BAM - Brookfield Asset Management: If I Could Own Just One Company This Would Be It

2023-08-24 07:15:00 ET

Summary

- Brookfield Asset Management is a top pick for a buy-and-hold forever stock due to its strong growth potential and track record.

- BAM is the second-largest alternative asset manager globally and focuses on hard assets, such as global infrastructure and private credit, two of the largest megatrends in history.

- The company has a robust risk management profile, and management says it can grow 15% to 20% for the next 20 years, delivering Buffett-like returns for decades to come.

- BAM has delivered 40 years of almost 20% returns and is the only investment team I know of that has a chance to beat Buffett as the investing GOAT.

- Don't pay a hedge fund to manage your money when you can just buy BAM and get paid a fast-growing 4% yield while investing alongside two of the greatest investors in history (Bruce Flatt and Howard Marks) and their team of 1,500 investment analysts.

Many wonderful companies can be considered buy-and-hold forever blue-chips.

AAA-rated Johnson & Johnson (JNJ) and Microsoft (MSFT) are two obvious examples. Or how about Apple (AAPL), the new aspirational luxury brand likely to last for decades, if not centuries?

And, of course, we can't forget about single ticker retirement solutions like my favorite core ETFs, such as VIG ( aristocrats and future aristocrats ), SCHD (king of high-yield blue-chip ETFs), and SCHG (gold standard growth).

I would select SCHG as the ultimate single ticker "buy this forever and never sell" security. That's because it's the 50% fastest-growing companies in the S&P 500. So you are always getting the fastest growth world-beater blue chips.

But that's me. Many retirees would choose SCHD as the ultimate "set and forget and never check my portfolio" solution.

But recently, a member asked me, "What single stock, not ETF, but an individual company would you consider your favorite buy-and-hold forever company?"

You might think it's Amazon (AMZN) or British American (BTI); both are good guesses. Both are two of my highest conviction ideas of all time.

- Amazon: The Hype Is Right

- Buy Like Buffett: British American's 9.3% Yield Is The Highest In 23 Years

However, to answer this question, I took a different approach.

I asked myself, "what if I had to invest 100% of my life savings into one single company and then not check for 20 years".

That would truly be the ultimate buy-and-hold forever stock, wouldn't it? I would call Brookfield Asset Management ( BAM ) my ultimate buy-and-hold-and-forget stock and possibly the best SWAN investment of the next 20 years.

Brookfield: The Buffett Of Global Hard Assets

Brookfield traces its roots back to 1902 when it acquired its first asset, a Brazilian hydroelectric dam.

{kind=link}

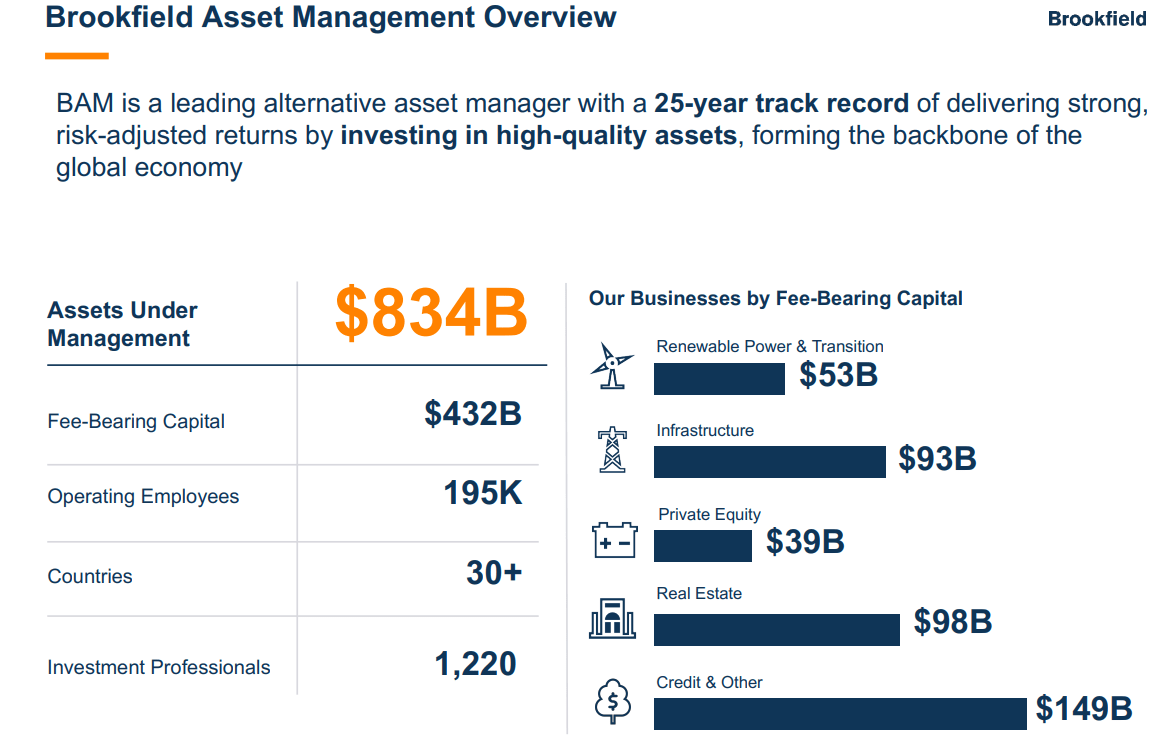

Since then BAM has grown to become the 2nd largest alternative asset manager in the world, right behind Blackstone in terms of assets under management.

