BAM - Brookfield Asset Management: Record Fundraising Likely In 2023

2023-08-10 05:34:54 ET

Summary

- Fundraising has picked up in Q2 and with the AEL deal done, management expects a record 2023 raise of $150 Billion.

- Between BAM and BN, Brookfield is my largest position.

- I present my updated thesis for my favorite asset manager.

Dear readers/followers,

I've written a number of articles on Brookfield here on Seeking Alpha: from the head of the empire - Brookfield Corporation ( BN ), through the ultimate dividend growth machine - Brookfield Asset Management ( BAM ), to its subsidiaries such as Brookfield Renewable Partners ( BEP ).

Depending on your strategy, each of these can represent a solid investment. Personally, I slightly prefer the corporation ((BN)), because I believe it's most undervalued and best aligned with management's interests, but I invest heavily in both BN and BAM.

And frankly, my conviction is high as between the two tickers, Brookfield represents my largest position at 10% of my portfolio.

With that said, the manager ((BAM)) seems to be more popular amongst investors, because of its easy to understand asset-light model which promises high growing dividends and very appealing upside potential over the next three to five years.

The company reported its Q2 2023 results today, which means it's time for an update to the investment thesis.

Alternative Asset Management 101

Before diving into the results, let me quickly recap what really matters for BAM's performance. As an asset manager, their business model is incredibly simple to analyze.

