RA - Brookfield Real Assets Vs SJNK: Birds Of A Feather

2023-12-07 09:29:36 ET

Summary

- The Brookfield Real Assets Income Fund cut its distribution in August and predictably got punished for it.

- Since it predominantly holds high yield assets, we compare it to a high yield bond ETF.

- We conclude with our outlook on the Brookfield Fund.

The Brookfield Real Assets Income Fund ( RA ) took flight during the pandemic and did not touch down until August of this year.

We covered it when it took flight in 2020, and explained why the distribution was unsustainable. It took almost three years, but RA saw our point and cut the distribution by 40%. Better late than never. With that action, it lost its raison d'etre for income investors. The exodus that followed got RA reacquainted with trading at one of its steepest discounts, which it remains close to even now. We took a look at the numbers after that carnage and chose to continue to stay out. In our opinion, the relatively low leverage was just an offset to the high interest expenses and management fees. We still thought the fund could reasonably manage 7% in annual total returns from that point onwards, provided its predominantly high yield asset portfolio did not get hit by multiple defaults. The decision to stay out was again influenced by the amount the fund was doling out to its investors.

So 7% on NAV would mean about a $1.00 annually. The fund is still going the way of overdistributing and aiming for $1.416 annually. So NAV depletion will still happen, even in the very best-case situation. At present, we would avoid buying the falling knife.

Source: RA: Brookfield Real Assets But Fake Yield

The NAV depleting distributions have helped stem most of the market price decline since then.

Seeking Alpha

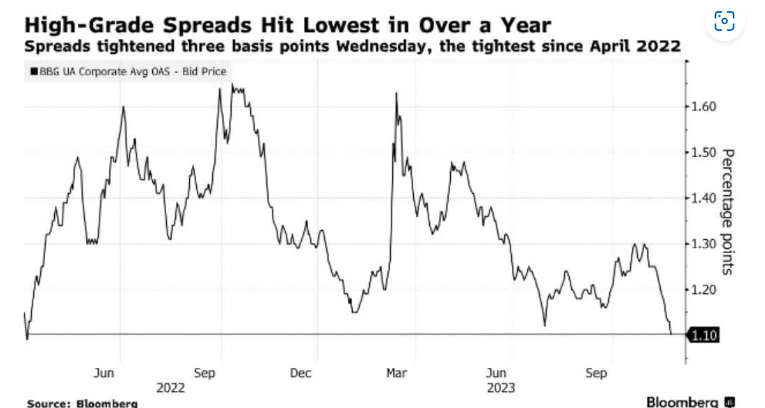

We have had a substantial rally in the high yield space recently, with the spreads tightening to April 2022 levels.

{kind=link}

Bloomberg

We take this opportune time to revisit RA. We show you why it is still not the right time to buy this Brookfield Fund and we do it by comparing it to the SPDR Bloomberg Short Term High Yield Bond ETF ( SJNK ).

Objective and Holdings

RA aims to deliver a high total return to its investors, via high current income (primarily) and capital appreciation. This closed end fund uses "real assets" such as infrastructure and real estate for this endeavor. The September 30 fact sheet showed corporate and securitized credit making up almost all of the portfolio.

RA Fact Sheet

Equities occupied a meager 2.9%, almost all of which was in infrastructure companies. In contrast, RA had 28.4% in equities when we covered it in August. While, neither the information we have today (September 30), nor what we had access to back in August, was most up to date, it shows RA is moving in the right direction (in our opinion). The fixed income tide is overwhelmingly the safer one than that of equities in the current environment. The fund held 536 securities at the end of September (332 at July 31).

RA Fact Sheet

With the top 10 making up around 11% of the total, there is little to complain about in terms of holding level diversification. Alongside RA's move away from equities, there has been an increase in the average coupon (previously 4.30%) and duration (previously 1.72 years). The corporate credit is trading well under par, unlike the $100.16 average dollar price we saw during our prior coverage. The investment grade exposure has come down from 23.8% to 19.4%.

RA Fact Sheet

With a preponderance of high yield credit of the corporate kind, RA continues to represent a high yield bond fund to us. Speaking of which...

SJNK is a passive ETF that pursues that performance of the Bloomberg US High Yield 350mn Cash Pay 0-5 Yr 2% Capped Index. The fund fact sheet expands on the various components of the index name.

The Index includes publicly issued U.S. dollar denominated, non-investment-grade, fixed rate, taxable corporate bonds that have a remaining maturity of less than 5 years regardless of optionality, are rated between Caa3/ CCC-/ CCC- and Ba1/BB+/BB+ using the middle rating of Moody's Investors Service, Inc., Fitch Ratings Inc., or S&P Global Ratings, respectively, and have $350 million or more of outstanding par value.

