BIP - Brookfield: 50% Discount To NAV Brookfield Infrastructure Distribution Risk Investigated

2023-10-30 09:14:23 ET

Summary

- BN is trading as if a ~50% haircut on Brookfield Property Partners, Infrastructure, and every other asset, has already occurred.

- BIP is covering any payout shortfall through capital recycling over the long term rather than through the issuance of debt or shares.

- BIP distributions to BAM, BN, and unit holders will not be cut barring material changes to the ability of the company to dispose of mature assets at attractive rates.

Editor's note: Seeking Alpha is proud to welcome Basil Finance as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Thesis

Brookfield Corporation ( BN ) is trading at a substantial 48% discount to my non-aggressive target of $43/share. Beyond that, the current market price reflects a -3% 5-year compounding on NAV compared to the +17% target set by management. For these reasons, I rate the stock as a 'Buy' today. While elevated interest rates and concerns around Brookfield Infrastructure ( BIP ) cash flows present risk, the margin of safety is more than large enough to offset the potential downside.

Company Overview

Brookfield Corporation is a conglomerate of three divisions.

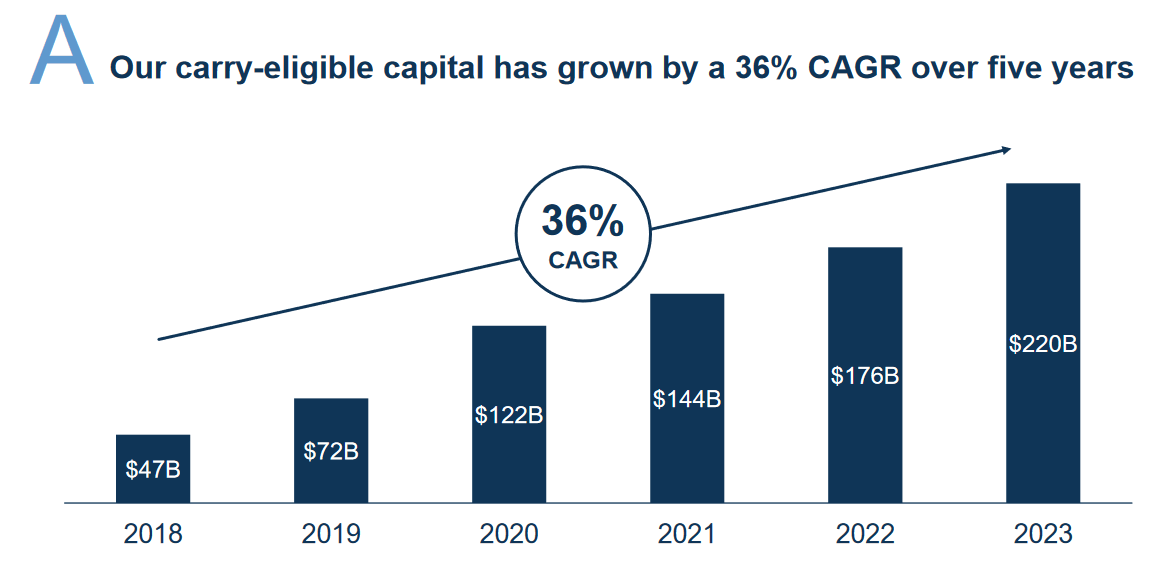

The largest and, therefore, most critical to the company is asset management. The asset management division has historically delivered very strong returns on their direct investments and has a proven reputation as a capital manager with a robust 36% CAGR in carry-eligible capital over the past 5 years. The ability for the company to consistently generate returns at or above target makes assets under management ((AUM)) 'sticky'. Combined with the high-margin nature of a wealth manager, this division provides high-quality revenue and earnings.

{kind=link}

The continued future success of the asset management division hinges on the continuation of their reputation as a high-quality manager of capital. The trend of AUM growth shows that this reputation remains intact to date. Recent Seeking Alpha articles have brought to light some concerns regarding BIP that some believe could potentially spill over as reputational damage onto the parent entities BN and Brookfield Asset Management ( BAM ). I believe that this risk is overblown and cover that in this article below.

