BEPC - Brookfield Infrastructure Vs. Renewable: Market Inefficiency At Its Finest

2023-05-31 05:16:44 ET

Summary

- We had suggested investors ditch Brookfield Renewable and jump into Brookfield Infrastructure 16 months back.

- We examine that call and where the two stand today.

- The two entities and their related securities offer multiple examples of just how inefficient the market can be.

Arguing relative valuations can be a difficult task when investors put premium on one company's management. But often times we see gaps in valuation pop up on companies managed by the same parent. Just as frequently, we see valuation gaps open up on different tax structures of the same company. The Brookfield entities, Brookfield Infrastructure Partners LP. ( BIP ) and Brookfield Renewable Partners LP. ( BEP ), offer examples of both these pricing discrepancies and point to some serious market inefficiencies over time.

The Last Major Call

About 16 months back we made a clear call favoring one over the other.

Seeking Alpha

Guess how that turned out? The two moved like Siamese twins and if the charts were mislabeled pretty much no one would notice.

Ok, so those that dumped BEP for BIP are not exactly suffering on a relative basis but definitely did not benefit from that call. There is some pure irony in that recommended trade though and we can show you that by moving the comparison meter to a different set.

Both BIP and BEP are LPs and they also have corresponding corporations. If we run Brookfield Infrastructure Corporation ( BIPC ) vs Brookfield Renewable Corporation ( BEPC ) we get a very different result.

Where Things Stand Today

There was no clear winner between these two BIP in the 2022-2023 time frame. BIP appeared to have the lead for 2022, but then moved back in 2023. Funds from operations ((FFO)) grew by 11.5% for BIP in 2022 and is on course for growing another 9% in 2023. This is despite some strong headwinds from interest rates and even some currency movements going unfavorably.

BEP started off slower and delivered 7.6% growth in 2022, but we are on track for big move up by 14% for FFO in 2023. Both delivered solid growth, along expected lines. But there are few places that BIP gets the edge.

BIP's expected growth in 2024 dwarfs that of BEP. Mean estimates call for a 23% jump in FFO per share versus 11% for BEP. This is because a lot of BIP's investments that were not producing FFO begin to kick in. Notable here is the progress is being made on the Heartland Petrochemical Complex which is part of InterPipeline transaction. The complex was put into service in January 2023 and should achieve maximum run-rates towards the end of 2023. BEP's capital deployments are proceeding nicely as well, with inflation adjusters helping the company hit a second consecutive double digit increase in FFO per share.

Looking out over this entire timeframe, thanks to the flattish price, BIP's multiple will compress from 15, all the way to 10. BEP's FFO multiple will compress from 22 to 16 based on 2024 numbers.