- BX has $1.03 trillion in AUM

BAM's claim to fame is hard assets. It's how it started and where it thrives most.

In 2019, BAM bought Oaktree, home to Howard Marks, the Warren Buffett of credit markets. Oaktree and Brookfield are like Buffett and Munger working together at Berkshire. It's a match made in heaven and benefits investors immensely.

It's how BAM's largest growth market suddenly became private credit, a massive investable universe, paired with global infrastructure.

According to Boston Consulting Group and Brookfield, the global infrastructure investment opportunity through 2050 is about $150 trillion and through 2100 about $390 trillion.

Guess how countries and companies are going to fund that? With private credit! Brookfield now has the two largest megatrends in history at its back to drive those incredible Buffett-like returns we'll talk about in a minute. Not just for a few years, but potentially for the next 20 to 30 years.

{kind=link}

I personally have no interest in owning Brookfield Corp ( BN ) but BAM because this is where all the magic happens. BAM owns all the publicly traded partnerships. It owns Oaktree, it owns the hedge funds.

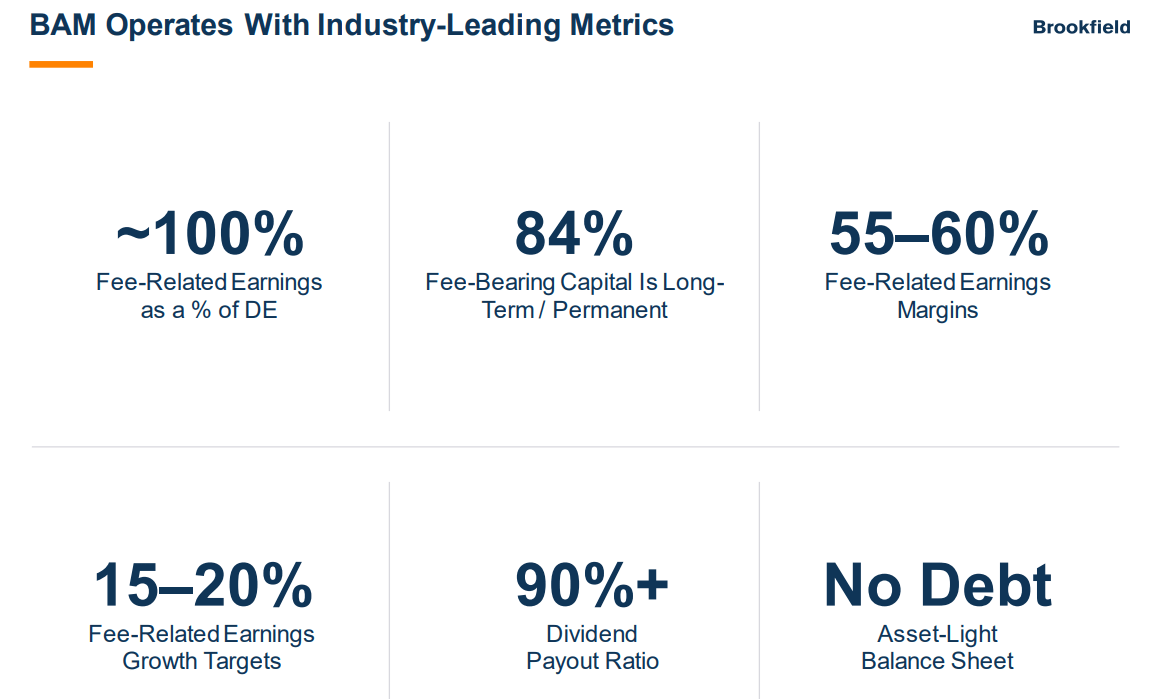

It's minting free cash at a 70% margin and paying out 90% of it as dividends that are expected to double every five years per the latest analyst consensus.

If you want legendary CEO Bruce Flatt and Howard Marks, two of the greatest investors in history, working for you, and paying you fat dividends? Then BAM is what you want.

