KKR - Brookfield: Transparently Bullish Analysis So You Can Decide For Yourself

Summary

- We demystify the Brookfield universe and business model, revealing it to be like Warren Buffett's Berkshire Hathaway in structure, quality and long-term returns, but with some important differences.

- Brookfield Corporation, or BN, is quite undervalued, but justifiably so, as it is complex and relies on management execution regarding asset allocation and market re-valuation.

- Brookfield Asset Management, or BAM, is more fully priced, but deservedly so, as it’s growing faster, its dividend is better, and its future revenue is more predictable.

- Both Brookfield entities appear ready to return at least 15% annually into 2027, with more upside possible.

- Unless you’re a financial oracle or insider, which Brookfield stock you choose is mostly a matter of preference at current prices.

Introduction

I intend to qualitatively and quantitively exhibit my reasons for being a buyer of both Brookfield Asset Management Ltd. (BAM) and Brookfield Corporation (BN) at these levels. The result is somewhat lengthy and thorough, but I hope readable and beneficial to retail investors like myself. My goal is that instead of adopting someone else’s opinion, you can make your own. Let’s begin!

The Brookfield Universe

The Brookfield universe can be intimidating. Firstly, their business operates in what is called alternative assets, which sounds suspicious to begin with. Secondly, Brookfield has multiple publicly listed companies besides BAM and BN, namely (BIP), (BIPC), (BEP), (BEPC), and (BBU). What does that all mean? Additionally, the parent company BN can’t be valued using any traditional metric except dividend yield, which is less than ideal. Despite this, Brookfield Corporation has returned almost 20% annually over the last 20 years, like the performance of another complex but worthwhile company we all know.

Berkshire Hathaway, Inc., Warren Buffett’s famous conglomerate, despite being monstrously complex, functions very simply. Operating businesses (like See’s Candies, Dairy Queen, or the BNSF Railway) and insurance operations (like Geico) send excess cash flow to Omaha, where Warren and Charlie Munger reinvest it with legendary success.

Graphic depicting Berkshire-Hathaway's business model (Author's Creation - Made in Word)

Brookfield is much the same. Operating businesses (infrastructure, renewables, real estate, private equity, and credit) and insurance operations in Brookfield Reinsurance Ltd. (BNRE) funnel excess cash flow into the hands of Brookfield’s Warren and Charlie, the asset manager BAM, which invests it at similarly legendary rates of return. Berkshire and Brookfield both use their eco-system to efficiently allocate capital with great success.

They have their differences, however. The most significant difference is that Brookfield’s manager, BAM, doesn’t just manage its own capital, it also manages other people’s capital, too, for a fee. It would be as if Warren and Charlie went about and said, “Hey, since we’re investing all the time anyways, we’re going start a fund on the side. Want to be a part of it?” You can imagine how successful that would be; Brookfield does exactly this. They charge significant fees for this service (1%), which are usually recurring and predictable because the money, once committed, is locked up for 5-7 years in private, illiquid assets. Additionally, Brookfield is more willing to sell assets it owns that have significantly increased in value and re-allocate that capital to higher return endeavors; they recycle their capital. In short, Brookfield has additional capital generation levers that Berkshire does not.

Brookfield's business model - much like Berkshire-Hathaway, but with a few more sources of investment capital (Author's Creation )

This is Brookfield: recycle capital, re-invest cash flows alongside other’s people money (for a fee), repeat.

Alternatives is the name for this industry, but it is perhaps a misnomer. By alternative assets, we really mean all that is not cash, stocks, or bonds. Until two years ago, I had never looked at the stock market, and if you’d asked me then what alternative assets were, I would have said stocks and bonds, not property, data centers, or nuclear power plants; stocks and bonds seem more abstract and "alternatives" more real.

The financial world thinks differently. As of now, around $200T is invested into stocks and bonds, while just $13T is invested into alternative (real) assets today. The opportunity is clearly large and in its infancy. Slowly, the traditional mindset of allocating towards stocks and bonds is beginning to change, allocation to real assets is increasing, and Brookfield and its alternative asset management peers are ready to benefit from this development.

