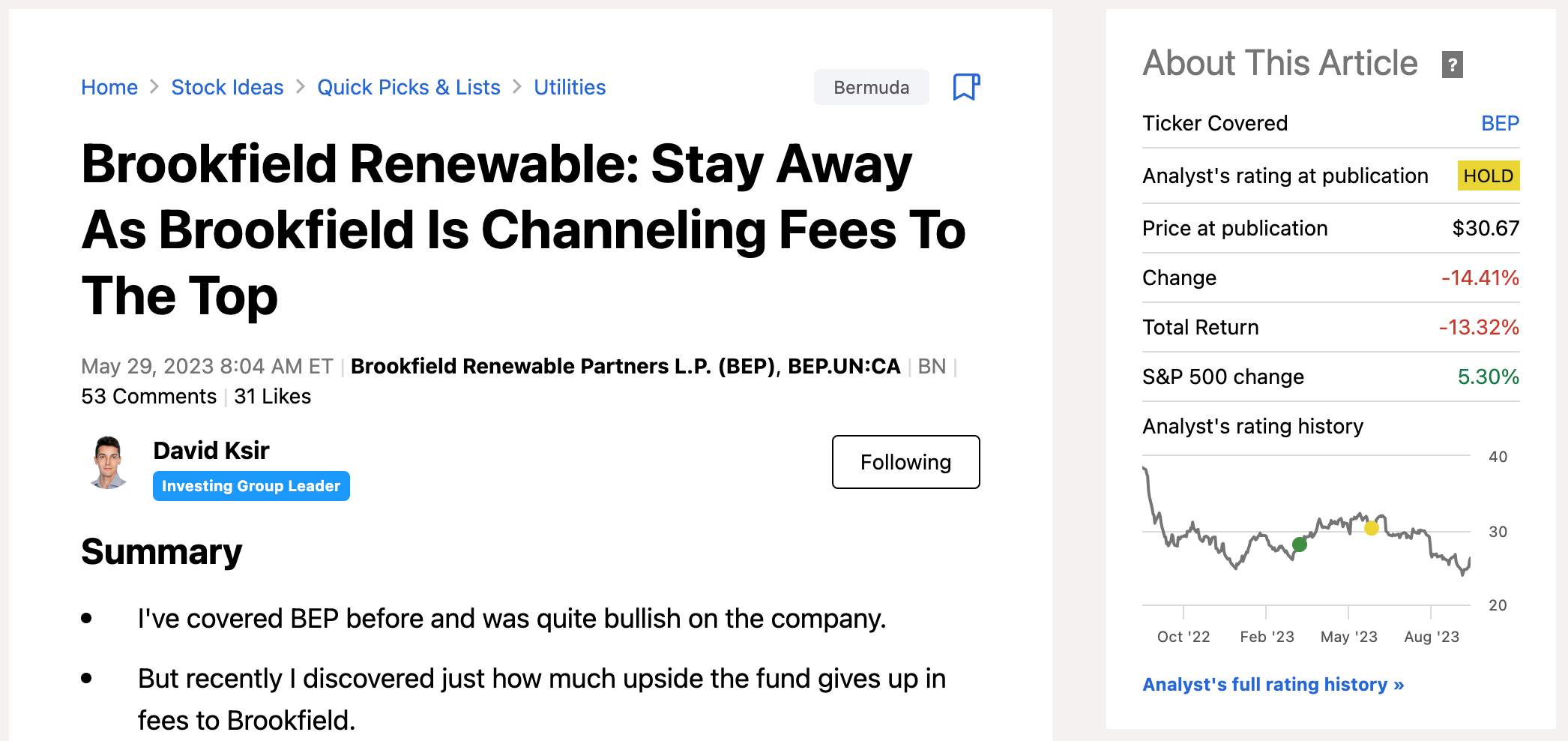

BEP - Brookfield Renewable: Not Worth It On A Risk Adjusted Basis

2023-09-19 08:42:26 ET

Summary

- BEP owns a world-class portfolio of assets with high hydro exposure.

- The company is well positioned to deliver 11% returns, in line with its historical performance.

- I suggest an alternative with a 20% expected return and a similar level of risk.

Dear readers,

Last time I downgraded Brookfield Renewable Partners L.P. ( BEP ) and suggested that investors look into buying Brookfield Asset Management ( BAM ) instead.

