BIPC - Brookfield Infrastructure 5.00% Preferred Units: 38% Discount To Stated Value Plus 8% Yield

Summary

- $72 billion-asset Brookfield Infrastructure owns and operates assets in the utility, transport, midstream and data sectors worldwide.

- The partnership's investments generate stable, largely inflation-linked cash flows that have increased FFO by 11% annually for a decade.

- Brookfield Infrastructure Partners LP 5.00% PFD provides a reasonable trade-off between risk and value for potential capital gains combined with an 8% current yield.

Brookfield Infrastructure Partners L.P. (BIP) has a complicated capital structure with “mirror-image” C-Corp shares (BIPC), seven different preferred securities and two “baby bonds” that trade on either the Toronto or New York Stock Exchange, not to mention numerous debt tranches. To limit the complexity, unless noted, we’ll be reviewing the partnership’s operations and financial statements on a consolidated basis without subtracting non-controlling interests and the interests of others in operating subsidiaries necessary to derive Brookfield Infrastructure’s proportionate share.

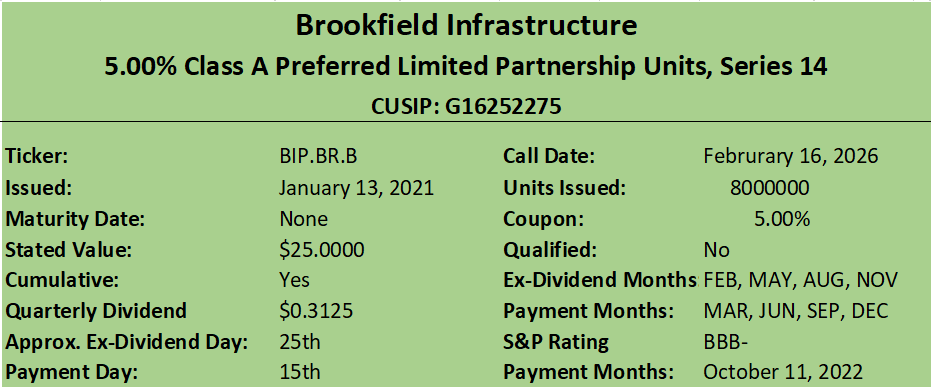

We’re going to discuss my personal favorite of the preferred units, referred to by most brokers as Brookfield Infrastructure Partners LP 5.00% PFD A 14 (NYSE: BIP.PR.B), sometimes BIP.PRB - not to be confused with BIP.PR.B Series 3 that trades on the TSX), but referred to in the Prospectus as Brookfield Infrastructure Partners L.P. 5.00% Class A Preferred Limited Partnership Units, Series 14. I am being pedantic as it’s easy to confuse Brookfield’s preferred units. And yes, they are units so if you don’t want a K-1 you can stop reading now. Please note that with average daily trading volume typically around 25,000 units, BIP.PR.B is often missing from stock research and analysis websites. Here’s some relevant information about the units:

Brookfield Infrastructure Partners L.P. 5.00% Class A Preferred Limited Partnership Units, Series 14 Prospectus