Alt assets have considerable room to grow, as this graph illustrates (Author's Creation - numbers from SA Author Alex Steinberg)

Brookfield is particularly well-placed because, where some alternative asset managers are leaders in property (Blackstone ( BX )) or private equity (KKR & Co. ( KKR )), Brookfield is the undisputed leader in green energy and infrastructure investing. With decarbonization and de-globalization as major drivers of the economy going forward, Brookfield is at the confluence of two secular growth trends: the migration of institutional investors to real assets and the economy’s growing need for green and local infrastructure investment. One recent event illustrates this point well.

Prior to Russia's invasion of Ukraine, Brookfield’s private equity arm had bought a stake in and had been busy turning around the Westinghouse Electric Company, which supplies technology to over half the world’s nuclear power plants. The Ukraine invasion induced an energy crisis all over the world, forcing countries to rethink their energy dependencies and sources; nuclear was suddenly back on the table. Brookfield seemed to have been planning for this development.

Another branch of Brookfield and Canadian uranium miner Cameco (CCJ) bought 51% of the Westinghouse for around $8B. Shortly thereafter, in a move to decarbonize and deglobalize energy production, Ukraine signed a deal with Westinghouse to build more nuclear reactors in order to reduce Ukraine’s reliance on Russian power while decarbonizing its energy sources. In this case, we can see that Brookfield's unique expertise dovetailed well with trends in green energy investment and infrastructure localization.

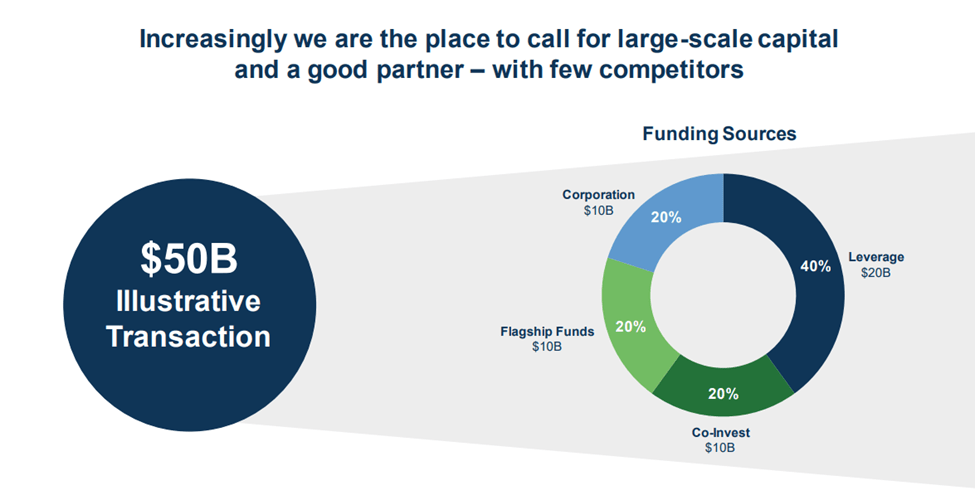

Access to investment capital is another aspect that sets the big alternative asset managers like Brookfield apart; scale is a huge competitive advantage. One might think that if the infrastructure and alt asset space is so promising, tons of new competitors would arrive on the scene. For smaller deals, this may be true, but mega deals, like $15B in financing to build Intel’s Arizona chip factory or $17B to acquire half of Germany’s telecom towers have much fewer suitors. Brookfield, according to its Q3 supplemental, has the second most assets under management ("AUM") of alternative asset managers, at $750B, and as of the end of Q3, Brookfield had $125B of funds ready to be put to work and a balance sheet (at the BN level) with next to no debt. To put that in perspective, Brookfield has more liquidity than Alphabet (GOOG), a company 20 times the size, with only a little more debt; very rarely does a company have this kind of financial profile. Combine this scale of investment capital with its operating expertise and long track record of investing success, and we can see the Brookfield moat is very wide indeed.