{kind=link}

Seeking Alpha

My reasoning was mainly based on the fact that management is clearly incentivized to maximize value at the asset manager level, which in turn maximizes value at the Brookfield Corporation ( BN ) level which is where management is invested the most. BAM consumes about a third of BEP's returns, by charging BEP significant management (1.25%) and performance (3.5%) fees. Combined these fees reduce the return potential of BEP from their 15% targeted ROE to about 10% per year.

Since that article, shares of BEP have dropped by 15%, while shares of BAM have appreciated by 16%. Of course, my call was long-term in nature and this short-term divergence was caused by multiple catalysts/trends beyond the scope of my original article, but it's good to see that so far, my thesis of investing in the asset light BAM is paying off.

Following this divergence in price and in particular a now lower valuation of BEP, as well as their recent Q2 earnings , I want to present my updated thesis for the company.

Note: BEP and Brookfield Renewable Corporation ( BEPC ) represent the same ownership interest in the underlying business. Throughout the article, I will be referring to BEP, but everything applies to BEPC as well. The only difference between the two entities is tax treatment (LP vs. a C-corp) and price as the corporation trades at a slight premium.

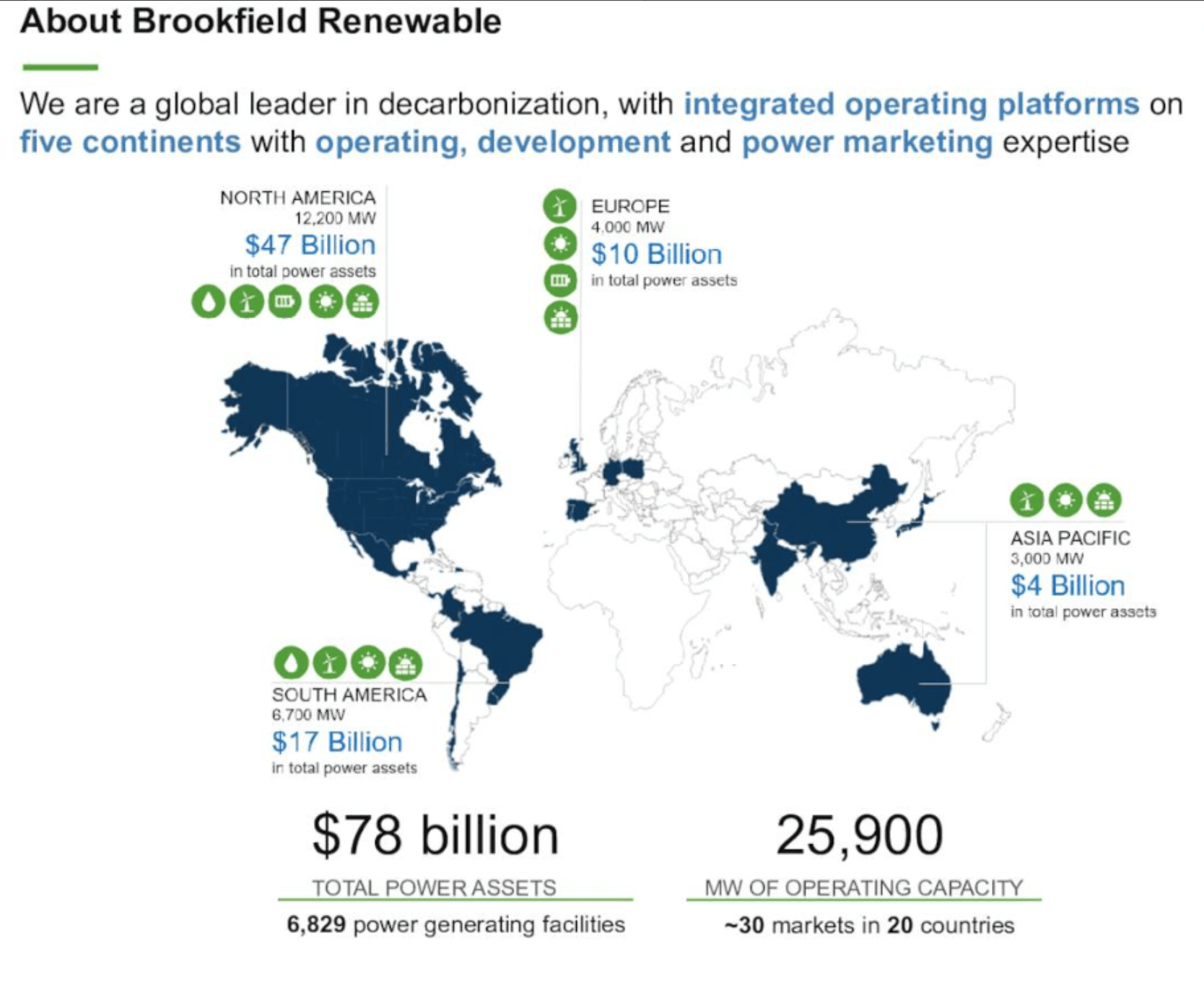

Brookfield Renewable Portfolio

Brookfield Renewable is a major renewable energy production player on a global scale. The company owns 26,000 MW of operating capacity located across 20 different countries with a heavy focus North America (63%), followed by South America (20%) and Europe (15%).

{kind=link}

BEP Presentation

What really sets BEP apart from other renewable energy players is their heavy involvement in hydro (53% of capacity) as opposed to just focusing on wind and solar which account for 20% and 15%, respectively.

New wind and solar projects are easy to build, which makes expansion easier, but also increases competition. For hydro power plants, there are only so many places where they can work and most of those places are already taken. This makes hydro assets much more valuable, especially in the long-run. Moreover, hydro provides much more stable generation capacity.

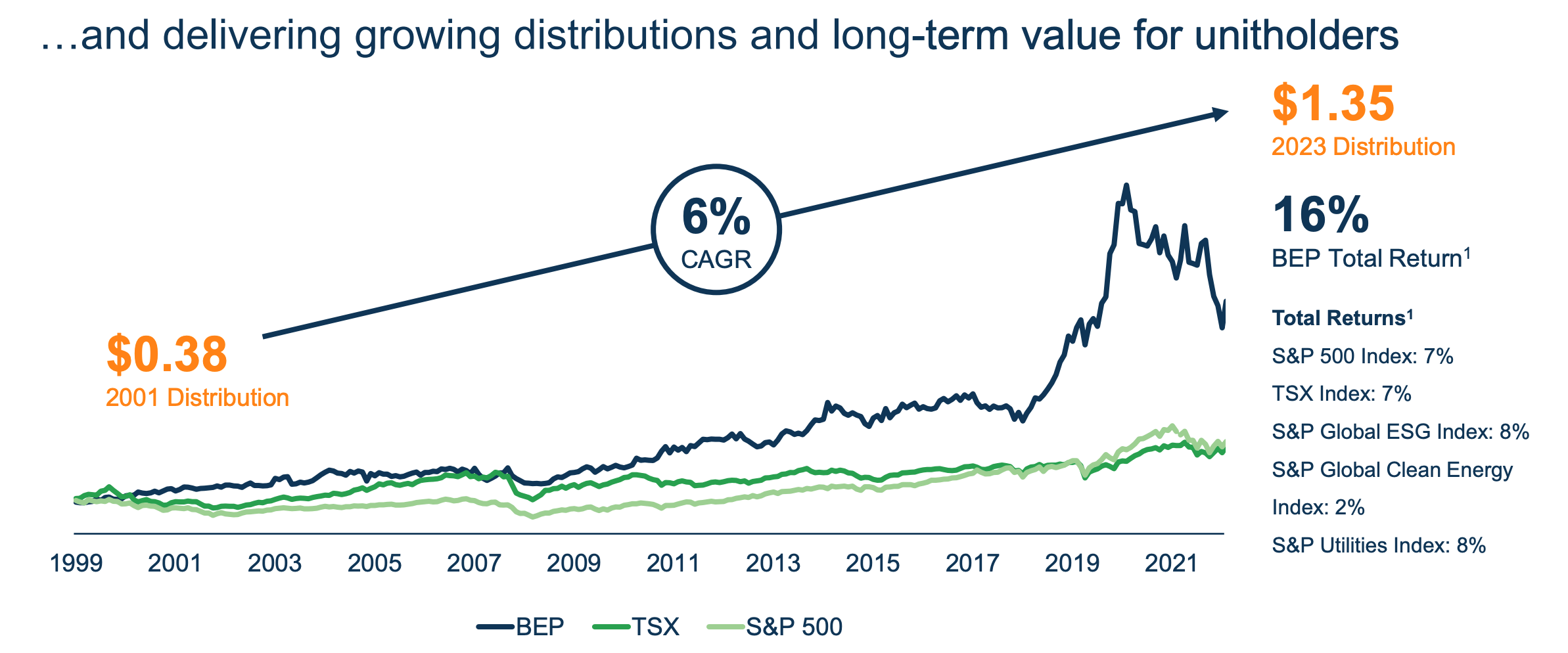

Growth Prospects

BEP's high quality assets and top management have enabled them to deliver on their growth targets very consistently. In particular, distributions have grown by a CAGR of 6% over the past 20 year, which is in line with the company's target of 5-9%.

