PDRDF - Brown-Forman: Near 52-Week Low But Not Cheap Enough

2023-03-23 17:16:28 ET

Summary

- Brown-Forman is a high-quality spirits business targeting mid-single-digits sales growth and high-single-digit EBIT growth.

- Its track record was consistent before COVID-19, but margins have fallen, in part due to a focus on investments and the long term.

- Shares have a 35.9x P/E, a 2.6% Free Cash Flow Yield and a 1.3% Dividend Yield, more expensive than global peers.

- Growth may exceed high-single-digits if its international expansion and/or Coca-Cola partnership succeed beyond expectations.

- With Class B shares at $62.43, on balance we see Brown-Forman as too expensive and wait for a better entry point. Avoid for now.

Introduction

We review Brown-Forman Corporation ( BF.B ) as its Class B shares continue to hover just above their 52-week low, having lost another 6% since the release of Q3 FY23 results on March 8.

| Brown-Forman Class B Share Price (Last 1 Year) Source: Google Finance (22-Mar-23). |

Brown-Forman has two classes of shares, the voting Class A and the non-voting Class B. Both have the same economic rights, and we prefer Class B for its slightly lower price (at present) as well as higher liquidity, and refer to it throughout this article.

Brown-Forman is a unique asset and management has a long-term growth algorithm of mid-single-digits sales growth and high-single-digits EBIT growth. Mid-single-digit sales growth has been remarkably consistent, and underlying EBIT growth averaged 9% in FY12-18. However, FY19-22 were disrupted by the U.S.-Europe tariff war, COVID-19 and then supply chain disruptions. Gross Margin has been shrinking, in part due to management keeping price increases consistent at low-single-digits. FY23 is benefiting from a rebound from recent headwinds, with underlying Net Sales growth of 8-10% and underlying EBIT growth in the high-single-digits. Future EBIT growth can potentially be even higher, as Brown-Forman expands its distribution capabilities in key non-U.S. markets and the new Ready-to-Drink partnership with Coca-Cola ( KO ) develops. Relative to FY22, shares have a 35.9x P/E and a 2.6% Free Cash Flow Yield. The Dividend Yield is 1.3%. Compared to global spirits peers, Brown-Forman has a more focused portfolio, different growth drivers but also higher valuation multiples. On balance, we see Brown-Forman stock as still too expensive and wait for a better entry point. Avoid for now.

Brown-Forman Company Overview

Brown-Forman is a U.S. spirits company with a market capitalization of $30bn. The U.S. is by far its largest market, contributing 49% of Net Sales in FY22; Developed International Markets such as Germany, Australia and the U.K. contributed another 30% of Net Sales, and Emerging Markets such as Mexico, Poland and Brazil contributed 17%.

| Brown-Forman Net Sales By Market (FY22) Source: Brown-Forman 10-K filing (FY22). NB. FY ends April 30. |

Travel Retail was 3% of Net Sales in FY22, but its sales of $104m was 26% below pre-COVID FY19.

Whiskey is by far the largest category, representing 79% of Net Sales in FY22, followed by Tequila (9%).

| Brown-Forman Net Sales By Category (FY22) Source: Brown-Forman 10-K filing (FY22). NB. FY ends April 30. |

Brown-Forman’s Whiskey category consists primarily of American Whiskeys, in particular the Jack Daniel's family of brands, which includes the classic Jack Daniel's Tennessee Whisky, flavored varieties such as Jack Daniel's Tennessee Honey, as well as Ready-to-Drink (“RTD”) and Ready-to-Pour (“RTP”) products.

Other American Whiskey brands include Woodford Reserve and Old Forester. Brown-Forman also has some Irish whiskey and Scotch whisky brands but their volumes are modest.

Its Tequila category consists mainly of the Herradura and el Jimador brands. The Vodka category consists primarily of Finlandia, a regional brand important in some countries (including Russia). It has also acquired a number of gin and rum brands since 2022.

| Brown-Forman Depletions By Brand (FY22) Source: Brown-Forman results release (FY22). NB. FY ends April 30. |

Brown-Forman brands primarily serve the premium+ segment of the market. As of 2020, the company has a 38% value share in premium+ American Whiskey, a 13% in premium+ whiskey, and a 2% share in total distilled spirits.

FY22 Net Sales figures included a 2% contribution from Russia and Ukraine. Brown-Forman suspended operations in Russia in March 2022 following its invasion of Ukraine, and has no plans to return to the country.

Brown-Forman has been active in M&A. The company disposed of its Early Times, Canadian Mist and Collingwood whiskey assets for $177m in August 2020, and agreed to acquire Part Time Rangers (in RTD) for $14m in October 2020. It acquired Gin Mare for $524m in November 2022, and acquired Diplomático Rum for $727m in January 2023.

Brown-Forman continues to be controlled by the founding Brown family, who own a majority in both the Class A voting stock and in the total economic interest. Campbell Brown , a great-great grandson of the founder, is the chairman.

