BAM - Brookfield: Attractive For The Long Term

2023-09-12 06:18:52 ET

Summary

- Brookfield engages in various sectors, focusing on areas with future value and the need for private capital.

- Concerns exist about Brookfield's real estate segment and its debt structure.

- The company has used non recourse debt to increase assets under management, but investors should consider financials and valuation using FFO.

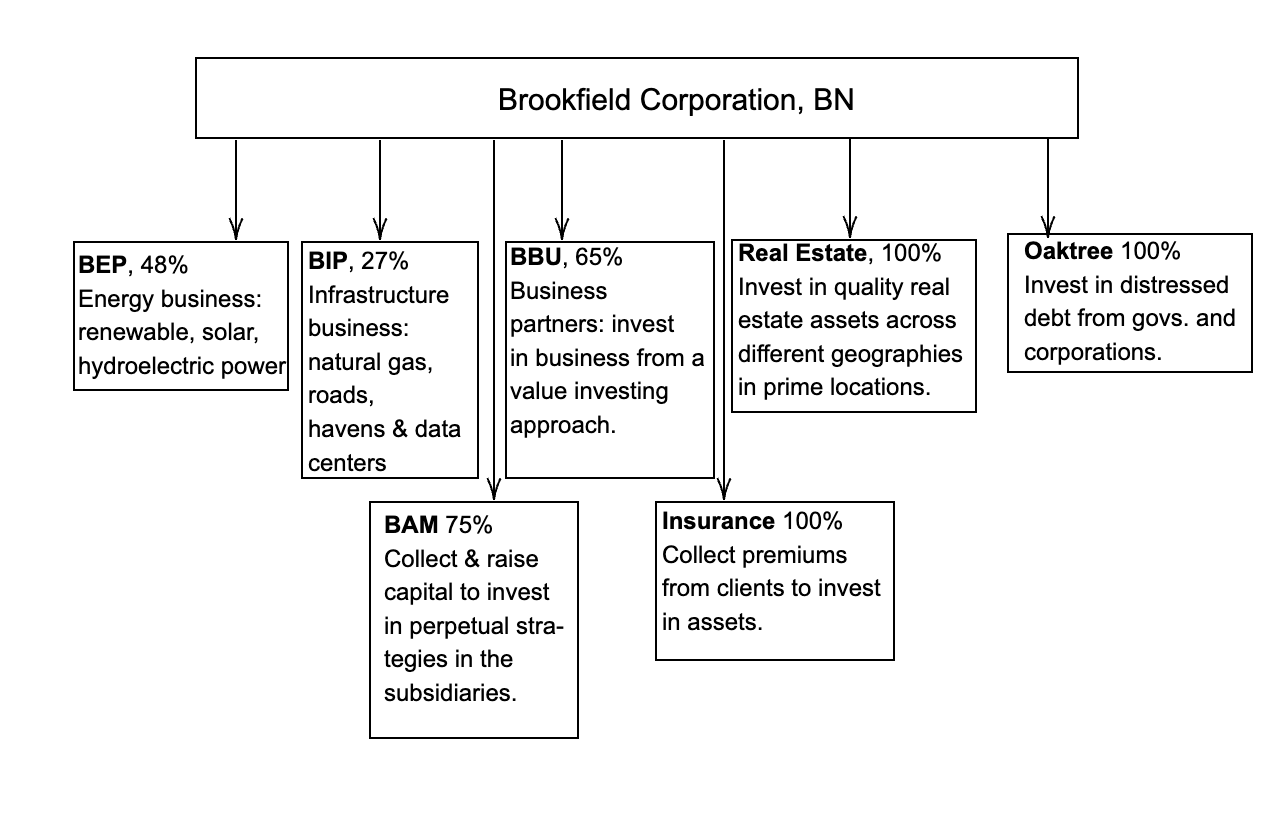

In the dynamic landscape of global investments, few entities stand as tall and diverse as Brookfield Corporation ( BN:CA , BAM:CA , BN , BAM ) and its subsidiaries. This multifaceted conglomerate has strategically positioned itself across various sectors, including energy production, business management, infrastructure operations, private equity, and real estate. In this article, we will delve into the nature of Brookfield's operations, revealing how they posses the power of long-term tailwinds to drive their growth and capitalize on global economic and environmental trends.

