BSJO - BSJO: Decreasing Risk Increasing Rewards As Time Passes

2023-09-19 10:47:18 ET

Summary

- The Invesco BulletShares 2024 High Yield Corporate Bond ETF is a fixed-income ETF with a termination date of December 15, 2024.

- The majority of the fund's portfolio is maturity matched, reducing market risk and potential losses for investors.

- The fund's duration and credit spread sensitivity will decrease over time, resulting in lower volatility and shallower drawdowns compared to other high-yield funds.

Thesis

The Invesco BulletShares 2024 High Yield Corporate Bond ETF ( BSJO ) is a fixed-income exchange traded fund. The vehicle has a fixed termination date, scheduled for December 15, 2024. More importantly, the vast majority of the fund's portfolio is maturity matched. That translates into the underlying bonds having a maturity date before December 2024 (with a few exceptions).

Maturity matched funds are the ideal structuring choice when building such a vehicle because they eliminate market risk. Market risk references the probability that, due to risk-off conditions, the underlying collateral trades below the purchase price on the fund's maturity date. Such a construction can thus result in losses for fund investors. Not for maturity matched funds.

Furthermore, another added benefit for matched maturity funds is the reduction in risk factors as time passes due to the approaching maturity dates for the underlying bonds. Duration compresses here, as well as sensitivity to credit spreads. Let us just go through an intuitive example: let us assume an investor is contemplating two different bonds. One with a 10-year maturity and 5% coupon, and one with a 1-year maturity and 5% coupon. Without knowing anything about finance, which one do you think is less risky? The shorter the maturity, the shorter the duration (i.e., price sensitivity to interest rate changes) and the lower the CS01 profile of said fund (the CS01s are an analytical model output that captures the change in present value for a one basis point parallel upward shift in the underlying credit spread curve).

We can already observe these analytics for BSJO during the 2022 market sell-off:

While the overall junk market as measured by the SPDR Bloomberg High Yield Bond ETF ( JNK ) had a -16% drawdown, BSJO only experienced a -9% one. Furthermore, as time passes, the depth of a new drawdown is going to get increasingly shallow due to the 'pull to par' effect. As bonds approach their maturity dates, their prices are going to go to 100% (or par). Unless a bond actually defaults, we are going to see this effect across the entire portfolio.

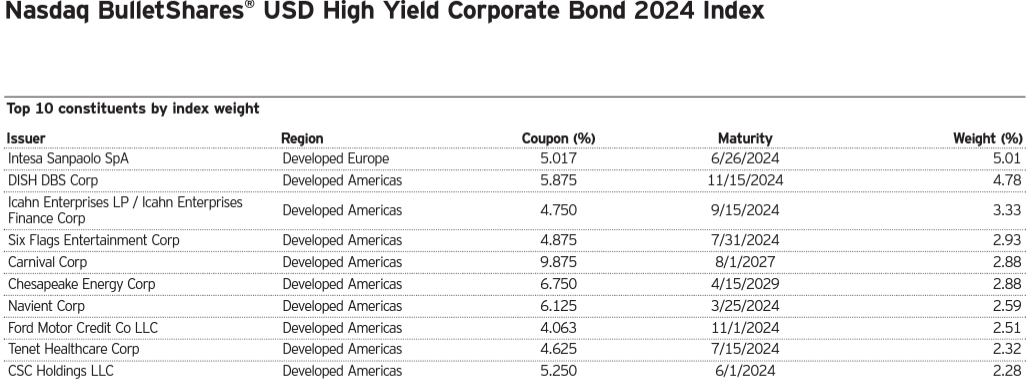

Nasdaq Bullet-Shares USD High Yield Corporate Bond 2024 Index

To note, the ETF is based on the Nasdaq Bullet-shares High Yield Corporate Bond 2024 Index , and it will invest at least 80% of its portfolio in corporate bonds which are comprised in the respective index.

It is interesting to note that indeed the fund's top holdings are not exactly as the ones present in the index:

{kind=link}

As measured by weight, the top holdings in the Index are Intesa, DISH, and Icahn Enterprises. The ETF contains DISH, Wesco, and Intesa as its top 3 for example. Furthermore, one aspect amply discussed in the article, and one of the main risk factors is constituted by the lack of a 100% maturity matching for the collateral and fund maturity date. This is due to the index construction, which itself has this issue:

Index Maturity Breakdown (Index Fact Sheet)

Analytics

- AUM: $0.65 billion

- Sharpe Ratio: 0.09 (3Y)

- Std. Deviation: 5.9 (3Y)

- Yield: 7.26% (30-day SEC yield)

- Portfolio Yield: 7.66%

- Z-Stat: N/A

- Leverage Ratio: 0%

- Composition: Fixed Income - High Yield Bonds

- Duration: 1.23 yrs (modified duration)

- Expense Ratio: 0.42%

Holdings

The fund holds a portfolio of high yield bonds:

Ratings (Fund Fact Sheet)

We can see from the ratings paring that the vehicle is not overly aggressive, being overweight BB names and having a very low CCC bucket. That bodes well for the probability of default associated with the names in the portfolio.

