RA - Brookfield Real Asset Income Fund Just Cut Its Distribution What Now?

2023-08-31 10:51:43 ET

Summary

- Brookfield Real Asset Income Fund Inc. just announced a significant cut to its distribution, leading to a 27% decline in its stock.

- The fund has had poor long-term performance and was paying a high distribution yield that it did not earn.

- The fund is now trading at a discount to NAV, but the new distribution rate may still be too high. Investors should consider switching out of the fund.

About a year ago, I reviewed the Brookfield Real Asset Income Fund Inc. ( RA ) and warned that its ~14% yield may not be sustainable, as the fund had only earned 5 year average annual returns of 1.5%.

Unfortunately, my worst fears were realized as the RA fund just announced a significant cut to its distribution, from $0.1990 / month to $0.1180 / month for October to December, 2023. Investors were blindsided by the announcement and punished the stock with a 27% decline and counting.

For unitholders unlucky enough to be caught in this fiasco, is the worst over for RA's share decline, or is there more downside?

Brief Fund Overview

The Brookfield Real Asset Income Fund has a broad investment mandate. As long as an investment is considered a 'real asset company' by Brookfield, it is fair game for the RA fund. This means the fund can invest in REITs, operating real estate companies, real estate developers, infrastructure assets like pipelines and toll roads, and natural resource companies.

