DLR - Brookfield Infrastructure: You May Kick Yourself For Not Buying At These Prices

2023-10-16 21:13:06 ET

Summary

- Brookfield Infrastructure Partners offers a durable income stream and strong operating performance, making it a quality dividend stock.

- It has a 14-year distribution growth history and has raised its distribution at an 8% CAGR over the past 10 years.

- BIP has growth drivers in digitization, deglobalization, and decarbonization, and currently trades very close to its 52-week low.

It’s not hard to be a dividend seeker these days, as there is a wide-ranging menu of selections to choose from, whether it be REITs, consumer staples, MLPs, etc. It pays to be selective, however, and for those who are choosy, it’s hard to go wrong with an infrastructure stock that can deliver a durable income stream in good times and bad.

This brings me to Brookfield Infrastructure Partners ( BIP ), which I last covered here back in February, at which time I thought the units were already cheap enough. With a downturn in the price over the past year, BIP now trades within a percentage point of its 52-week low, despite displaying strong underlying operating performance during this time. In this piece, I discuss why now may be a terrific time to add to this quality dividend stock. (Note: BIP issues a Schedule K-1).

{kind=link}

Why BIP?

Brookfield Infrastructure Partners is managed by the global asset manager, Brookfield Asset Management ( BAM ), and holds a leading portfolio of high-quality, long-life assets in utilities, transport, midstream, and data segments across North and South America.

In my previous piece on BIP, I noted that the shares were already cheap enough. However, BIP hasn't been immune to a general downturn in dividend stocks. For one thing, the market has become extra cautious around yield names as the anticipation of a higher for longer rate environment makes Treasury bonds more appealing than before compared to dividend stocks. In addition, a higher for longer rate environment also creates refinancing risk and makes debt-funded growth more expensive, as reflected by the downturn in stocks such as NextEra Energy ( NEE ), which has relied in part on issuing debt at low interest rates in over the past decade to grow.