Source: SJNK Fact Sheet

SJNK employs sampling to select the index components for its portfolio. Generally, the ETF has at least 80% of its total assets invested in the index securities or those that are deemed by the advisor to be of comparable quality. It has done a decent job of tracking the index over the years, especially considering the fund has expenses (0.40%/year), unlike the index.

{kind=link}

SJNK

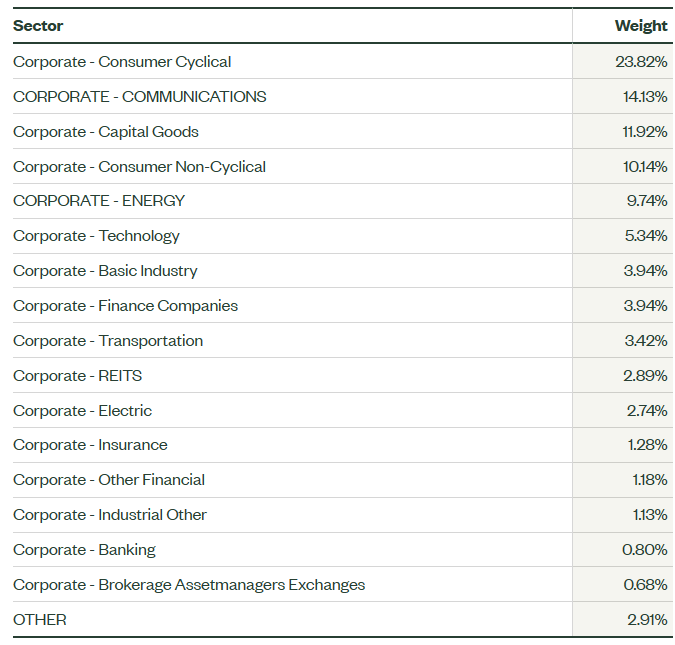

According to the most recent data published on the fund website, over two thirds of the SJNK assets are concentrated in corporate credit of the consumer goods, communications, capital goods and energy sectors.

{kind=link}

SJNK - Dec 4

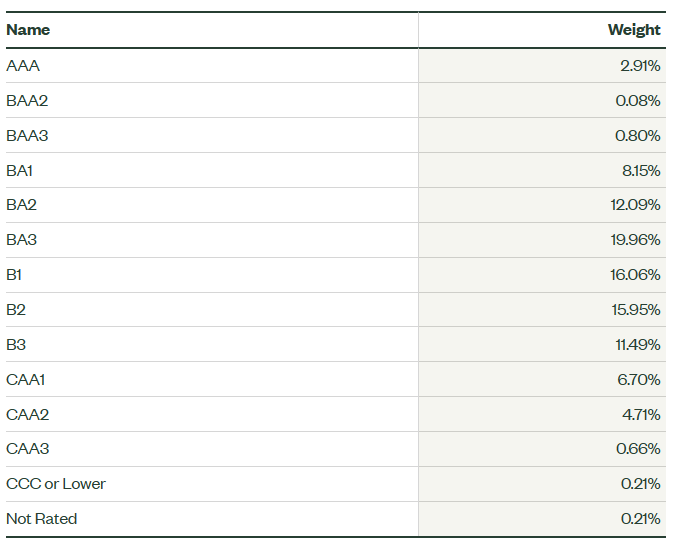

Real Estate has a meager 2.89% presence in SJNK's portfolio, in contrast to what we saw for RA. Almost all of the portfolio is in high yield securities, with a token 4% in investment grade counterparts.

