VNORP - Brookfield Property Preferreds: The Trend Is Not Your Friend

2023-08-15 10:00:00 ET

Summary

- Brookfield Property Partners LP preferred shares were downgraded to "Sell" due to high debt levels and a declining FFO.

- Q2-2023 saw FFO remain negative even though there was marginal improvement in office occupancy levels.

- Refinancing will be challenging, and mortgage defaults are expected to increase.

- Don't chase the double digit yields.

On our last coverage of Brookfield Property Partners LP publicly traded preferred shares, we gave it an upgrade of sorts to account for the price decline.

Our take is that we are probably looking at an 20X debt to EBITDA by the fourth quarter of this year. We are taking our Strong Sell Rating and upgrading it here to just a "Sell" to account for more appropriate pricing for the risks.

Source: FFO Goes Negative

The three stocks in question, Brookfield Property Partners L.P. 5.75 CL A PF SR3 ( BPYPN ), Brookfield Property Partners L.P. 6.375 CL A PFD 2 ( BPYPO ) and Brookfield Property Partners L.P. 6.50 PF UNIT A 1 ( BPYPP ), are up from that point but remain down from the original Sell rating . They sport double digit yields today and that is the lure that will likely hook some people in. We look the Q2-2023 results to see if the company has started turning its fundamentals around

Q2-2023

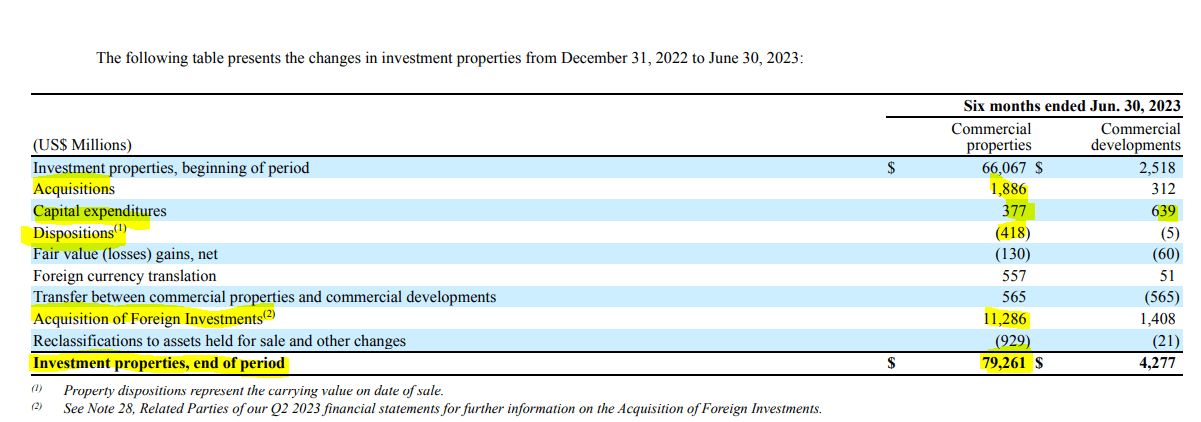

2023 has so far been a complex year for BPY as it has engaged in the routine acquisitions and dispositions alongside a large internal reorganization which saw it add $11.29 billion in property assets.

{kind=link}

BPY Q2-2023 Financials

But the asset level jumps have also resulted in similar increases in debt load.

