DEO - Brown-Forman Stock: A Good Buy Now After The Drop?

2023-12-08 09:20:34 ET

Summary

- Brown-Forman Corporation reported disappointing results for the second quarter, which led to a sharp decline in the price of its shares.

- Net sales growth was weak and the company lowered its outlook for fiscal 2024.

- In this update, I share my take on Brown-Forman's latest results, take a look at free cash flow and working capital management, and provide an update on the company's debt.

- Given the current free cash flow vacuum, I assess the dividend safety and put the recently announced share buyback program in perspective.

- Finally, I answer the question whether Brown-Forman stock is a buy now after the drop and considering it is trading close to its 52-week low.

Introduction

Brown-Forman Corporation ( BF.A , BF.B ), the spirits company behind the world-famous Jack Daniel's Tennessee Whiskey, has been on my radar since early 2023, when I first discussed it here on Seeking Alpha in a comparative analysis with U.K. spirits company Diageo plc ( DEO , DGEAF ). At the time, I concluded that Brown-Forman was a fundamentally sound company with reliable earnings, profitability and a solid balance sheet . Nevertheless, I preferred Diageo due to its stronger international exposure and more diversified brand portfolio. Also, Brown-Forman's rather high valuation kept me from taking a position in this family-controlled company (the Brown family owns the majority of Class A voting shares).

Brown-Forman released its results for the second quarter of fiscal 2024 (ended October 31, 2023) on December 6. The report caused the price of both classes of shares to plummet by around 10% to $56 and $54.5, respectively, with BF.A and BF.B shares now trading near their respective 52-week lows and well below long-term resistance and all-time highs in the region of around $75-$80. As a value investor, a selloff like this naturally grabs my attention. So in this update, I will reassess the company's valuation, share my opinion on the Q2 results, and conclude whether I think Brown-Forman stock is a buy now after earnings.

Brown-Forman Q2 Fiscal 2024 Earnings Review

Earnings, Sales, And Inventories

Earnings for the second quarter came in at $0.50, slightly below the consensus estimate of $0.51, which translates to year-over-year growth of 6.4%. Operating income increased 8% on a reported basis and 9% on an organic basis. The company did not adjust earnings for one-offs, which I generally appreciate. There is nothing worse than seemingly one-off expenses such as restructuring charges or stock-based compensation expenses that turn out to be recurring expenses after all (good examples are PayPal Holdings, Inc. (PYPL) or Dell Technologies Inc. , (DELL), which I covered recently).

Net sales for the quarter increased by 1% on a reported basis but decreased organically by 1%. The difference of 2 percentage points is due to a foreign exchange tailwind and a small gain on the sale of certain fixed assets. However, the adjustments also exclude transaction, transition and integration costs related to the acquisitions made in fiscal 2023 (most importantly Diplomático rum brand ). Notable asset disposition-related news include the completion of the sale of the Finlandia vodka brand to Coca-Cola HBC AG ( CCHBF , CCHGY ) for $220 million before adjustments, underlining Brown-Forman management's course of giving the portfolio more of a premium aspect.

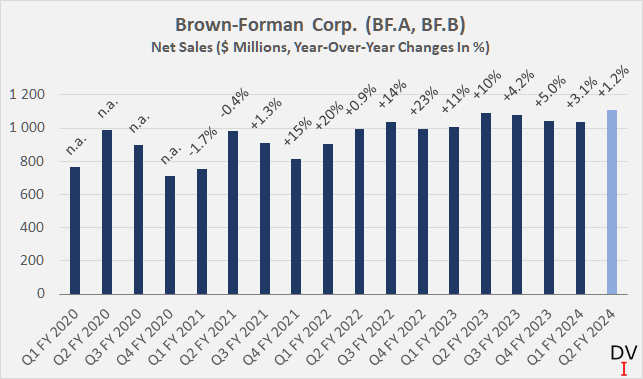

Overall, profit performance was good, but net sales growth continued to disappoint. Following the (expected) recovery from the pandemic low (Q4 fiscal 2020 and Q1 fiscal 2021), Brown-Forman’s top line has been treading water (Figure 1).