Brown-Forman’s Track Record

Management has a long-term growth algorithm of mid-single-digits sales growth and high-single-digits EBIT growth, as CEO Lawson Whiting reiterated on the Q3 FY23 earnings call :

“We will continue to deliver against our long-term growth algorithm, producing mid-single-digit organic top-line growth and high-single-digit organic operating income growth over the next decade”

At the 2021 investor day, CFO Leanne Cunningham further elaborated that long-term Net Sales growth is likely to consist of growth in the mid-single-digits in the U.S., 1-2 ppts faster than this in Developed International Markets, and “several points higher” in Emerging Markets.

Net Sales growth has been remarkably consistent, with underlying growth (which exclude changes in distributor inventories) at or above 5% almost every year since FY12, except in FY17 and FY20 (impacted by COVID-19):

| Brown-Forman Net Sales Growth (Since FY12) Source: Brown-Forman company filings. NB. FY ends April 30. |

(In FY17, the U.S. only grew 4% and Australia grew only 2%; in FY20, growth was +3% for Q1-3 but -10% in Q4.)

Underlying EBIT growth had historically exceeded sales growth by several points and averaged 9% in FY12-18.

| Brown-Forman Underlying Net Sales & EBIT Growth (FY12-21) Source: Brown-Forman company filings. NB. FY ends April 30. “Underlying” EBIT growth not disclosed from FY22. |

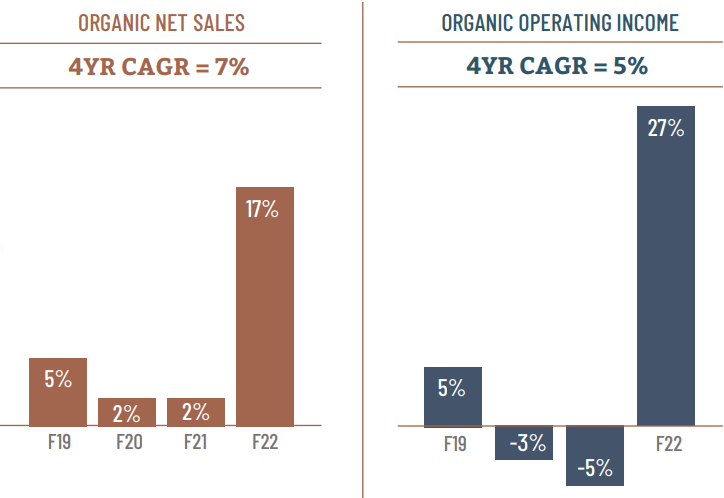

FY19-22 were disrupted by a number of one-off events, including the U.S.-Europe tariff war (which resulted in a 25% European tariff on U.S. Whiskey from June 2018), COVID-19 and then supply chain disruptions. Across FY19-22, organic growth (which included the impact of distributor inventory changes) was 7% in Net Sales and 5% in EBIT.

| Brown-Forman Organic Net Sales & EBIT Growth (FY19-22) NB. FY ends April 30. |

{kind=link}

Brown-Forman was more negatively impacted by the pandemic and the subsequent supply chain disruptions than larger global competitors like Diageo ( DEO ) and Pernod Ricard ( PRNDY ). While the company also benefited from the increase in at-home consumption since COVID-19, it was relatively more exposed to “on premise” consumption that was hit by lockdown restrictions, and it also suffered more from input shortages (particularly in glass).

Brown-Forman’s Shrinking Gross Margin

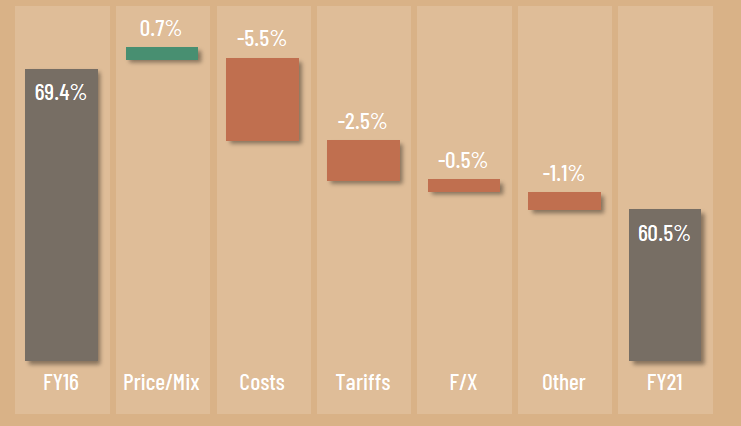

Input shortages contributed to the higher costs that have impacted Gross Margin, which fell 8.9 ppt in FY16-21.

| Brown-Forman Gross Margin Evolution (FY21 vs. FY16) NB. FY ends April 30. |

{kind=link}

Gross Margin recovered 0.3 ppt in FY22 (to 60.8%) but is expected to fall again in FY23 (being guided to be “consistent” with H1 FY23, which had a Gross Margin of 58.8%), despite the suspension of E.U. and U.K. tariffs on American Whiskey during H2 of Brown-Forman’s FY22 (from January and March 2022 respectively).