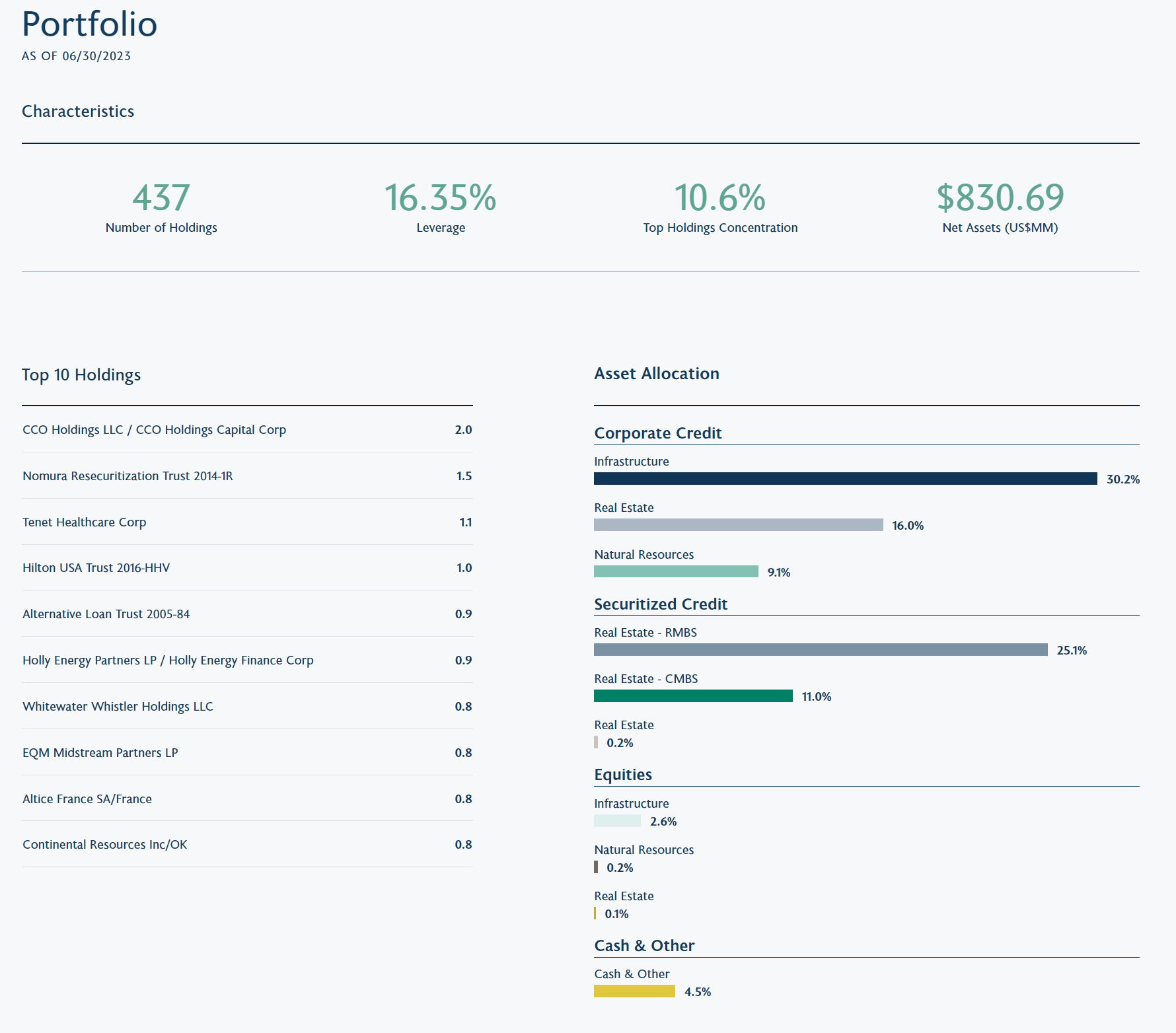

As of June 30, 2023, the RA fund had $831 million in net assets that are predominantly invested in infrastructure (30.2%), residential mortgage backed securities ("RMBS", 25.1%), real estate (16.0%), commercial mortgage backed securities ("CMBS", 11.0%), and natural resource companies (9.1%) (Figure 1).

Figure 1 - RA fund portfolio overview (brookfieldoaktree.com)

{kind=link}

Poor Long-Term Returns...