{kind=link}

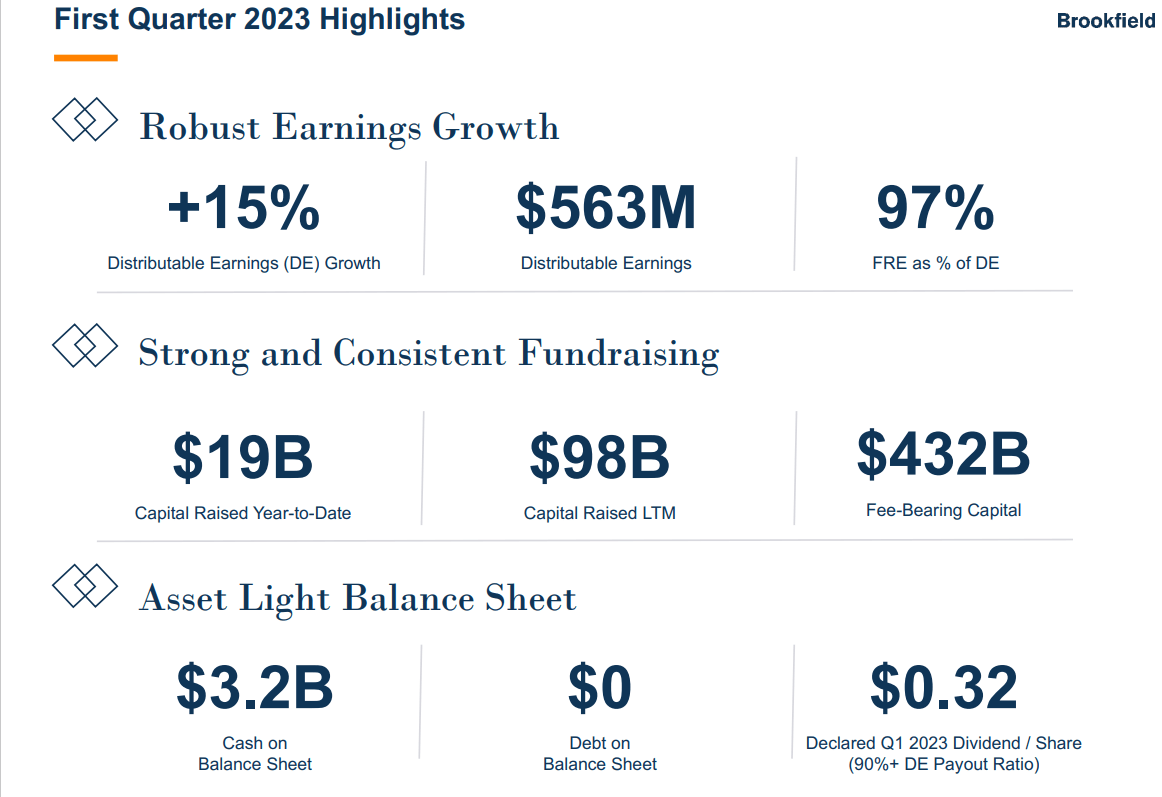

Just like management had been guiding for BAM grew distributable earnings by 15%. That's what analysts expected as well. How can management nail its numbers so consistently well? It's not because of some kind of accounting shenanigans like what GE was doing for a decade under Jack Welch.

It's because BAM has tens of billions in AUM already contracted for. They can call up their clients at any time and bring in those fee-bearing assets. For the next five years, BAM pretty much knows just how fast it is going to grow.

It's a lean, mean, money minting machine, with basically no capex and almost pure cash flow.

If I had $1 billion? I'd invest in BAM rather than its hedge funds. Because I can earn the same returns while having them pay me rather than the other way around.

Fortunately for the rest of us, enough big institutions do pay BAM attractive though not outrageous 2% and 20% fees that average 5% per year.

- BAM's fees work out to around 1.16% for the entire company

That's about compared to 0.66% for the average actively managed mutual fund and 0.22% for the average ETF.

So BAM gets to charge its clients 6X more than the ETF industry because of returns like these.

