BBU - Brookfield Corporation Is Undervalued And So What

2023-05-28 04:50:21 ET

Summary

- BN keeps trading at a big discount from its SOTP value. The main cause of this discount is struggling real estate operations.

- BN investors are hopeful for big buybacks. They may or may not happen as there is intense competition for cash within the company.

- Using cash to grow asset management has the highest priority. Supporting insurance growth comes second. Whatever is left may be used for buybacks.

- BN investors should not be overly optimistic that the gap between the value and price will close quickly.

Several authors (including yours truly) have posted about Brookfield Corporation ( BN ) being undervalued. In this article, I am not going to challenge this thesis. Instead, I will argue that BN may remain undervalued for quite some time, and this is a risk for holders.

SOTP Value

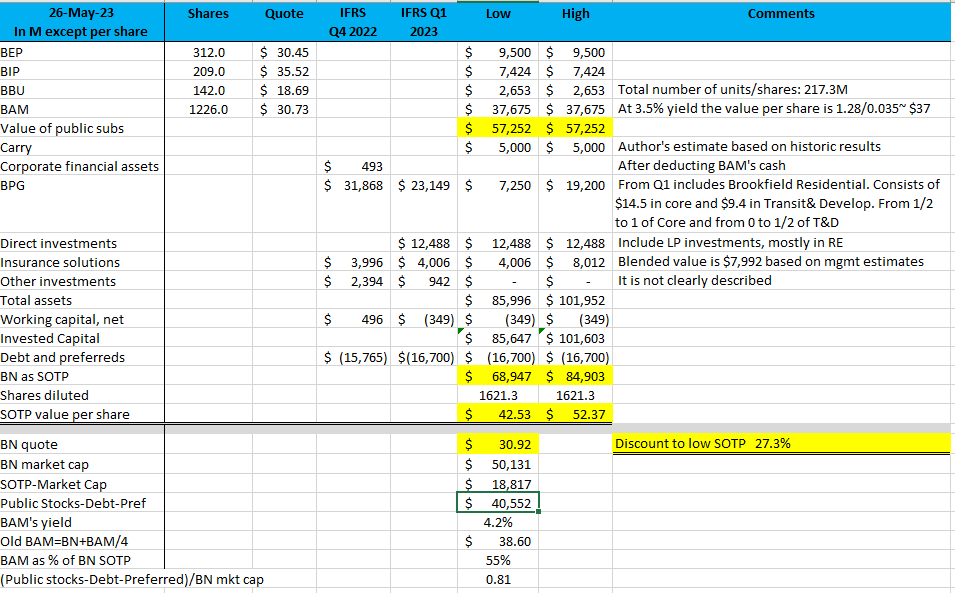

Since BN is a holding company, it is natural to use SOTP to value it. Here is my latest table for this method based on Q1 filings.

{kind=link}

Please note that in Q1, BN rearranged segments. BPG (Brookfield Property Group) now includes Brookfield Residential. A new line of Direct Investments includes BN interests in private funds (LP interests) that are mostly in Real Estate.

The changes attempt to present BN more favorably to investors but make it more difficult to figure out quarter-to-quarter changes.

Some entries in the table, such as publicly-traded subs or debt and preferreds do not leave any room for misinterpretation. Several others are too small to make a difference, and we should not be concerned with them.

I intentionally used an ultraconservative estimate for BPG value. At the low end, it is equal to half of the IFRS book value for core holdings (such as Brookfield Places and prime properties in NY, Toronto, Sydney, and London) with zero value assigned to the Transitional and Development (various malls, non-prime offices, and buildings in construction). One can hardly go lower.

I also have to comment on the insurance segment, even though it is still rather small. I valued it at its book value, Brookfield suggests it is worth two book values. The early results of insurance operations have been successful in terms of growth because of acquisitions and higher interest rates. When Brookfield negotiated the American National acquisition, bonds in the insurer's investment portfolio were producing little. With higher interest rates, Brookfield can reinvest the insurance float at better yields. There is nothing magic here, and it is too early to judge the ultimate success of insurance operations. I am optimistic about the insurance segment of Brookfield, but do not want to transfer my optimism into accounting. Let us give Brookfield 3-4 years before pricing the insurance segment more aggressively.