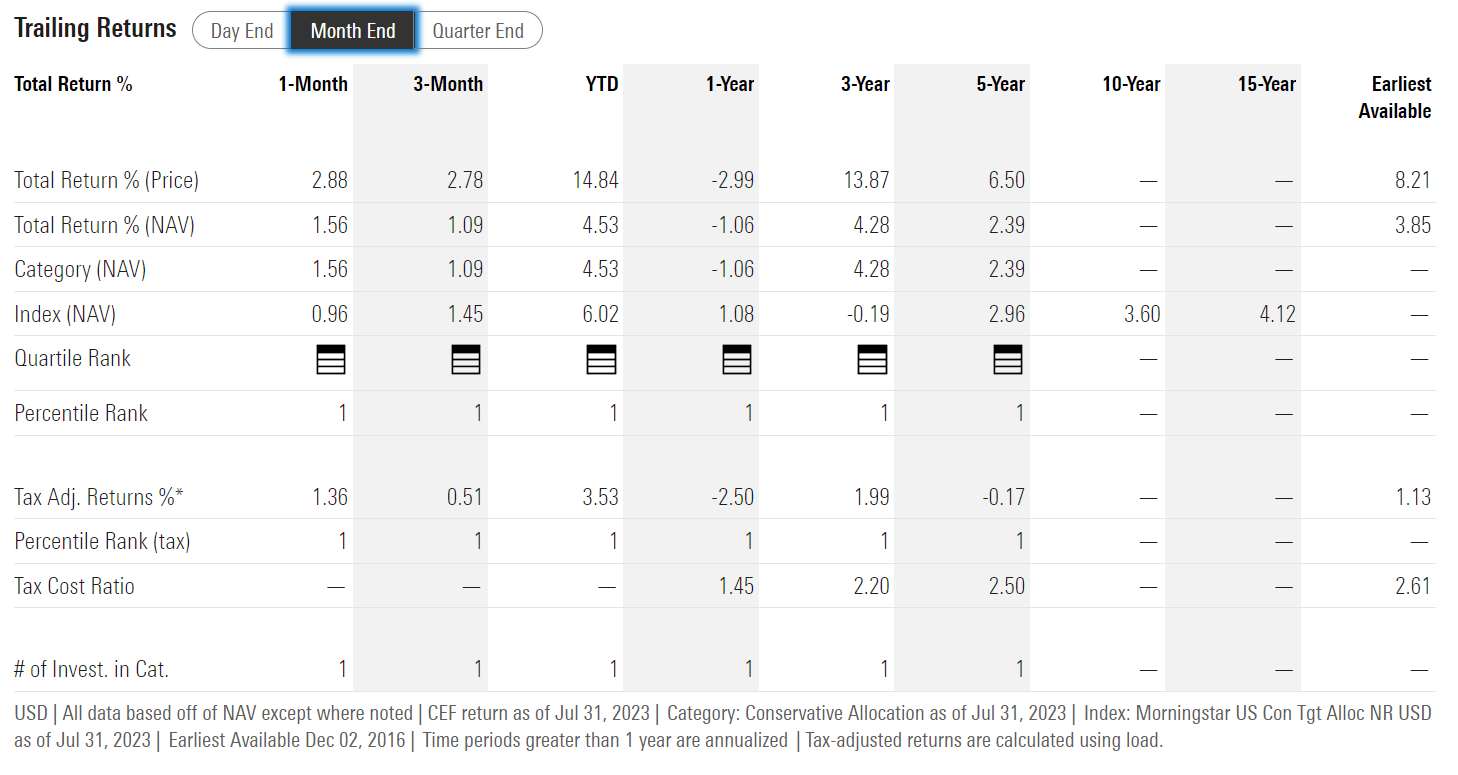

I had two main concerns with the RA fund. First, the fund has had poor long-term performance, with 3 and 5 year average annual returns of only 4.3% and 2.4% respectively to July 31, 2023 (Figure 2).

{kind=link}

... Combined With High Distribution Yield Is A Bad Combo

At the same time, the RA fund was paying a $0.1990 / month distribution that yielded ~14.0% on RA's August 29th closing price of $16.88. On last published NAV, the RA fund was actually paying an eye-watering 16.3%.