The second largest division of BN contains the operating businesses including Brookfield Renewables, Infrastructure, Business Partners (private equity), and Property Partners (BPY, real estate). All of these sub-businesses are publicly traded outside of real estate, which is the subsidiary that receives the most negative press. Although they own 'trophy' core holdings, BPY faces a potential downgrade from credit ratings agencies to junk status due to a deteriorating fixed-charge coverage ratio. I view this as a significant contributing factor to the under-performance in the stock. It is an overblown risk that has created a good buying opportunity. The reasons being that:

- BPY makes up less than 20% of the assets of BN

- the non-recourse debt on BPY properties

- BPY could be valued at zero and BN would still be undervalued

- BN has the option to liquidate or walk away from lower-performing real estate assets to focus on servicing the higher-quality assets. Thus, it would be highly improbable for BPY to have zero value in the future

Finally, the insurance division. Although small today, it currently offers the highest cash flow yield across BN's various businesses. It also offers among the largest potential CAGRs. This business makes up 7% of NAV today but management growth targets show the potential to grow to 17% of NAV by 2028.

Equity Valuation

NAV Discount

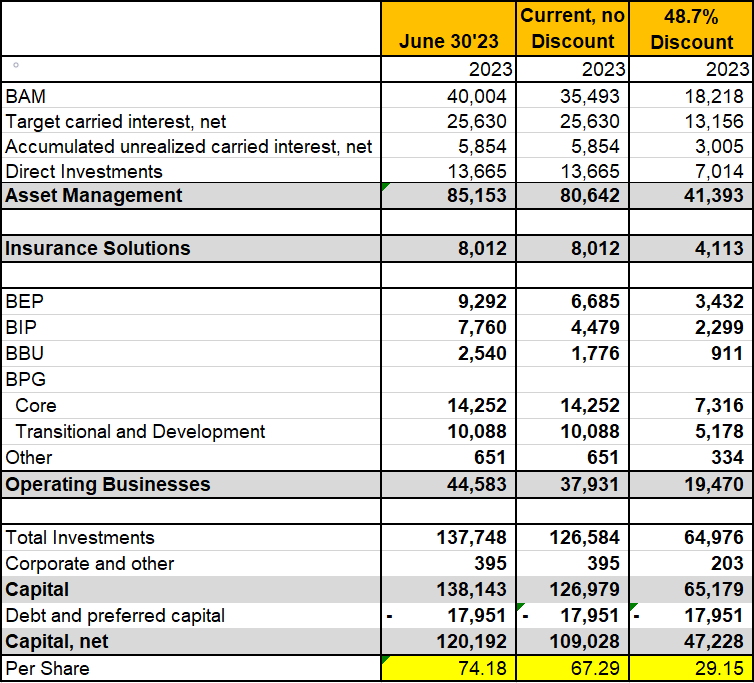

At the time of writing this article, Brookfield Corporation closed the trading week at $29.15 per share. On their August investor day and in the Q2 supplementary financials , they stated a current plan value of $74 per share.

Below, I modify the company financials to show:

- The current updated value after market corrections across the Brookfield companies

- How much of a discount is currently built into all of their assets while leaving debt unchanged

Brookfield Corporation SOTP Analysis (generated from Brookfield Corporation financials and market data)

{kind=link}

The first column of data is a replication of BN's work showing how they arrived at a plan value of $74 per share. The next column shows a plan value of $67 per share based on recent corrections across BAM, BEP, BIP, and BBU. The final column shows that a 48.7% discount is required on all assets in order to arrive at today's share price of $29.15.

The implication here is that BN is trading at a substantial discount and/or has a large margin of safety built into the current price.

Price Target

Using the $67/share current plan value shown above as a starting point, I take a conservative approach and subtract 50% of the value of BPY, resulting in $60/share plan value. I then project the current per share value based on five scenarios of NAV growth:

- A negative goal-seeked growth rate to determine the implicit rate implied by the current share price

- No growth

- 5% growth, my conservative base case

- 8.5% growth, half of management's target

- 17% growth, actual management target

These growth rate scenarios are projected out 5 years matching the company outlook and are then discounted back at 12% annually. This discount rate is made up from the current 10-year treasury rate of 4.84% plus a healthy 7% equity risk premium, rounded up.

The per share scenarios are summarized in the table below. These reflect the 2023 values based on the listed growth rates and the stated 12% discount rate.

Per share values by NAV growth (Author's calculations)

Thus, with a relatively conservative 5% NAV growth rate, a 12% discount rate, and a 50% discounted BPY asset value, my current price target for the company is $43/share. This is a 48% premium to the current share price and, therefore, qualifies for a Buy rating.

I used a discounted NAV method of valuation instead of discounted cash flows as the substantial carried interest earned by the company is lumpy and non-recurring. Thus, an analysis using a multiple of cash flows would exclude a material portion of the business.

Risks

Brookfield Infrastructure Concerns

Recently, concerns have been raised about the ability of the company to cover distributions from cash flows received from their investments. The concern stems from the fact that FFO supposedly does not equal to cash received. Simply put, FFO is based on how much the company's investments generate in cash flows. However, if their equity investments only pay out 50% of their cash flows to BIP but BIP bases their distributions to shareholders based on 100% of their equity investment cash flows, there is a cash shortfall for BIP.