Figure 1: Brown-Forman Corp. (BF.A, BF.B): Quarterly net sales (own work, based on company filings)

{kind=link}

In addition, management issued a reduced outlook for fiscal 2024 during the Q2 conference call and now expects organic net sales growth of only 3% to 5%, compared to 5% to 7% previously . Operating profit growth is expected to be slightly higher than sales growth (midpoint of 5.0%, down 1 percentage point vs. the previous guidance). The company is seeing weaker demand for spirits (e.g., -7% and -8% volume decline for whiskey and tequila in the first half of the fiscal year) and continued pressure on input costs. On a positive note, however, supply chain issues are gradually being resolved.

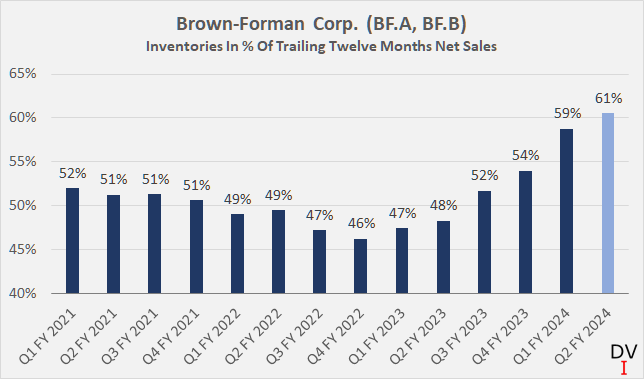

The challenges Brown-Forman is currently facing are also evident when looking at the company's inventories. In my view, inventories as a percentage of trailing twelve months ((TTM)) net sales reflect the situation well (Figure 2). Since the trough at the end of fiscal 2022 ((ended April 30, 2022), relative (and also absolute) inventories have continued to rise as retailers had previously significantly increased their inventories, due in part to counter expected inflationary pressures. The apparent inventory overhang (currently more than 60% of TTM net sales) is likely a key reason for the lowered guidance, along with relatively weak demand. The surplus inventories have to be disposed of, which means that pressure on the gross margin can be expected (increased likelihood of discounts). Although the situation at Diageo is more concentrated on the South American market and more serious, it shows that spirits companies are currently facing broadly similar challenges (see my last update on Diageo ).

Figure 2: Brown-Forman Corp. (BF.A, BF.B): Inventories in percent of trailing twelve months net sales (own work, based on company filings)

{kind=link}

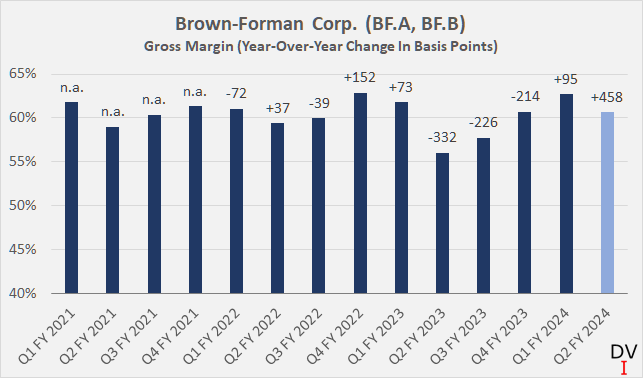

However, I don't think the temporarily expected pressure on gross margin is an issue given how well profitability has recovered from the inflation-driven decline in the second quarter of fiscal 2023 (Figure 3). The generally solid margin structure of spirits businesses, which provides a cushion in tough times, is one reason why I strongly favor this sector over beer-focused companies. However, one notable exception is Constellation Brands, Inc. ( STZ ), which has worked tirelessly over the past few years to improve its gross margin to around 50% (see my article here ).