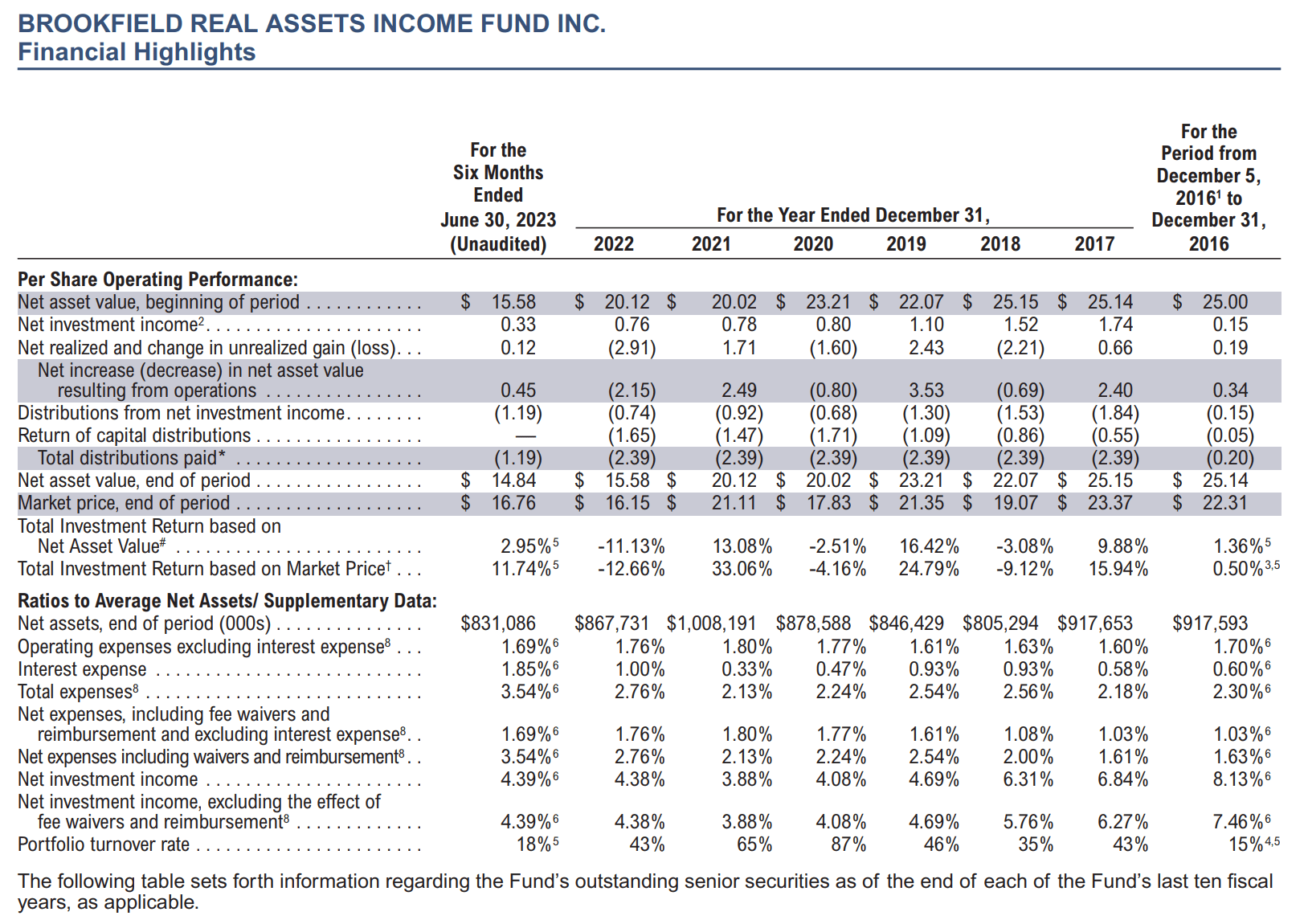

However, the RA fund did not 'earn' its distribution. If we look at the fund's latest semi-annual report, we can see the RA fund had been using return of capital ("ROC") to fund the vast majority of its distributions (Figure 3).

Figure 3 - RA fund was using ROC to fund distribution (RA semi-annual report)

{kind=link}

In effect, investors were simply paid back their own capital through the distribution.

