CL - Brush Up With Colgate-Palmolive Stock As Earnings Growth Drips On

2023-11-14 01:10:25 ET

Summary

- Colgate-Palmolive stock gets buy rating today, agreeing with consensus from SA analysts and Wall Street.

- Pumping up this rating is healthy revenue and earnings growth along with dividend growth / stability.

- Squeezing the situation are items like underperformance vs the S&P 500 index, and below average dividend yield.

- Elevated debt loads are offset by strong operating cashflow performance.

Research Note Summary

I can almost hear the water faucet dripping with both revenue and earnings growth at Colgate-Palmolive ( CL ), who I am covering today as part of my article series this fall on household and consumer products, and who just had its most recent quarterly earnings call a few weeks ago.

In today's research note, this stock got a buy rating.

Turning on my bullish sentiment was its healthy YoY revenue growth among peers, YoY profitability growth, cashflow improvements and 3 year dividend growth.

At the same time, the waters are clouded by falling equity, overvaluation, below average dividend yield, and underperformance vs the S&P500.

The risk of rising debt and interest expense has been addressed too.

Methodology Used

My WholeScore Rating methodology looks at this stock holistically across multiple categories including key risks, and assigns a rating score. I exclusively cover stocks and foreign ADRs that are dividend-paying and trade on major US exchanges only (NYSE, Nasdaq).

Some of the data comes from the most recent FY23 Q3 results from October 27th, while the forward-looking sentiment relates to the upcoming FY23 Q4 earnings results not expected for a new months, on January 26th.

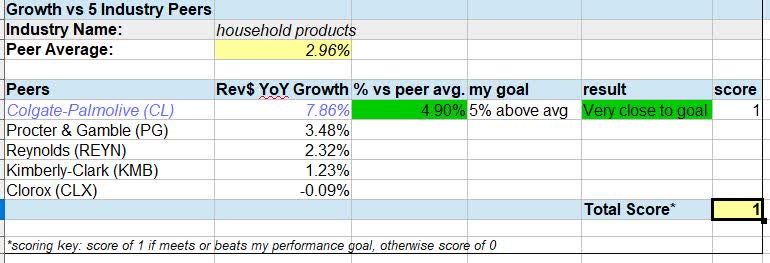

Growth vs Industry Peers

Here, I will compare a peer group of 5 stocks in the household products sector, and their YoY revenue growth. In this peer group, I selected 5 stocks of companies that are comparable due to their market presence and brand penetration.

This particular group had an average YoY revenue growth of 2.96%, whereas Colgate's was 7.86%, nearly 5% higher than the peer average and very nearly making my 5% target so I gave it a point there.

{kind=link}

A fun fact about the Colgate brand.. long before I was a contributing analyst for Seeking Alpha, I walked by a stretch of waterfront along the Hudson River across from Manhattan, an area where I grew up, and there happens to be an old Colgate sign there looking out towards NYC harbor.

This is a remnant of the industrial age, when Colgate had a plant in that area, along with many other companies like Maxwell House coffee. Fast forward over the last several decades and even though the industrial era has morphed into the digital age, Colgate as a brand has stood the test of time, the 2008 financial meltdown, the 2020 pandemic, and shifting technology trends, yet still is alive and well as it continues to grace the supermarket shelves with its products.

The nature of this sector, household products , is that they sell "consumables" which have to be replenished often. Things like toothpaste, soap, and so on. I like to say that customers don't buy a product they buy the brand, so Colgate can rely on brand loyalty, in my opinion, but also relying on consumers considering their products a household "necessity".

With that said, it relies on products selling and moving off the shelf so that new product can be replenished. Any of my readers that have ever worked seasonally in a supermarket or major pharmacy chain knows that the new batch of inventory comes with this week's truck shipment, and has to be unloaded and stocked.

So, this points to the question: What helped drive revenue growth for Colgate in Q3?

One word: volume!

According to the company's Q3 comments ,

Net sales increased 10.5% and organic sales grew 9.0% with volume improving sequentially versus second quarter 2023.

