BIP - Brookfield Infrastructure: Checking Numbers Before Rushing In

2023-03-27 03:13:40 ET

Summary

- Brookfield Infrastructure Partners is trading at relatively low valuations but it does not make it a buy.

- BIP's further growth is squeezed by growing incentive distributions and higher interest rates.

- BIP is unlikely to increase its distributions by more than 6%.

- On an absolute basis, BIP is not cheap for its growth rates and leverage, while BIPC is outrageously expensive.

I have held Brookfield Infrastructure Partners ( BIP ) Brookfield Infrastructure Corp. ( BIPC ) for almost 10 years beating both the index' and parent Brookfield Corporation's ( BN ) returns. I kept adding to my position at every significant drop to reach these results. But not this time.

Almost all recent BIP articles on SA are bullish because of three main arguments: 1) the infrastructure industry is up-and-coming with some major tailwinds; 2) the BIP management team is second to none; 3) BIP has not been so cheap for a long time. All three points are correct but not sufficient to justify a buy.

For convenience, I will be talking primarily about BIP but every point will relate to BIPC as well. Economically, partnership BIP and corporation BIPC are equivalent. They enjoy the same distributions and a BIPC share is exchangeable to a BIP unit. However, due to different taxation, many investors prefer BIPC which is trading persistently higher than BIP.

Why BIP is so cool

BN holds ~30% of BIP units and its interests may seem aligned with that of outside investors. BIP's business interests are focused on several major infrastructure segments with a focus on low-risk countries of North America, South America, Australasia, and Europe:

- Utilities include both regulated transmissions and commercial and residential distribution.

- Transport includes sea terminals, railways, and toll roads.

- Midstream includes natural gas pipelines, storage, processing facilities, and a major petrochemical plant.

- Data operations include telecom towers, fiber, data centers, and semiconductor foundries.

Most businesses within segments are simply outstanding with high margins, long-term contractually- and inflation-protected cash flows, and huge capital backlogs securing further growth. The company has been uniquely creative in acquiring and building these businesses. Typically but not always BIP buys businesses for value, leverages them on an investment-grade basis, grows them profitably both organically and inorganically for many years, and eventually sells them for extraordinarily high prices. Superficially it may seem a usual buyout activity similar to traditional private equity, but there are two important differences.

Often BIP keeps its businesses much longer than required for a profitable quick exit typical for private equity. Secondly, BIP is one of the best infrastructure operators in addition to its financial prowess. Both factors make BIP more of a strategic player in the segments of its choice rather than a buyout outlet.

Sam Pollock has been the company's CEO since its very beginning in 2008 and, in my opinion, he has been impeccable and brilliant. Quite a few of his deals may deserve a place as business cases in MBA courses.

Well-run BIP deserves high valuations and is always expensive. But currently, it is less so. At the end of 2021, its market cap was ~$31B while now it is only ~$24B (make no mistake - BIP is still expensive on an absolute basis as I will show later). The drop in market cap is not due to some management mistakes or misfortunes. Quite on the contrary - over the last year or so, BIP has been very successful as evidenced by its high ROIC (more about it later).

So is it the right time to buy BIP units?

Financial arithmetic

BIP is the most transparent part of Brookfield's empire. Based on its supplemental filings, one can make conclusions that seem hardly possible for Brookfield's renewables, private equity, or real estate operations.