Yet RA Traded At A Steep Premium To NAV

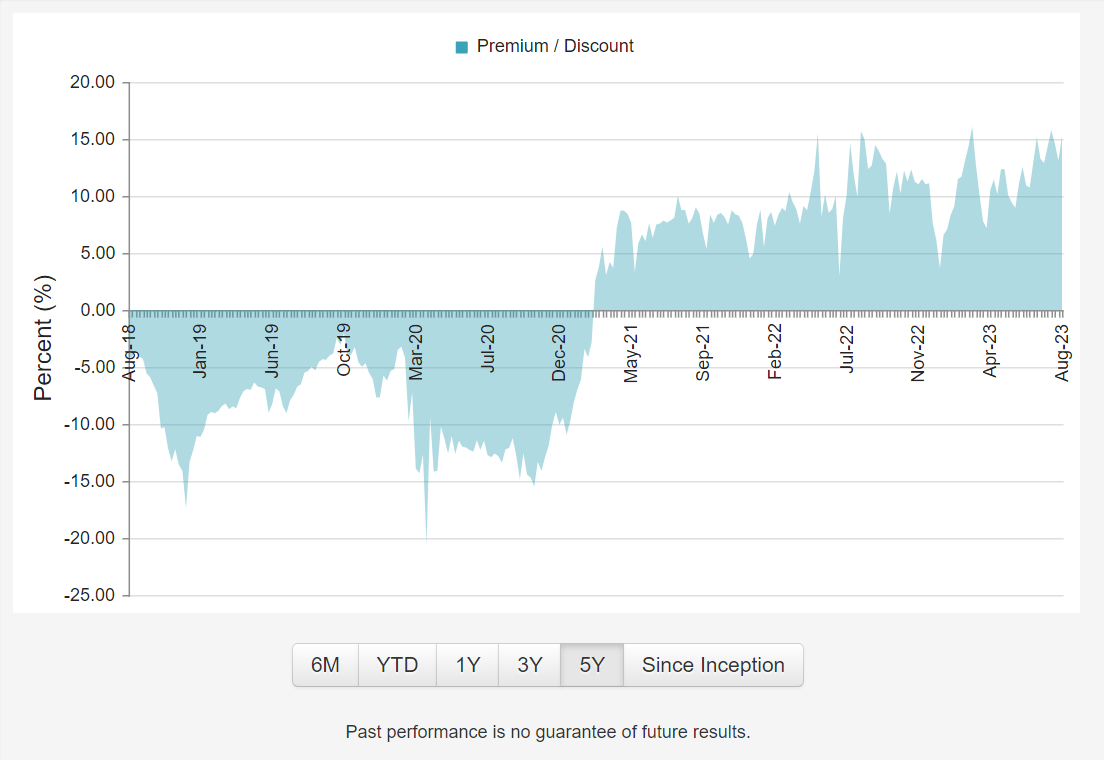

However, investors seem to be enamored with the RA fund, bidding it up to a 15% premium to NAV (Figure 4).

Figure 4 - RA fund traded at a 15% premium to NAV (cefconnect.com)

{kind=link}

I speculated in my prior article that many investors were attracted by the RA fund's brand name, as Brookfield/Oaktree, the fund's sponsor, is one of the most well-known alternative asset manager in the industry. Furthermore, like many other CEFs, the RA fund has a 'dividend reinvestment' ("DRIP") feature that allows investors to reinvest distributions into newly issued shares at the greater of 95% of market price or NAV.

For many retirees and income-oriented investors, this DRIP feature sounded like a good idea, as they can buy shares yielding 14% at a 'discount' to the market price. Never mind that if the shares are issued at a premium to NAV, they are overpaying for those shares.

This situation of paying 16.3% of NAV distribution while earning 4.3% is clearly unsustainable. The problem is that a large fund like RA can go on funding distributions for a very long time, as long as it has assets to liquidate.

Mirage Comes Crashing Down

The mirage of the RA fund paying a steady $0.1990 / month distribution came crashing down on August 29th when the fund announced upcoming distributions for October to December of only $0.1180 / month, a dramatic 41% cut. At the current forward distribution of $0.118 / month, the RA fund is now yielding 10.6% at the most recent trading price of $13.31 / share. On NAV, the new distribution rate is now yielding 9.7%.

Valuation Back To Earth; Downside Priced In?

The question of whether the worst is over for the RA fund is hard to say, as investors can become very emotional when they are selling. However, we can say that with the fund now trading at a 9.4% discount to NAV ($13.31 share price vs. $14.67 last published NAV), a lot of the downside has now been priced in.

If the RA fund's stock price falls further, it may even attract the attention of activist funds like Boaz Weinstein's Saba Closed-End Funds ETF ( CEFS ) that invests in underpriced closed-end funds and agitate for management changes.

New Distribution May Still Too High

Another question current investors should consider is whether the RA fund's new distribution rate of $0.1180 / month may still be too high, given the earnings power of the fund to date. The RA fund's 3 and 5 year average annual total return of 4.3% and 2.4% respectively is still too low relative to the new distribution rate of 9.7% of NAV.