{kind=link}

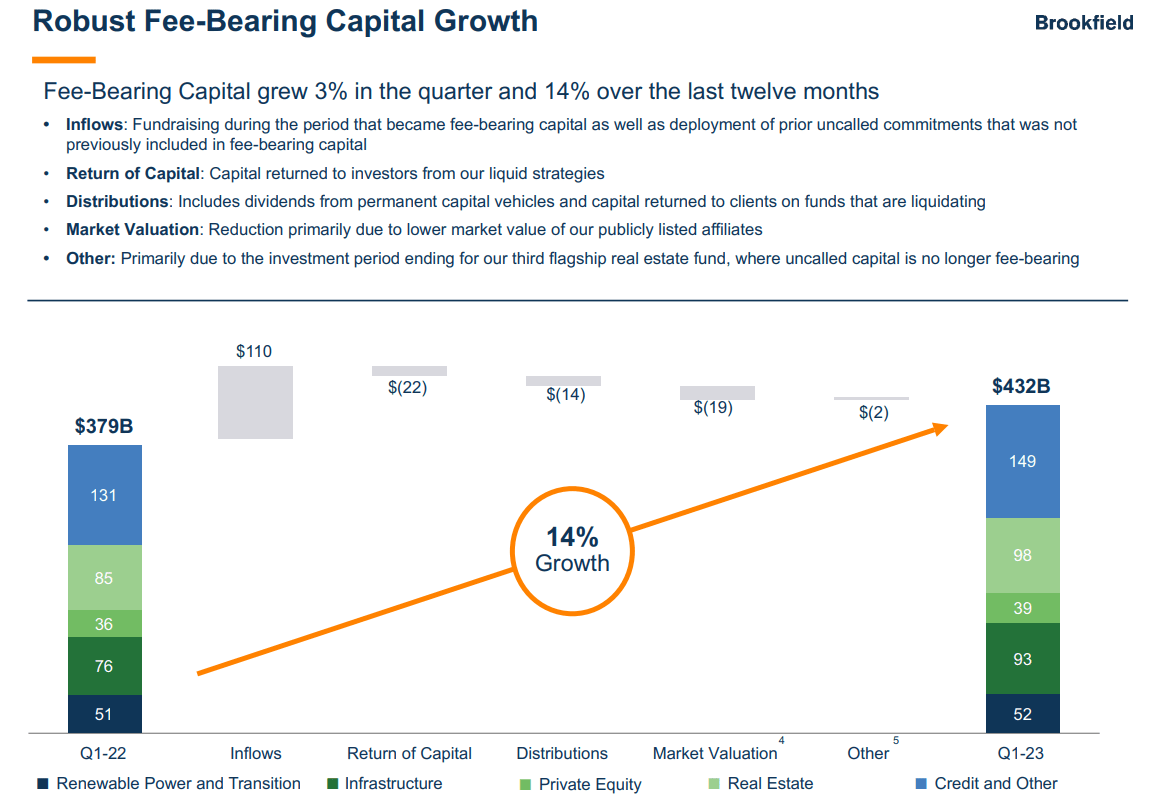

BAM was able to raise almost $20 billion in new capital this year and in the most recent quarter alone total inflows were $110 billion. So it's not just new money, it's old money giving BAM more to invest!

The world's richest institutions and families trust BAM to invest their money in non-stock related investments. In fact, it has about 1,000 major institutional clients. Think Saudi Arabia's sovereign wealth fund, Norway's pension fund, and the world's richest family home offices. Insurance companies, endowments, the so called "smart money" prove they are smart by giving their capital to the actual experts.

{kind=link}

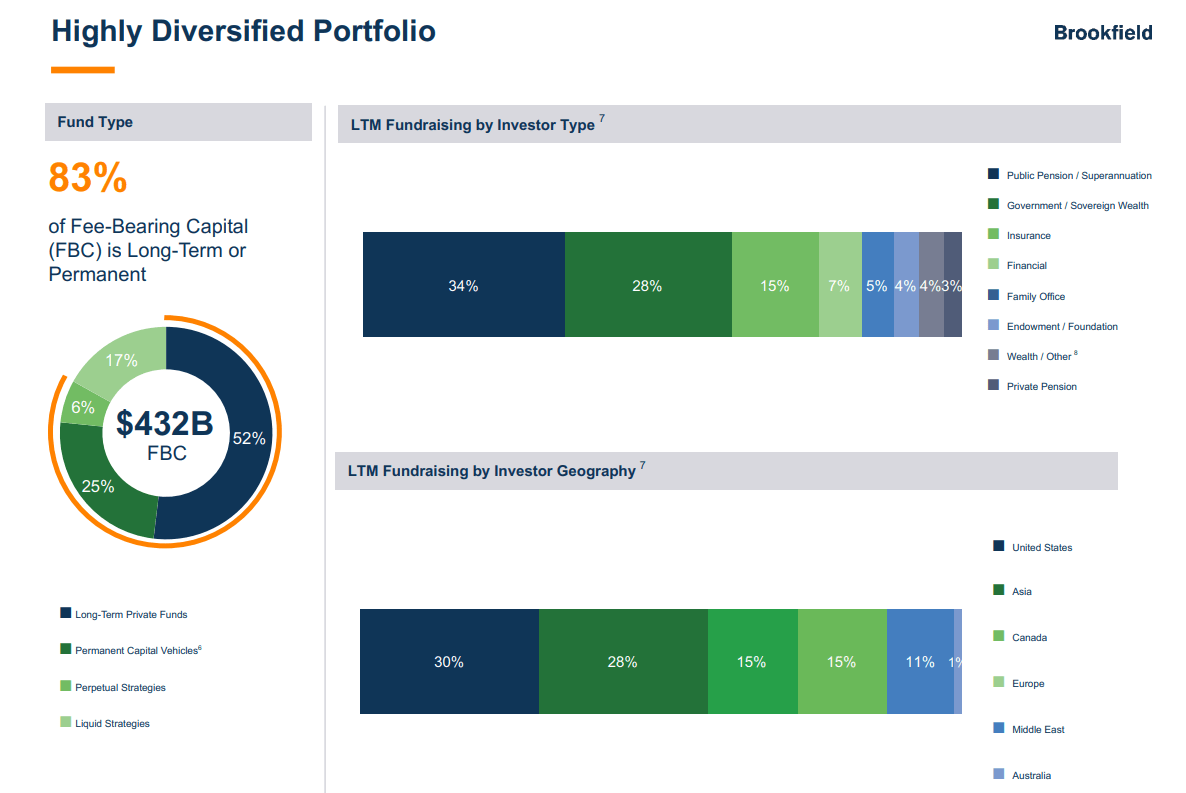

83% of fee-bearing capital is permanent or long-term and do you know why? Other than contractual lockup periods and gating? Because BAM has been delivering around 20% returns for investors for 40 years.