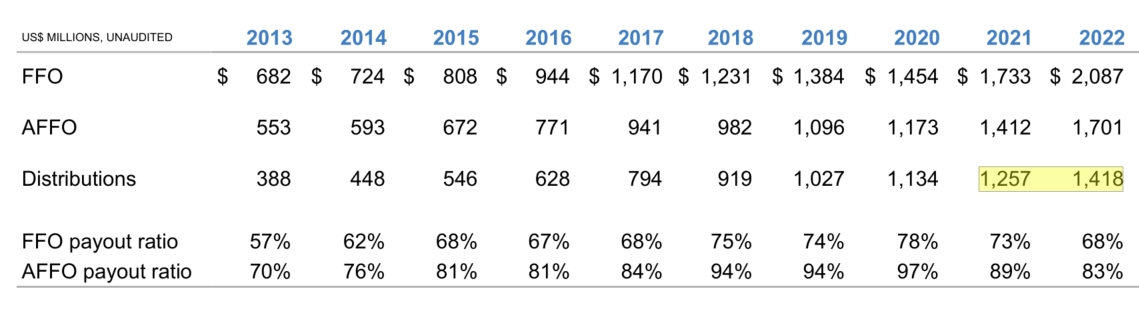

In its filings, BIP measures its profits in terms of net income, FFO, EBITDA, AFFO, and adjusted AFFO. Net income does not tell us much because the depreciation of infrastructure assets is much higher than maintenance capex. EBITDA completely ignores big interest expenses (BIP is highly leveraged) and maintenance capex. AFFO equals FFO less maintenance capex and is the most important number for us (we will get to adjusted AFFO in due course). AFFO shows how much cash BIP generates BEFORE investing in growth.

Cash measured by AFFO is used, first of all, to pay distributions on common units and equivalents (including those owned by BN), distributions on preferred units, and incentive distributions to Brookfield Asset Management ( BAM ), a corporation that externally manages BIP (BIP does not have its own personnel). Here is how incentive distributions are calculated:

{kind=link}

I marked the most important part in yellow. Since the current quarterly distribution is much higher than $0.1320 (it is $0.3825), a lot of money is going to BAM in addition to 1.25% of enterprise value in management fees (enterprise value is calculated using only corporate debt). Importantly, incentive distributions are growing much higher than common distributions.

For example, in 2022 distributions per common unit grew at 6% while incentive distributions grew at 16.5% (from $206M to $240M as reported in BIP's filings). It was due to both growth in common distributions and the increase in the number of units. But even without the latter, incentive distributions would have grown higher than 6%.

Below is the slide that makes the situation more palpable:

{kind=link}

In 2021, incentive distributions consumed 206/1257=16.4% of total distributions. In 2022, the same figure was 240/1418=16.9%.

Each year, incentive distributions' share is creeping higher and slowly strangling the common distributions growth.

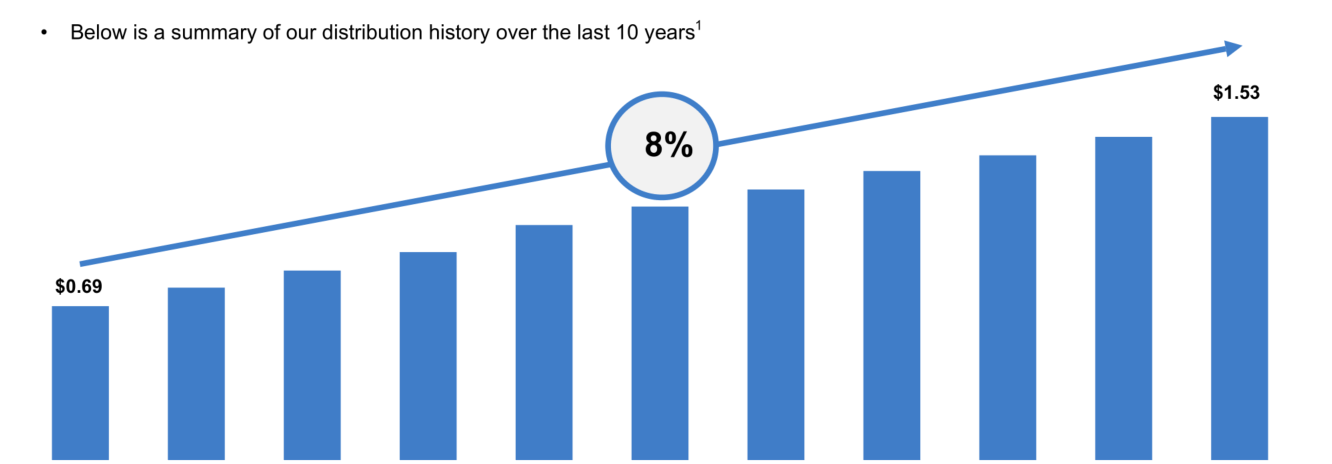

BIP likes to present the slide below boasting its long-term distribution growth:

{kind=link}

But this slide masks the fact that in very successful 2021 and 2022 common distributions grew only at 6% partially because of the "strangling" by incentive distributions.