One aspect of companies that I like to pay particular attention to, largely because some investors who have influenced me frequently make this point, is management’s alignment of interests with investors. This is usually achieved by significant insider ownership. A cook who eats his own cooking is better than one who doesn’t; he is less likely to neglect or poison the food and much more likely to do his best. At Brookfield, the CEO and effectively founder of the alternative asset management strategy 25 years ago, Bruce Flatt, has billions of dollars of personal net worth wrapped up in the Brookfield Corporation. The CEOs of its various subsidiaries all own and periodically buy significant chunks of stock as well. In addition, because Brookfield also invests money from institutional investor partners, it aligns interests by putting significant amounts of its own capital in its own funds. This is unique in the alternative asset manager space, as far as I am aware. Brookfield goes to great lengths to align its interests with its partner investors and shareholders. I take great comfort knowing my cook is serving himself the same food he’s serving me.

This is of particular importance because my account up until now could be perceived as too good to be true. I readily accept this criticism, and in fact hold it myself. I continue to investigate, even perusing footnotes of Brookfield’s quarterly reports looking for off-balance sheet derivatives and such. Thus far, nothing is concerning but I remain wary. Whenever a new asset class is doing exceptionally well, it becomes a prime candidate for corruption, even if the original idea itself is good. We need not look further than mortgage-backed securities in 2008 for a clear example. Take a really good idea, packaging up quality mortgages into a bond-like security for risk-averse investors, then corrupting that idea by mixing in worse and worse quality mortgages, keeping the credit ratings the same, then selling derivatives that allow investors to bet on the success or failure of these securities. If the big banks who partook in these trades on behalf of clients had their own personal wealth on line, instead of being given bonuses for getting deals done, would they have done more due diligence on the actual products they were hawking? I expect so. In the alternative asset management space, Brookfield uniquely counteracts this danger by going to great lengths to align its interests with shareholders and investing partners, which provides a great hedge against unforeseen risk. I remain alert however, and should signs of irrational exuberance show themselves, Brookfield is a sell.

A second concern is leverage. One of the first things investors learn (usually the hard way) is that leverage can be used to enhance returns but also increases the risk of losing it all. We are trained to avoid companies with excessive debt for this reason. Though Brookfield Corporation - BN - itself has very little debt at the top, the individual projects and funds it operates, do. This would be concerning, but because Brookfield was recently upgraded to an A credit rating (a rating similar to that of developed countries), it can get debt at relatively low interest rates.

Additionally, this debt is also almost entirely long-dated and fixed-rate, meaning temporary changes in interest rates are not too concerning. The way Brookfield structures its debt is most important, however: default-risk is limited to the individual project, not the company as a whole. Meaning that in the case a project goes belly up and/or they can’t afford the debt they used to finance it, the bank simply seizes the asset, rather than have the bank move up the corporate chain for the money it’s owed. They call this “non-recourse” debt and is the primary reason the total debt used in the Brookfield universe is not systemically concerning. That said, an investor not comfortable with even low-cost, fixed-rate, long-term, non-recourse debt should not buy Brookfield.

An illustration of how a typical Brookfield investment is funded. Note the leverage, corporation contribution and investment partner contribution (from Flagship Funds), we discussed in the last two paragraphs (Brookfield Investor Day Presentation)

{kind=link}

The Brookfield universe, though the business model is simply an enhanced version of Berkshire-Hathaway, remains complex, shadowy, and intimidating to retail investors like me. I’ve done my best to elucidate readers to the reality (as I understand it), but a summary is in order.

Brookfield’s business, alternative asset management, is not alternative at all. It is better described as real, as they deal in very concrete assets like pipelines, railroads, data centers, telecom towers, nuclear plants, offshore wind, and solar farms. I mention these examples because infrastructure and green energy are Brookfield’s specialty, and also at the center of important global trends, namely localization and decarbonization. Brookfield’s moat is dug by this expertise, in addition to its tremendous scale, Buffett-esque track record of returns, deliberate alignment of management with investors/shareholders, and global reach. Growth going forward is not slowing, as institutional investors are significantly underweight real assets in their portfolios; the party is just getting started, as they say. Where there’s a profit party though, there is risk.