Figure 3: Brown-Forman Corp. (BF.A, BF.B): Quarterly gross margin (own work, based on company filings)

{kind=link}

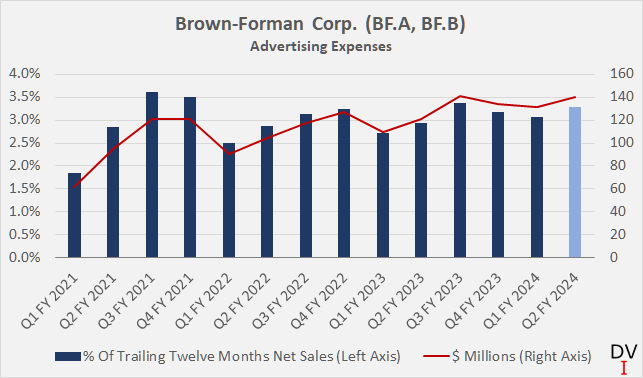

In this context, it should be emphasized that the company is not sacrificing its solid long-term position by trying to compensate for potentially weaker gross margins by spending less on advertising. Management continues to spend a healthy percentage of net sales on advertising (Figure 4). This makes a lot of sense considering the aforementioned acquisition of Diplomático Rum and also that of Gin Mare in fiscal 2023.

Brown-Forman is also investing heavily in brand awareness of its increasingly important ready-to-drink ((RTD)) offerings. RTD is a trend I highlighted in my first article on Diageo in early 2022, and it's good to see Brown-Forman also focusing on this increasingly important convenience segment. Speaking of which, the company reported solid progress in its RTD segment despite weak growth at Jack Daniels & Coca-Cola (+1% organic sales growth), thanks to New Mix (a tequila-based cocktail), which posted a new 41% increase in net sales (22% organic) in the second quarter. The segment was responsible for 12% of consolidated net sales and increased its share by around 80 basis points year-over-year.

Figure 4: Brown-Forman Corp. (BF.A, BF.B): Quarterly advertising expenses (own work, based on company filings)

{kind=link}

Free Cash Flow, Dividend Safety, And An Updated Look At Brown-Forman's Debt

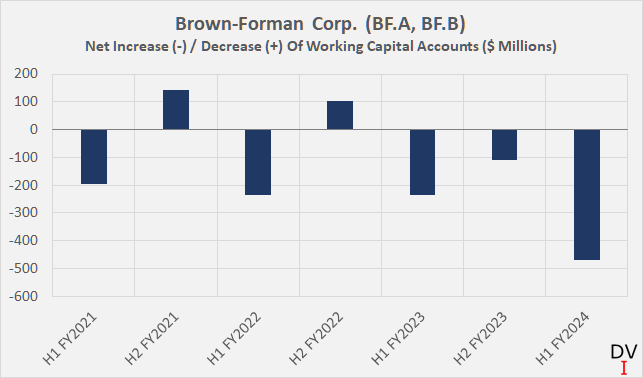

The inventory issues discussed above are also evident from a cash earnings perspective. Brown-Forman continues to struggle to convert its profits into cash flow (Figure 5), largely due to the significant build-up of inventories. However, considering that receivables have also increased year-over-year (+$93 million) while payables have decreased somewhat (-$33 million), it is only reasonable that free cash flow will be (once again) skewed to the second half of the year. The seasonality of free cash flow is probably best illustrated by the net increase/decrease in working capital accounts (Figure 6).

Figure 5: Brown-Forman Corp. (BF.A, BF.B): Free cash flow, adjusted for stock-based compensation (own work, based on company filings) Figure 6: Brown-Forman Corp. (BF.A, BF.B): Net increase or decrease in working capital accounts (own work, based on company filings)

{kind=link}

{kind=link}

Given the cash tied up in working capital and the fact that management has maintained its fiscal 2024 capital expenditure guidance of $250 million to $270 million, it is reasonable to expect Brown-Forman to (temporarily) increase its debt to fund the dividend and the $400 million (ca. 1.5% of market capitalization) buyback program announced in October .