This text will provide an in-depth understanding of Brookfield's debt structure, financials, valuation, and the key segments within the corporation, offering a holistic view of its potential as a long-term investment option. Despite the complexities and inherent risks, Brookfield's history of value creation, prudent debt management, and its alignment with long-term trends make it a compelling prospect for investors with a horizon beyond a decade.

Company and long-term opportunities

Brookfield subsidiaries work on different segments including energy production, business management, infrastructure operations, private equity and real estate.

{kind=link}

The company has been strategically positioning itself in these segments to benefit from the following long term tailwinds, that are key for the long term thesis to remain intact.

Energy transition and decarbonization of the economy: the global shift towards renewable energy sources, such as wind, solar, and hydropower, is a significant tailwind for the corporation, especially for the energy subsidiary BEP. Increasing government incentives and corporate commitments to sustainability drive demand for clean energy, enhancing the value of BEP's renewable energy assets. In addition to this, other markets that may proliferate around energy transition are: electric vehicles, energy storage... New verticals that may further increase the value of Brookfield's investments in renewable energy.

Infrastructure challenges: governments around the world are increasingly recognizing the importance of infrastructure investment. Policies aimed at upgrading and expanding infrastructure, including transportation, utilities, and communication networks, can create opportunities for Brookfield to continue acquiring and operating these assets.

Global Real Estate : Brookfield's extensive real estate portfolio spans various asset classes and geographies. The long-term growth in global real estate markets provides opportunities for steady income and capital appreciation, as well as capital recycling strategy.

Low interest rates: even though interest rates have been rising to combat inflation, it is rare for them to rise to extraordinarily high levels due to: excessive government borrowing (an excessive rise in rates would increase the cost of debt and increase the tax burden on wealth producers) and the demographic structure of developed countries. In addition, persistently low interest rates favor investment in alternative assets due to the low profitability provided by traditional investment vehicles such as treasury bills or bank deposits.

These long-term tailwinds show that Brookfield Corporation is well-positioned to capitalize on global economic and environmental trends, making it an attractive investment option for those seeking exposure to alternative assets and long-term growth opportunities.

