BIP - Brookfield Infrastructure Partners: Undervalued With Above-Average Income And Growth

2023-03-10 12:17:50 ET

Summary

- Brookfield Infrastructure Partners L.P. has a track record of increasing its funds from operations and dividend faster than the utility sector.

- A higher cost of capital has dragged down stock valuations, including triggering a correction in debt-heavy BIP.

- The units are currently undervalued and offers a nice cash distribution yield of about 4.7%.

Brookfield Infrastructure Partners L.P. (BIP.UN:CA) (BIP) stock has declined meaningfully by about 18% in the last 12 months. In the same period, the U.S. stock market, using SPDR S&P 500 ETF Trust ( SPY ) as a proxy, was only down about 6%.

Despite the correction, BIP's long-term return has been decent. For example, its 10-year total return (with the period ending Feb 28, 2022) was about 13.55%, beating marginally the U.S. stock market that returned 12.64% in the period.

BIP also offers higher income that's more than double the market's. Its cash distribution yield stands at almost 4.7% versus SPY's yield of about 2%.

What's Weighing on BIP Stock?

A higher cost of capital from higher interest rates that started in 2022 is weighing on the stock.

As a utility, it's natural that Brookfield Infrastructure has sizeable debt on its balance sheet. From 2019 to 2022, its total liabilities increased 39%, long term debt increased by 54%, while its total assets increased by 30%. In the period, its debt to asset ratio increased from approximately 61% to 65%.

| Year |

| Total Liabilities () |

| Long Term Debt () |

| % LT debt to Total Liabilities |

| Total Assets () |

| Debt to Asset |

| Interest Expense () |

| 2022 |

| $47.4 |

| $30.2 |

| 64% |

| $73.0 |

| 65% |

| $1,855 |

| 2021 |

| $47.6 |

| $26.1 |

| 55% |

| $74.0 |

| 64% |

| $1,237 |

| 2020 |

| $39.7 |

| $21.7 |

| 55% |

| $61.3 |

| 65% |

| $1,039 |

| 2019 |

| $34.1 |

| $19.6 |

| 58% |

| $56.3 |

| 61% |

| $821 |

Since interest rates increased last year, it's more meaningful to look at the change in its long term debt and interest expense in the period. Last year, its long term debt climbed 16%, while the interest expense jumped 50%. Debt-heavy businesses are simply riskier investment, particularly, in a higher interest rate environment.

That said, in its Q4 Supplemental Information , management noted that it has a "well-laddered debt profile with an average term to maturity of ~7 years with ~90% of debt fixed rate and no significant maturities this year." Much of its debt is at the asset level, such that in the worst case scenario, it would turn over a bad asset and the rest of the company would not be impacted.

Furthermore, it's all too common for BIP to raise capital from equity offerings. The graph below shows that BIP has increased its share count by 38% in the last 10 years.

It makes it less attractive or is even a bad idea for management to raise capital from equity offering when the stock valuation is compressed. So, here's one less avenue of capital raising.

Dividend

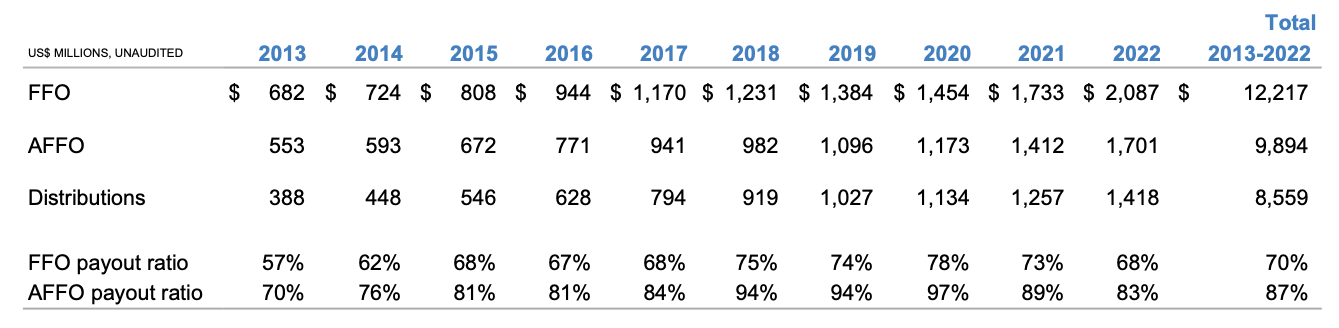

Brookfield Infrastructure has increased its cash distribution since inception. Its 10-year cash distribution growth rate is about 8%.

Management targets to maintain an funds from operations ("FFO") payout ratio of 60-70%. Brookfield Infrastructure's FFO payout ratio was 68% in 2022. So, unitholders can expect the cash distribution to continue growing more or less at about the rate of its FFO per unit growth, depending on how much FFO the utility might retain to reinvest into the business.