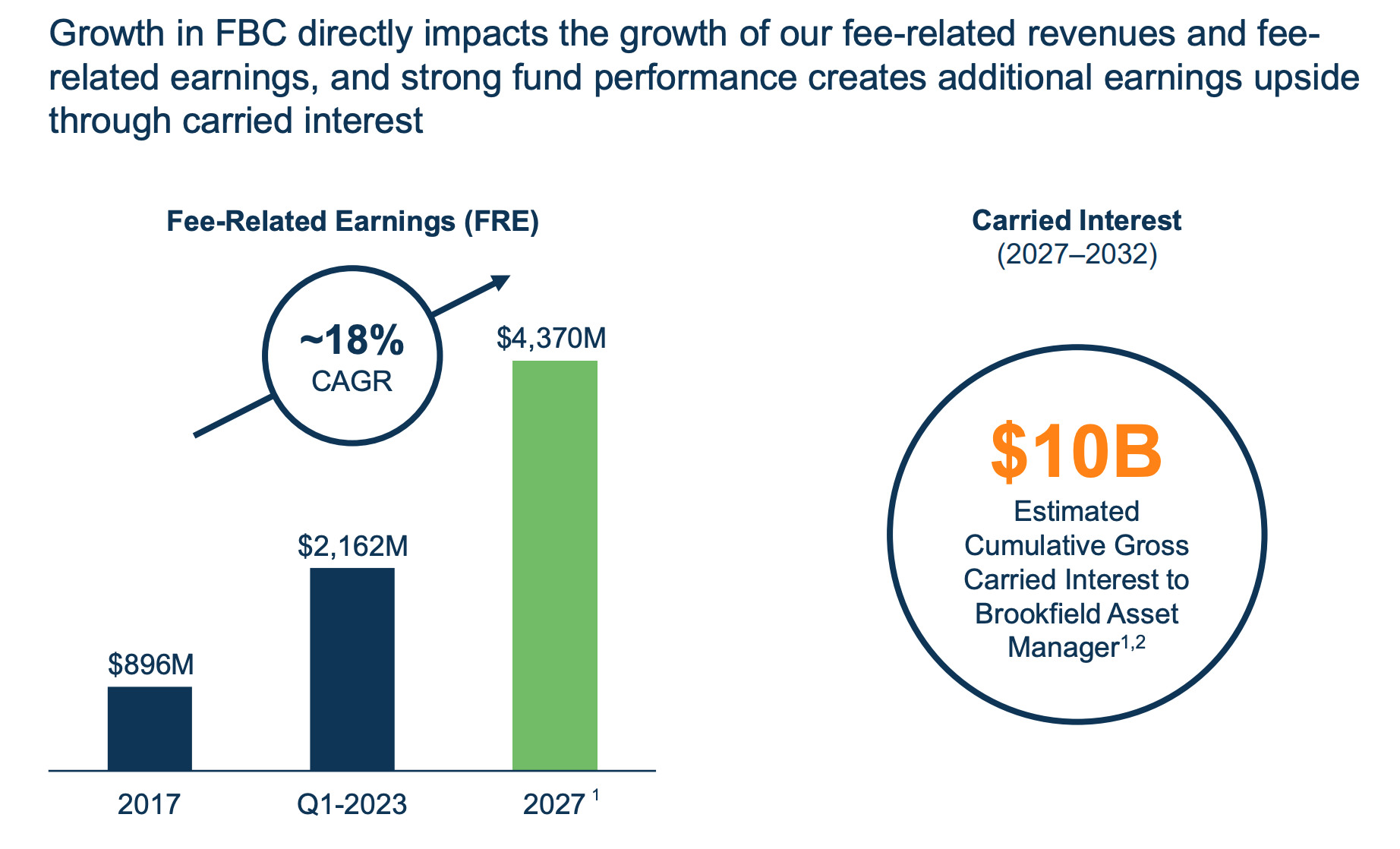

They get money from investors and charge about a 1% fee for investing the money into various projects and subsidiaries. After paying its overhead, Brookfield keeps about 55-60% of revenues in form of fee-related earnings (FRE). The vast majority of FRE (90%) is then distributed to shareholders as dividends.

On top of these fees, asset managers also earn performance related fees called carry . But because of its unpredictable nature, carry doesn't earn nearly as high valuation multiples as FRE and is therefore somewhat less important. In case of BAM, there will be no carry for the first five years, which makes valuation straightforward.

With this in mind, it's clear that the most important driver of BAM's performance is their ability to attract new capital. Of course, retaining existing capital is also important, but with 83%of capital invested in long-dated or perpetual strategies, growth tends to be mostly driven by inflows rather than outflows.