{kind=link}

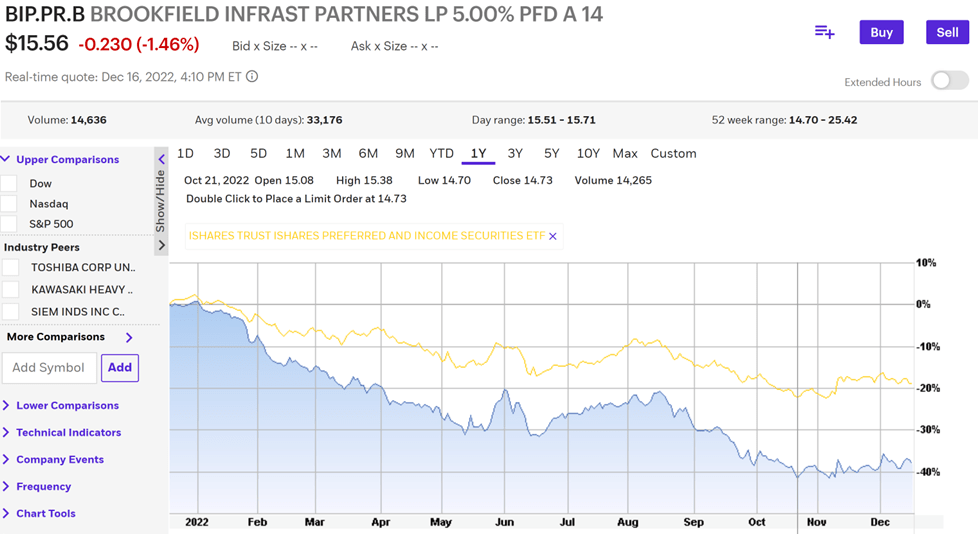

There are two obvious attractions to BIP.PR.B, now trading at $15.60 on December 19, 2022; 1) a hefty 38% discount to the $25.00 liquidation preference - and its previous trading range - plus 2) a 8.03% yield at that price. The discount to stated value is interesting in that the preferred units can be called at par on or after February 16, 2026. The chart below, courtesy of E*Trade, illustrates the unit’s precipitous decline over the past year compared to the iShares Preferred and Income Securities ETF.

{kind=link}

Essentially fixed-rate, a large part of the decline in both securities has resulted from the Fed’s tightening cycle, but, although the ETF is not a pure-play preferred vehicle, the units have suffered a decline of roughly 40% compared to the ETF’s 20%. Also notice in the chart above that the October 11, 2022 BBB- S&P rating had little impact on the price per unit. My opinion is that BIP.PR.B’s high yield is not merited by any underlying issues in the partnership’s business.

Business: A Global Infrastructure Partnership

$72 billion-asset Brookfield Infrastructure owns and operates assets in the utility, transport, midstream and data sectors across North and South America, Asia Pacific and Europe. It’s a partnership with Brookfield Asset Management (BAM) as the managing general partner with a 27.1% interest and Brookfield Infrastructure Partners as the limited partner with a 72.9% interest. The company also offers C-Corp shares which own part of the limited partnership for investors not wanting to deal with a K-1, but not for the preferred securities.

The partnership is one of the largest direct owners of infrastructure operating assets. Brookfield Infrastructure’s competition for investments is mainly 1) infrastructure mutual funds, although these primarily own stock in publicly-traded “infrastructure companies” like Siemens (SIEGY), Consolidated Edison ( ED ) or Waste Management ( WM ), and 2) private equity companies like Blackstone ( BX ) that own a mixture; investing directly in operating assets and the stock of infrastructure companies. An August 2021 paper in The Review of Financial Studies entitled Institutional Investors and Infrastructure Investing , identified 633 infrastructure funds holding a total of an estimated $500 billion in assets. By this account, Brookfield Infrastructure owns about 14.4% of all infrastructure fund assets.