How many Berkshire investors are going to panic sell their shares if BRK has a bad quarter? Sells its airline stocks at the exact wrong time? How about sell IBM at basically breakeven after several years?

No investor is perfect, and no team of infrastructure investing or bond market geniuses will be either. BAM has earned the trust of 1,000 major financial institutions by proving it knows what it's doing across 40 years and

- four recessions

- two economic catastrophes

- six bear markets

- inflation as low as -3%

- inflation as high as 9%

- interest rates as low as 0%

- interest rates as high as 12%

Think Brookfield doesn't know how to handle whatever is coming next with the global economy? Unless you think the world of the future is going to be crazier than the world since 1902 with world wars, and killer pandemics wiping out 5% of humanity and a global great depression, I am pretty sure BAM can handle anything that's coming next.

{kind=link}

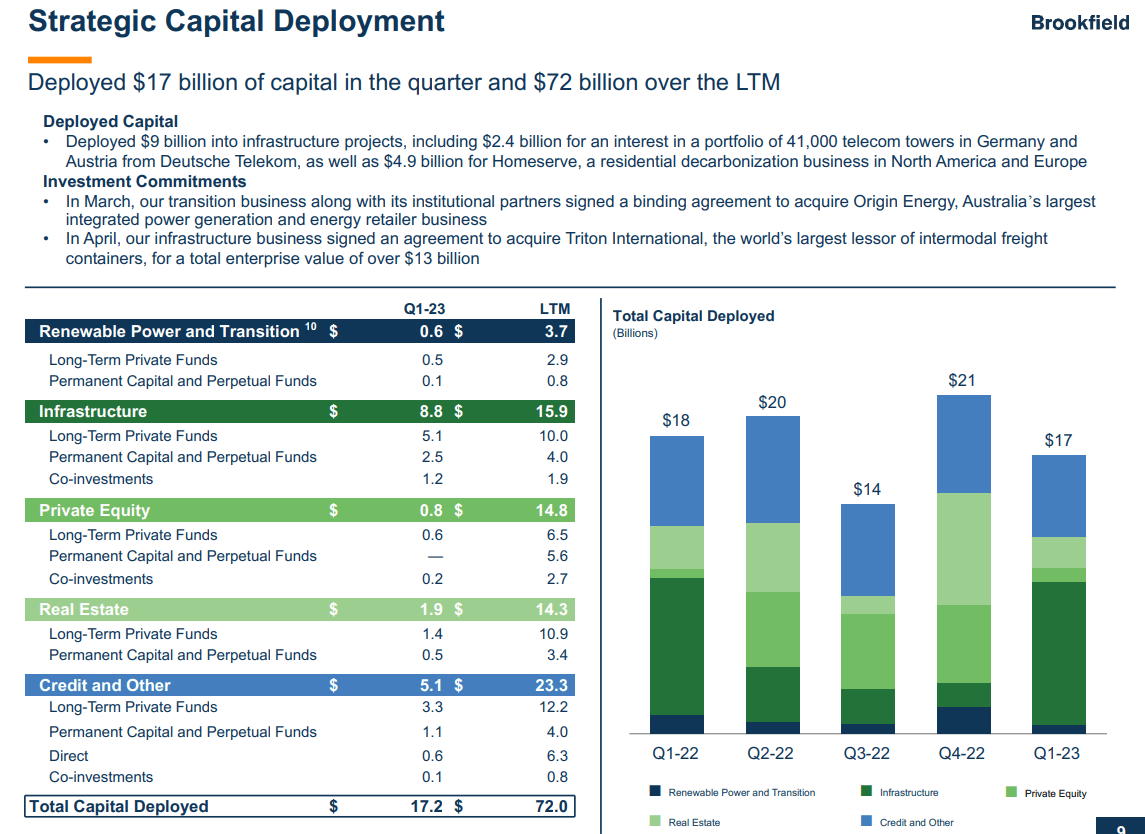

Are you confused about what to buy now? BAM isn't, it has put $72 billion to work in the first half of the year.