{kind=link}

SJNK - Dec 4

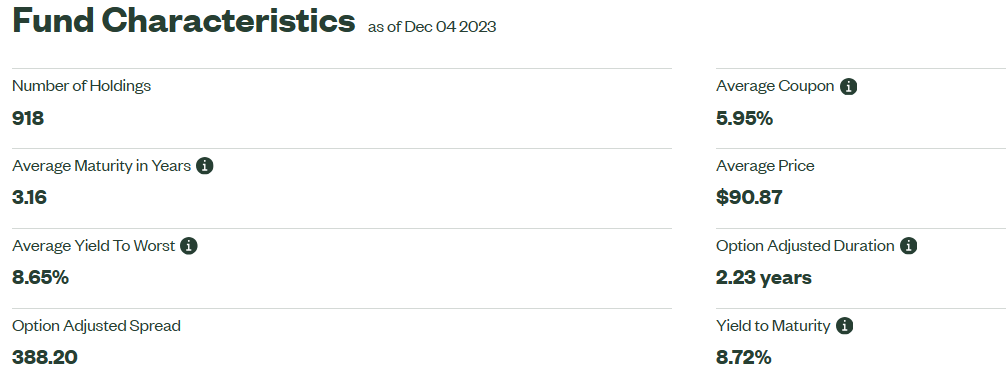

No judgement here, as we already know that SJNK is a passive ETF and its overarching goal is to replicate the performance of its high yield benchmark. The fund's 918 holdings have an average maturity of 3.16 years.

{kind=link}

SJNK

While the average coupon is 5.95%, the yield to maturity is 277 basis points higher at 8.72%. The yield to worst is not far behind at 8.65%. The difference between the coupon and the yield to maturity makes sense when we see that collectively the portfolio holdings are trading close to $9 under par. The duration risk is not much to speak of and is in the same ballpark as that of RA. The 2.23 years in duration risk signifies the extent to which the SJNK portfolio value will decline (2.23%) with a 100 basis points increase in interest rates, and vice versa. This of course, assumes that the credit risk remains unchanged and s**t does not hit the fan.

Leverage

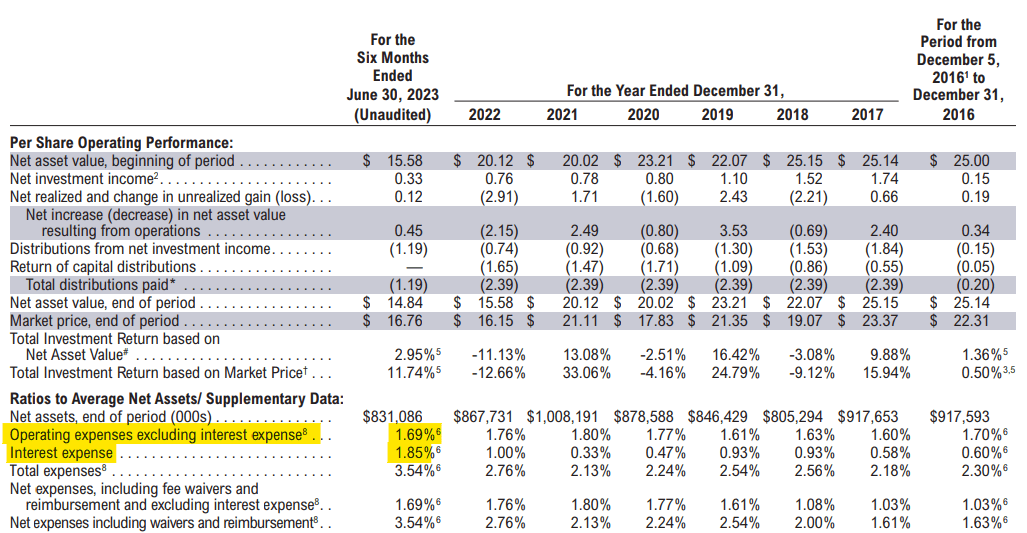

RA uses leverage ( around 17% of gross assets ) to enhance returns, and as we noted in our previous piece, we like that it is on the lower side compared to its peers. The majority of the borrowings originate from a credit facility, and that bore a weighted average rate of 5.74% for the six months ending June 30, 2023. The interest expense actually surpassed the operating expenses for that reporting period.

{kind=link}

RA Financial Report

As we noted in our earlier piece, Management fees (around 1.3%, included in the OPX above), along with the high interest expenses, offset all the benefit of having a low leverage.

SJNK does not have any leverage.

Mano A Mano

Performance

So investors are paying close to 3% in annualized expenses for holding RA, and 0.40% for holding SJNK. RA returns must be worth it on the face of it. Does not appear so over the last decade at least.

Maybe a shorter timeframe of perhaps three years? Close, but still no cigar.

SJNK extended the lead over the last year. It broke out from the coupling in April and RA has not been able to catch up. The momentous dividend cut in August did not help.

There is one clear winner in terms of performance on NAV.

Distributions

In terms of distributions, RA currently pays 11.80 cents/month, which using the market price of $12.73, yields the fund investors around 11.12%. On an NAV basis ($14.66), it yields slight less (9.65%), as it trades at a discount. We think it reasonable that RA assets return around 7% in total return to investors, provided the defaults remain mild in this high yield portfolio. The current distribution on NAV is still higher than the earning power of this fund, so the NAV will continue to deplete with ROC forming a portion of the monthly payouts.