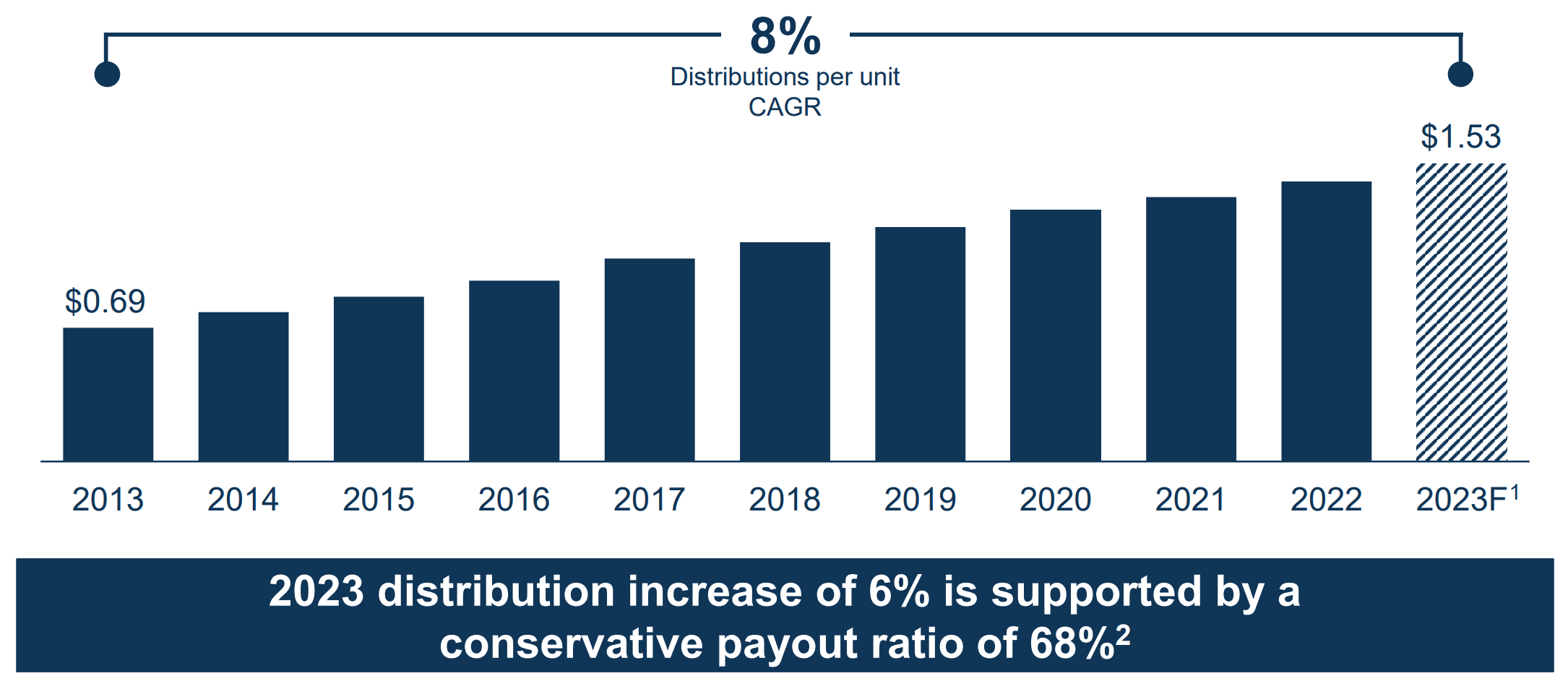

However, I believe the market has overly punished BIP's stock, considering the long-lived nature of BIP’s assets with inflation-protection built into the contracts, combined with 90% of debt held at long-term fixed rates provide a steady recurring income stream for the company. This has enabled strong capital returns to shareholders over the past 10 years. BIP has a 14-year distribution growth history and has raised its distribution at an 8% CAGR over the past 10 years, as shown below.

BIP Distribution Growth (Investor Presentation)

{kind=link}

Judging by the unit price downturn over the past 12 months, one may be led to believe that the business was performing poorly. That’s simply not the case, as operating fundamentals have continued to exude strength since I last visited the company after 2022 results. This is reflected by the first half 2023 FFO per share growing by 10% YoY to $1.44, and for the full year 2023, management is guiding for even higher 13% YoY FFO/share growth to $3.05.

A potential headwind for BIP stems from the current low share price, which at $25.98 and a forward FFO/share of $3.05 equates to a forward 11.7% cost of equity, thereby making it expensive to raise equity. However, what’s good for BIP is that it has BIPC ( BIPC ), which is economically identical to BIP, but carries a higher share price. That’s because some investors prefer to pay a higher price to not have to deal with Schedule K-1s.