{kind=link}

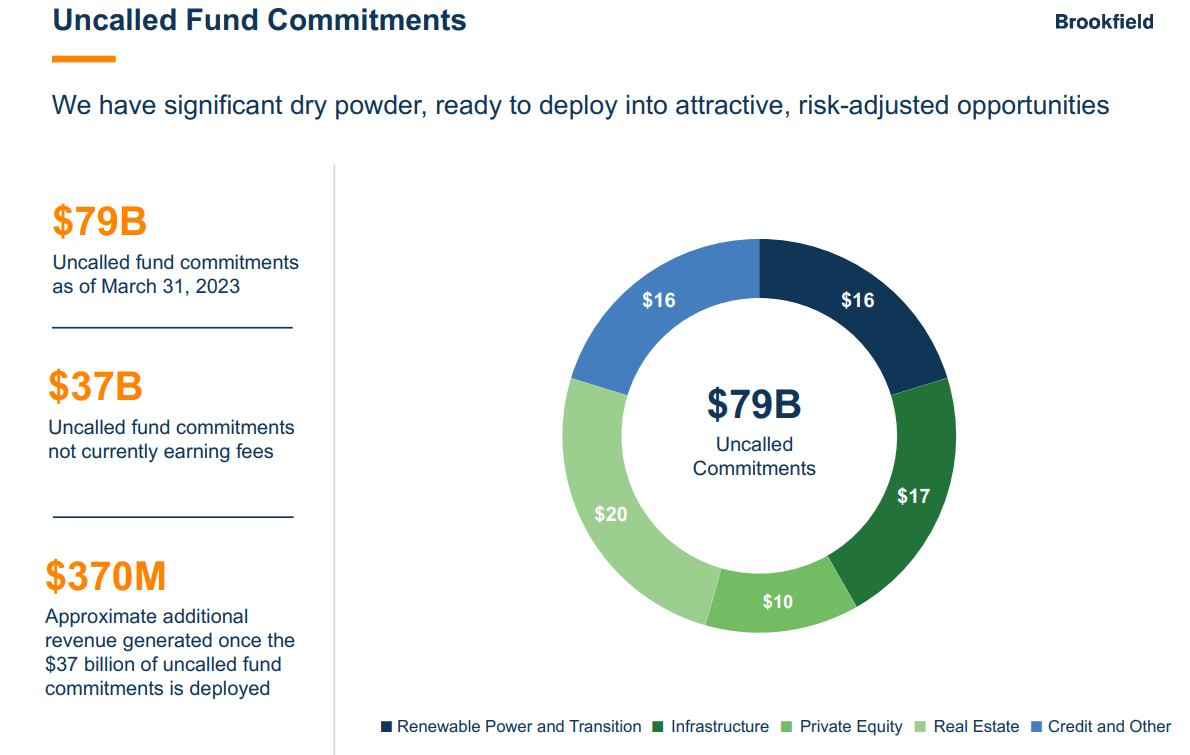

BAM can call its clients and within days get almost $80 billion in new funds under management if it has opportunities to invest in. On half of that uncalled funds BAM is earning fees and the part it's not represents another $370 million per year in sales. That means almost a 10% jump in revenue converting to 7% higher free cash flow just from calling in its commitments.

Spectacular Long-Term Growth Runaway

| Metric |

| 2022 Growth |

| 2023 Growth Consensus |

| 2024 Growth Consensus |

| 2025 Growth Consensus |

| Sales |

| 22% |

| 26% |

| 20% |

| 17% |

| Dividend |

| NA |

| NA |

| 14% |

| 15% |

| EPS |

| NA |

| 13% |

| 21% |

| 17% |

(Source: FAST Graphs, FactSet)

BAM is growing at a very respectable rate even in some pretty tough markets. That's to be expected since this isn't a stock based asset manager but one focused on alternative assets including specialized bond funds and private credit products.

When the market sucks like it does in 2022, BAM is a lot more resilient in terms of its fee based revenue than someone like TROW or BLK.

Furthermore, BAM's funds tend to be gated and have lockup periods, which is why its fee-based revenue is so annuity like.

{kind=link}

BAM is expected to grow 14% to 15% long-term which combined with a 3.9% yield means around 18% to 19% long-term return potential.

That's Buffett-like returns, from a company that has delivered 20% annual returns for the last 20 years. And whose management says they have a clear road to similar returns for the next 20 years.