I also do not want to challenge the validity of valuing Direct Investments. First, we have no basis for questioning it, as we do not know what exactly is going on within Brookfield private funds and how they are marked to market. Secondly, Brookfield's private funds have been successful so far.

Now we are ready to address the important issues.

BN is persistently trading at a ~30% discount to its conservative SOTP. Why is it happening? Does Brookfield have the tools in its arsenal to narrow this discount? Can BN stock trade higher than the low thirties with or without narrowing the discount?

Cash Flows

Stocks can trade below their calculated values for a long time. Usually, management tries to talk up a stock price, hinting at the gap between the price and the value. Sometimes it works, but often it does not when investors do not see a specific way to unlock the value.

The latter case is well illustrated by the misfortunes of Brookfield Business Partners ( BBU ) ( BBUC ). The partnership is structured favorably for Brookfield and unfavorably for investors (please see my " Elusive cash of Brookfield Business Partners " for details). But despite this, the parts of BBU are worth far more than the partnership, no matter what method one uses to calculate its value. BBU buys back as many units as TSE allows, but it is still not sufficient and the value remains locked.

I am far from comparing BN with BBU, and invoked the latter only to illustrate that the value is not always unlocked by itself.

In general, the company can unlock its value by liquidating, going private, getting acquired, increasing dividends, and buying back shares. Everybody familiar with BN understands that only the last option is real. And this is precisely what Bruce Flatt mentioned in the Q4 22 letter to shareholders:

With a net asset value per share which we estimate to be vastly higher than our share price, we expect to continue to use our cash resources to repurchase shares in the market. If the discount persists, we will also consider other options, including a tender offer.

The letter was posted on Feb 9 when BN was trading at ~$37. During the next quarter, BN dropped to the low thirties (around $32) but Mr. Flatt's response was immaterial - net buybacks of ~$10M in Q1 23, negligible compared with the market cap of ~$50B. The language in the Q1 23 letter to shareholders was rather timid as well:

Given the current share price and our view of the intrinsic value of our business, we expect to continue to repurchase shares.

On paper, BN has strong distributable earnings ("DE") that can be used for share repurchases. In Q1, DE was more than $1B, so less than 1% was spent on buybacks. But only a fraction of DE can be used for buybacks, even in theory.

Company

The problem is that BN consumes a lot of cash to pay dividends and build out its operations, in particular insurance and asset management.

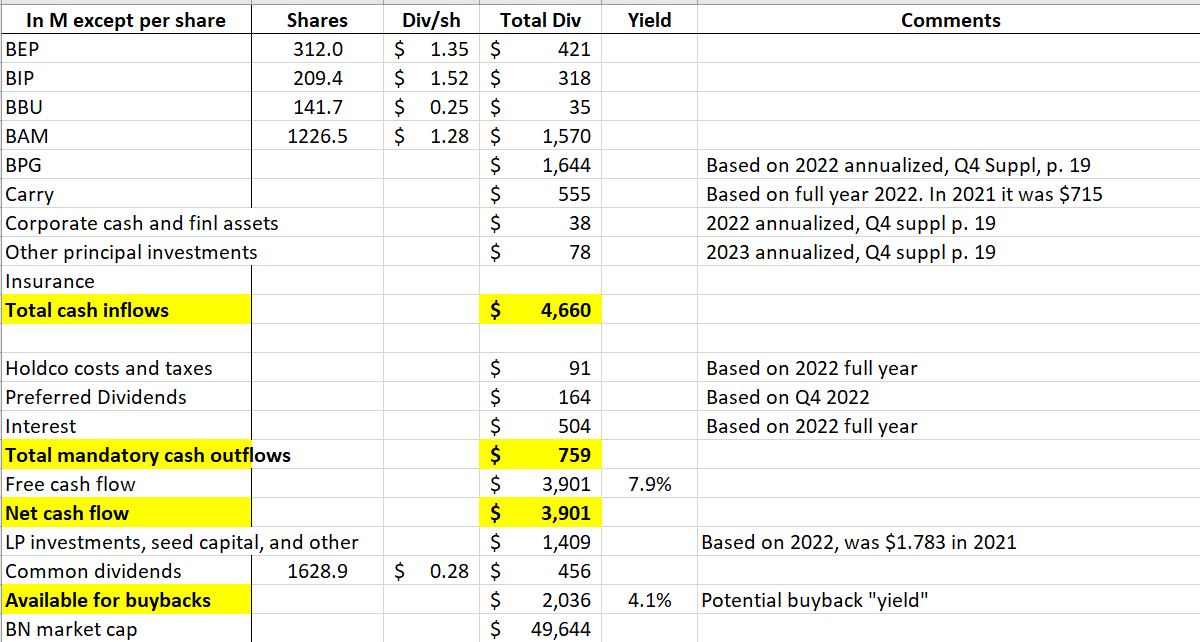

For this article, I built a table projecting BN cash flows in 2023. For some line items, I used actuals for 2022.