Brookfield’s moat will keep out many smaller competitors, but investors should keep an eye out for irrational exuberance from asset managers and overuse of leverage. With that in mind, owning Brookfield gives investors exposure to a high quality, unique name in real assets that the global economy relies upon to function and grow, which would otherwise be inaccessible to small-time investors like myself. For me, Brookfield is as essential to my portfolio as its assets are to the functioning of the world.

So how do we get exposure? As I mentioned at the start and showed in the graphic illustrating the business model, Brookfield has numerous subsidiaries trading publicly. We really ought to focus on only two, however: Brookfield Corporation - BN - which is essentially an exchange-traded fund ("ETF") for everything happening at Brookfield and thus extremely attractive for all the reasons outlined above; and the newly spun-off Brookfield Asset Management - BAM - which, as the graphic showed, is to Brookfield what Warren Buffett is to Berkshire Hathaway.

Where prior spinoffs like BIP or BEP have been simply elements of the business Brookfield uses to generate and re-invest cash flow, BAM is the mastermind of it all and earns stable, growing fees on its services. If Berkshire Hathaway were to spin-out a piece of Fruit of the Loom, investors might appreciate it, but if they were to sell Warren Buffett’s services and offer investors a way to invest in that enterprise, there might be a stampede to Omaha in such numbers to cause the first earthquake in Nebraska. As CEO Flatt so eloquently described the spinoff , “This one’s a big deal.” So, what do we want, BN or BAM?

BN vs. BAM - Valuations and Expectations

Because both are excellent, the simple answer is whichever one offers a clearly better risk-adjusted return, and if the return profiles are similar, then own both. For those who prefer a short story, owning both is the conclusion I come to. For those, who, like me, prefer to know the reasons behind one’s conclusions, then read on.

A slightly more nuanced answer calls attention to a couple factors other than valuation. Though part of the same business, BAM and BN are dramatically different stocks. BAM is what analysts refer to as “asset light,” meaning they have little capital of their own invested (implying they provide a service) while BN is “asset heavy,” meaning they invest lots of their own capital. BAM is significantly less complex, their earnings are more predictable and growing faster, their dividend yield and dividend growth rate are higher, returns on capital will be higher (since they have so little capital), and debt will be negligible. When you look at BAM on a finance website like Seeking Alpha, all its charts are going to be up and to the right. In a word, BAM is sexy.

Contrast this with asset-heavy BN, whose corporate structure is difficult to understand, whose earnings are lumpy, whose returns on capital vary, whose debt can appear extreme, whose dividend yield is low, and whose growth is slower. When you look at BN on Seeking Alpha, even if its returns have been 19% for the last 20 years, BN appears the cross-eyed, yet hard-working, cousin of sexy BAM. As such, I expect BAM will spend a lot of time overvalued while BN will languish in its shadow, perpetually undervalued to a varying degree. Pure value investors will appreciate BN, growth and dividend investors will gravitate towards BAM, but all investors will benefit.

Whatever your preference, it’s important to firstly not overpay, and secondly, know what expectations are in your price. In short, we need to value our options.

BAM is relatively easy to value because its cash flows are so transparent and predictable. Management guided $4.4B in fee-related earnings by 2027, and almost $1T of fee-bearing capital in that year. Though we haven’t had an earnings report from them yet, they have declared their first dividend, an annualized $1.28, and we can look back in Brookfield reports to see BAM’s financial history. BN has retained 75% of BAM and all the carry (bonuses earned by funds’ outperformance), but in the future BAM will be entitled to two thirds of the carry earned. Below is the result:

BAM Valuation (Author's Calculation)

Before we get excited by the 20% annual return over the next five years, let me explain my assumptions and exclusions, so we can get a sense of what this means. I assumed a multiple on FRE of 25 because with BAM growing at roughly 20% and having a 3-5% dividend yield, we arrive at a rough (and round) PEG nearing one. There’s no reason this multiple can’t go higher or lower, but I expect it to hover around 25.