The utility targets cash distribution growth of 5-9% per year. However, for example, its 2022 FFO per unit growth was 12%, but it raised its cash distribution per unit by 6.25% last month. The fact that BIP raises its dividend at a slower rate than its FFO is not necessarily a bad thing because it means more FFO went into funding future growth. And the management has a track record of creating value for unitholders in the form of higher FFO and cash distributions per unit.

Growth

It's important to note that even though interest rates rose last year, the growth for BIP did not slow. 2022 was a strong year for BIP. It increased its FFO by 20% to $2,087 million. This is the key performance metric for the company as this is what it uses to pay out its growing cash distributions. On a per-unit basis, its FFO increased by 12% to $2.71.

{kind=link}

BIP has delivered a track record of growth -- from 2013 to 2022, its FFO growth rate was 13.2% per year, while its five-year FFO growth rate was 12.3%.

{kind=link}

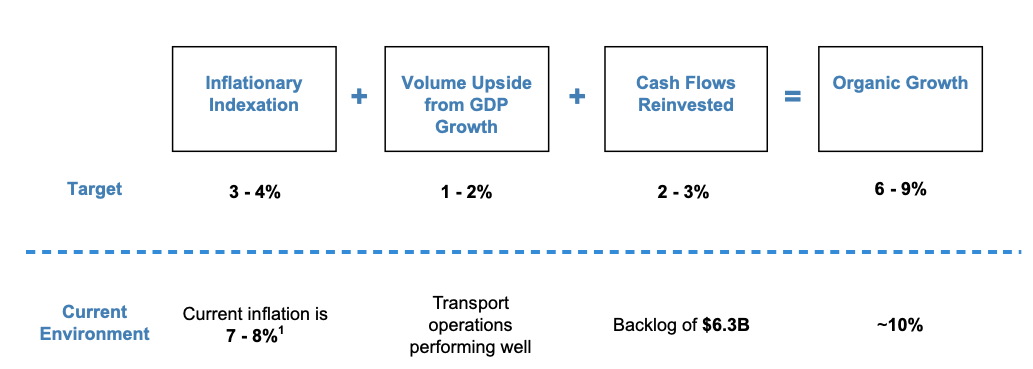

The relatively high inflation last year boosted BIP's results because about 70% of its cash flows are indexed to inflation. BIP normally expects FFO per unit to grow organically by 6-9% per year. In today's environment, it sees the potential for an extended growth rate of about 10%.

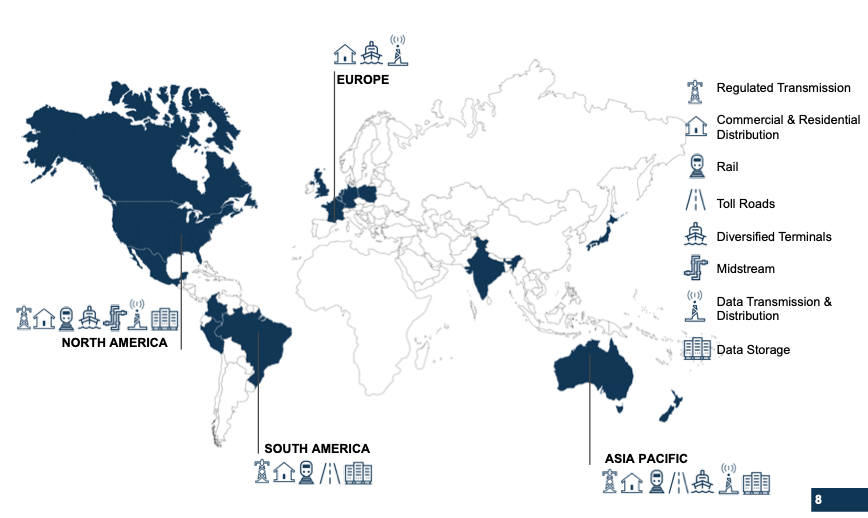

Brookfield Infrastructure has multi-decades of growth runaway. Its tentacles stretch internationally across essential infrastructure sectors in utility, transport, midstream, and data infrastructure.

{kind=link}

An important component of BIP's growth is its capital recycling program. It's an avid value investor. For example, last year, it secured $2.9 billion of capital to be deployed across five new investments. It also sold five mature businesses for proceeds of about $1 billion. As well, it has $6.3 billion backlog of projects to boost growth.

Investor Takeaway

At $32.72 per unit, Brookfield Infrastructure Partners L.P. trades at a forward FFO of about 14.6 assuming a 10% growth on its FFO per unit this year. The stock correction is a good opportunity to buy the investment-grade utility, with an S&P credit rating of BBB+, which offers relatively high growth versus the sector and at a nice cash distribution yield of 4.7%.

Yahoo Finance

Sure enough, analysts generally think the dividend stock is undervalued. They believe BIP stock trades at a discount of 24% from the consensus 12-month price target of $43.27 per share, which also implies near-term upside potential of 32%.

For further details see:

Brookfield Infrastructure Partners: Undervalued With Above-Average Income And Growth