Debt structure

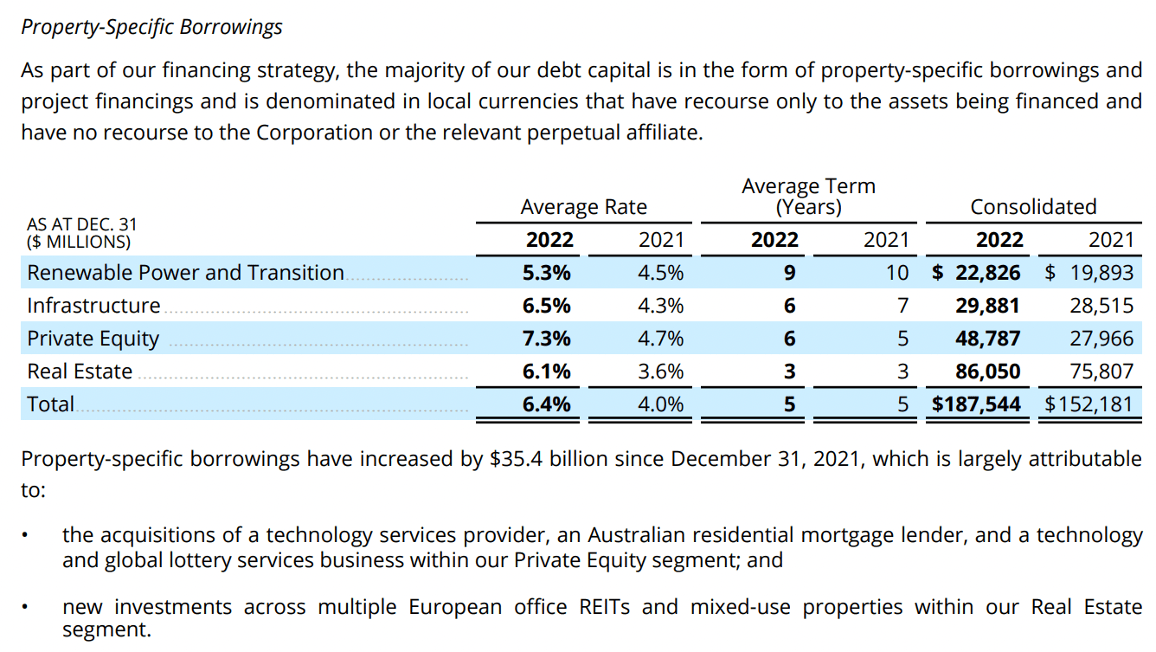

Investors are often misguided by Brookfield corporation and their debt. One of the key points that make the company different is how wisely the management team has used leverage in their favor. The secret ingredient that Brookfield has used to increase the assets under management and collect fees has been non recourse debt. Generally this type of leverage is a loan secured by a collateral, commonly high quality cash flow producing assets. If the Brookfield defaults, the issuer can seize the collateral but cannot seek out the corporation for any further compensation, even if the collateral does not cover the full value of the defaulted amount.

{kind=link}

The company currently has almost $200 billion in long term non-recourse debt with half of it at fixed rate and another half of it at variable rate. The current debt against the corporation stands at a level of $11 billion, while the subsidiaries borrowings stand at $15 billion, which again are not against the corporation.

The final benefits of this debt structuring are: limited liability (the assets of the corporation are protected), risk sharing between lender and borrower, higher amount of leverage (allows Brookfield to have access to assets other managers do not have) and asset protection. However, this normally comes at the cost of a higher interest rate due to the not beneficial position in which the lender is put. This is not a problem for Brookfield due to its strong financial position and its liquidity availability.

Financials and valuation

Within the Brookfield universe there are several concepts that acquire special importance and are key to understanding the evolution at a fundamental level of the business. In relation to the types of capital, there are normally two types: long-term capital and perpetual capital.

Asset management segment

The first one refers to all the own funds (put in by Brookfield and by institutional investors) to yield in a period of ten years. In general, they tend to follow capital recycling strategies: purchase of quality assets at a low price, optimization of the asset via increased yield on cost, and sale at a profit. One example of this is the sale of part of their US gas storage business where they generated gross proceeds of $235 million in a joint venture.

The latter refers to capital immobilized for a period of more than 10 years in unlisted assets. As in the previous case, Brookfield puts part of its capital together with institutional investors who are looking for real assets in which to achieve higher returns than in listed markets. These types of projects allow Brookfield to have a long-term vision in investing in assets with a longer time horizon than the rest of the market.

In general, this type of capital (both long-term and perpetual) is often known within the Brookfield world as fee bearing capital. Namely, it is a type of capital for which the management company charges to manage it in the private markets. As of December 31, 2022, Brookfield Corporation (within the Asset Management segment) managed more than $200 billion in long-term funds, $127 billion in perpetual funds and $71 billion in liquid strategies (credit and bond markets). This figure represents more than $400 billion of assets under management on which they have the ability to charge commissions and generate profits without any incremental cost.

One of the keys within the assets under management segment is that the capital base continues to increase in the coming years. I believe that this market will continue to expand in size in the coming years due to a series of structural points that I list below: institutional search for profitability outside of traditional assets such as fixed income due to persistent and growing inflation in the long term, the need for infrastructure renovation and commitment to the energy transition via more renewable power installed.