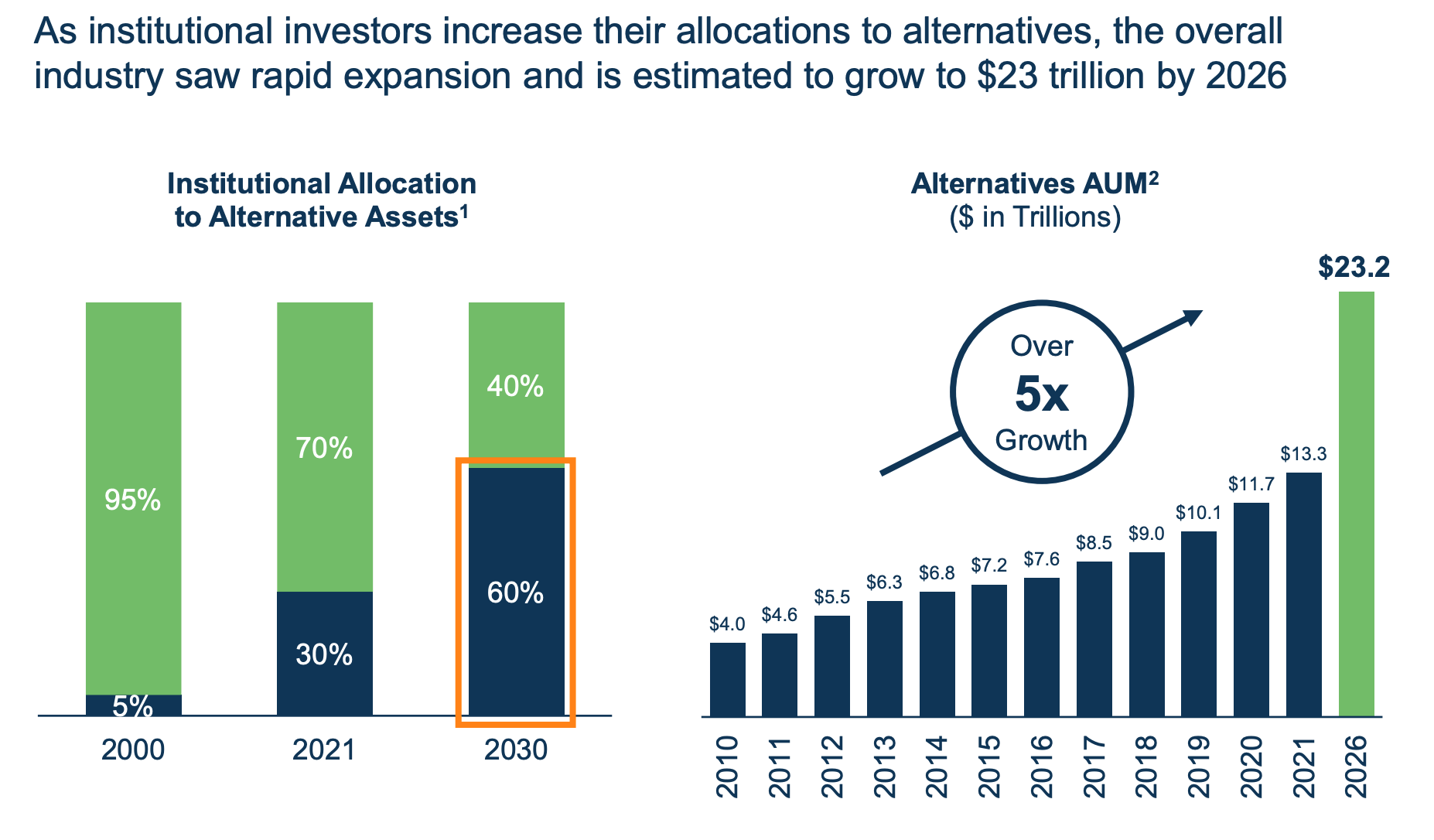

Therefore the ability to fundraise translates directly into AUM growth. And the thing is that the industry as a whole is expected to see major capital inflows over the next couple of years as institutional investors are expected to increase their allocations towards alternative assets.

{kind=link}

The asset management industry is competitive, but what's most important is size and reputation. According to Bruce Flatt , investors have become increasingly selective in today's uncertain market, which directly benefits Brookfield.

This makes sense, as institutional investors are unlikely to put their money with small unproven funds, which is why Brookfield is likely to grow its own AUM as least in proportion to the growth of the industry.

Consequently management is guiding towards a 15-20% growth in fee-related earnings for the next three to five years. That's impressive growth potential and with a very good track-record of over-delivering on their guidance, I'm excited to go over their recent results.