Considering the recently increased dividend (BF is a dividend aristocrat with now 40 consecutive annual dividend increases), the company will distribute about $420 million to its shareholders over the next 12 months. Combined with the buyback program, which is expected to be completed by October 2024, the company is therefore expected to return more than $800 million to its shareholders.

Brown-Forman has not bought back any shares in the last three years and has distributed less to shareholders than it has generated in free cash flow. It is worth noting that the comparatively high three-year average payout ratio of 79% of free cash flow is partly due to the weak cash flow in fiscal 2023 and partly due to the special dividend of $480 million paid in December 2021.

All in all, I would not worry too much about the temporarily underfunded dividend and share buybacks due to the expected rebound in free cash flow. Nevertheless, it is advisable to take a fresh look at the company's debt and credit quality.

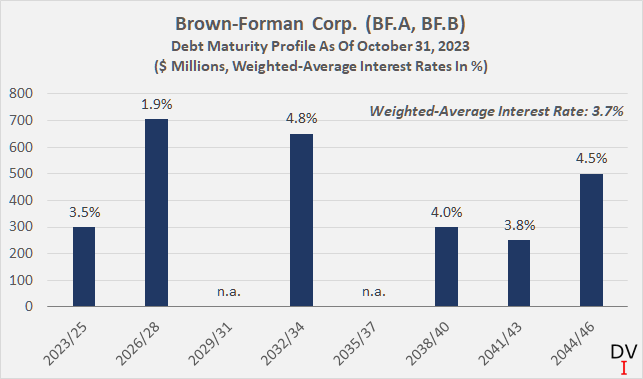

Brown-Forman enjoys a good reputation with the rating agencies. For example, the current long-term rating from Moody's is A1 with stable outlook, which was last affirmed in April 2020. At the end of the second quarter of fiscal 2024, the company had net debt of $2.7 billion, which translates to a leverage ratio of around 4.2 times the average three-year free cash flow ( read here why I prefer this metric to conventional ratios). While this ratio sounds high, it's worth noting Brown-Forman's quite comfortable maturity profile (Figure 7) and weighted-average interest rate of 3.7%. Including interest income estimated at currently $17 million per year (assuming a 3.5% interest rate on cash), this translates into a comfortable interest coverage ratio of almost nine times three-year average free cash flow before interest. All in all, despite the short-term weakness in free cash flow, I see no cause for concern.

Figure 7: Brown-Forman Corp. (BF.A, BF.B): Debt maturity profile as of October 31, 2023 (own work, based on company filings)

{kind=link}

Is Brown-Forman Stock A Good Buy Now After The Drop?

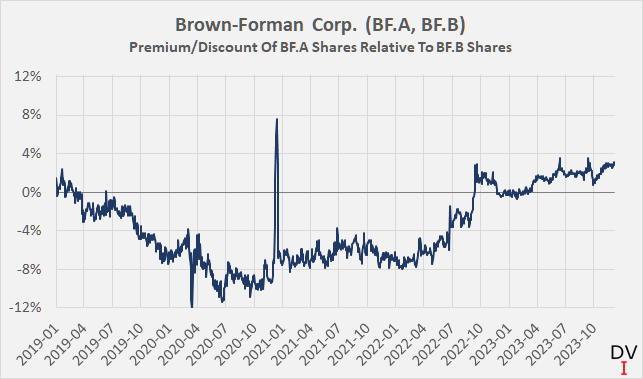

Before valuing Brown-Forman stock, let's consider the trading characteristics of the two classes of stock. In my view, the fact that Class A shares trade at a premium or discount at times can be used to the investor's advantage. Building a position in Class A shares when they are trading at an unwarranted discount (Figure 8) could therefore be used to realize a modest arbitrage profit when the anomaly resolves. I noticed a similar opportunity in German conglomerate Henkel AG & Co. KGaA ( HENKY , HELKF ) in May 2022. The company's preferred shares traded at the same price as the common shares for a short period of time. After a few months, the spread settled back to its long-term average of 10%, allowing holders of the voting shares to realize a quick profit by switching to the preferred shares and back.