As shown in the chart above, price/mix has not been large enough to offset the increase in costs. In fact, since FY18, price/mix was less than cost increase every year except in FY22, when the two were roughly equal.

| Brown-Forman Gross Margin Evolution (Since FY18) Source: Brown-Forman company filings. NB. FY ends April 30. |

This may be an intentional result rather than the result of the lack of pricing power. Management’s pricing strategy is to increase prices by low-single-digits consistently each year, even when input cost inflation is higher. Price/mix has averaged 2% since FY12, and was at 4% or less every year except in FY22, when it rebounded from FY21’s -6%.

Brown-Forman’s EBIT Margin vs. Investments

The shrinking Gross Margin means EBIT margin has taken a step down in recent years.

| Brown-Forman Profit & Cost Margins (Since FY18) Source: Brown-Forman company filings. NB. FY ends April 30. FY21-23 adjusted to exclude disposal gains, Finlandia impairments and certain distribution contract termination costs. |

Again this is at least in part intentional. When E.U. and U.K. tariffs on American Whiskey were removed in late FY22, a substantial part of the benefit was reinvested in the P&L (as management has long predicted they would do). Advertising Costs have been kept broadly flat as a percentage of sales. SG&A Costs Margin has only declined slightly as Brown-Forman has embarked on a number of investment programs in recent years, including its Integrated Marketing Communications organisation, an Emerging Brands teams in Europe (replicating the strategy in the U.S.), the build-out of distribution capabilities in key non-U.S. markets such as the U.K., Germany, Australia, Poland, Taiwan, etc.

Brown-Forman’s FY23 Outlook

As of Q3 FY23 results, management’s outlook for the full year is as follows:

- Organic net sales growth to be 8-10%

- Reported Gross Margin to be “consistent” with H1 FY23 (58.8%)

- Organic EBIT growth to be high-single-digits

- Effective tax rate to be 22-23% (FY22: 24.8%)

- CapEx to be $190-$210m (FY22: $138m)

FY23 is benefiting from a rebound from recent headwinds, though supply disruptions in FY22 means growth is expected to be weaker in H2 than in H1. (Organic Net Sales growth was +17% in H1 and +5% in Q3.) Organic Net Sales growth was 12% and Organic EBIT growth was 9% for Q3 FY23 year-to-date.

Possible Upside Over Management Algorithm

Management comments indicate that most of Brown-Forman’s businesses have returned to normal by FY23. By implication, growth from FY24 onwards will likely be closer to the long-term algorithm of mid-single-digits Net Sales growth and high-single-digits EBIT growth (on an organic basis).

We believe it is possible that growth can potentially be much higher than this, as Brown-Forman expands its distribution capabilities in key non-U.S. markets and the new Ready-to-Drink partnership with Coca-Cola develops.

Brown-Forman has historically been a U.S. centric business, but has been making strong investments internationally in recent years, both improving existing direct distribution and moving certain markets from distributor-based to a direct distribution. Such efforts appear to be generating results, with Developed International Markets and Emerging Markets both reporting much larger growth than the U.S. since FY22, more than making up for their lower growth in FY20-21.

| Brown-Forman Sales Growth By Area (Since FY18) Source: Brown-Forman company filings. NB. Company reporting moved from “underlying” to “organic” growth in FY22. |

Brown-Forman also signed a global partnership agreement with Coca Cola in June 2022 on a new “Jack Daniel’s & Coca-Cola RTD” range that will be available around the world. Brown-Forman will be responsible for manufacturing and distribution in the U.S., Germany and Australia, while Coca-Cola will be responsible for the same in all other markets (with Brown-Forman providing the whiskey and collecting a royalty, in an arrangement similar to its partnership with Pabst on Jack Daniel’s Country Cocktails announced in December 2020). The initiative is in its early stages, with the first launch in Cancun, Mexico, in late 2022, but can have huge potential over time.

Brown-Forman Stock Valuation

With Class B shares at $62.43, relative to FY22, Brown-Forman has a 35.9x P/E and a 2.4% Free Cash Flow Yield.

| Brown-Forman Earnings, Cashflows & Valuation (Since FY19) Source: Brown-Forman company filings. |

The dividend is $0.2055 per quarter, or $0.82 annualized, which implies a 1.3% Dividend Yield. Brown-Forman targets an “increasing” dividend and occasionally pays out special dividends (for example $1 in FY22).

Comparison with Global Spirits Peers

Brown-Forman’s valuation multiples appear to be more expensive than those of Diageo (23.1x P/E and 3.3% FCF Yield based on CY22, and a 2.2% Dividend Yield) and Pernod Ricard (21.9x P/E and 2.6% FCF Yield based on CY22, and a 2.0% Dividend Yield), despite all three companies basically targeting a high-single-digit EBIT CAGR.

However, Brown-Forman currently has a more focused portfolio (in American Whiskey and Tequila), and its growth depends less on China and India, while overlapping in the same growth markets in the U.S. and Travel Retail.

Is Brown-Forman Stock A Buy? Conclusion

On balance, we see Brown-Forman stock as still too expensive and wait for a better entry point.

Avoid for now.

For further details see:

Brown-Forman: Near 52-Week Low, But Not Cheap Enough