{kind=link}

Recent Results

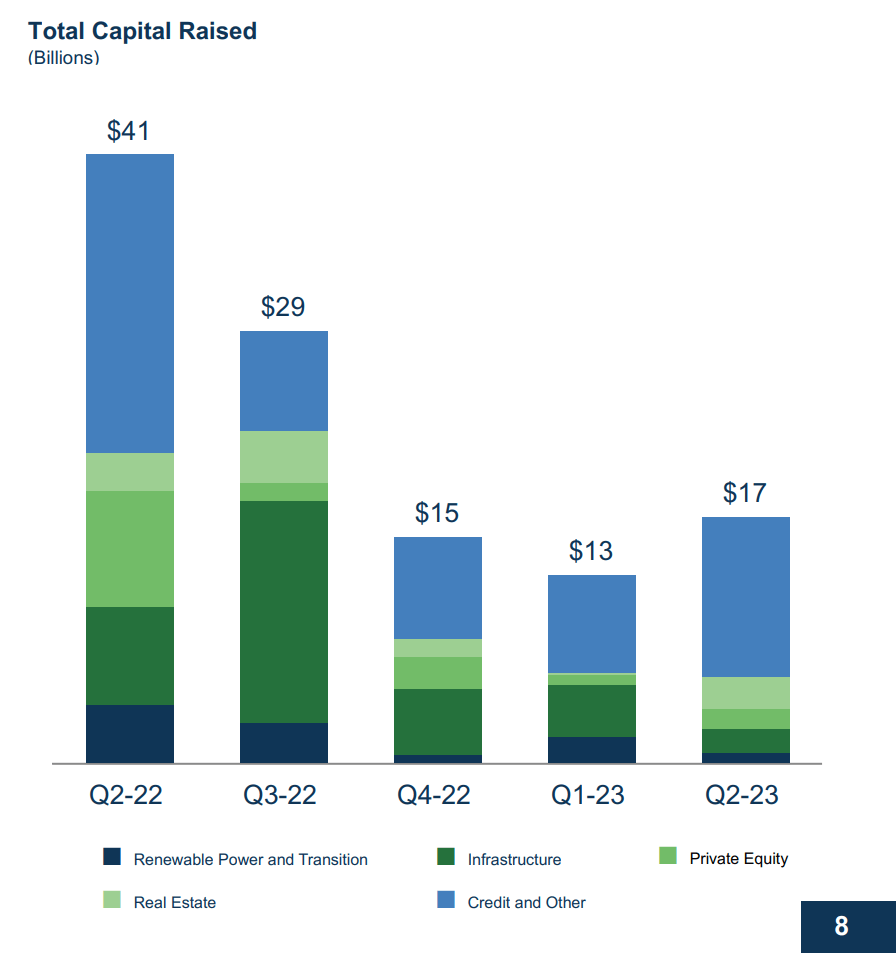

Fundraising over the second quarter has picked up to $17 Billion, primarily driven by private credit, which is very well positioned to take advantage of high interest rates and scarcity of capital. Year-to-date BAM has raised $37 Billion of private capital and reached assets under management of $850 Billion.

{kind=link}

In July, Brookfield Reinsurance ( BNRE ) announced a major deal which will significantly expand BAM's business. An agreement was made to acquire American Equity Investment Life Holding Company ( AEL ).

Once complete, the transaction is expected to bring $50 Billion of new capital to BAM, which will effectively triple its insurance business and bring an additional $125 Million in fee-related earnings annually. The transaction doesn't have an immediate positive effect on BAM, but will bring a lot of value over time.

On top of the already raised $37 Billion, plus $50 Billion from the AEL deal, management expects fundraising to accelerate in the second half of the year with an additional raise of around $65 Billion, for a record total annual raise of $150 Billion. I find that pretty astounding in the current economic environment.