{kind=link}

BEP Presentation

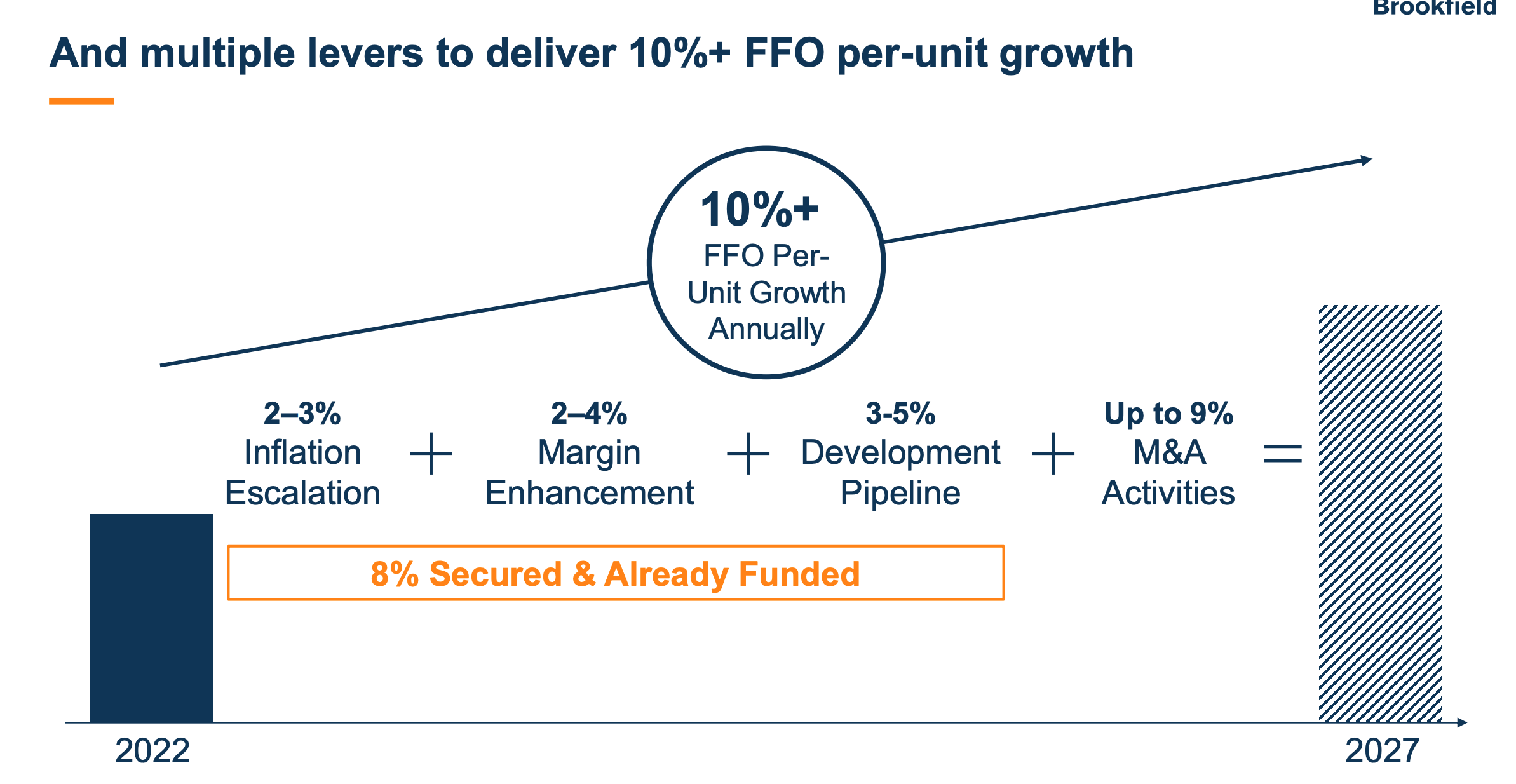

And going forward, growth in FFO per share is expected around 10% per year, thanks to inflation escalation, margin enhancement and a sizeable development pipeline which has doubled from last year and now stands at 132 GW.