I excluded carry because they have none so far, it tends to be lumpy, and the market will likely price BAM based on a multiple of FRE anyways. Its exclusion however does mean that when/if carry is realized, it means further upside that’s not priced in. We also don’t know the exact financials for 2022, and the recent dividend declaration of $1.28, with a 90% payout ratio, implies significantly more than the $2.1B of FRE in the last twelve months. We don’t have the explanation, so I kept assumptions conservative, but again, if BAM is making more money than we expect, then of course it should be worth more. Lastly, buybacks have been excluded, despite the fact BAM initiated a buyback program almost as soon as it was spun-off. Its price was down significantly then but has bounced hard. As a result, I’m not sure whether they’ll execute on the buybacks so I didn’t include them. Again, further upside potential.

Given all this, if we require a minimum return of 15%, BAM at around $32/share provides a reasonable margin of safety to make up for any mistakes in these assumptions and exclusions. The price is getting close to needing perfection to return 15% (“Fair Value”), so I wouldn’t buy it past $35-$36/share, especially if potentially better options exist.

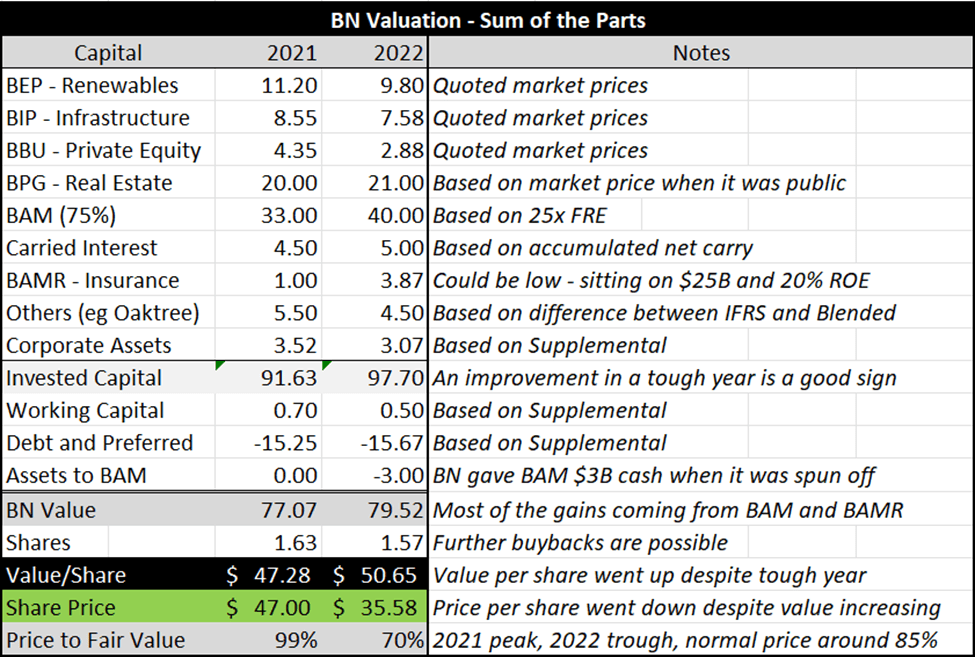

BN is a potentially better option. Unfortunately, like Berkshire-Hathaway, it is also significantly more difficult and controversial to value, indeed that’s one of the reasons it rarely has been overvalued in its history. The most commonly used method to value BN is “Sum of the Parts,” meaning we value each piece individually and add them together. This has the disadvantage of increasing the number of assumptions we must make, and at times ignoring cash flow for equity value, but it is nonetheless worth doing. The summing is below, using information from Brookfield’s Q3 supplemental:

For more opinions, you can look at Brookfield's Q3 supplemental or SA contributor Alex Steinberg's excellent articles. (Author's Calculation)

{kind=link}

Not quite as simple as valuing BAM! BN, as you can see, is basically a free ETF for everything Brookfield owns, including BAM, which makes up half of BN’s value. That’s the first takeaway from this table: buying BN is still buying a significant stake in BAM, in addition to other attractive businesses. A second important aspect to note, is that BN’s value went up while the price went down. This is a very good sign from a buyers point of view. The last thing to notice is that BN is 70% undervalued right now in the depths of a bear market, whereas in 2021, in the height of the bull market, it was fully valued; a 15% discount to fair value of the sum of the parts value is probably fair going forward. Importantly, this table does not give us an estimate of BN’s return potential, for that we need to incorporate the future:

Brookfield Corporation return potential (Author's Calculation)

Factoring in three different growth scenarios, we can see that even in the low scenario, BN returns 15% annually at the current price of around $35, thus I would suggest there is a significant margin of safety built into the current price. In a best case scenario, where BN continues to compound at 20% annually, our return is better than that stated above for BAM, but to compound at 20% BN would likely be getting a lot of help from BAM, so both would deliver returns above expectations. As such, I think the mid scenario of 15% compounding is a fair, conservative assumption, which, combined with a re-valuation, brings about a return of around 20% annually to 2027, roughly on par with BAM.