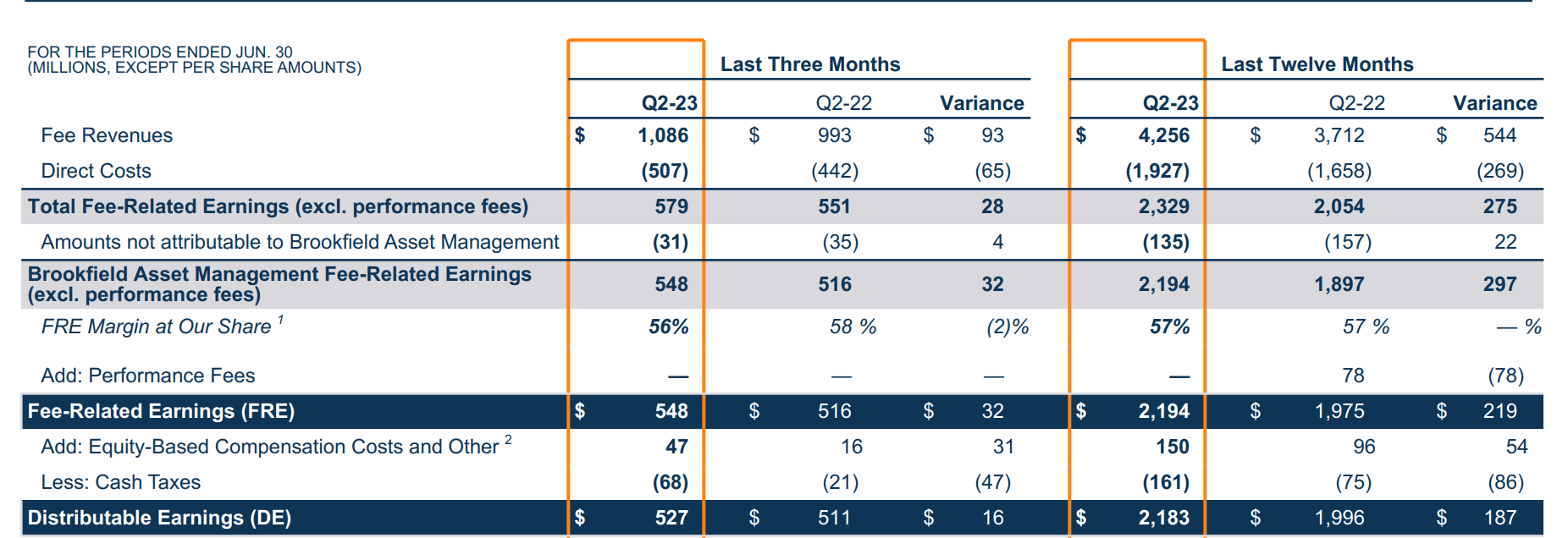

Year-over-year BAM has grown its fee-bearing AUM by 12% to $440 Billion has increased fee-related earnings by 6% YoY to $548 Million or $0.34 per share. Consequently, the board has announced a $0.32 per share dividend for the quarter which represents a 4% dividend yield and a 100% payout ratio relative to distributable earnings ((DE)).

{kind=link}

Going forward, BAM is very well positioned to continue to grow its management business by double-digits per year.