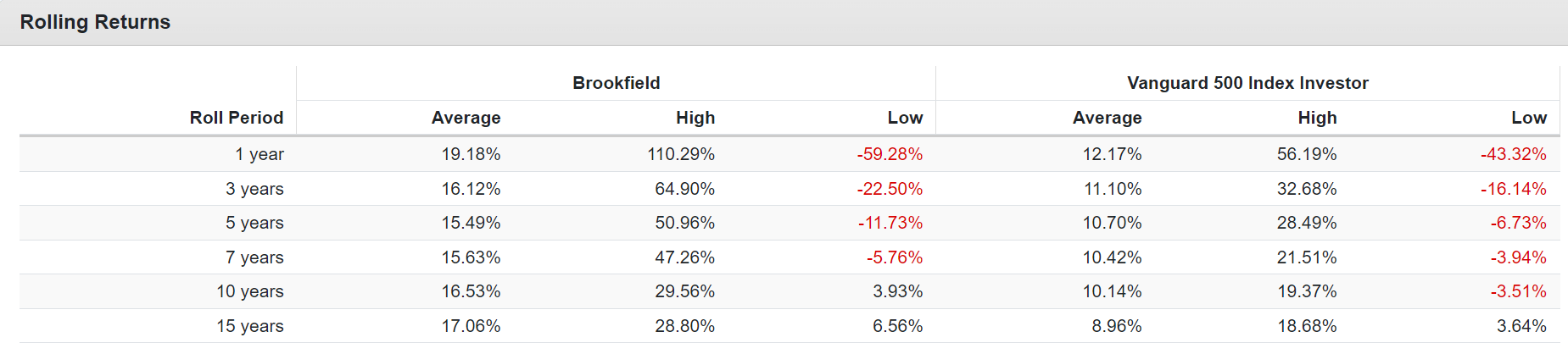

Rolling Returns Since 1985

{kind=link}

Buffett doubled the market for 58 years to become the GOAT.

Brookfield has doubled the market's returns for 40 years with a plan to get that to 60 years.

Brookfield, its CEO and corporate culture, is the Warren Buffett of alternative asset management.

Would you trust Berkshire with your life savings? Plenty of BRK investors already do. Well, that's how I feel about BAM. Everything about this company screams world-beater skill combined with the top integrity in the industry.

The Ultimate Buffett-Style Wonderful Company At A Fair Price

There is a bit of uncertainty surrounding BAM's fair value since this incarnation of the stock is just under a year old.

| Metric |

| Historical Fair Value Multiples (All Years) |

| 2022 |

| 2023 |

| 2024 |

| 2025 |

| 12-Month Forward Fair Value |

| 12-Month Forward Fair Value |

| PE |

| 24.50 |

| $28.67 |

| $32.59 |

| $38.47 |

| $44.59 |

| Average |

| $28.67 |

| $32.59 |

| $38.47 |

| $44.59 |

| $36.43 |

| $36.43 |

| Current Price |

| $33.31 |

| Discount To Fair Value |

| -16.20% |

| -2.22% |

| 13.40% |

| 25.30% |

| 8.56% |

| 8.56% |

| Upside To Fair Value (including dividend) |

| -13.94% |

| -2.18% |

| 15.48% |

| 33.86% |

| 13.21% |

| 13.21% |

| 2023 EPS |

| 2024 EPS |

| 2022 Weighted EPS |

| 2023 Weighted EPS |

| 12-Month Forward EPS |

| Historical Average Fair Value Forward PE |

| Current Forward PE |

| $1.33 |

| $1.57 |

| $0.46 |

| $1.03 |

| $1.49 |

| 24.5 |

| 22.4 |

However, the current historical PE corresponds to a 3.5% yield which I consider reasonable for a yield oriented growth investment that management says can deliver around 15% to 17% long-term growth.

| Rating |

| Margin Of Safety For low-Risk 11/13 SWAN |

| 2023 Fair Value Price |

| 2024 Fair Value Price |

| 12-Month Forward Fair Value |

| Potentially Reasonable Buy |

| 0% |

| $32.59 |

| $38.47 |

| $36.43 |

| Potentially Good Buy |

| 15% |

| $27.70 |

| $32.70 |

| $30.97 |

| Potentially Strong Buy |

| 25% |

| $24.44 |

| $28.85 |

| $27.32 |

| Potentially Very Strong Buy |

| 35% |

| $18.00 |

| $25.00 |

| $23.68 |

| Potentially Ultra-Value Buy |

| 45% |

| $17.92 |

| $21.16 |

| $20.04 |

| Currently |

| $33.31 |

| -2.22% |

| 13.40% |

| 8.56% |

| Upside To Fair Value (Including Dividends) |

| 1.67% |

| 19.32% |

| 13.21% |

BAM is a variable payer, like BX, and thus will never be more than a SWAN, and likely a more volatile one than most SWANs.

But for anyone comfortable with its risk profile and variable payout nature, BAM is a potentially reasonable buy right now.

Risk Profile: Why Brookfield Isn't Right For Everyone

There are no risk-free companies, and no company is right for everyone. You have to be comfortable with the fundamental risk profile.

BAM Risk Profile Summary

-

regulatory risk in the dozens of countries in which it operates (120 years of experience, the most of any asset manager)

-

interest rate risk (its projects are financed with non-recourse self-amortizing debt)

-

operating risk: if projects fail for any reason (such as drought hitting hydropower projects), then BAM "gives up the keys" to creditors, but cash flow for BAM would be reduced

-

M&A risk: Brookfield is frequently making acquisitions to expand its offerings (like insurance service in 2022)

-

currency risk: BAM operates all over the world.

How do we quantify, monitor, and track such a complex risk profile? By doing what big institutions do.

Long-Term Risk Management Analysis: How Large Institutions Measure Total Risk Management

DK uses S&P Global's global long-term risk-management ratings for our risk rating.

-

S&P has spent over 20 years perfecting its risk model...

-

...which is based on over 30 major risk categories, over 130 subcategories, and 1,000 individual metrics

-

50% of metrics are industry specific

-

this risk rating has been included in every credit rating for decades.