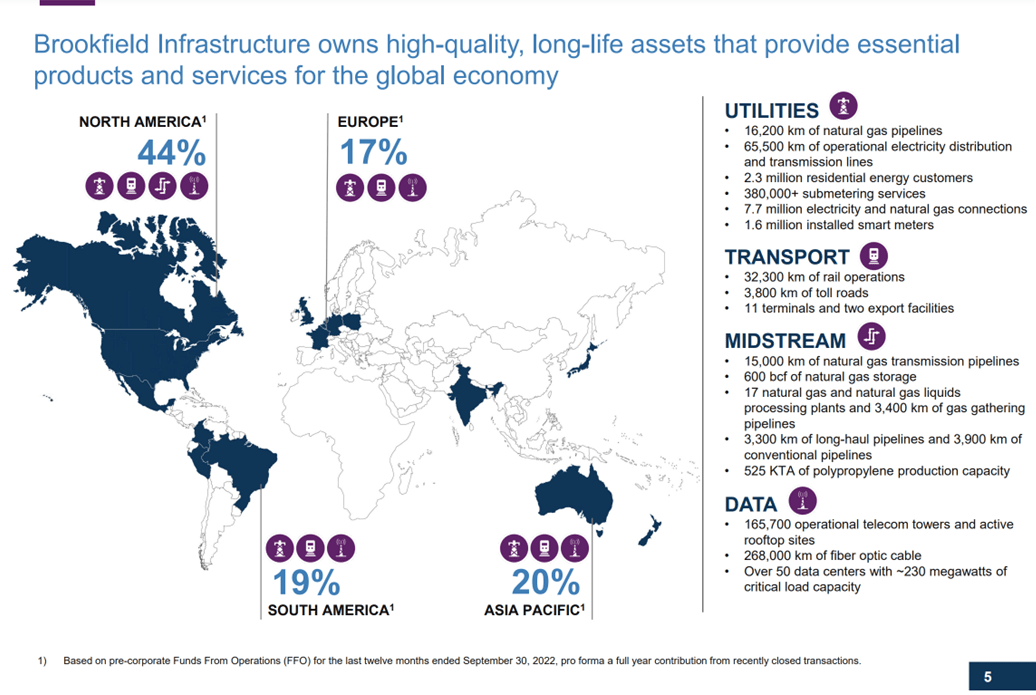

The partnership’s assets are split into four categories; 1) Utilities, 2) Transport, 3) Midstream and 4) Data. See the chart below for more detail.

Brookfield Infrastructure November 2022 Corporate Profile Slide 5

{kind=link}

Typically a somewhat “quiet company,” the partnership has been in the news lately due to its announced investment of up to $15 billion for a 49% interest in Intel’s ( INTC ) manufacturing expansion in Chandler, Arizona, with Intel retaining the remaining 51% interest. The deal is typical for Brookfield in both size and scope.

By their very nature, the assets owned and operated by the partnership are essential and in some cases irreplaceable. Those are nice assets to own in any market, but do they earn enough to enable Brookfield Infrastructure with its complicated capital structure to reliably pay its preferred distributions?

Financial Performance: Steady Growth In FFO And Distributions

The various Brookfield Asset Management affiliates are known for being share or unitholder friendly. For example, Brookfield Infrastructure’s mission statement from the November 2022 Corporate Profile is as follows:

Our objective is to own and operate a globally diversified portfolio of high-quality infrastructure assets that will generate sustainable and growing distributions over the long term for our unitholders.

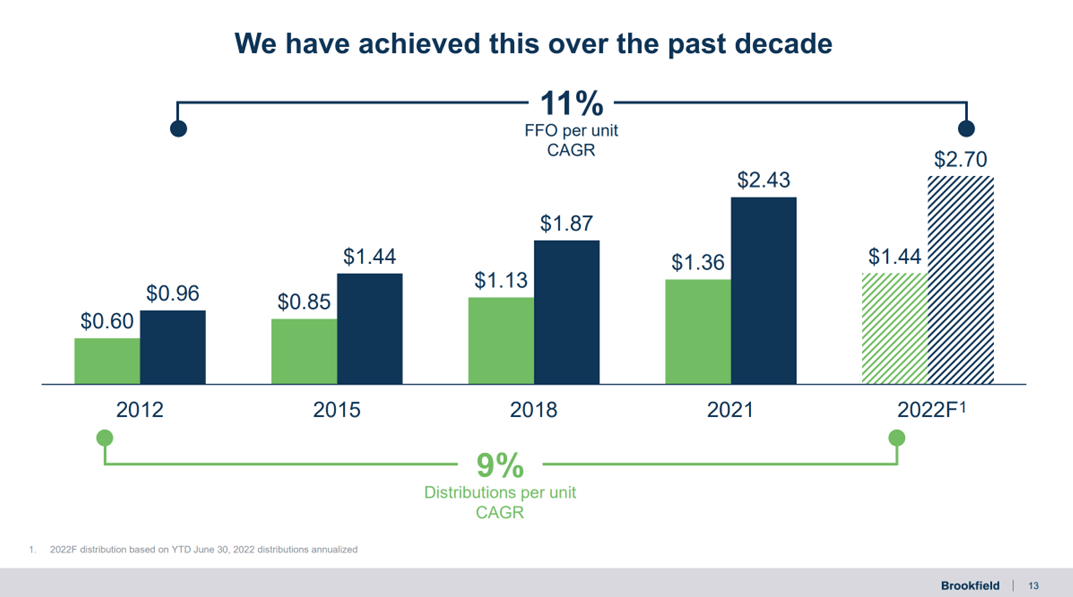

Specifically, management targets a 5% to 9% annual growth in cash distributions. As the partnership demonstrated at the Brookfield 2022 Affiliates Investor Day, through June 30, 2022, both FFO and distributions have increased in line with this target.

