BC - Brunswick Corporation Q3: Showing Resilience Amidst Macroeconomic Challenges

2023-11-09 10:35:35 ET

Summary

- I believe BC can achieve its targets due to its product leadership, inventory normalization, and growth in electrification.

- Despite a decline in revenue and earnings, BC's segment level reported healthy numbers and is performing well.

- The Freedom Boat Club should see strong growth and expansion, which I expect to drive future revenue growth.

Overview

Note that I previously gave a buy rating for Brunswick Corporation ( BC ) back in 25 Sep 2023, as I expect them to achieve their targets given their product leadership in the propulsion segment. During the third quarter of 2023, BC’s propulsion business saw an increase in its top line compared to a record third quarter of 2022. This is especially impressive as it is still able to grow even when compared with a tough period. The reason for this was the rise in outboard engine sales, offset by comparatively lower sales of sterndrives, especially in high-horsepower categories, controls, and rigging.

In this post, I am reiterating my buy rating as I believe that the stock has been heavily sold given the negative numbers reported in the third quarter of 2023. However, after deeper analysis, I believe these numbers showed strength rather than weakness, as they are operating in a challenging environment. In addition, BC’s segment level reported healthy numbers and is performing well. Although revenue decline year-over-year by 6.2% and EPS by 9%, it was mainly driven by the persistent inflationary environment which hampered general economic growth. Since the start of 2023, inflation has been easing and I believe this positive recovery will aid in BC growth outlook.

Recent results & updates

In my opinion, I believe BC reported resilient third quarter 2023 results. Although BC operated in challenging market conditions due to persistent inflation and a high interest rate that dampened consumer spending, its revenue only decreased by 6.2% from the all-time high of the previous year. The all-time high revenue also created a tough comparison period, which makes reporting strong numbers even tougher. Reduced wholesale orders as a result of field inventory returning to normal levels and weaker retail market conditions were offset by net sales gains in each segment from annualized price increases, gains in market share, and well-received new products. The benefits of aggressive cost control measures across the entire organization were more than offset by lower sales, slightly higher input costs, higher absorption, and the unfavorable impact of foreign currency exchange rates, resulting in lower operating earnings, which fell by 17.5%, and margins, which fell by 2% compared to the previous year.

The third quarter performance of Navico Group improved, as expected. Softness among OEM customers for marine and RVs was somewhat offset by stability in the aftermarket channel. These sales dynamics caused segment sales to decline by 9%; however, benefits from accelerated cost reduction actions and reorganization efforts, along with strong performance from new products, more than offset the impact of lower sales. As a result, adjusted operating margins increased by 1.1% and adjusted operating earnings increased by 3%. The fourth quarter is crucial for the business as holiday season drives aftermarket retail sales. Therefore, I'll be keeping an eye on consumer health and holiday spending intentions, as well as retailers' wholesale reordering patterns during a period when inventory levels are normalizing.

The Freedom Boat Club has reported strong numbers. With 400 locations and nearly 60,000 membership agreements covering over 91,000 members nationwide, Freedom Boat Club is still actively expanding its membership base and not showing signs of deceleration. With the recent announcement of its seventh location, Freedom Boat Club is continuing to grow quickly in the Australian market. Management stated that they consider the ANZZP region to be a significant new growth opportunity for Freedom. Therefore, I expect this move to be one of the catalysts for future revenue growth.

Moving into FY23 and FY24, I do expect that the current challenging economic conditions will continue creating headwinds for BC. Ever since the start of COVID in 2020, inflation has been on a steady rise from near 0% to a peak of 9% in mid-2022. Since the peak, inflation has been cooling off and has settled at ~4%. Although it has come down, it is still double the federal reserve’s target rate of 2%. As a result of it, central banks all around the world are hiking interest rates in a bid to get inflation under control. BC operates in the boat manufacturing segment, and boats are considered recreational products, which are highly elastic. As inflation and interest rates rise, disposal income decreases. In addition, it also makes the financing of boats more expensive. As long as inflation and interest stay elevated, they are going to exert downward pressure on BC’s future growth. This is evident in the market consensus revenue forecast of mid-single digits for the next 2 years vs. 2022’s 16%. To further prove this point that these challenging economic conditions are putting pressure on BC, management during the earnings call highlighted that higher costs, higher interest rates, and credit availability continue to be major obstacles for customers, even in spite of the favorable promotional environment and stable boat purchase considerations. Not just on end consumers, mid-stream clients such as dealers are also wary of storing too much inventory in anticipation of an unpredictable 2024.