In the case of Brown-Forman, as shown in Figure 8, there is currently no profitable trading opportunity, but it is nonetheless worth monitoring the BF.A/BF.B spread. However, in the current environment and considering that the Brown family holds most of the voting rights, I think it only makes sense to buy BF.B shares at the moment. Therefore, my valuation focuses on the category of non-voting shares.

Figure 8: Brown-Forman Corp. (BF.A, BF.B): Premium/discount on BF.A shares versus BF.B shares (own work, based on company filings)

{kind=link}

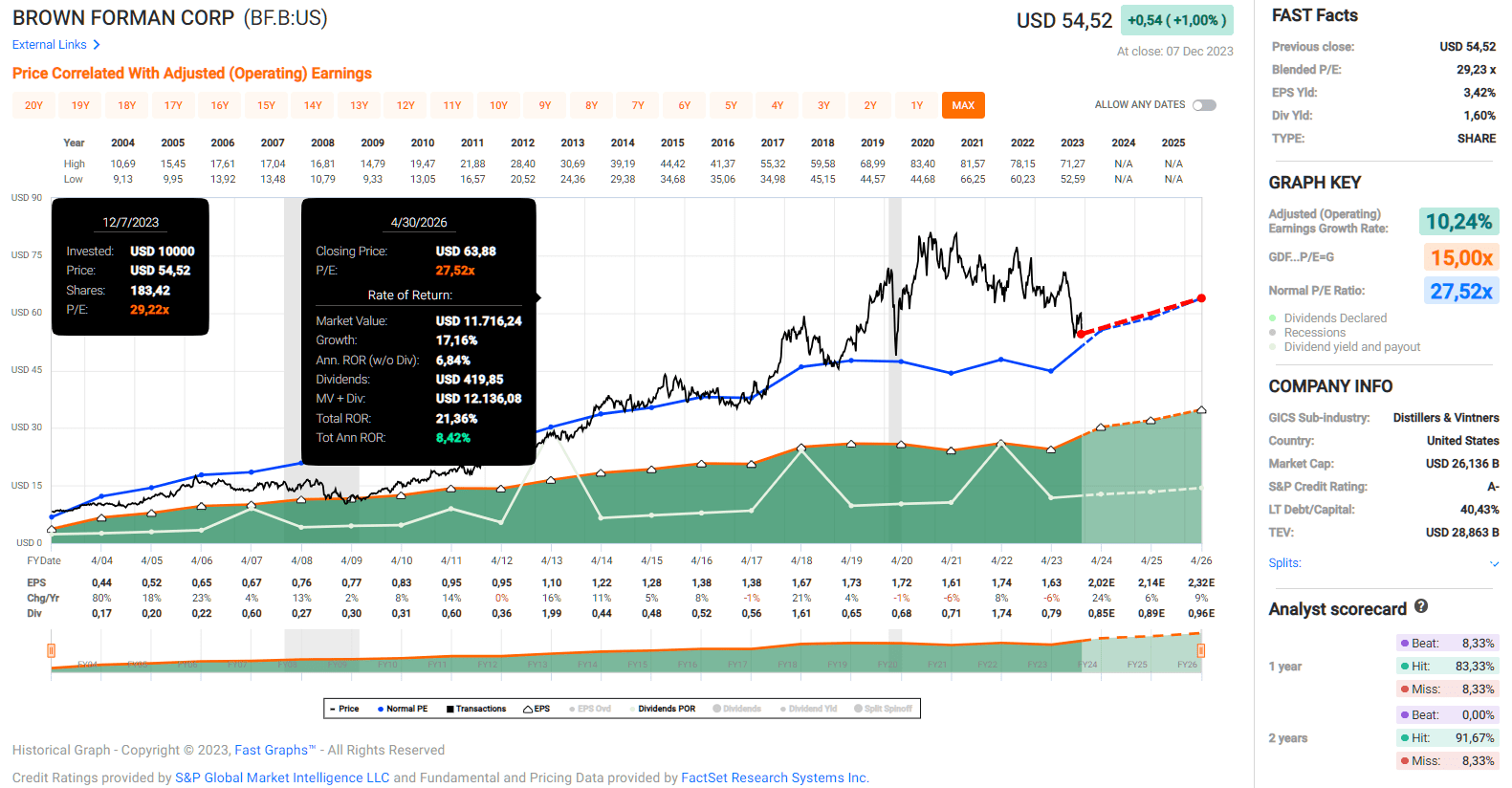

At a blended price-to-earnings ratio of 29 (Figure 9), Brown-Forman stock remains relatively expensive, and I think it's important to consider the significant - and largely unwarranted - multiple expansion since the Great Recession. Of course, a modest premium is warranted given the company's strong track record, solid economic moat (see my last article) and