Outlook

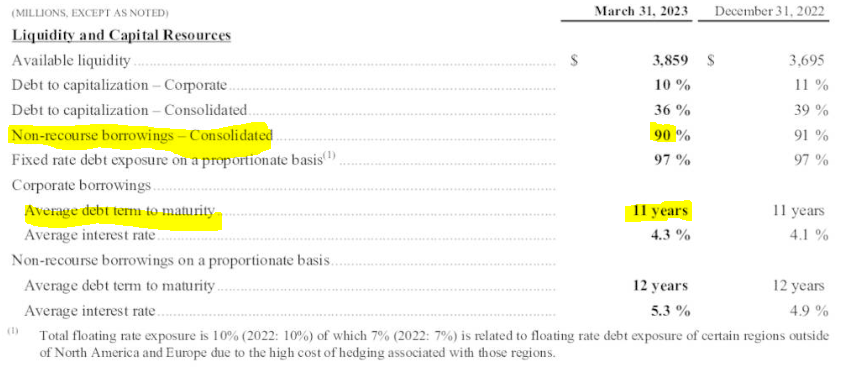

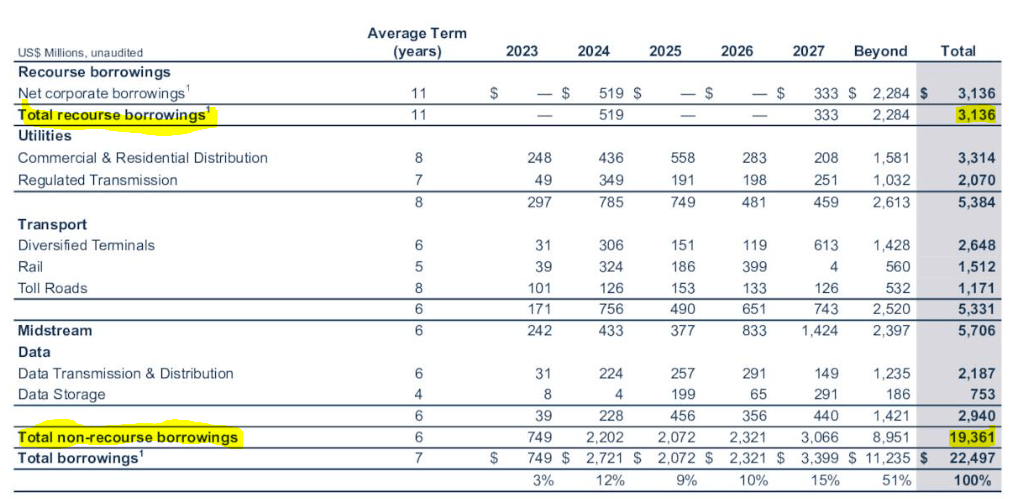

BIP's diversified model has produced solid growth while doling out a generous dividend. BEP has done a very similar job. Both firms use relatively high levels of debt with net debt EBITDA bordering near 6.5X. In both cases, the debt has been kept very manageable by primarily asset level obligations. This is the Brookfield Asset Management Ltd. ( BAM ) playbook in full glory. Leverage to the hilt, but don't endanger the corporation. BEP has done really well here with 90% of borrowings coming under the non-recourse category.

{kind=link}

BIP has a bit lower proportion for non-recourse, but it works for us nonetheless.

{kind=link}

Both corporations have a BBB+ credit rating, despite the high debt and that is because they never bought into the silly notion (as many did) that secured debt was a bad idea.

Here, we have to conclude that it makes absolutely no sense to pay 60% higher multiple for BEP vs BIP. The best case for BEP vs BIP is that the multiple remains the same and both produce similar growth over time, giving you similar returns. The worst case for BEP is that the multiple contracts down to the level of BIP giving you terrible relative and absolute returns. At present we rate BIP a buy and BEP a hold.

Market Inefficiency

This is one of those unusual cases where we are actually giving different ratings on the different entities attached to the same outfit.

BIPC is trading at 13X 2024 FFO versus 10X for BIP. The spread between them in dollar terms is absolutely insane and near the top of the range for the time period where both of these have been in existence.

We have doubts that the extra tax work associated with a Bermuda LP justifies that kind of premium. We rate BIPC a hold in an absolute sense and a sell relative to BIP.

The spread between the BEP and BEPC is very different. Very briefly during BEPC's initial existence, investors went raving mad and added a $15 premium for the silly concept that accountants are more expensive than paying 35% extra for a stock.

The spread has narrowed and hence we rate both BEP and BEPC the same, as hold/neutral.

Verdict

BIP has finally grown into its valuation and one could argue that it is a tad undervalued here. This is our first buy rating on the stock. Those looking for an even lower risk entry on BIP should consider selling $35 cash secured puts for December 2023 at $2.25.

Author's App

It provides an excellent "yield" if the stock stays above $35.00 and your effective entry price is $32.75 if it moves below that strike expiration. Brookfield Infrastructure Partners L.P. 5.125 CL A PFD13 ( BIP.PA ) is another defensive option from the same company where you get bulletproof 7.3% yield with very low risk.

BEP has done a good deal of the journey but we think forward numbers may be a little optimistic as there is so much capital chasing for the same opportunities in the renewables space. Here, we think that options would be a bit premature as downside risk would not be sufficiently negated by the near strike cash secured puts. Instead of BEP, we would go for Brookfield Renewable Partners L.P. 5.25% PFD CL A ( BEP.PA ) which has a yield over 7.30% at the current price. We had previously compared BIP.PA and BEP.PA and recommended BIP.PA as it was significantly cheaper (yet another example of market inefficiency). At present, both yield about the same so we are indifferent to either.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

Brookfield Infrastructure Vs. Renewable: Market Inefficiency At Its Finest