Notably, growth visibility is very high. BEP has 16 GW of projects under development that will be commissioned within the next three years and with a large portion of newly added capacity already contracted, management estimates that 8% annual per FFO per share growth is already locked-in until 2027.

{kind=link}

BEP Presentation

BEP has the experience, pipeline and necessary liquidity ($3.9 Billion) to grow their production capacity. And importantly, demand is expected to be very strong as well, driven by:

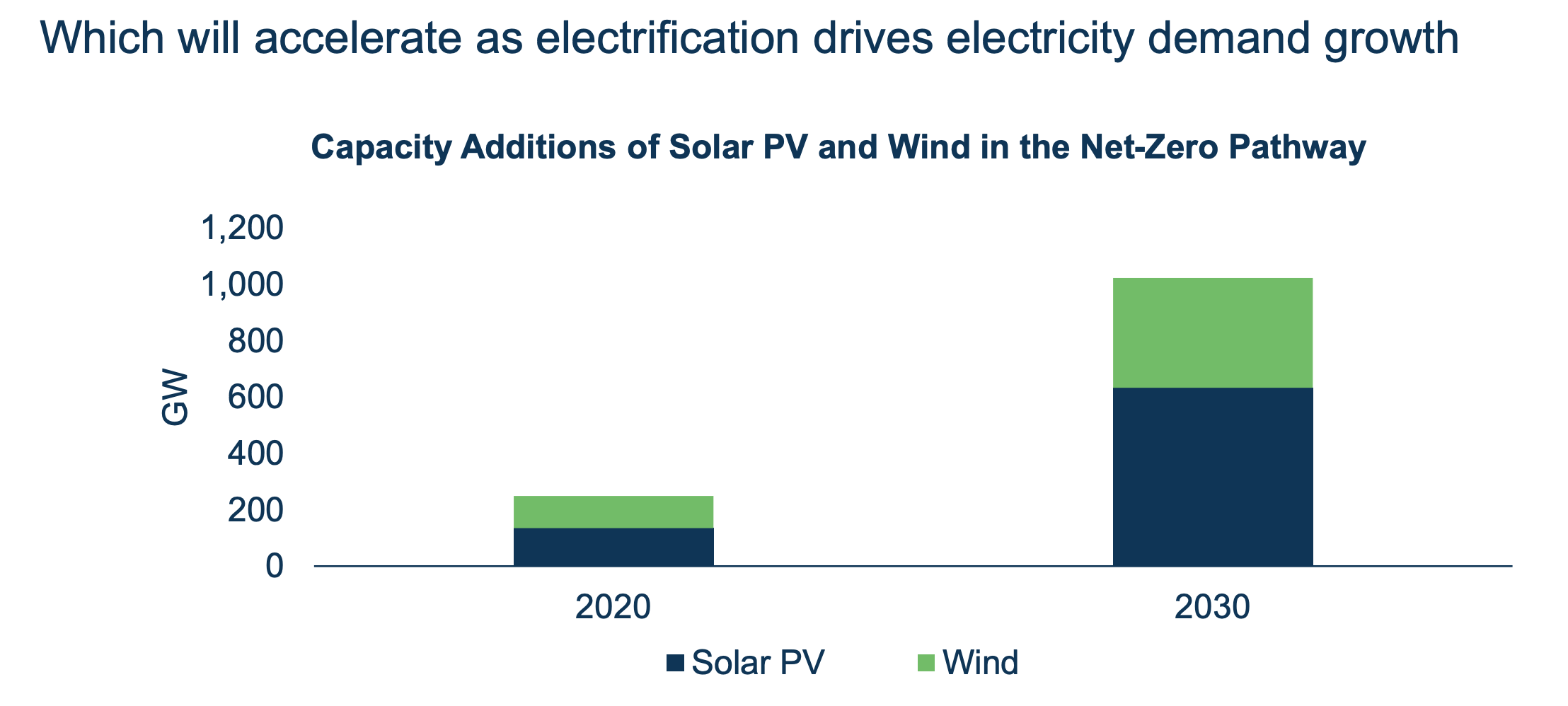

- government's net-zero initiatives which are expected to increase solar and wind energy demand by 4x .