conservative management. However, given the long-term average earnings growth of 10% per year and the significant slowdown in growth in recent years (e.g., 3.0% between fiscal 2015 and fiscal 2023), I do not believe a current multiple of 30 times adjusted earnings is justified.

Figure 9: Brown-Forman Corp. (BF.B): FAST Graphs chart, based on adjusted operating earnings per share (FAST Graphs)

{kind=link}

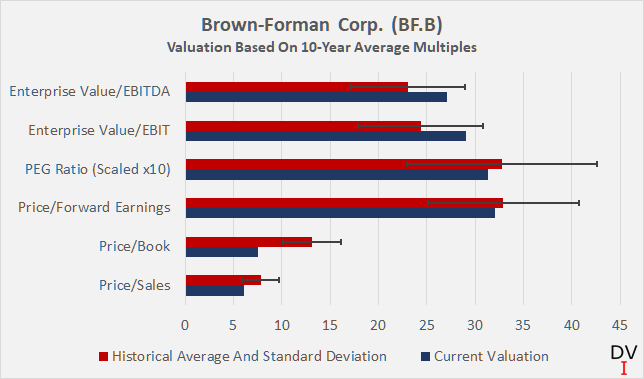

Other valuation multiples such as the price-to-sales ratio, the price-to-book ratio and the price-to-earnings-growth ratio ((PEG)) also suggest that Brown-Forman shares are trading in line with their long-term average valuation, although this does not mean that they represent a compelling value, of course:

Figure 10: Brown-Forman Corp. (BF.B): Valuation based on 10-year average multiples; the PEG ratio is scaled by factor 10 to improve readability (own work, based on data from Morningstar)