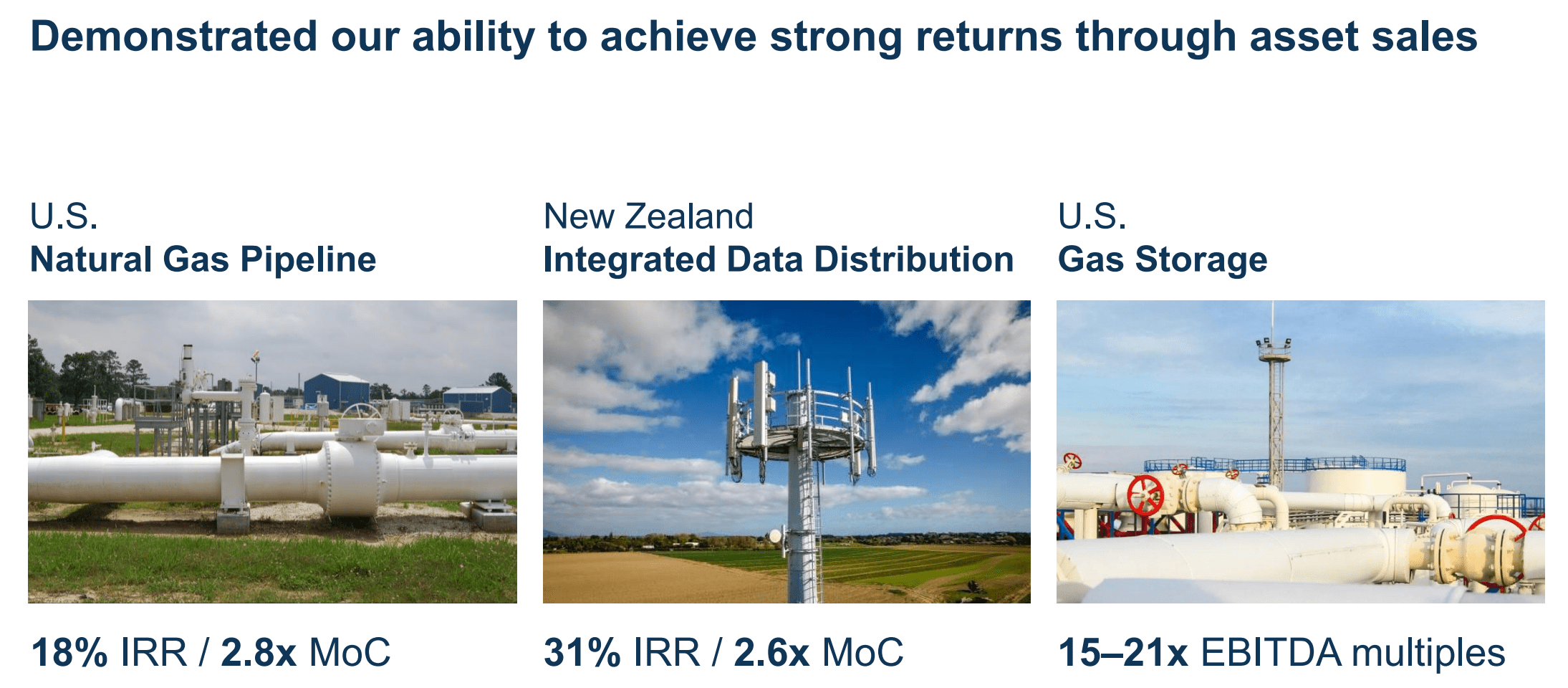

The price differential between BIPC and BIP is significant, and through previous equity raises and asset sales, BIP was able to secure sufficient capital ($2.8 billion) to fully fund its 2023 growth spend of $2.6 billion. As shown below, BIP was also able to realize substantial capital with gains on the sale of assets.

BIP Recent Asset Sales (Investor Presentation)

{kind=link}

BIP sees three underlying drivers of growth going forward, with them being digitization, deglobalization, and decarbonization. This includes opportunities in generative AI and opportunities in the data center as enterprises migrate workloads and applications from on-premises to the cloud. This segment is expected to see a significant ramp up over the next few years, as mentioned during the last conference call :

We secured the acquisitions of two development platforms, Data4 and Compass, which meaningfully contribute to our operating capacity and expand our presence in Europe and North America, respectively.

In fact, following the closing of both transactions, we will own and operate one of the largest global hyperscale data center platforms. Our operating capacity will increase to over 485 megawatts with an additional 775 megawatts capacity already contracted and reserved that will be built out over the next several years.

Combined, we expect to have over 1.25 gigawatts of capacity over the next few years that is highly contracted to provide stable cash flow and is underpinned by major hyperscale customers.

Meanwhile, BIP carries a strong BBB+ credit rating, putting it on par with that of other high-quality infrastructure companies such as midstream player Enbridge ( ENB ) and sitting higher than the BBB credit rating of Digital Realty Trust ( DLR ). This rating comes in handy in a higher interest rate environment, and BIP has $2.3 billion in available liquidity.

It also carries a net debt to EBITDA ratio of 6.2x, which is reasonable for the capital-intensive nature of the business, especially considering that there are plenty of REITs on the market with less durable cash flow streams and a 6x leverage ratio that’s generally considered to be safe by ratings agencies.

Importantly, BIP raised its distribution this year by 6% and it remains well covered by a dividend-to-FFO payout ratio of 68%, leaving plenty of retained capital for growth funding. BIP also trades at a highly attractive price of $25.98 with a forward P/FFO of just 8.7. Performing the following NPV analysis, I arrive at a $45.46 fair value for BIP units.

This is based on a modest 4% growth rate and a 5% discount rate to account for BIP’s reliance on external growth capital in recent years. This represents a significant upside from today’s share price and sits within the range of analyst price targets of $36 to $50 .

NPV Analysis (Produced by Author)

{kind=link}

Looking ahead to Q3 earnings, I don't expect to see surprises, considering the long-lived nature of BIP's contracts. I do look forward to getting an update on the Triton International (TRTN) acquisition , which recently received regulatory approvals. TRIN is the world's largest lessor of intermodal freight containers, and I look forward to hearing how this $13.3 billion deal is going to add to the bottom line in the coming quarters.

Investor Takeaway

In conclusion, Brookfield Infrastructure Partners has strong underlying operating fundamentals and growth drivers, a solid balance sheet and liquidity position, and an attractive distribution with room for further increases. While BIP's 5.9% yield isn't the highest on the market today, its management track record, diverse asset base, and strong credit rating make it a compelling choice at the current valuation.

Risks to the thesis include a materially higher rate environment should interest rate growth outpace the rate of inflation. Moreover, faster than expected ramp of renewable energy and or higher commodity prices could pose as a headwind to BIP's midstream assets and its customer base. Nonetheless, I believe the market is overweighing the potential negatives while ignoring the positives, thereby creating an attractive valuation on the stock. As such, I'm upgrading BIP to a 'Strong Buy'.

For further details see:

Brookfield Infrastructure: You May Kick Yourself For Not Buying At These Prices