BAM - Brookfield Asset Management: Best In Class But Caution Is Advised

2023-06-21 05:25:47 ET

Summary

- Brookfield Asset Management was spun off from Brookfield Corporation (formerly: Brookfield Asset Management).

- Although Brookfield Asset Management is not facing the same risks as banks, a recession will most likely have a negative effect on the business.

- Over the long term, management is very optimistic for the business to grow at least in the double-digits.

- And although the company has a wide economic moat around its business, I would be cautious at this point.

After several months of just providing updates on companies and stocks I already covered before, we will finally cover new businesses again. In this article I will (mostly) look at Brookfield Asset Management ( BAM ) as well as the parent company Brookfield Corporation ( BN ) as overlaps are hard to ignore. In particular, to get a feeling for the long-time performance of the business, we must look at the parent company as BAM was spun-off only a few months ago (we will get to this).

Screening for Wide Moats

Before taking a closer look at Brookfield Asset Management we start with a brief digression about the difficulties to identify companies with a wide economic moat. One way is to screen for certain metrics (like high return on invested capital or the outperformance of a stock over long timeframes). But one of the key requirements – and key characteristics– of wide economic moat companies is the stability in its reported numbers and consistency over time. And at least for me (and with the tools available to me) it is hard to screen for “consistency” as we must look at least at ten years of gross and operating margins as well as revenue and/or earnings per share growth to make qualified statement about consistency.

Another way to identify such businesses is by looking at other investors and their recommendations for high-quality businesses. I am always happy when someone else is providing hints or a list of companies. With the company names available, it is a lot easier to identify which companies might have the potential for a wide economic moat and it often takes only a few minutes to exclude those businesses without an economic moat. And a few days ago, I stumbled over “ Business Breakdowns ” – a podcast which is breaking down the business models of companies. Aside from some exceptions it seems like the list of companies covered so far in this podcast is a list of high-quality companies and including many businesses I have already written about.

As already mentioned above, I will start with Brookfield Asset Management and as always when I cover a “new” business for the first time, I will offer a description of the business (although Brookfield Asset Management seems to be well-known).

Business Description

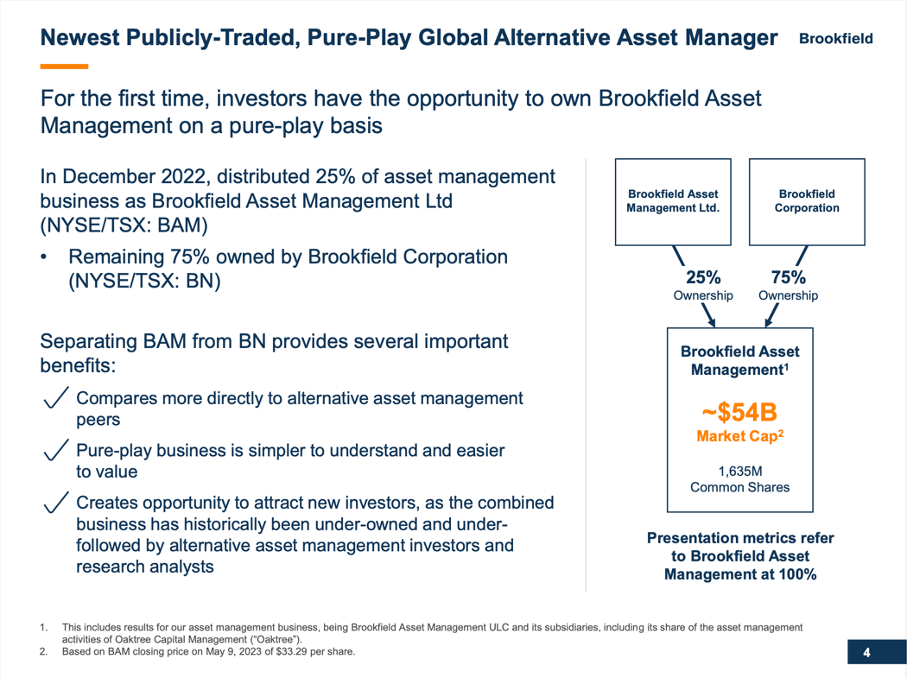

As mentioned above, on December 9, 2022, Brookfield Asset Management was spun-off from its parent company – which was previously named Brookfield Asset Management as well and now changed its name to Brookfield Corporation. 25% of the company’s asset management business was distributed as Brookfield Asset Management Ltd. and the reminding 75% are still owned by Brookfield Corporation.