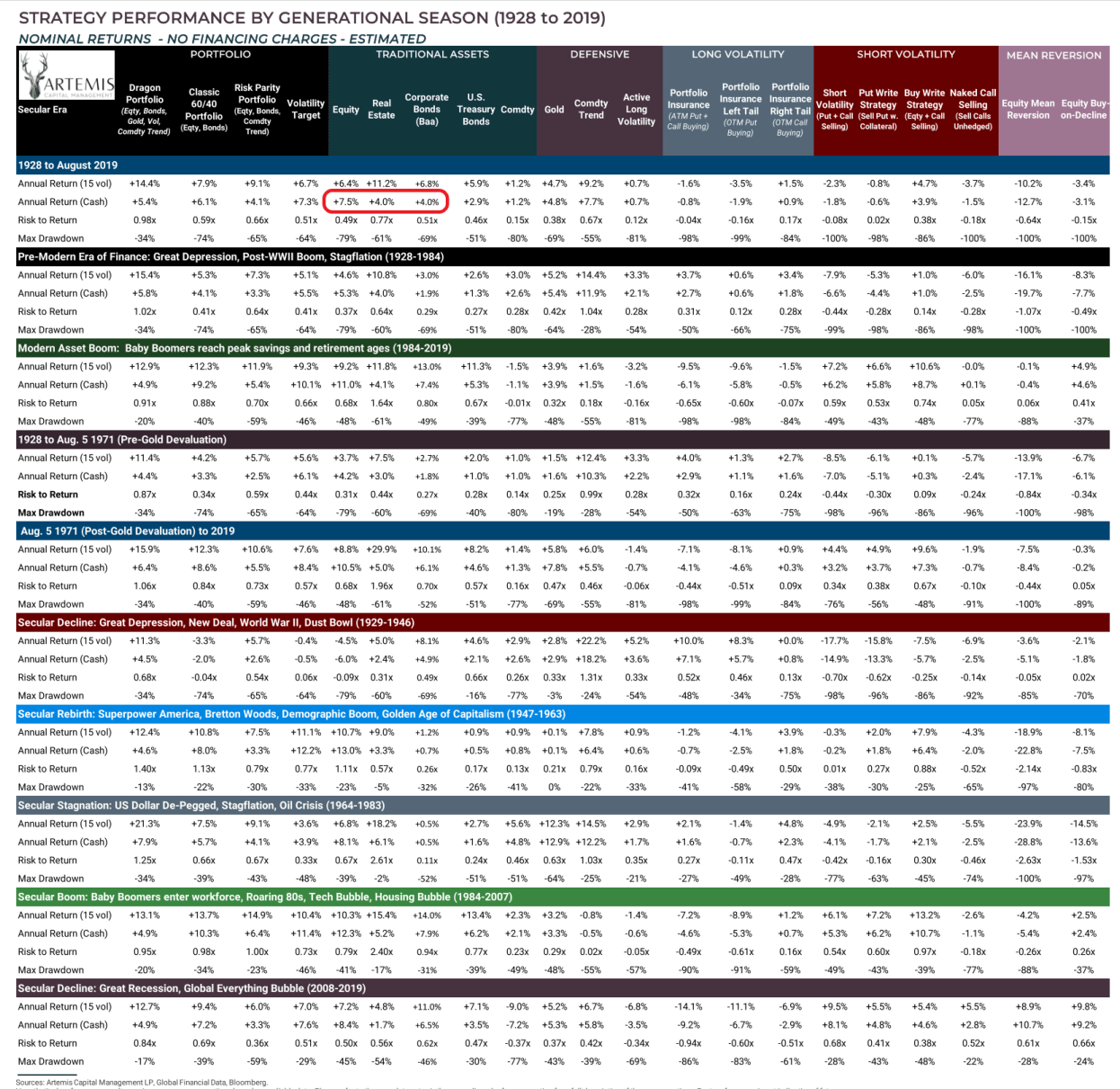

Looking at very long-term historical returns of asset classes (provided by Artemis Capital Management), we can see that stocks, real estate, and corporate bonds have returned 7.5%, 4.0% and 4.0% respectively from 1928 to 2019 (Figure 5).

Figure 5 - Long term asset class returns (Artemis Capital Management)

{kind=link}

Therefore, a reasonably constructed portfolio of equities, REITs, infrastructure assets, and bonds like the RA fund should not be expected to earn more than 5-7% over the long-term in my view.

RA Should Convert To A Managed Distribution

Rather than commit to pay an unsustainable ~10% distribution yield, I believe the RA fund should convert to a managed distribution strategy where the fund pays 1% of NAV / quarter as a 'base' distribution, and in years when the fund generates large returns, the RA fund can 'reward' unitholders with special distributions.

Many successful CEFs like Tri-Continental Corp ( TY ) employ this model and have delivered superior long-term performance for unitholders without amortizing its NAV.

Conclusion

The dramatic reaction to the RA fund's distribution cut has brought the RA fund to a 9% discount to NAV, so a lot of the downside has been priced in. However, even at the reduced distribution rate of $0.1180 / month, it still annualizes to a 9.7% forward yield on NAV, which may be too high for the fund's earnings power. Investors currently stuck in the RA fund should use any upcoming rebound in the fund's shares to switch out of the fund.

For further details see:

Brookfield Real Asset Income Fund Just Cut Its Distribution, What Now?