{kind=link}

BPY Q2-2023 Financials

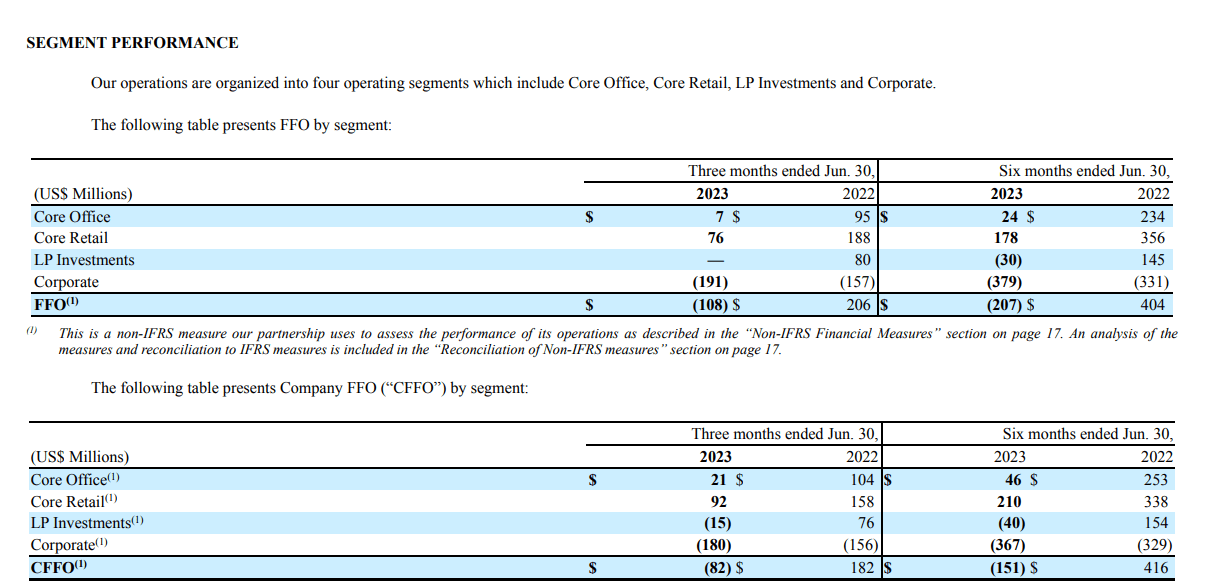

Despite the relatively large asset increases, funds from operations (FFO) was negative at both levels. Whether you used total FFO or company FFO you came away with a negative number.

{kind=link}

BPY Q2-2023 Financials

The big area for BPY to watch has been the stress on the office properties side. This quarter looked a little better in some ways as the occupancy levels nudged up to 83.7%.

{kind=link}

BPY Q2-2023 Financials

These were at 82.9 in Q1-2023.

BPY Q1-2023 Financials

One point to note here though is that we have 2 properties less in Q2-2023 (60 total) versus Q1-2023 (62 total). Even more interestingly, some asset sales that were conducted in this segment were those where the counterparty was none other Brookfield Reinsurance ( BNRE ).

In June 2023 we sold partial interests in six Core Office assets to Brookfield Reinsurance Ltd (“BN Re”), which include partial interests in three assets in the U.S. for net proceeds of approximately $306 million and three assets in Canada for net proceeds of approximately C$405 million ($306 million).

Source: BPY Q2-2023 Financials

On the core retail side, net operating income (NOI) held steady year over year.

{kind=link}

BPY Q2-2023 Financials

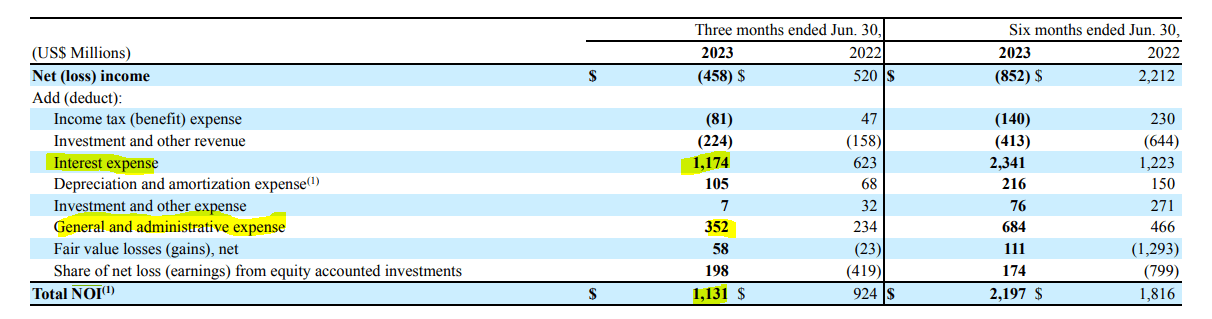

FFO still declined sharply as interest expenses continued their bite. Q2-2023 was also lower than Q1-2023, a face you can discern easily by comparing the six month results with the quarterly numbers.