Brookfield Asset Management June 2023 Presentation

{kind=link}

While Brookfield Asset Management Ltd. is only a few months old, the parent company was founded 124 years ago in 1899 and is one of the world’s largest alternative investment management companies. It was founded by William Mackenzie and Frederick Stark Pearson and started operating in Brazil.

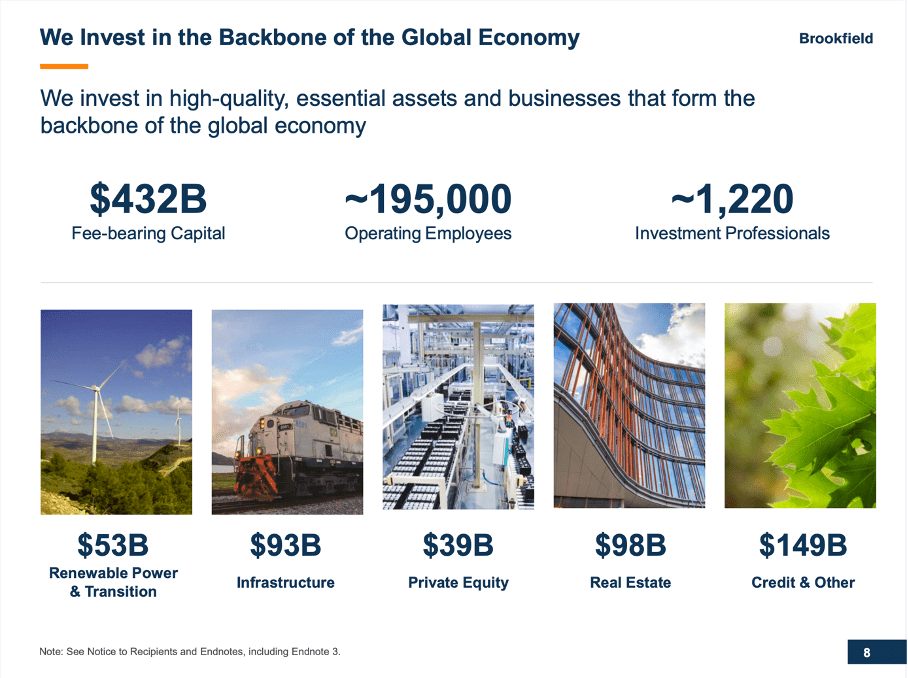

Today, Brookfield Asset Management is one of the largest and fastest growing alternative asset managers in the world (according to Annual Report 2022 ). The company is focusing on real assets like infrastructure, real estate and similar other “hard assets”. In the first quarter of 2023, Brookfield Asset Management had $825 billion in assets under management with $432 billion in fee-bearing capital. The company is operating in 30 countries around five continents and has more than 2,000 institutional clients.

Brookfield Asset Management June 2023 Presentation

{kind=link}

The company’s fee-bearing capital is mostly deployed in five different asset classes:

- Renewable Power and Transition : Asset types are including hydro, wind and solar as well as storage and sustainable solutions. In the first quarter of fiscal 2023, fee-bearing capital was $53 billion, and it generated $483 million in fee-related earnings in the past twelve months.

- Infrastructure : Asset types are including transportation, utilities, data infrastructure and midstream. With $98 billion in invested capital, this segment generated $836 million in fee-related earnings in the past twelve months.

- Private Equity : Asset types are including industrials, infrastructure services, business services, technology services as well as healthcare services. In the first quarter of fiscal 2023, the company had invested $39 billion in capital and generated $339 million in fee-related earnings in the past twelve months.