This segment is currently generating fees coming from managing capital that amounted to $4 billion in 2022. The only costs associated to this kind of niche are the ones regarding personnel costs, this is, people working within Brookfield that are actively looking for deals in all the verticals in which they operate. If we subtract the fee related earnings not attributable to the corporation plus cash taxes and other expenses we end up in an operating FFO of $1.9 billion in the same period or, equivalently, an FFO margin of 47.5%.

Operating segments

Within this category we include the aforementioned divisions which operate as different arms of the corporation: renewable segment, infrastructure segment, business partners, real estate and insurance. For each of the business we will determine its FFO, estimations for the coming year and a fair valuation using the next year estimated earnings.

For the valuation I have performed a simple model based on future estimates to determine the FFO yield at which the company is trading. I have estimated that growth in FFO in the energy segment will be around 10%, as well as in infrastructure, since most of the contracts are inflation linked and can increase the fees of the services they provide. With regard to the segments of private equity and real estate, I have not been that optimistic. Real estate assets will most likely suffer, interest payments will increase and distributable earnings to shareholders will be reduced. This is the reason why I have estimated that growth of FFO in this segment will be around -10% while for BBU it will remain flat.

Final valuation

Combining the assumptions that we have previously made for the asset management segment and the operating segments, we arrive to the following valuation of Brookfield Corporation, as can be seen in the Figure below.

BN: valuation (Own Models)

