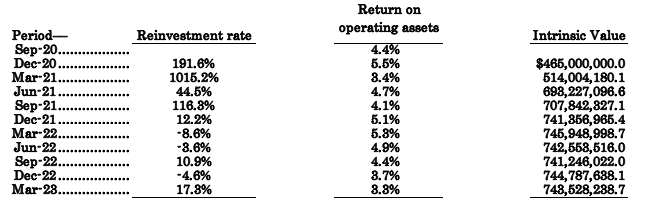

The market, therefore, has just about got it right with BKD in terms of its pricing on the company, in my view. Looking back to the last 2 years, at month end of September 2020, the company was selling at ~$465mm. A firm can compound its intrinsic value at the product of its return on invested capital, and the amount at which it invests at these rates. Permitted the ROIC is above the cost of capital, we can expect a higher market valuation.

By September 2021, the company was trading at $1.16Bn, whereas its intrinsic value had compounded to only $707mm. It was investing 116% of its earnings at ~5%, not intrinsically valuable – but, we all remember the irrational exuberance shown over the 2020–'21 period. Hence, by September 2022, when the market was looking at fundamentals vs. liquidity again, the market had valued the company back at $797mm, a nudge above the intrinsic value of $741m. It now trades at $764mm on a calculated intrinsic value of $748mm.

Over time, the market is a fairly accurate judge of fair value in my opinion, as mentioned.

Figure 5.

Data: Author, BKD 10-K's, market data

{kind=link}

Valuation and conclusion

Investors are selling BKD at ~ 17x forward sales , and thus are really clinging onto hope in my opinion. That, or trying to avoid any more pain from the last 10-years of results. There is heavy short interest in the stock for one, at c.12% as mentioned earlier, which could be one factor for that valuation also.

Not only that, the company has created $0.42 in book value for every $1 invested in operating assets, not surprising given earlier findings. Ideally, you'd look for a 1:1 if everything else stacked up. That tells me the propensity for a valuation upside is limited for two reasons:

- BKD is divesting its core assets, not reinvesting for growth, hence it will be difficult to create market value without the capital deployment; and

- The market is only rewarding each $1 with sub-par market returns anyway.

Just to show you how overvalued I believe BKD is at 17x forward sales, take the sector multiple of 15x. Given the complexities in the company's return, I am comfortable with management's Q2 guidance numbers. That is, adj. EBITDA annualizes to $288mm if the company does hit its $78mm target, and that's reasonable upside on FY'22, I will give the company that.

At 15x forward on the $288mm estimated you're looking at a $22.90 per share valuation (15x288/188.2 = $22.90). That is simply not acceptable in my view. Especially given the myriad of headwinds explained here. Thus, I would have to value BKD at 4x EBITDA forward, getting to $6 per share. Upside is noted, but it's not a risk I want to partake in. Therefore, I am reiterating hold.

In summary

Net-net, there are plenty of headwinds that suggest BKD has a ways to go before attracting investment. It has yet to pass my investment criteria on fundamental and economic grounds. Valuations are far too pricey as well and I'm not one to buy companies at a "discount" just for that reason. As such, BKD stock warrants a reiterated hold rating in my view.

For further details see:

Brookdale Senior Living: Margins, Asset Utilization Hitting Capital Productivity