- Real Estate : Asset types are including housing, logistics and storage, hospitality, office, retail as well as science and innovation. The segment had $98 billion in fee-bearing capital and generated $984 million in fee-related earnings.

- Credit & Other : Asset types are including private debt, publicly listed equity and debt, insurance, and Oaktree Capital Management ( purchased a 62% stake in 2019 of the investment management firm founded by Howard Marks). Brookfield Asset Management has $149 billion in fee-bearing capital and is generating $999 million in fee-related earnings in the past twelve months.

Brookfield Asset Management Q1/23 Supplemental Information

{kind=link}

Risk

With the S&P 500 constantly climbing higher and many investors and news outlets being convinced that we are in a new bull market and extreme greed dominating the markets, collapsing banks are already forgotten. I myself are neither convinced we are in a new bull market, nor do I think we should ignore banks and the risk associated with them. In several articles about different banks (located in Canada , the United States or Sweden for example) I mentioned again and again that investing in banks is posing a rather high risk right now although most banking stocks appear to be extremely cheap (from a valuation point of view).

And while asset managers are a bit different from banks, some risks are similar. But let’s start with the positive news: the risk of bank runs (and those runs leading to a complete collapse) is rather limited for asset managers – especially compared to banks. While asset managers are also confronted with the risk of investors pulling out funds, there is a huge difference to banks. When putting my money into a bank deposit I expect to receive the same amount when I want to get my deposits back (and maybe interest along the way). However, the bank might purchase different assets with the money I deposited and when these assets decline in value the bank could face a problem when many depositors want their money back at the same time. Banks might give out loans and mortgages by using the deposits and are faced with the risk of default or – like it was the case for Silicon Valley Bank – purchase mid-to-long term bonds at a time when interest rates were extremely low and rising rates lead to a declining value of these bonds.

In case of asset managers, I will receive the amount my investment is worth at the time I want to sell (or withdraw) and the asset management firm therefore “outsourced” the risk to the investor. Brookfield Asset Management is also structured in an “asset-light” way as it does not have many assets on its balance sheet (and therefore limited the risk of declining assets). It makes its money via fees it receives for its management of funds from outside investors and when these funds decline in value it’s the investors’ problem.

Of course, Brookfield Asset Management will generate less fees when investors pull funds and revenue as well as profitability will decrease - risks we should not ignore. And when looking at the performance during the last few decades (we are looking at Brookfield Corporation again, as we don’t have the data for Brookfield Asset Management) we clearly see recessions having an impact and recessions are usually the time when investors pull out funds.

And one of the major risks for Brookfield Asset Management is the recession on the horizon (I know it doesn’t seem like it right now, but my opinion remains the same). When looking at past data, we must be a little cautious if the data is correct. To be honest, I don’t know how revenue can decline 111% as it apparently did during the Dotcom crash (I could not find any information, but the annual reports I checked indicate that number is false). However, the picture is quite clear. During recessions we must assume lower earnings per share and in a potential upcoming recession this will once again be the case. And with the company’s total direct costs being rather fixed (mostly compensation and benefits), the company would see its profit decline.

Economic Moat

Brookfield Asset Management is clearly facing risks – like most other asset managers and financial institutions – but the company also has a wide economic moat around its business – like most other asset managers. And one of my goals is to identify companies with a wide economic moat around the business and build a portfolio (or watchlist) including such companies.

In theory, asset management is easy to scale and that can lead to cost advantages for those businesses that have billions in assets under management. For Brookfield Asset Management it doesn’t make a huge difference if it manages $400 billion or $800 billion – the staff necessary and its expenditures are similar. But fees will double when assets under management double. And while this can lead to higher income, BAM can also use its dominance to lower fees a little bit to undercut competitors and make it difficult for new players to enter the market.