BAM’s return potential didn’t factor in several variables, leaving possible upside. The same is true with BN. Firstly, like with BAM, we didn’t factor in stock buybacks, which, if the price remains depressed (which it always seems to be), seem almost inevitable. Share buybacks are not factored into the chart above and could generate unexpected return.

Secondly, Brookfield’s insurance subsidiary (BAMR), only started two years ago by acquisition, as they were anticipating higher rates and wanted to take advantage. In the low-rate environment of two years ago, they sold all the assets the company had and sat on cash for two full years (again, Buffett-esque), waiting for higher yields into which to invest their premiums. As of the Brookfield investor day, BAMR had $40B in investable premiums, $25B of which were un-invested. Now, they’re investing it into much higher yields and making a fortune. BAMR could be severely undervalued.

Valuing Brookfield’s real estate is controversial because Brookfield thinks its worth much more than the market does. When part of their real estate portfolio was publicly traded, the market disliked it enough that Brookfield just bought it back (its dividend yield close to 8%). On the table above I put its value at roughly what the market valued it at which is 25% more than the auditor’s estimation and about 40% less than what Brookfield values it at. Uncertain indeed! As per their investor day presentation, they expect rates to be higher for longer and are considering selling some real estate assets to invest more into insurance. The prices they get for that real estate could be significantly more than I account for above. We’ll see. Because of our conservative assumption though, this re-allocation of capital is more likely to be unexpected upside.

BN’s sum of the parts valuation, like BAM’s cash flow valuation, has several variables that have been conservatively assumed or excluded which add to our margin of safety at worst, and add to our return at best. If we were to require a 15% return, the fair value of BN would be around $41/share, much higher than its current price of around $35/share. On this basis, we could conclude that BN and BAM at current prices are just a matter of preference.

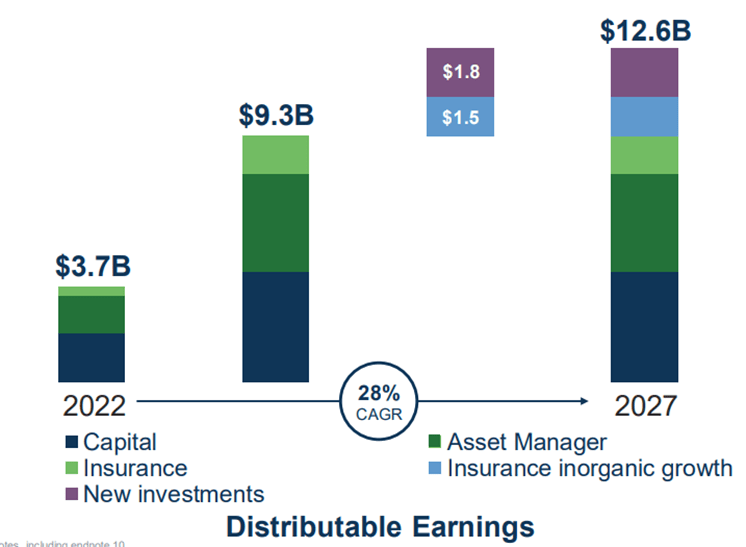

Valuing BN takes up a lot more time than valuing BAM and uses a totally different method. Might there be an easier and more comparable approach? Brookfield recently proposed one, but the market hasn’t yet taken to it. Brookfield calls it “Distributable Earnings,” which includes BAM’s fee-related earnings, all other cash flows generated for BN, less costs; essentially, DE is free cash flow (nothing is ever simple with Brookfield Corporation). Below is how Brookfield is expecting DE to grow over the next five years:

