BBU - Brookfield Business Partners: Can't Fight The Fed

2023-03-28 06:18:54 ET

Summary

- Brookfield Business Partners is a company whose business model is heavily impacted by the actions of the Federal Reserve.

- Creating a high interest rate environment has disrupted the performance of the company.

- Now it's getting more expensive to borrow capital to make deals, and for it to sell its businesses to others for the same reason.

- It appears the company is going to remain under downward pressure until there's more clarity on interest rate policies over the long term.

Brookfield Business Partners L.P. ( BBU ) has been a frustration for management and shareholders because they believe the market is undervaluing the company.

Not long after it went public in 2016 it began an upward move from approximately $13.00 per share in August 2026, to about $30.00 per share in October 2018.

From there it fell back to around $19.50 per share before making another run in January 2019 and tested the $30.00 per share mark again in February 2020, before collapsing to approximately $12.00 per share in March 2020.

After hitting that low it began another prolonged upward move, soaring to almost $40.00 per share on November 8, 2021, before once again plummeting in price, dropping to its 52-week low of $15.29 on December 19, 2022. Since then it remains volatile, jumping to about $22.00 per share before pulling back to $16.55 as I write.

Based upon the business model of BBU, which is to acquire, improve upon, and sell businesses, it's operating in as bad as an economic environment as it could with the Federal Reserve increasing interest rates to fight inflation.

That has resulted in elevated costs associated with paying down debt, an increase in the cost of capital to make acquisitions, and hesitancy of companies looking for acquisitions to make them in the current high-interest-rate environment.

In this article we'll look at the probable ongoing negative impact of Federal Reserve policies on the company, its rising interest rate payments, selling off of Westinghouse, and the long-term outlook going forward.

{kind=link}

Federal Reserve impact

As mentioned in my opening remarks, the main headwind BBU faces at this time is the impact of the policies of the Federal Reserve on its business model. All of it is centered around the rising cost of capital and servicing its increasing debt level.

Along with that, it makes it harder to attract interest from companies looking to make acquisitions from BBU because of the same high interest rates that make them more expensive.

With the Fed remaining committed to bring inflation down to 2 percent or lower, the high interest rate environment is going to remain in play for the foreseeable future; it's not going to go away anytime soon.

The implications of this are obvious in regard to buying, selling, and investing in existing businesses. The primary end result is the elevated debt payments the company must make to service its debt. The main thing to take into consideration is the Federal Reserve has clearly stated it's not going to pivot in the near future and won't until its confirmed inflation is sustainably declining. That means even if the Fed were to stop raising interest rates, the impact of higher interest rates for longer is going to remain in play, which means the cost of capital is going to remain high.

The effect on BBU will be that it'll make doing business more expensive, and especially so since it's heavily reliant on leverage to execute on its business model.

I want to make it clear that this doesn't mean BBU can't or won't make deals, as evidenced by the upcoming divestiture of Westinghouse, and the fairly recent acquisition of CDK Global. The point is it's going to be more expensive and less attractive to make these deals, which suggests to me there's going to be fewer deals than has been in the past until the Fed does in fact pivot.

In its last earnings report BBU management said that the 25-basis point rate hike in January 2023 would add at least another $25.00 million or so to its existing $269.00 million in interest rate expense for the company, and possibly higher. Add to that another 25-basis point rate hike just announced by the Fed, and that should increase it by another $25.00 million in the quarters ahead. That would bring interest rate expense to about $300.00 million on a quarterly basis.

The company noted that the anticipated sale of Westinghouse in the second half of 2023 will help improve its debt structure.

At the end of calendar 2022 the company $1.6 billion in liquidity, which for now should be more than enough to see it through these difficult economic times, as far as the defensive side of doing business. On the offensive side of the business, i.e., taking steps to grow the company, I see it having less options until the Fed impact is resolved.