SJNK on the other hand has a variable monthly distribution, which is based on the net earnings. The last declared distribution is in the amount of 14.78 cents, which gets us to an annual yield of 7.14%. As shown above with the yield to maturity, we can expect about 8.72% total, but that is assuming there are zero defaults, not an assumption for this stage of the cycle.

RA wins this round (if you just compare yield), but the cost to investors that can glean the implications of NAV depletion are high.

Outlook and Verdict

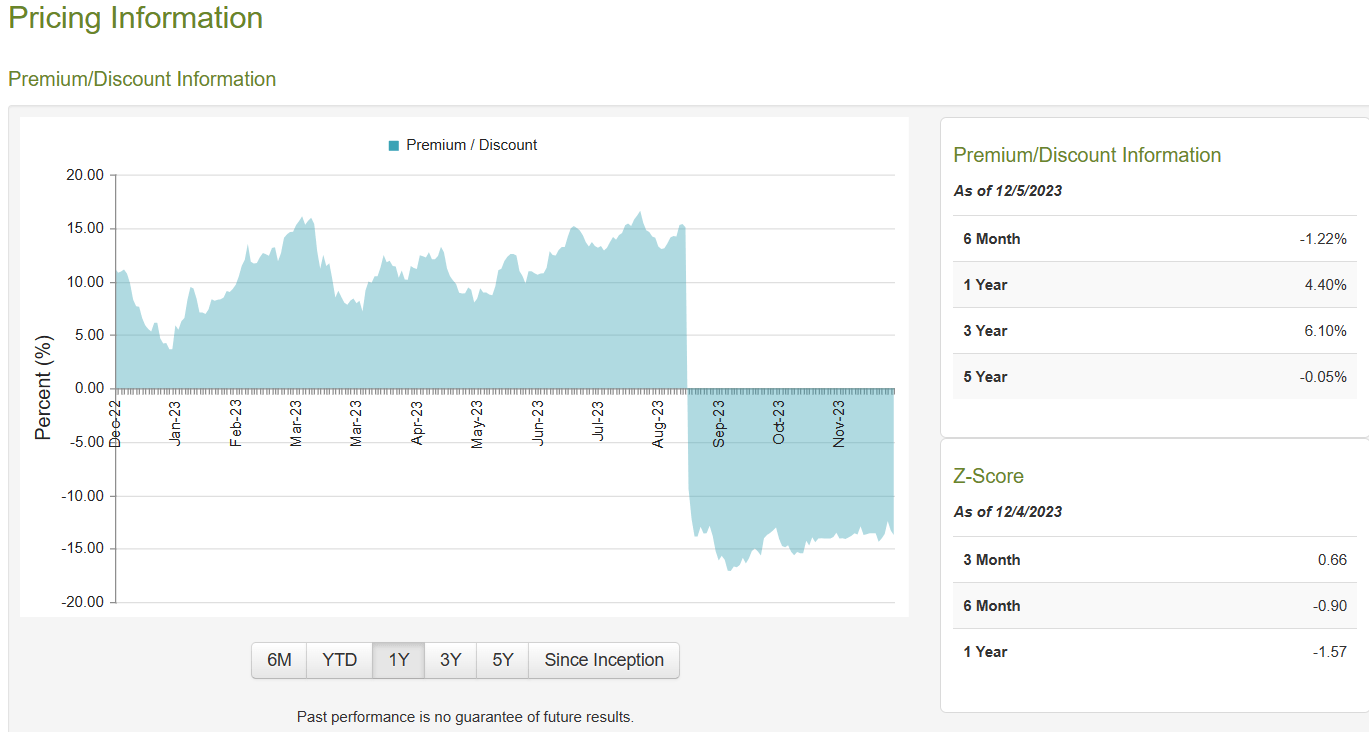

Based on the prior two sections, our readers probably expected us to espouse buying SJNK over RA. We are not interested in buying SJNK at the moment, so the point of the piece was, why would we even go for RA considering how it compares to SJNK. One thing going for RA is that one can get it at a steep discount.

{kind=link}

CEF Connect

RA just did not cut its distribution sufficiently back in August and still continues to overdistribute. We like the low levels of leverage though and that was one reason for our only high yield CEF purchase some time back . Overall, we need the above blue wave to hit negative 20% before we consider a purchase. If that happens in conjunction with a high-yield spread blowout, consider us sold. We continue to stay out.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

Brookfield Real Assets Vs SJNK: Birds Of A Feather