{kind=link}

BPY Q2-2023 Financials

Outlook

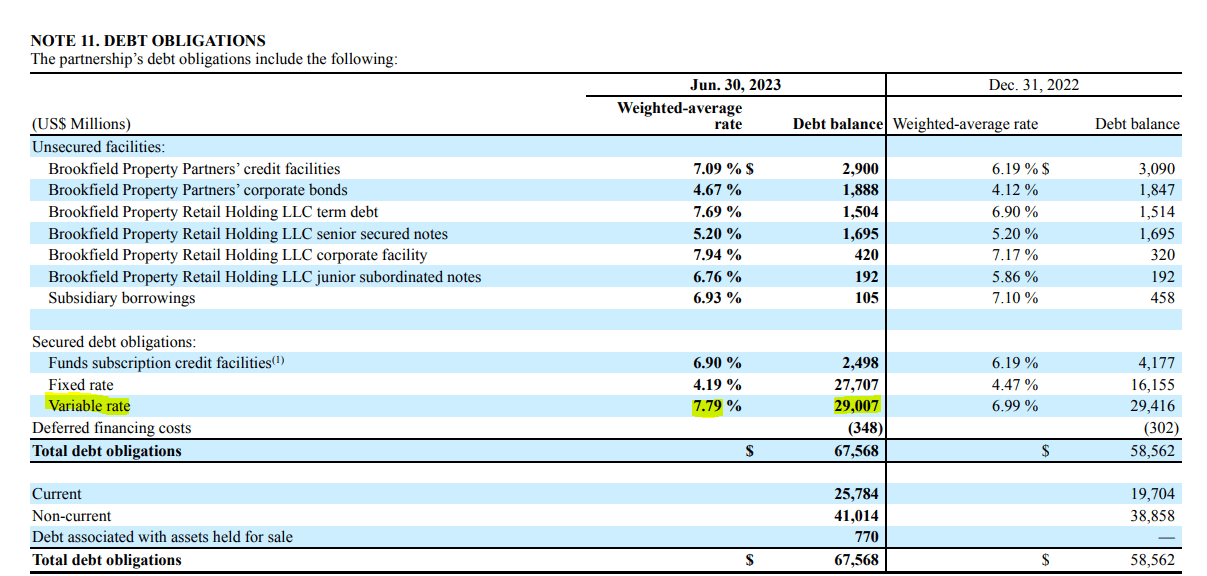

BPY preferreds continue to be a story about the debt load. The $67.6 billion of debt has almost $30 billion tied to variable interest rates and the company was paying almost 8% on that. Those numbers are weighted average rate for the quarter and in all likelihood will be up past 8% in Q3-2023.

{kind=link}

BPY Q2-2023 Financials

This vast exposure to floating rate debt is somewhat offset by its swaps.

{kind=link}

BPY Q2-2023 Financials

Some of these hedges only cap only after a certain threshold is hit and many will be going into maturity dates, and won't protect any more.