Brookfield Infrastructure September 29, 2022 Brookfield Listed Affiliates Investor Day Presentation

{kind=link}

The company also targets an annual return on invested capital of 12% to 15% over the long term with 13% reported YTD 3Q2022. With a weighted average cost of capital usually estimated at around 4.95% to 5.25% per gurufocus.com , the company is building long term value.

The partnership benefits from its general partner’s active and profitable capital allocation on behalf of its affiliates. During 2022, for example, management expects to complete approximately $1.5 billion in sales including its U.S container terminal operations, a New Zealand telecom tower portfolio, Brazilian electricity transmission lines and Indian toll roads. Another $900 million in sales are under contract, but expected to close in 2023. $2.8 billion in 2022 investments include AusNet, a natural gas transmission company in Australia, HomeServe, a British home repairs services company and Deutsche Funkturm, a radio and microwave tower subsidiary of Deutsche Telekon (OTC: DETGY), plus the previously mentioned Intel deal. Acquisitions are funded with proceeds from capital recycling, capital market issuances and retained operating cash flows.

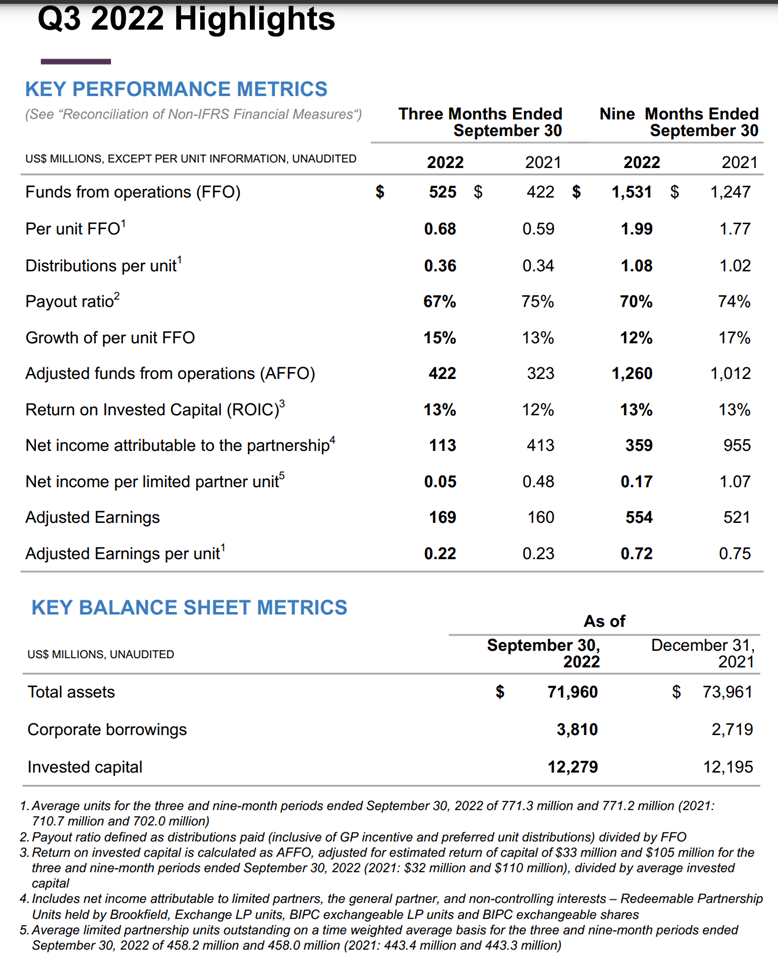

As with any partnership, GAAP net income does not always indicate true profitability. Year-to-date 3Q2022 net income attributable to the partnership was $359.0 million, down 62.4% from $955.0 million for the comparable 2021 period. FFO for the same periods, however, was up 22.7% to $1.5 billion from $1.2 billion. In the 2022 Brookfield Listed Affiliates Investor Day Presentation, management noted that approximately 85% of the partnership’s business actually benefits from inflation as 70% to 75% of EBITDA is directly linked to inflation and 10% to 15% is based on fee-for-service models.

The table below from the 3Q2022 Brookfield Infrastructure Supplemental Information Presentation shows almost all metrics headed in the right direction.