Brookfield's estimates for distributable earnings into 2027 (Brookfield Investor Day Presentation)

{kind=link}

Taking this information, we can use free cash flow to value both BN and BAM, estimate the return potential of each, and potentially have much more comparable estimates (not to mention potentially save some time). Below is that calculation:

Brookfield Corporation valued by distributable earnings (free cash flow) (Author's Calculation)

That 29% is why I don’t think the market has yet taken to this method, because if it had, BN’s price might be significantly higher than it is now. As for assumptions and exclusions, I updated DE for the last twelve months, and adjusted it for the spin-off of BAM. I assumed that a 15 multiple of earnings was fair as that’s the rate at which we expect its capital to compound (for a PEG of one). Combined with the high end of earnings potential, we could see a nearly 30% return on BN (assuming its 15% complexity discount disappears as the DE valuation method reduces that complexity). On the other hand, if Brookfield meets its low DE target, and that complexity discount remains, we’re looking at a return of closer to 18%, which is still excellent and suggests a margin of safety at current prices.

Comparing BAM and BN, free cash flow to free cash flow, BN has an edge as its margin of safety is greater and its upside higher. But it may be the case that the market decides to continue to value Brookfield Corporation the same way it always has. Is it wrong to do this? I’m not expert enough to say, but, whether this method is predictive or not, it tells me that Brookfield expects its capital to be getting more efficient. And that, as a shareholder, is something I love to hear.

To sum, BAM is currently priced around $32, and estimated to return around 20% a year into 2027, though its valuation is a little tight relative to BN, which trades at $35, and after consulting two different valuation methods, is also likely to return around 20% from this level, though this estimate is more uncertain than BAM’s. Assuming a minimum required rate of return of 15%, conservative fair value of BAM is near $35, and BN $41. Both are quality, growing and at least doubles by 2027, with the ability to be more. A pure value investor may lean more to BN, while other investors may lean towards BAM.

{kind=link}

As I side at the start of this section, because BN and BAM’s return profiles are similar and we aren’t financial prophets, it may just be best to own both.

Risks

Aside from Brookfield or one of its peers being revealed to be some sort of elaborate fraud, the main risk to Brookfield is high interest rates, for several reasons. Firstly, high interest rates make bonds more appealing as investments. Currently, the US 10-year treasury bond yields around 3.5%, still not close to the 10% yield or 20%+ return Brookfield’s funds provide, but if bonds were to supply a high enough risk-free return, Brookfield could see fewer assets coming under their management as their institutional clients opt for bonds over alternative assets.

A second reason is that high interest rates make debt more expensive. As we saw, Brookfield uses up to 40% leverage on investments, which for various reasons we went over is not too concerning, but if interest rates were to climb higher, even A-rated Brookfield would find returns slowing as their cost of capital increases. Reduced returns would likely also slow assets coming into their funds. Assets under management, capital, is essential to Brookfield’s moat and business model, and high interest rates threaten that.

Interest rates are certainly higher than they were during the pandemic, and central banks seem keen to keep them higher for longer, but historically speaking, they are still below average. Significantly, over the last twenty years, Brookfield has operated in all kinds of rate environments and been successful. In addition, Brookfield’s competitive advantages keep competition out, and its near-term fund commitments are relatively secured, with CEO Flatt even suggesting they’re mostly thinking about getting fund commitments beyond 2027. Assets under management don’t seem to be under threat as of now. But if you think rates are going into the 7-8-9-10% range, Brookfield is probably not for you.

Conclusion

I’m a buyer of Brookfield, the corporation - BN - and the asset manager - BAM - at these levels, up to $41 and $35-36 dollars, respectively. The Brookfield universe is well worth investing in because of its quality, it is invested in diverse real assets, competitively advantaged, still in the early stages of growth, and expertly managed. The Brookfield universe has been worth the effort to understand.

Brookfield is the first stock I ever bought, and the latest, with good reason. Whether you agree or disagree, I hope this was helpful.

For further details see:

Brookfield: Transparently Bullish Analysis So You Can Decide For Yourself