{kind=link}

Valuation and risk

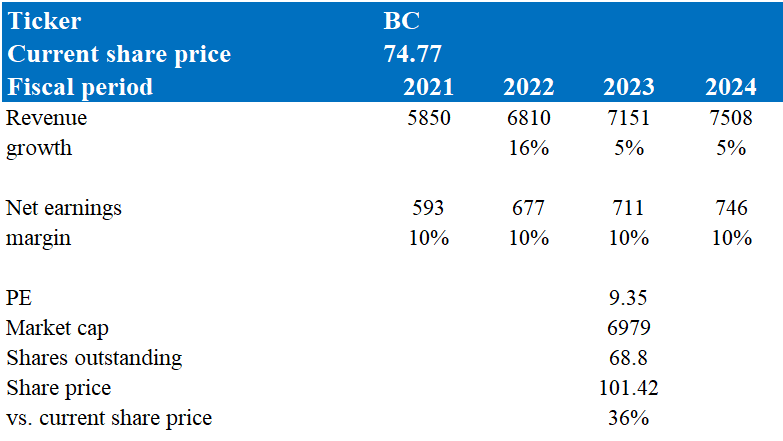

According to my model, BC is valued at $101.42 in FY24, representing a 36% increase. This target price is based on my growth forecast of the mid-single digits of 5% over the next two years. The rationale for my assumption is based on its impressive third-quarter result. Although sales declined 6.2%, it was compared with a tough year, as 2022 second quarter sales were at record levels. In addition, it is operating in a challenging market due to macroeconomic uncertainty caused by high inflation and interest rates. Despite all these, sales only fell by single digits. Additionally, each segment's net sales all increased due to better pricing, which indicates BC’s pricing power and its ability to pass costs down to clients without much consequence. Moving ahead into 2023 and 2024, I do not foresee sales to be near the levels seen in 2022 due to macroeconomic challenges such as high inflation and interest. I expect these challenges to exert pressure on BC’s top-line revenue, which will result in mid-single-digit growth. However, I do note that these factors are subsiding and stabilizing. If these challenges dim, I expect BC to grow strongly, but when this will happen is anyone’s guess. But based on my current view, I see BC standing strong against these challenges and making tremendous efforts to minimize their impact.

{kind=link}

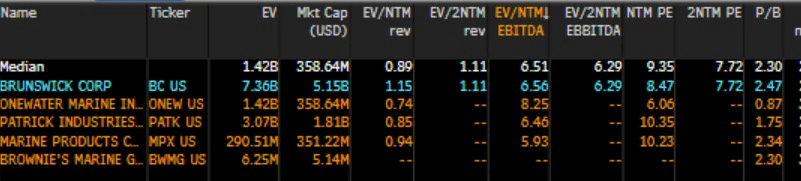

In this post, I employed the P/E ratio in my model because I believe it is a good fit for BC. In my opinion, P/E is a reflection of the market's sentiment for a stock’s earnings potential. A lower P/E might suggest that the company might be oversold due to a myriad of reasons, such as a poor growth outlook or poorer profitability, and vice versa. For Brunswick, which manufactures recreational products and is not a high-growth company, the P/E ratio is a good indication as it shows how efficiently BC is translating its revenue into profits.

As of now, BC's P/E stands at 8.47x, below its peers’ median P/E of 9.35x. In my analysis of its comparables, this lower multiple of 8.47x is unjustified. BC has a higher net margin of approximately 11% (adjusted earnings based on Bloomberg) compared to its peers' 8.34%. In addition, its EBITDA margin of 18% is also better than its peer’s 14%. Lastly, BC has a brighter growth outlook of 5% in 2023 vs. its peers' flat 0% growth outlook. With a 36% price difference, I maintain my buy rating for BC.

{kind=link}

One downside risk is BC’s high leverage ratio of ~42% and debt/equity ratio of ~1.22. In the current high interest rate environment driven by high inflation, high debt on balance sheet creates a vulnerable position for the company as they are more susceptible to liquidity issues such as principle and interest payments. If the interest rate were to rise, it would create significant interest rate risk for them. On top of these, as BC operates in the boat segment, which is considered a recreational item, higher interest rate and inflation will dampen retail spending due to the high cost of purchasing and financing a boat. This will create pressure on the BC top line as well as the growth outlook.

Summary

In summary, BC showed robustness and resilience in the third quarter of 2023. With the stock price having been heavily sold in light of the negative numbers reported for the third quarter of 2023, I am restating my buy rating here. A challenging comparison period in the second quarter of 2022, as well as ongoing inflation and high interest rates, were the main contributors to the decline in sales and earnings per share. Although these are creating headwinds for BC, take note that it has been on a recovery path and has stabilized. When considering the difficult operating environment, they face, I see these results as indicative of strength rather than weakness. As BC is the current market leader in the propulsion market, its market dominance has continued to benefit BC in the third quarter by growing its propulsion business, even though it is operating in a challenging economic environment. Hence, moving forward, I expect these traits to continue generating tailwinds for BC and push its growth in the future.

For further details see:

Brunswick Corporation Q3: Showing Resilience Amidst Macroeconomic Challenges