Another potential source for an economic moat might be the brand name of a business. And although Brookfield Asset Management doesn’t have a similar recognizable brand name as BlackRock ( BLK ) or Vanguard, such a brand name is not necessary as there is a huge difference between BAM and BLK: While many of the ETFs that companies like Vanguard or Blackrock offer, must be seen as commodities (it does not matter if I purchase an ETF matching the performance of the S&P 500 from BlackRock or Vanguard, the performance will be the same), Brookfield Asset Management’s focus is on alternative investments. These investments in infrastructure, real estate or renewable energy can’t be duplicated by other asset managers (and are therefore not commodity-like). Competitors can have similar funds, but the performance will differ.

And at this point, switching costs might also play a role. To be clear, asset managers usually don’t have “real” switching costs as it is quite easy to switch to other investments – to overstate a little bit: You press a button and sell. However, there might be a type of switching costs called procedural switching costs – in this case evaluation costs: It takes a lot of time to identify similar funds and as long as Brookfield Asset Management is performing well, slightly increased fees won’t be enough to make its customers search for and evaluated better options (as countless hours of work might be necessary).

Growth

A final aspect we must pay attention to is the company’s potential to grow in the years and decades to come. When looking at the past performance and the company’s targets for the years to come, we see quite impressive numbers. When looking at the last ten years – here we are looking at the numbers for the parent company Brookfield Corporation again – we see revenue growing with a CAGR of 17.37% and in the last 5 years revenue increased with a CAGR of 17.86%. Operating income in the last ten years increased with a CAGR of 15.43% and in the last five years with a CAGR of 18.86% (to be fair and not only present selected data, earnings per share increased with a CAGR of 3.12% in the last ten years, but the problem here are the low earnings per share in 2022). During its 2022 Investor Day, the company also reported annualized returns of 19% over the last 20 years.