3Q2022 Brookfield Infrastructure Supplemental Information Presentation

{kind=link}

The partnership’s FFO payout ratio was 70% for YTD 3Q2022; on the high side of management’s targeted range of 60% to 70%. The stricter AFFO payout ratio - subtracting required capital maintenance expenses from FFO - for the same period was 84.5%. These payout ratios include regular, preferred and general partner incentive distributions, but the preferred units have first call on distributable funds.

In order to provide a better idea of the ability to pay preferred distributions, let’s consider a custom Preferred FFO Payout Ratio. At 3Q2022 there were preferred units outstanding amounting to $918.0 million at stated or book value. These units were senior to both general partner and common unit distributions. If we 1) ignore the liquidation ranking of the preferred units and assign a rough 5.25% average coupon, then the annual distributions on all the partnership’s preferred units amount to roughly $48.2 million or $36.1 million YTD 3Q2022. With first call on FFO of $1.5 billion, that’s a Preferred FFO Payout Ratio of only 2.4%. Additionally, total preferred unit distributions are declining. On November 28, 2022, the partnership renewed its normal course bid to purchase and retire up to 10% of the total public float of Series 1, 3, 9 and 11 that trade on the Toronto Stock Exchange. The takeaway is that the partnership would have to suffer an earnings catastrophe before lacking funds to pay preferred distributions.

A Complicated But Sustainable Capital Structure

Active capital redeployment plus a complicated capital structure equals a challenge for analysts and investors. Fortunately, there is no latent catastrophe lurking in the balance sheet, but the partnership carries a lot of debt. At the end of 3Q2022, consolidated long term debt totaled $25.4 billion with another $3.7 billion consisting of the current portion of long-term debt. On a net basis, subtracting cash and securities, that’s $29.0 billion in debt against $25.0 billion in partnership equity. Net debt to Adjusted EBITDA (essentially EBITDA less hedging and non-recurring items) YTD 3Q2022 was 5.2, enough to merit a yellow flag, but down from 6.1 for the YTD 3Q2021 period. Interest coverage measured as Adjusted EBITDA to interest expense was 3.0, a healthy number, but had slipped a bit from 3.3 for the YTD 3Q2021 period.

There are several factors that mitigate worries about Brookfield infrastructure’s debt.

- The partnership’s assets have long useful lives and generate stable cash flows that are largely inflation-linked or fee-for-service.

- Management’s active capital redeployment means that while large amounts of debt are typically incurred for acquisitions; equally large amounts are retired for dispositions. For example, YTD 3Q2022, $4.8 billion in nonrecourse debt was incurred, but $3.2 billion was repaid, for a net addition of $1.6 billion.

- The debt portfolio is laddered with no major maturities in any one year. For example, approximately 1% of long-term debt matures in two years, 7% in two years and 15% in three years.

- Roughly 85% to 90% of debt is fixed rate with a weighted average interest rate of 5.3% for the overall business as of 3Q2022.

- About 87% of debt was non-recourse as of 3Q2022.

A reasonable conclusion is that the partnership merits its management-targeted BBB investment grade debt rating.

Conclusion

Rates have gone up. It will cost Brookfield Infrastructure more to finance its large acquisitions, but the market-required return on those projects will go up, too, or they won’t be sold – and this will all be for incremental projects added to the existing portfolio. There is also a lot of room between the partnership’s 4.95% to 5.25% weighted average cost of capital and its 13% return on invested capital. Even if FFO declines - breaking the historical trend - our rough-and-ready Preferred FFO Payout Ratio of 2.4% indicates there’s a long way to go before preferred distributions are not paid.

Inflation, another possible headwind, is not a big issue for the partnership as the stable cash flows of its large infrastructure acquisitions are either inflation-linked or fee-for-service.

Nor will the need for electric transmission lines, railways, ports, gas processing plants and telecom towers suddenly disappear. During the height of the COVID epidemic, most western countries, like France , Germany and the U.S. , passed legislation to fund infrastructure projects. As the Intel deal shows, the partnership will be operating in a “target rich” environment.

For income investors, BIP.PR.B trading at $15.60 and an 8.03% yield mid-day December 19, 2022, provides a reasonable trade-off between risk and value for potential capital gains combined with current income.

For further details see:

Brookfield Infrastructure 5.00% Preferred Units: 38% Discount To Stated Value Plus 8% Yield