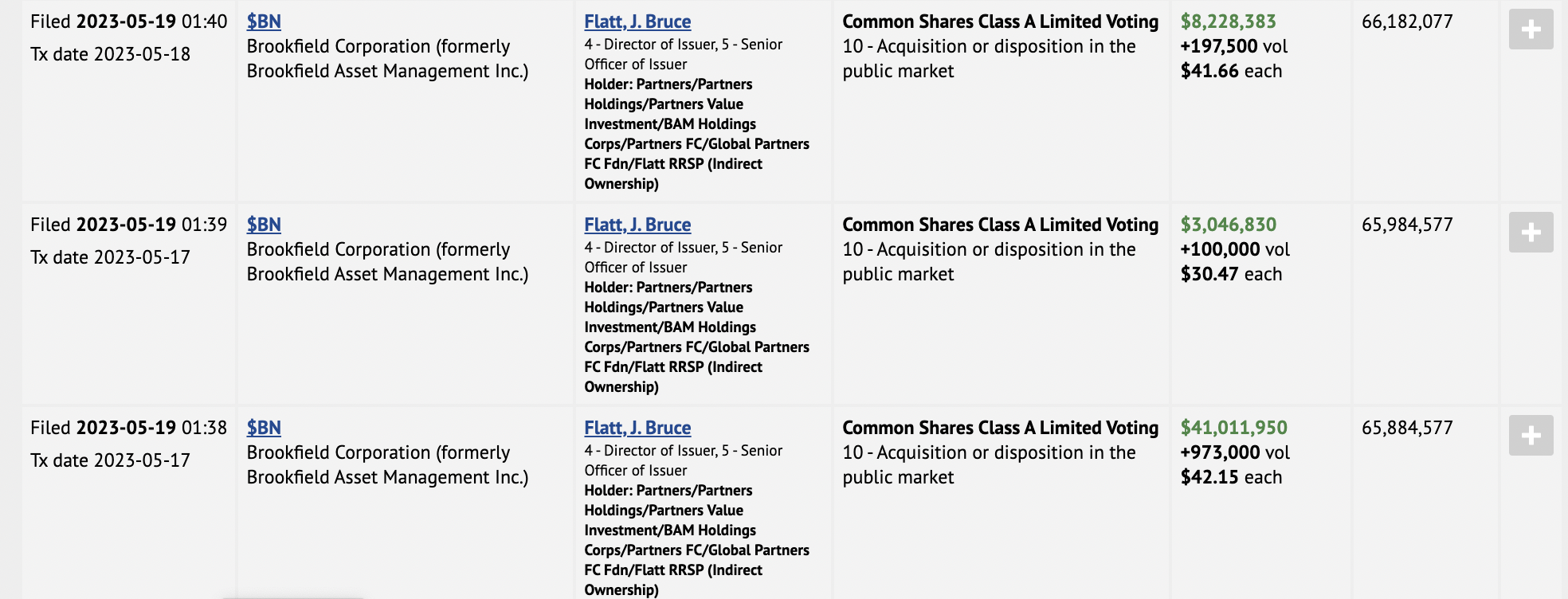

An initial valuation of 9% FFO yield combined with the latter's growth capacity offer a very attractive opportunity compared to how the risk-free asset against which all equity investments are compared is trading. Unlike other companies in the market, Brookfield has an undeniable history of generating value as well as a fully aligned management team that has always been focused on generating value through all corporate operations. CEO Bruce Flatt's alignment is complete, he is currently worth $2.2 billion and has been increasing his position in Brookfield in the recent declines in the stock

{kind=link}

Risks

Even though this article is bullish on Brookfield and firmly believes in the long term value generation that will be produced in the coming years, this is not an obstacle to indicate that the holding of shares of Brookfield is not free of risk.

One of the first barriers that keep investors away from investing in Brookfield is its extreme complexity at the level of subsidiaries and operating activities. One way to mitigate this risk is a direct exposure to the shares of the manager ( BAM:CA , BAM ) without participation in the rest of the corporation's businesses. Another of the risks that the reader must understand is that Brookfield uses a lot of leverage in the development of its operating activities. Although this practice may seem risky a priori, used wisely it can release a large amount of value over long periods of time. Brookfield is aware of this and has used non-recourse debt against assets and not against the corporation. Another way through which Brookfield has reduced risk is via mixed debt issuance programs: combining fixed rates with variable rates. On fixed-rate debt, the average rate over the last two years was 4.7%, with a total amount of $78 billion. Regarding variable rate debt, the average rate that pays has increased from 3.5% to 7.0%, with the total amount increasing more than $30 billion, exceeding $135 billion in variable rate debt.

The highest increases in debt have occurred in the private equity and real estate sectors, and particularly in the latter with more intensity. Throughout the last few months, a significant part of the Brookfield portfolio has been under the scrutiny of investors due to bankruptcies and defaults on office buildings that were taking place in many parts of the US geography. In relation to this issue, it is important to tone down the pessimistic tone of the press and realize that the Brookfield portfolio has been under construction for more than 30 years. Throughout this period of time, the company has cautiously selected high-quality properties in the office, retail, housing and science & technology categories. This sectoral diversification, combined also with international diversification, exposes the company to different economies with heterogeneous economic trends that reduce the risk of bankruptcy for the portfolio as a whole. In the words of Bruce Flatt, CEO of Brookfield :

I'll say just that it is worth emphasizing that the real estate business that we have built, over the last 40 years is focused on owning the highest quality assets in all categories.

On top of this, and maybe most importantly, our vast capital resources and highly diversified global business always allows us to emerge from a downturn in a more dominant and powerful position. Sudbury, specifically, single industry participants just do not have the resources that we have, and therefore, the opportunities come to us. So, while others in this environment possibly are having to be more defensive, we are looking ahead to what could be a significant opportunity to acquire great real estate at fractions of long-term intrinsic value where some do not have the staying power.

In short, Brookfield is a company present in verticals benefiting from long-term trends, with solid fundamentals, debt used wisely for the acquisition of strategic assets and that has a management team that has demonstrated its ability to generate value for its customers. long-term shareholders. At the current price, I think it could be an interesting option to incorporate for investors with a time horizon of more than 10 years.

For further details see:

Brookfield: Attractive For The Long Term