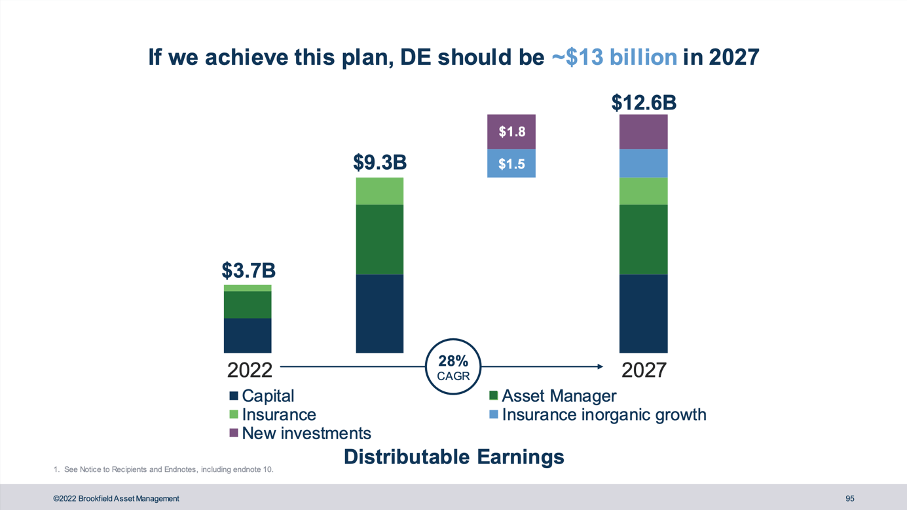

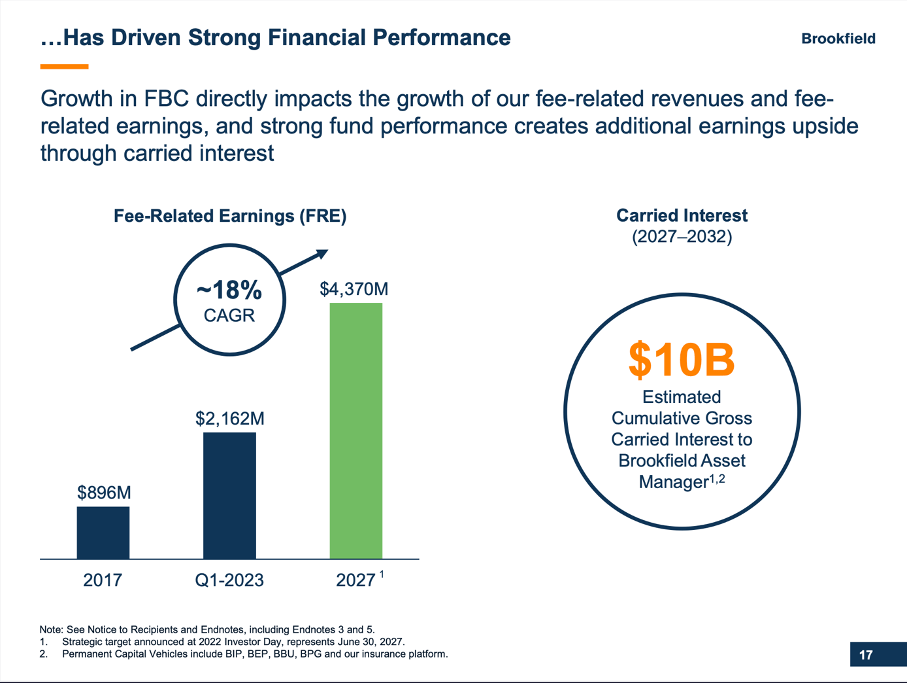

While these are without doubt great numbers, past performance is only a hint. Much more important however are growth rates we can expect in the years to come. And management has ambitious targets. Not only is management seeing the company positioned to deliver similar returns over the next 20 years as during the last 20 years (it has a growth target of 15% to 20%). For the years 2023 till 2027, Brookfield Asset Management is expecting $34 billion in free cash flow and is expecting its distributable earnings (one of the most important metrics for the company) to grow from $3.7 billion in 2022 to $9.3 billion in 2027 due to its capital, asset management and insurance business. And management is even more optimistic and assumes $1.8 billion in distributable earnings from new investments and $1.5 billion from inorganic growth of its insurance business. This would result in a CAGR of 28% for the next four to five years.

Brookfield Corporation 2022 Investor Day Presentation

{kind=link}

While these numbers are from a 2022 presentation when Brookfield Asset Management was not spun off yet (and are therefore targets for Brookfield Corporation), the targets for the asset business (according to Q1/23 presentation) are also ambitious.

Brookfield Asset Management June 2023 Presentation

{kind=link}

The question would now be how Brookfield Asset Management can achieve that extremely ambitious target. Some points are worth mentioning.