With that said, I forecast that this company will continue to show positive top-line results going into the end of the year.

Financial Statements

Now that we said a few words about the company and industry, lets dive into some financial waters right now because after all we are investors and analysts, not simply consumers, and so we should care about these metrics below.

The income statement tells a great story, that this company has achieved a nice YoY revenue growth of 10.3% along with 14.6% YoY earnings growth , both of which beat my target goal and earned a rating point each.

{kind=link}

The cashflow statement also showed YoY improvement with free cashflow per share increasing 26.3% on a YoY basis, while the balance sheet showed a 61% decline in equity in that same period.

Many readers may be interested, however, in how the company is expected to do in the near future. I think it will continue to outperform on earnings and revenue, as their own forecasts appear to be positive:

The Company now expects net sales growth to be 6% to 8% (versus 5% to 8% previously), including the benefit from our acquisitions of pet food businesses.

Company still expects gross profit margin expansion and increased advertising investment and increased its earnings-per-share growth guidance to high-single digits.

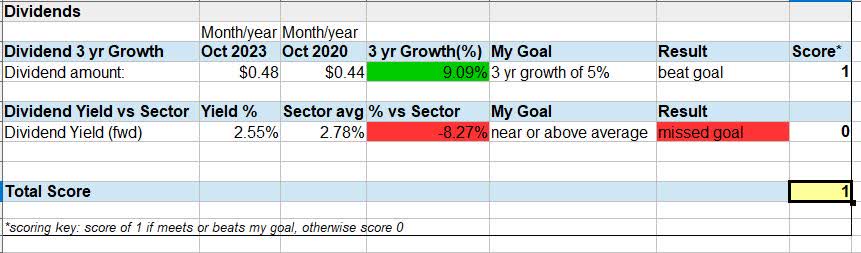

Dividends

When it comes to dividends , I would love to have added this one to my dividend quick picks of the week but it is just not quite there yet.

For instance, it did achieve a 9% growth in dividends over 3 years, when comparing the dividend from Oct 2023 with that of Oct 2020. However, its dividend yield is somewhat below the sector average of 2.8%. Not terrible and not great either.

{kind=link}

When comparing its yield with some of its peers, for example, you can get a better yield at Reynolds ( REYN ) at 3.39%, and 3.91% at peer Kimberly-Clark ( KMB ), who incidentally also has a much higher quarterly dividend amount now at $1.18.

Just some thoughts for dividend-income investors.

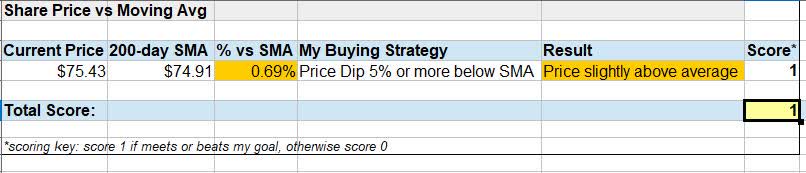

Share Price vs Moving Average

At first glance of this chart below, if looking for dip-buying value opportunities and crossovers below the 200-day average, it may appear that opportunity was missed back during the October dip.

However, as of the writing of this article the share price of $75.43 is just slightly above the moving average of $74.91, so although it is not the price dip I would like right now I think I would give it a chance as it is practically hovering around the average and not much higher, so I am giving it another rating point here.

{kind=link}

In particular, I am expecting it to steadily climb further up due to positive Q3 results, and if it can beat Q4 estimates then we can see another little price spike perhaps.

Consider that it has already beat 3 of the last 4 earnings estimates , and came in line with 1 of them.

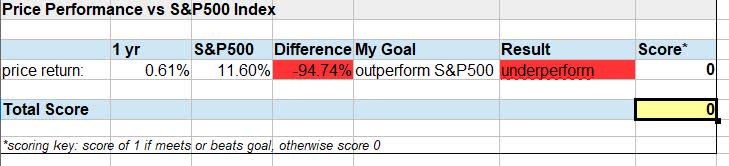

Performance vs S&P500 Index

Although this stock's momentum shows that its 1 year price return was a positive 0.61%, this is nearly 95% below the S&P500 index performance for that same period, so a major disappointment and a lost rating point.