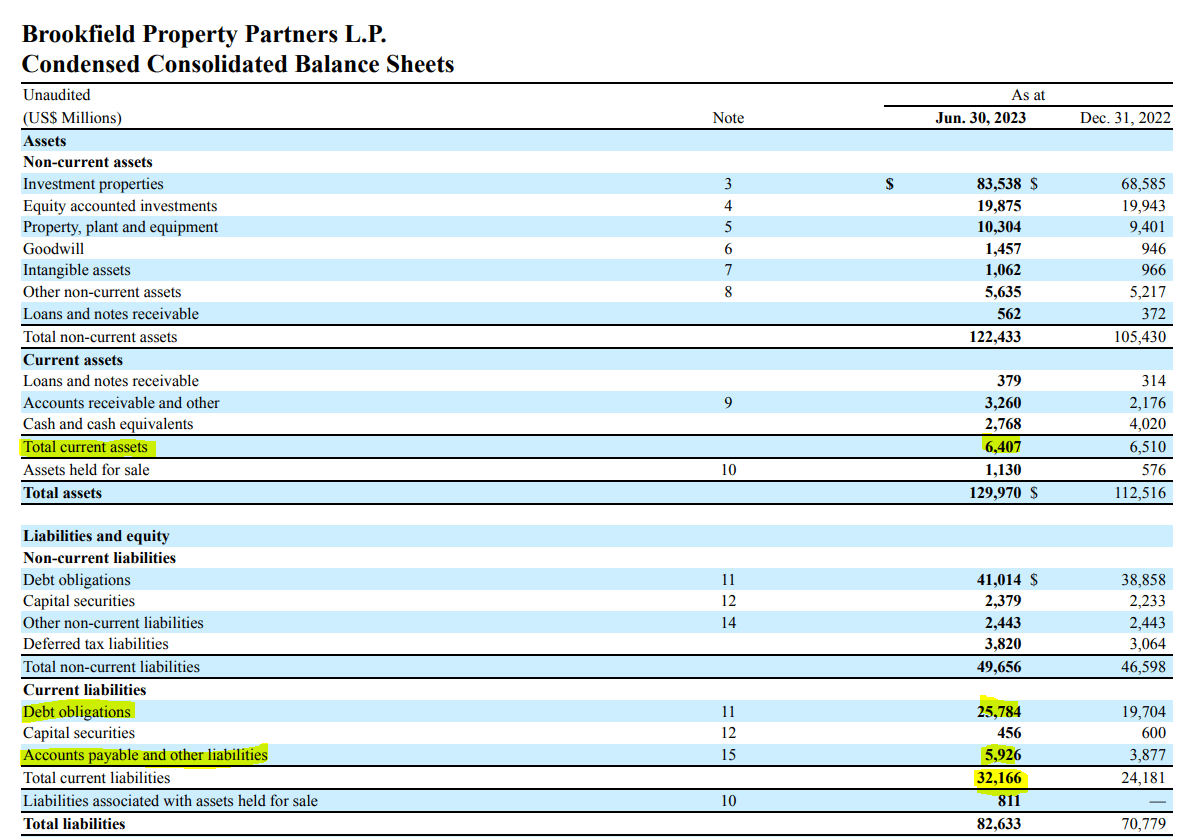

BPY has current liabilities of $32.16 billion against current assets of $6.4 billion.

{kind=link}

BPY Q2-2023 Financials

Refinancing will be tough and/or come with requirements for substantial debt paydowns. We saw this in the latest quarter for Vornado ( VNO ) which carries less than half the debt to EBITDA levels of BPY. Currently BPY is in default on just 3% of its mortgages.

We generally believe that we will be able to either extend the maturity date, repay, or refinance the majority of the debt that is scheduled to mature in 2023-2024, however, approximately 3% of our debt obligations represent non-recourse mortgages where we have suspended contractual payments. We are currently engaging in modification or restructuring discussions with the respective creditors. These negotiations may, under certain circumstances, result in certain properties securing these loans being transferred to the lenders.

Source: BPY Q2-2023 Financials

Last quarter it was 2% and in Q3-2022 it was 1.2% . So a slow and steady deterioration is going on here and we expect this number to go past 5% at some point. Would 5% of defaults matter? They definitely would as BPY already has a negative FFO run-rate.

Verdict

BPY has about $130 billion of assets and $83 billion of liabilities as per their Q2-2023 IFRS statement. That is the bull case for the preferreds that there is a big buffer ahead of the preferred shares. We have two problems with that. The first being due to the extremely convoluted setup within BPY, not all of that equity can buffer ahead of the preferred shares. There are several consolidated partnerships, each with their own terms and conditions and non-controlling interests. How the losses are allocated will only be known to BPY and the parent Brookfield Asset Management ( BAM ).

The second issue is that the equity is valued using these terminal cap rates.

{kind=link}

BPY Q2-2023 Financials

We have watched this over a few quarters and considering the kind of sales occurring in the office segment particularly, those terminal cap rates look really detached from reality. Interestingly enough, BPY lowered the cap rates on LP investments from December 31, 2022 to June 30, 2023.

If you can get past these hurdles because this is a Brookfield name, well then you have to contend with the negative FFO which likely gets worse as hedges roll off and higher rates go through the income statement. Even their fixed rate debt which is the mid 4% range, is likely to be refinanced well over 7% today. More than $30 billion needs to be refinanced in the next two years. All of this as NOI is less than interest expense.

{kind=link}

BPY Q2-2023 Financials

If you use EBITDA equals NOI minus G&A expenses, which would be about as generous as it gets, your annualized EBITDA would be $3.12 billion (($1,131 million minus $352) X 4). Your debt EBITDA ratio would be well over 25X. So how all of this works out absent a massive rate cutting cycle, remains unknown to us. We still rate all the preferred shares a Sell and suggest investors look for safety first in today's investing climate.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

Brookfield Property Preferreds: The Trend Is Not Your Friend