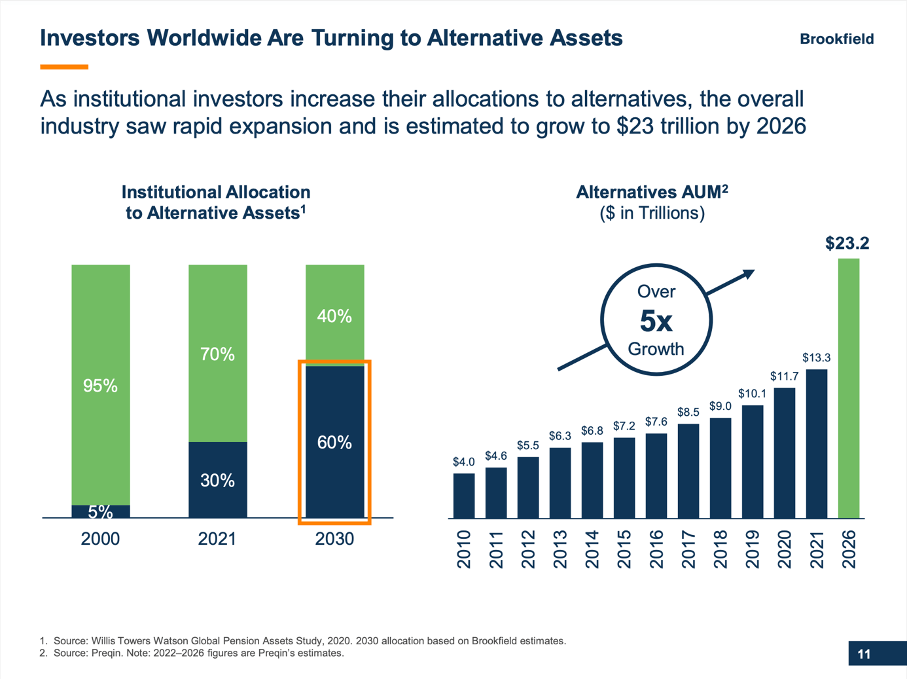

First, Brookfield Asset Management will profit from the trend towards alternative assets. Institutional allocations might increase from 30% into alternative assets in 2021 to expected 60% in 2030. And from $4.0 trillion in alternative assets under management in 2010 the number increased to $13.3 billion in assets under management in 2021. Until 2026, the company is expecting assets under management to increase to $23.2 billion. This is a major headwind for the business.

Brookfield Asset Management June 2023 Presentation

{kind=link}

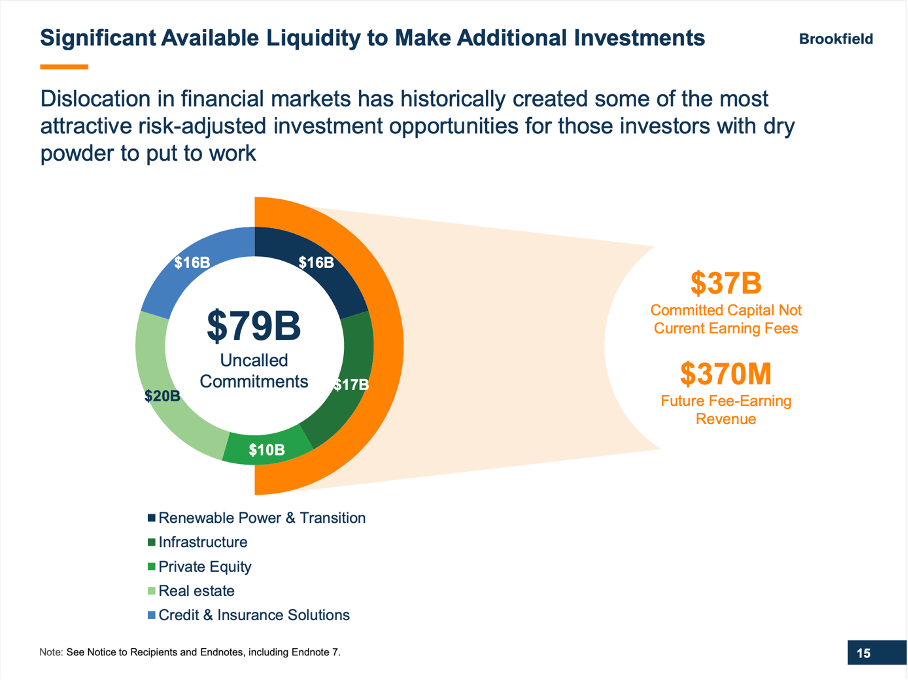

Second, the company has $79 billion in “dry powder” and about $37 billion in funds that are not earnings fees right now which will lead to $370 million in future fee-earnings revenue. Of course, this is only a small “booster” for such an ambitious target, but it should not be ignored as it could add about 15% in bottom line growth.

Brookfield Asset Management June 2023 Presentation

{kind=link}

I already mentioned above that the business is structured in an advantageous way for Brookfield Asset Management: Higher assets under management will lead to higher fees without the necessity for more staff (and therefore higher expenses). This will lead to improving margins over time and have an effect on the bottom line.