{kind=link}

BEP Presentation

- big tech firms which, according to the earnings call , are expected to increase their demand for renewable power by a factor of 3x in the latter half of this decade. The growth is expected to come from generative AI which requires immense amounts of energy. For perspective, it is estimated that if just one big tech company decides to go 100% renewable, their demand for power by 20230 could equal the demand of the entire United Kingdom today.

Valuation and Verdict

BEP pays a 5.2% dividend yield, which is well covered with a payout ratio of about 70%. Going forward, it's fair to assume that dividend growth will continue at 5% per year or more (management target 5-9%).

On top of the dividend, if management can hit their 10% FFO per share growth target, shareholders will earn additional return of about 6%-7% as the rest gets channelled to BAM in form of performance fees.

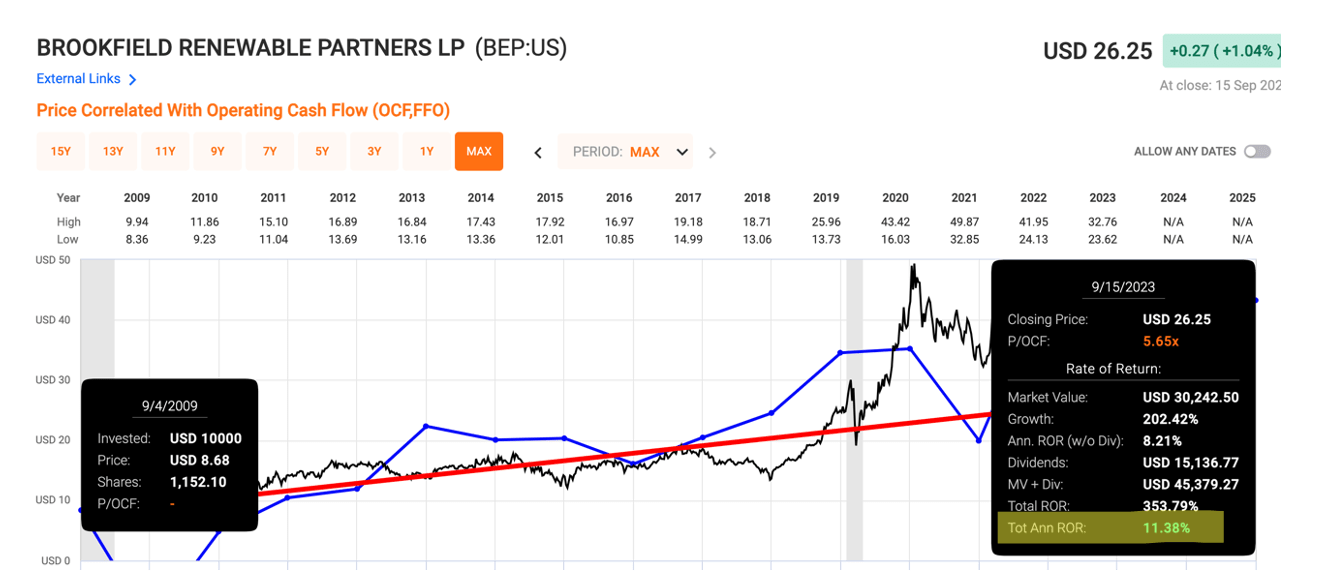

5.2% dividend + 6% from upside = 11% total annual return which is right in line with what the stock has deliver on an annual basis since 2009.

{kind=link}

FAST Graphs

Of course, growth is not guaranteed, but all things considered, I see returns of 8%+ as very likely and if all goes well 11% is quite achievable. Anything above 11-12% is quite unlikely as most of the upside beyond that point is shared with BAM. That's not bad. If you're looking for a renewable energy pure-play and these returns are good enough for you, by all means go ahead and buy BEP.

Personally though, I think investors can do better with BAM, with very little added risk, which is why I rate BEP a HOLD here at $26.25 per share.

I've published on BAM most recently here and outlined a clear path to 20% annual returns. That's almost double the return of BEP with a still solid dividend yield of 3.5%.

And honestly, I consider BAM less risky, because:

- it is asset-light

- it is more diversified (renewable energy, infrastructure, private equity, real estate and credit)

- it is more aligned with management's incentives

The bottom line is that the Brookfield empire is interconnected and one entity cannot function without the other, but BAM offers a better risk-adjusted return than BEP, in my opinion.

For further details see:

Brookfield Renewable: Not Worth It On A Risk Adjusted Basis