It is this cash shortfall that the company may then have to make up for with debt or issued shares.

Some Seeking Alpha commenters have written to investor relations. IR has replied stating that the cash shortfall is made up for through capital recycling. Through capital recycling, the company aims to dispose of mature assets to fund higher return new investments.

Now there is an obvious question about whether this capital recycling is working as intended. If it was not, we would expect to see increasing debt per unit of cash flow, an increasing payout ratio, or deteriorating distributions per share, i.e., we would expect to see signs of an unsustainable business practice over time.

First, let's look at the debt side. The chart below illustrates debt vs various measures of cash flows to the company. Despite the debate around how the FFO values are used, they still provide a consistent metric that, when compared to debt, illustrates the effectiveness of the company's capital recycling program and whether there is a need to increase debt to fund distribution shortfalls.

BIP Net Debt vs FFO (generated from Brookfield Corporation annual reports data)

As the graph above illustrates, net debt remains relatively stable vs FFO/AFFO/Adj EBITDA for the last decade. This shows that issuance of debt is not masking capital shortfalls from any perceived payout ratio shortfall. To put this another way, net debt is increasing over time but not at a materially faster rate than cash received or distributed by the company.

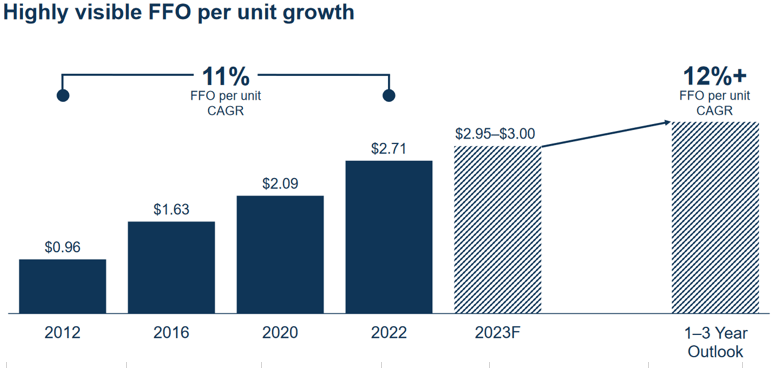

Next, we look at share issuance. The following two charts show the FFO/AFFO payout ratios and FFO per unit, respectively. Again, if the company was attempting to hide unsustainable business practices through share issuance, it would show up through increasing payout ratios or cause FFO per unit to stabilize/decline over time.

Payout Ratios (generated from Brookfield Corporation annual reports data) FFO per unit growth (Investor Presentation)

{kind=link}

Clearly, payout ratios remain stable over time. In fact, they have fallen to the target range of 60-70% of FFO in 2022. FFO per unit growth also continues as per plan.

The data on company debt, payout ratios, and FFO per unit growth shows that the company's claim, that capital recycling is making up any shortfall between cash received vs distributed, is valid.

Impact on BN, BAM, and BIP unitholders

Rising rates are certainly a risk for their continued ability to dispose of mature assets at attractive IRRs. Despite this risk, until BIP shows a slowdown in asset sale activity or shows a materially lower IRR generated in their asset sales, company cash flows earned and distributions to shareholders are expected to continue to increase as per management targets. Thus, unless or until these issues arise, cash distributions from BIP to BN, BAM, and BIP unit holders are not at risk in my view.

Interest Rate Risk

On top of the impact on the price of recycled assets, higher interest rates also affect the cash flow of the company at both the corporate and subsidiary levels. Higher interest expense are clearly a concern as seen in the BPY credit watch. However, based on the valuation section above, it is my view that we are more than compensated for this risk at the current share price.

Conclusion

Based on the large margin of safety on BN, both on an absolute basis and relative to other Brookfield entities, I currently hold shares in BN and hold no shares in BAM, BEP, BIP, or BBU at this time. The only thing holding back a 'Strong Buy' rating is a potentially looming recession that could sink all boats. A recession that sinks the BN share price without materially affecting the operations of the business should be viewed as a very attractive opportunity for accumulation.

I do not foresee a cut in distributions for BIP unitholders unless there is a change in the company's ability to recycle assets at attractive rates. The price of BIP units is based on a market multiple of the cash flows/NAV. This is a different story from the cash flows itself and one I may cover at another time.

For further details see:

Brookfield: 50% Discount To NAV, Brookfield Infrastructure Distribution Risk Investigated