Profitability and growth

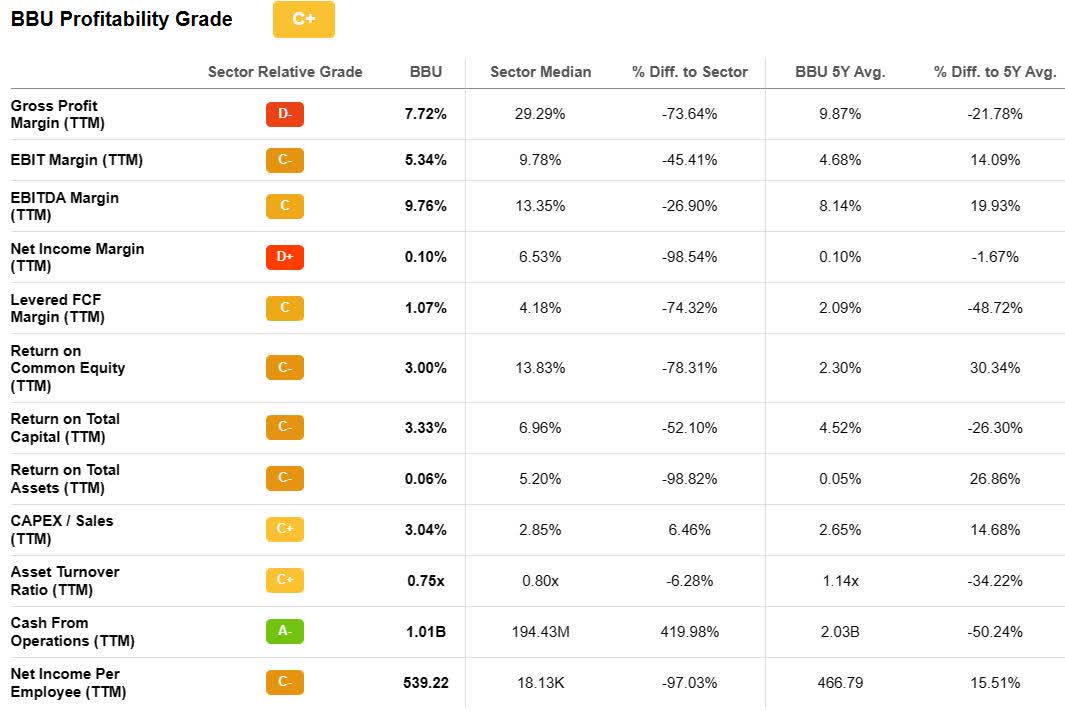

Profitability

In most profitability metrics BBU under performs the sector, starting with gross profit margin ((TTM)), which was 7.72, compared to the sector median of 29.29 percent, down by 73.64 percent.

EBITDA margin was 9.76 percent, compared to the sector median of 13.35 percent, lower by 26.90 percent.

Net income margin was only 0.10 percent, compared to the sector median of 6.53 percent, lower by 98.54 percent.

Return on equity was 3.00 percent, compared to the sector median of 13.83 percent, lower by 78.31 percent.

Return on capital was 3.33 percent, compared to the sector median of 6.96 percent, lower by 52.10 percent.

Return on assets was 0.06 percent, compared to the sector median of 5.20 percent, lower by 98.82 percent.

The one area where BBU shined was in cash from operations, which was $1.01 billion, compared to the sector median of $194.43 million, up by 419.98 percent.

{kind=link}

Seeking Alpha

Growth

As for growth , the company's revenue ((TTM)) came in at 23.52 percent, compared to the sector median of 15.10 percent, up by 55.73 percent. On the other hand, revenue growth ((FWD)) is -27.56 percent, compared to the sector median of 8.55 percent.

EBITDA (YoY) growth was similar in that it was 33.67 percent, compared to EBITDA ((FWD)) growth of 9.77 percent, basically in line with the sector median.

EPS (YoY) diluted growth was 85.48 percent, compared to the sector median of 14.78 percent. EPS ((FWD)) is 16.29 percent, compared to the sector median of 10.32 percent.

While over the last several years the company has improved its EBITDA and free cash flow, investors are looking at inflation, interest rates, and the actions of the Federal Reserve as the key metrics and elements to consider when determining the current value of the company.

Even though there has been some progress made, I don't see them as being discounted as measured against its current share price. My thought at this time is the company is trading at close to its real value based upon the current macro-economic conditions and weakness in many of the metrics affecting its bottom line.

As for its elevated input costs, the company hasn't done nearly as well as the sector in dealing with them and has to show it can remove more costs out of operations in the quarters ahead, if it wants to generate consistent and sustainable growth.

Conclusion

The business model of BBU is dependent upon low interest rates and liquidity within the debt markets to thrive. I believe it's going to get worse for the company before getting better, because of the current macro-economic environment and Fed policies.

The upcoming divestiture of Westinghouse will help the company, but that is probably already priced into the stock. Once the official date of the closing of the deal is released, it'll likely give a temporary boost to the stock, the level of which will be determined by how the economic outlook is at that time, as well as visibility on the actions of the Federal Reserve.

Also, if the company provides some compelling ways to deploy the capital after the sale of Westinghouse, it could be a tailwind for the company. I think it would be best to pay down debt and work on ways to cut expenses. That in itself would be like finding a new revenue stream that generates a profit.

My thesis is that BBU isn't undervalued, but valued at close to where it should be based upon its profitability metrics and expected slowdown in revenue growth. If things get worse in the second half as far as the economy goes, it could drop a lot further than where it is trading at today.

I see BBU as either a decent swing trade, or for those that believe it is undervalued, a stock that would probably best be invested in using a dollar-cost averaging strategy.

It appears to me the company has a much higher chance of falling further in 2023 than outperforming, and even with it trading at under $17.00 per share at this time, doesn't offer a compelling risk/reward scenario.

This is the type of stock that could get caught in a prolonged period of level growth and performance, which could result in investors having to wait for a long time to receive expected profits.

My view is there are a lot of stocks with far more growth potential than BBU for 2023, and why take the risk with the company when there are better risk/reward potential with other companies.

For further details see:

Brookfield Business Partners: Can't Fight The Fed