The DK risk rating is based on the global percentile of a company's risk management compared to 8,000 S&P-rated companies covering 90% of the world's market cap.

BAM scores 77th Percentile On Global Long-Term Risk Management

S&P's risk management scores factor in things like:

-

supply chain management

-

crisis management

-

cyber-security

-

privacy protection

-

efficiency

-

R&D efficiency

-

innovation management

-

labor relations

-

talent retention

-

worker training/skills improvement

-

occupational health & safety

-

customer relationship management

-

business ethics

-

climate strategy adaptation

-

sustainable agricultural practices

-

corporate governance

-

brand management.

BAM's Long-Term Risk Management Is The 171st Best In The Master List 66th Percentile In The Master List)

| Classification |

| S&P LT Risk-Management Global Percentile |

| Risk-Management Interpretation |

| Risk-Management Rating |

| BTI, ILMN, SIEGY, SPGI, WM, CI, CSCO, WMB, SAP, CL |

| 100 |

| Exceptional (Top 80 companies in the world) |

| Very Low Risk |

| Strong ESG Stocks |

| 86 |

| Very Good |

| Very Low Risk |

| Brookfield Asset Management |

| 77 |

| Good |

| Low Risk |

| Foreign Dividend Stocks |

| 77 |

| Good, Bordering On Very Good |

| Low Risk |

| Ultra SWANs |

| 74 |

| Good |

| Low Risk |

| Dividend Aristocrats |

| 67 |

| Above-Average (Bordering On Good) |

| Low Risk |

| Low Volatility Stocks |

| 65 |

| Above-Average |

| Low Risk |

| Master List average |

| 61 |

| Above-Average |

| Low Risk |

| Dividend Kings |

| 60 |

| Above-Average |

| Low Risk |

| Hyper-Growth stocks |

| 59 |

| Average, Bordering On Above-Average |

| Medium Risk |

| Dividend Champions |

| 55 |

| Average |

| Medium Risk |

| Monthly Dividend Stocks |

| 41 |

| Average |

| Medium Risk |

(Source: DK Research Terminal.)

BAM's risk-management consensus is in the top 34% of the world's best blue chips and is similar to:

-

Johnson & Johnson: Ultra SWAN dividend king

-

Federal Realty Investment Trust: Ultra SWAN dividend king

-

Illinois Tool Works: Ultra SWAN dividend aristocrat

-

Merck: Ultra SWAN

-

Texas Instruments: Ultra SWAN

-

McDonald's: Super SWAN dividend aristocrat.

The bottom line is that all companies have risks, and BAM is good at managing theirs, according to S&P.

How We Monitor BAM's Risk Profile

-

nine analysts (up from 5 on December 20th)

-

two credit rating agencies

-

11 experts who collectively know this business better than anyone other than management

When the facts change, I change my mind. What do you do, sir?"

- John Maynard Keynes.

There are no sacred cows for us. Wherever the fundamentals lead, we always follow. That's the essence of disciplined financial science, the math behind retiring rich and staying rich in retirement.

Bottom Line: Brookfield Asset Management Is My Favorite "Set And Forget Forever" Stock

{kind=link}

Here is all you really need to know about BAM. It's an industry leader, A-rated company and pays a safe 4% yield that's variable but expected to grow at 15% to 20% according to management.

4% yield + 15% to 20% growth = long-term returns that Buffett says he's not even trying to achieve anymore.

But BAM has achieved them for 40 years and says they can potentially deliver 20% returns for the next 20. And thanks to two megatrends that total over $500 trillion in addressable market by 2100, BAM can potentially deliver Buffett-like returns for longer than Buffett.

BAM might be the only one that can surpass Buffett as the GOAT. So that's why I want to invest alongside Bruce Flatt, and Howard Marks, the new Buffett and Munger.

There are many ways to define a set and forget buy and hold forever stock. But for me, it comes down to this.

For a single company that I had to trust for 20 years with complete trust, I would need a corporate culture and management team that is adaptable, skilled, and trustworthy.

I would need a company that is a leader in an industry with such strong megatrends at its back that the risk of a complete collapse in fundamentals was very low.

In the case of BAM, it's 0.66%, according to S&P, 4X lower risk than a nuclear war with Russia.

I would need a high-yield dividend growth stock that I can set on DRIP (dividend reinvestment plan) and be confident that the dividend will grow steadily and rapidly over time.

With Brookfield Asset Management, you get all of this and more. You get the ultimate Buffett-style "wonderful company at a fair price."

One that will adapt and overcome any challenges over the next 30 years. S&P is 99.4% confident that BAM will still be here in 30 years, and so am I.

So if I had to choose a single company, not an ETF or fund, but one single stock to trust with 100% of my life savings for the next 20 or even 30 years? I'd go with Brookfield, the king of global infrastructure and alternative assets.

Unless the world has ended in 30 years, I'm 80% certain (Templeton/Marks certainty limit) that you'll be happy you bought some BAM today.

For further details see:

Brookfield Asset Management: If I Could Own Just One Company This Would Be It