Brookfield Asset Management Q1/23 Supplemental Information

{kind=link}

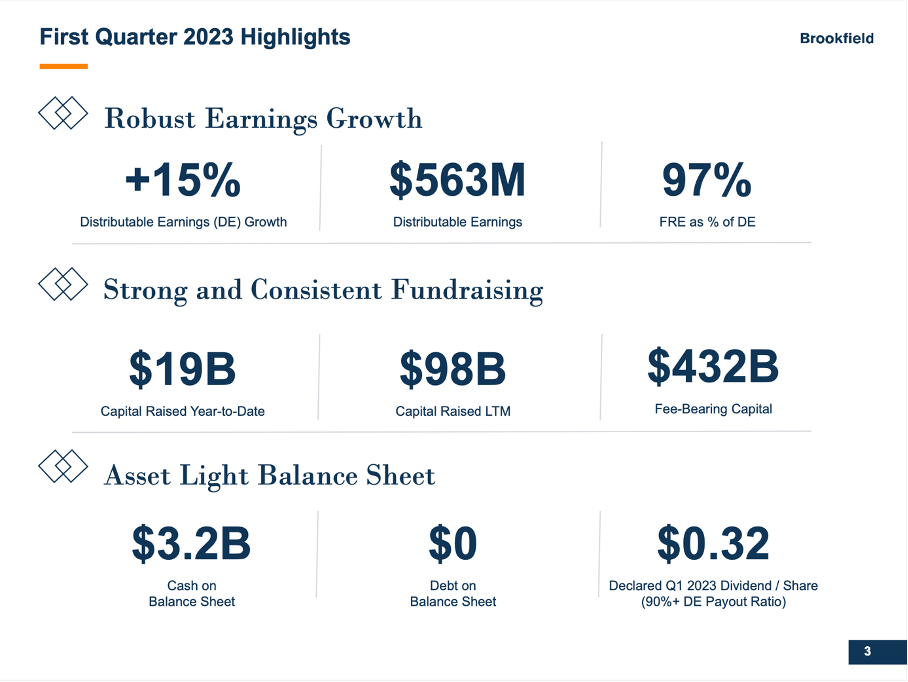

And we should also not ignore that Brookfield Asset Management is still growing with a high pace and could grow its distributable earnings 15% year-over-year to $563 million in the first quarter of 2023. And with $0 in debt on its balance sheet as well as $3.2 billion in cash on the balance sheet, acquisitions are also a possibility.

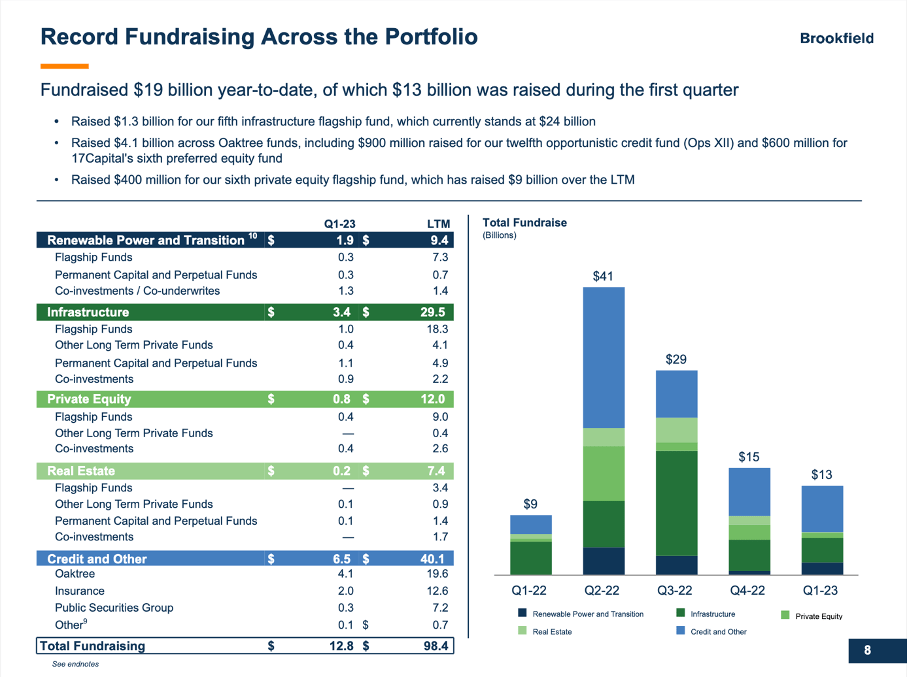

Nevertheless, Brookfield Asset Management is too optimistic for the next few years (in my opinion). I already mentioned above that we are probably headed towards a recession and in such a scenario we will most likely see lower inflows (or even outflows) and profitability of Brookfield Asset Management will suffer. And it certainly seems questionable if the company can continue to grow with the high pace it is predicting. So far, Brookfield Asset Management is still seeing inflows and raised $13 billion in funds in the first quarter of 2023. But we can also see inflows slowing down.