{kind=link}

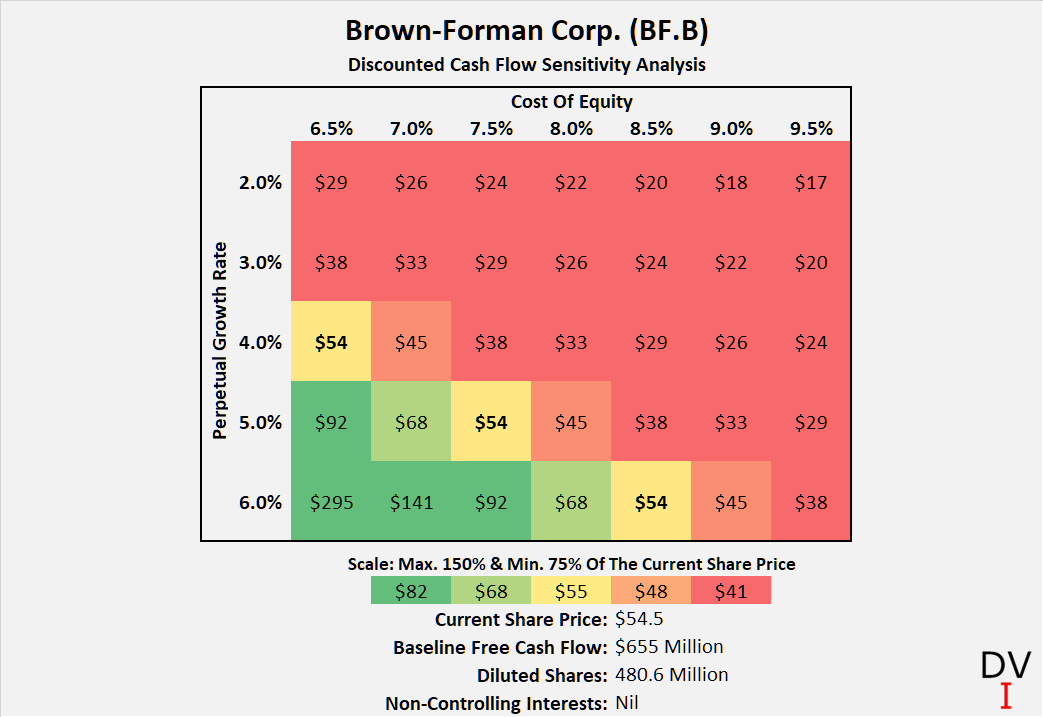

Finally, BF.B stock is not really compelling from a free cash flow perspective either. The discounted cash flow sensitivity analysis in Figure 11 suggests that at the current share price, the company needs to grow its three-year average free cash flow at a perpetual rate of 5%, assuming an investor is content with a cost of equity of 7.5%. It is worth remembering that discounted cash flow, or DCF, calculations are notoriously sensitive to the implied growth rate, and I am always cautious when the model suggests a mid-single digit or higher perpetual growth rate. Looking at the valuation from a different angle, the stock is currently trading at a rather poor free cash flow yield of 2.5%, or a multiple of 40.

Figure 11: Brown-Forman Corp. (BF.B): Discounted cash flow sensitivity analysis (own work, based on company filings and own calculations)

{kind=link}

Conclusion

Brown-Forman Corporation reported rather weak results for the first half of fiscal 2024, but it is worth noting that this is an industry-wide phenomenon rather than a company-specific issue. The demand environment is relatively weak, largely due to high inflation (consumers spending less and trading down), and Brown-Forman, like competitors such as Diageo, is currently suffering from an inventory overhang. The continued strong investment in the ready-to-drink convenience segment is, in my view, the right move. In addition, it's worth highlighting that management is not sacrificing marketing spend to drive short-term profitability and is sticking to its long-term approach, which is certainly in line with the Brown family's objectives.

It will take some time for free cash flow to normalize, but current investors who rely on the dividend income should not worry about the temporarily underfunded dividend. In my view, the fact that management has announced a modest share buyback program is a sign that it expects free cash flow to improve for the remainder of fiscal 2024 and into fiscal 2025. The balance sheet is in good shape and there is no material risk to the company's generally solid debt servicing ability due to a comfortable maturity profile.

In my view, the market is finally starting to catch up with reality, which is that Brown-Forman is a relatively slow-growth company. Frankly, I have never understood why investors were willing to pay such a high earnings multiple for a company whose growth has slowed considerably over the years. With a current earnings multiple of 30 and a free cash flow yield of 2.5%, the stock is still expensive, but the recent 10% drop was definitely a step in the right direction.

As a conservative and long-term oriented investor, I like Brown-Forman's fundamentals: a solid brand portfolio, shareholder-friendly management and largely untapped growth opportunities in emerging markets. As such, I'm keeping the stock on my watch list and can see myself starting a position in the low $40s, which equates to a free cash flow yield of over 3% and an earnings multiple in the low 20s. Given the recent sharp decline, the stock could rebound on the back of a benign market environment and potential positive macroeconomic news, so traders may view the current share price as a compelling opportunity. However, as a long-term investor, I simply see no reason to run out and buy Brown-Forman stock in haste.

Thank you for taking the time to read my latest article. Whether you agree or disagree with my conclusions, I always welcome your opinion and feedback in the comments below. And if there's anything I should improve or expand on in future articles, drop me a line as well. As always, please consider this article only as a first step in your own due diligence.

For further details see:

Brown-Forman Stock: A Good Buy Now After The Drop?