{kind=link}

Its peer Kimberly-Clark fared even worse in this metric with a 1 year price return of -5.43%, while peer Clorox ( CLX ) saw a negative -7.31% return in that same period.

When correlating the above data with that of the price chart for Colgate, we see that the market has been highly bearish on this stock for most of the summer and fall, and in my opinion it is not due to poor revenue or earnings but due to concerns over consumer product companies and impacts from inflation and a potential recession affecting spending.

The good news on that front is that the latest projections do not call for a certain recession, but rather a sentiment of "uncertainty".

A recent study by global consultancy Bain & Company on Oct 31st highlighted the current environment well:

The question of whether the US will fall into a recession remains open, as the tension between growth and inflation continues to challenge the Federal Reserve.

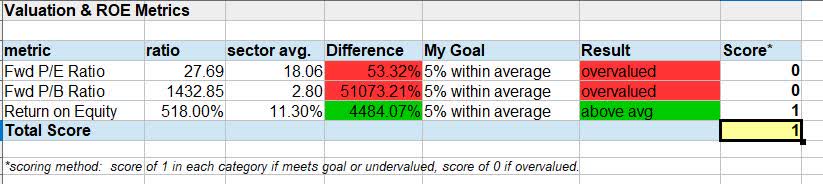

Valuation and ROE

The valuation levels of this company almost look like I left the faucet running too long and the bathroom got flooded with suds!

For example, the forward P/E ratio is 53% above the sector average, hovering at nearly 28x earnings, while the forward P/B ratio is an unimaginable 51,000% above the sector average at 1,433x book value!

This is according to Seeking Alpha's latest data .

{kind=link}

When it comes to return on equity, the company has beat the sector however it appears to be extreme at 518% ROE.

What I think the drivers of this are primarily the huge drop in positive equity I mentioned earlier, down to just over $400MM in equity, not much of a number for a company this size. Although earnings have grown, the recent price spike above the moving average may be the cause of the elevated P/E ratio as well.

Hence, it is losing 2 potential rating points due to overvaluation .

Key Risks

The risk I see for a company like this is a rising debt load when comparing Sep 2023 with that of Jun 2022, which is a 9% rise. In times of cheap credit, this would be less of a concern, however current interest rates make financing more costly for a business.

{kind=link}

For instance, if you correlate rising debt with interest in that same period, you see an 87% rise in interest costs, to $58MM in quarterly net interest expense.

{kind=link}

However, what I think is an offsetting factor and a positive mention is the cash flow strength of this company. If you look at their own data in the table below comparing 2023 with 2022, they saw a 38% spike in net cash from operations , as well as a 49% rise in free cash flow before dividends are paid.

{kind=link}

So, I expect this company will continue to be able to fund its debt obligations in a manageable way, and I gave it a moderate risk score because of this it is not losing a rating point here:

{kind=link}

WholeScore Rating

In today's note I gave this stock a WholeScore of 7, which earned it a buy rating from me.

Colgate - WholeScore (author report)

In comparing my rating to that of the consensus, my rating agrees with the sentiment from both Wall Street and SA analysts. I think the quant system is being a bit cautious on this stock, which is understandable as well.

Colgate - rating consensus (Seeking Alpha)

My Forward-Looking Sentiment

I expect this legacy company that has been such a major part of both American and international households for decades, to continue its success in selling products people consume and replenish regularly, so the continued demand is always there despite competition on the supermarket shelf it continues to be a "sticky" brand.

I would add at least a bit of this stock to my existing portfolio to "brush it up" so to speak and gain exposure to the household products segment, particularly at current share prices for this stock.

For further details see:

Brush Up With Colgate-Palmolive Stock As Earnings Growth Drips On