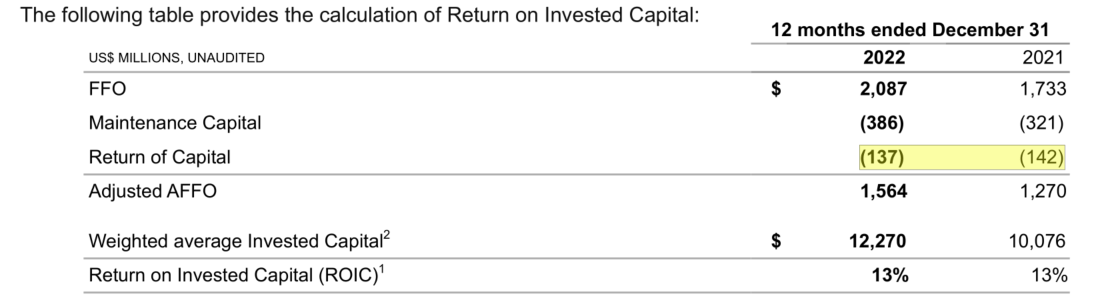

How do we know that 2021 and 2022 were very successful? BIP reports its ROIC (return on invested capital) every year and it has been fluctuating between 11 and 13%, but never higher than 13%. In both 2021 and 2022, ROIC was 13% and BIP still was not able to increase distributions by more than 6%!

One can find ROIC calculations in BIP's supplemental materials. Here it is:

{kind=link}

Since some of BIP's operations (such as toll roads) are based on finite-life government concessions, some invested capital will be eventually lost when the BIP concessions expire. To account for this, BIP differentiates between the return of capital and the return on capital with only the latter used to calculate true ROIC.

From the last slide, the adjusted AFFO in 2022 was $1,564. From one of the previous slides, the total distributions in 2022 were $1,418. The true payout ratio was 1418/1564=91%. It means that BIP did not have room to increase distributions further because something had to be invested in growth capex.

Why BIP is less attractive now

Once an investor buys BIP units, her return will be equal to the current distribution yield plus the distribution growth. The market determines the yield and it is currently 4.9% vs. the long-term average of 3.8%. The distribution growth is determined by the company's efficiency but as we have already seen it is unlikely to be higher than 6% even when the company operates at its maximum ROIC of 13%. Thus the expected return should be limited to 6+4.9=10.9%.

This figure appears mildly attractive when compared to the market average return of 10%. But it provides a slim margin of safety for the highly leveraged and expensive company. Please note that higher interest rates put pressure on financing growth by debt or preferred units. At the same time, BIP is unlikely to finance growth by issuing common units while they are trading that low (BIPC shares are still very expensive and can be issued for growth!).

To see how expensive BIP is, we need to calculate the ratio of its price to AFFO minus incentive distributions and preferred distributions that do not belong to investors. It immediately provides:

Market Cap/(AFFO-incentive distributions- preferred distributions) = 24.52/(1.70-0.24-0.05) = 17.4.

I would not call it cheap for a highly leveraged company growing at 6%. But the situation is worse than it seems. We calculated the company's market cap using BIP's price. But BIPC is trading at a staggering 38% higher than BIP! I cannot rationally justify this gap. It makes BIPC shares outrageously expensive.

Please note that since almost all of BIP's AFFO sans incentive and preferred distributions is being paid out in common distributions, yield is a good proxy for valuing the company.

I do not want to be overly negative about BIP due to the brilliance of its management. BIP can still appreciate and reach the yield of 4% (at ~$38 unit price) to be arguably fairly valued. 2023 can be very successful because BIP's huge Canadian petrochemical plant (which started operations only at the end of 2022) is supposed to reach its full capacity. In the best-case scenario, it will allow BIP to increase its distribution by 7% in 2024.

So BIP (but hardly BIPC!) may still have some potential but there are better opportunities available even within the Brookfield complex. Debt-free BAM is trading at a 4.2% yield. But its dividend is expected to grow much faster than BIP's at 15-20%.

For further details see:

Brookfield Infrastructure: Checking Numbers Before Rushing In