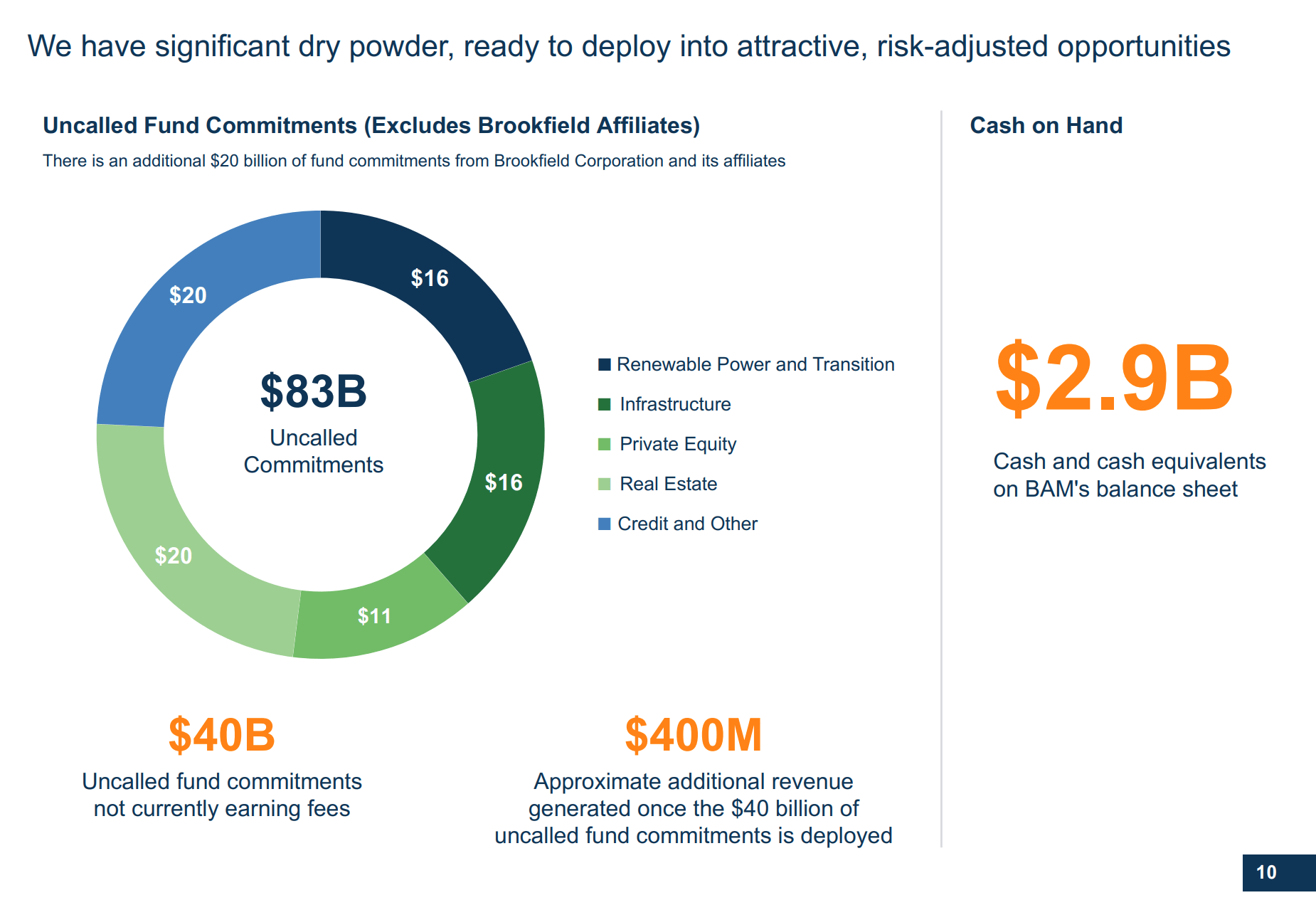

Not only do they have very high visibility on future capital raises due to their long-term relationships with clients, but they also have a lot of dry powder to take advantage of good deals when they come. In particular, BAM has $83 Billion in uncalled commitments, nearly $3 Billion of cash and no debt on its balance sheet.

{kind=link}

Valuation

If you look up BAM's market cap, you'll find $13.6 Billion. But keep in mind that only 25% of the manager is publicly traded, which means that the total market cap is 4x that ($55 Billion).

With annualized Q2 fee-related earnings of almost $2.2 Billion the stock trades at 25x FRE. This is below Blackstone's 28x FRE, but keep in mind that Blackstone also has some carry, which BAM doesn't. So in reality, I would say that both trade at a similar multiple relative to FRE.

Generally, a multiple of 20-25x or a 4% dividend yield is considered fair for asset managers, which means that while BAM is by no means cheap, it's priced around its fair value.

The real opportunity therefore lies in growth. If management delivers on their plan to grow fee-bearing capital by 15-20% per year for the next three to five years, dividends should grow at a similar pace and investors could enjoy total returns of around 20% per year for years to come.

I have no doubt that Bruce Flatt and his team will deliver, as they always have and I feel comfortable with my position. I see BAM as a BUY here at $33 per share, post Q2 earnings. What I find especially reassuring despite slower year-over-year FRE growth is their ability to fundraise, which of course will only translate into higher earnings later this year and next year.

Risks

As with any investment, there are risks. My thesis is, of course, predicated on the fact that management will be able to grow their AUM. I believe that recent fundraising, which has been pretty good despite tough economic conditions, provides evidence that management indeed knows what they're doing. Still, it's important to keep an eye on inflows and outflows periodically.

For further details see:

Brookfield Asset Management: Record Fundraising Likely In 2023