{kind=link}

Based on the table, at maximum, BN can repurchase about 4.1% of its shares at today's price. It implies spending close to $500M per quarter.

The biggest cash outflow item is supporting asset management operations (as a reminder: one-quarter of this business belongs to Brookfield Asset Management ( BAM )). The entry is called "LP investments, seed capital and other" - precisely what Brookfield calls it. It was $1.4B in 2022 and $1.8B in 2021. These cash outflows may seem discretionary, but they are not. Asset management is by far the best of Brookfield's business and the second-biggest cash supplier to BN, which is likely to become the biggest one.

But revealingly, asset management (I called the entry "BAM" in the table) consumes more cash than it delivers. This is the reason why I consider BAM a better investment compared with other asset-light alt managers. They do not receive such gifts from "third parties" but have to use their own cash for growth.

Secondly, the table above does not account for insurance acquisitions, and they are in billions. In 2023, Brookfield is expected to acquire Argo ( ARGO ) for more than $1B and most of this cash will come from BN in one form or another (in 2022, cash outlays for insurance were much larger, mostly due to American National acquisition). In general, the build-out of insurance will require plenty of cash from BN for many years. In supplemental filings, BAM lists insurance as a contributor to DE, but in reality, insurance consumes much more cash than it delivers. Accordingly, I left the entry for insurance cash inflows blank in the table.

Besides day-to-day operations, BN has two other sources of cash. It can issue additional debt and sell pieces of real estate. Debt is a double-edged sword, and I doubt BN will use it for buybacks. On the contrary, selling RE is precisely what BN wants to do but cannot under the current macro conditions.

On the last earnings call, Mr. Flatt and his colleagues spent a lot of time trying to depict a brighter picture for the real estate segment. Investors appear not convinced and BN keeps performing poorly.

BPY's preferred stocks (BPY is the old name for what is now called Brookfield Property Group) are trading at half of their par value. It shows how investors view the real estate segment and, in my opinion, proves that this segment is the main cause for BN's low price.

I do not share this extreme pessimism and may publish separately regarding these preferred stocks. If I am right, the situation in the real estate segment should gradually improve, which will be a major positive for BN stock. Under this scenario, the shares may recover even without major buybacks.

Conclusion

I have tried to show intense competition for cash within Brookfield Corporation. Despite a 30% gap (and probably more in case we are less cautious) between the conservative SOTP value and stock price, supporting asset management operations remains a priority. Supporting insurance operations comes second. Whatever is left may be used for buybacks.

This "whatever is left" fluctuates from quarter to quarter. In good quarters, I would still expect much higher buybacks than in Q1. However, based on cash flow analysis, buybacks will remain short of dramatic until strong progress in real estate is achieved. Carry may deliver substantial chunks of cash as well, but this requires big exits from old investments, which is unlikely under the current macro conditions. From the table, it follows that after adjusting for insurance investments ($1B for Argo) buybacks can reach a maximum of about $1B in 2023, but it excludes additional acquisitions by BN or higher investments in asset management. It represents about 2% of the shares outstanding.

Many investors cling to BN because of high insider ownership. This is understandable, but the biggest store of BN's value is BAM. BN invests plenty of cash to achieve BAM's growth, much more than it uses for buybacks. BAM's progress is the easiest and best way to affect BN's stock price, both in the medium and long term. Between these two and despite BN's low price, I would still bet on BAM.

If Brookfield keeps finding good uses of cash to grow asset management and insurance AND real estate keeps struggling, big buybacks may not follow. In this case, the gap between BN's value and stock price will not narrow. This is just one of the possible scenarios, but BN holders should not be overly optimistic.

For further details see:

Brookfield Corporation Is Undervalued And So What