Brookfield Asset Management Q1/23 Supplemental Information

{kind=link}

Intrinsic Value Calculation

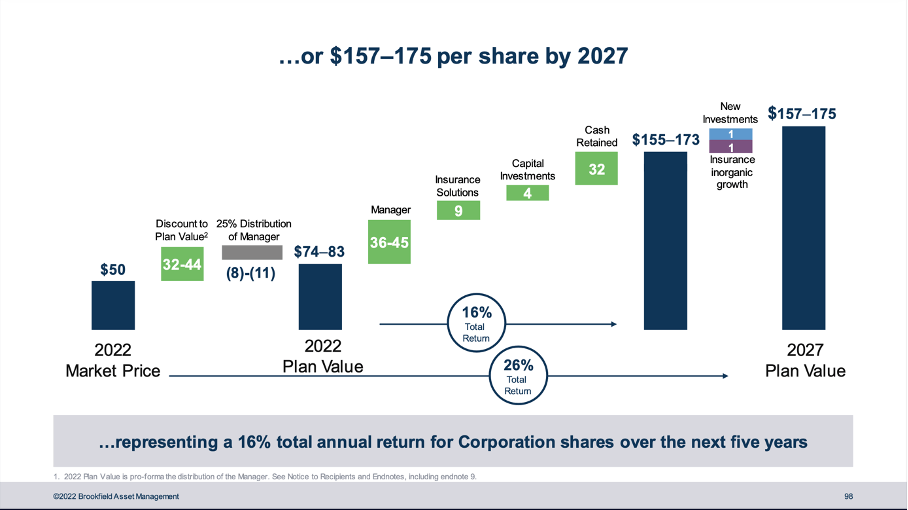

To be honest, I am a bit irritated that the company is providing such specific targets for its share price. Of course, I am doing the same when calculating an intrinsic value and it is absolutely fine for management to have an opinion what its share price should be and make projections. But I can’t remember any other business that is providing such specific share price targets for 5 years into the future.

Brookfield Corporation 2022 Investor Day Presentation

{kind=link}

And although the company is providing price targets itself (it is also important to mention that this presentation was held before the spin-off in December 2022), I would like to calculate an intrinsic value myself. I don’t want to predict a share price in 5 years from now but rather decide if the current stock price is a fair price for the business.

I already mentioned above that distributable earnings are probably the most important metric for the business, and we will take the distributable earnings of the last four quarters ($2,167 million) as basis. When assuming 1,635 million outstanding shares (and a 10% discount rate), the business must grow its distributable earnings about 6% annually from now till perpetuity to be fairly valued.

It is not like I don’t see Brookfield Asset Management being able to achieve these growth rates. I would not be so optimistic as management and assume growth rates in the high teens, but I definitely see the potential for the business to grow in the high single digits or low double digits. But I just don’t want to ignore the risk of very difficult quarters (and maybe years ahead) and am therefore a little cautious.

Conclusion

At this point, my conclusion for Brookfield Asset Management is similar as for most banks. The stock could be seen as undervalued, but I would be cautious about what will come in the next few quarters. With a dividend yield of 3.8% the stock can be seen as a solid long-term investment and under the premise not to panic in the next few quarters (and sell when the stock drops lower) it could be a cautious buy at this point. For me, the stock is only a “Hold” at this point, but I will keep a close eye and include the company and stock in my watchlist.

For further details see:

Brookfield Asset Management: Best In Class But Caution Is Advised