The fund is fairly well diversified from a sectoral standpoint, with no significant concentration outliers:

Sectors (Fund Website)

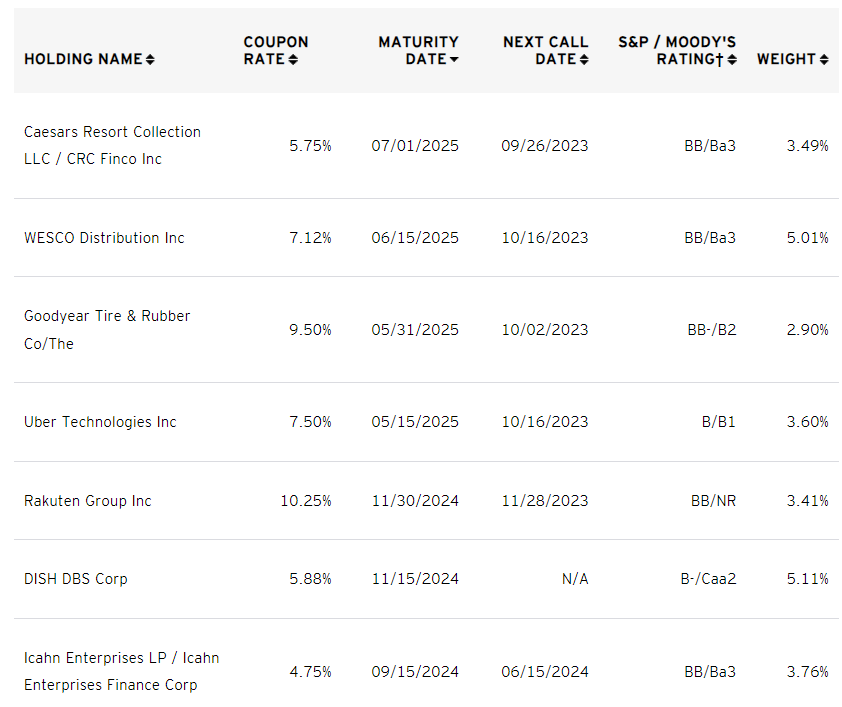

The granularity and tenor matching of the collateral are the most important factors here:

{kind=link}

From the manager's website, we are able to arrange the fund holdings per their maturity date. By utilizing that filter, we can see how a couple of names have maturity dates which exceed the fund's termination date. Specifically, we see the following names:

- Caesars Resorts, 3.49% of fund, 7/1/2025 maturity date

- WESCO Distribution, 5.01% of fund, 6/15/2025 maturity date

- Goodyear Tire, 2.9% of fund, 5/31/2025 maturity date

- Uber, 3.6% of fund, 5/15/2025

Firstly, while these names have maturity dates exceeding the fund's termination date, they are all very closely aligned - all the maturity dates above are 6 to 7 months out from the fund's termination date, thus the duration mismatch is minimal.

Secondly, all names are also very large well-known issuers, thus there is no question regarding liquidity or ability to sell names in the market.

The only concerning part here is regarding the total weighting of these names in the overall vehicle. That number comes to almost 15%, which is slightly concerning. We would have liked to see that figure under 5%.

Risk Factors to Consider - Granularity is the Biggest One

On the duration front, we do not have any concerns. The fund has a 1.23-year duration, which is decreasing as we speak. Its sensitivity to interest rates will continue to diminish as time passes.

Default probability and Granularity - this is a high-yield fund, and it does contain some CCC names. Bankruptcies are indeed increasing, and we might be entering a recession. Furthermore, there are some chunky positions held by this fund. We like to define funds as 'granular' when all individual issuers represent 1.5% of the collateral or less. Not here. We have in fact a significant number of names with exposures above 1.5%. The mitigating factor for the fund is going to be the investment manager, namely Invesco. Invesco is a behemoth in the fixed income management arena, and its credit research platform is industry-leading. We are of the opinion that fund managers are able to leverage that platform and analytical tool-set to pick credits which either have very large recovery factors, or will continue to perform through the business cycle.

Credit Spread sensitivity - just as the duration risk factor, the fund's sensitivity to credit spreads is going to decrease as time passes. The closer a bond gets to its stated maturity date, the lower the fluctuation in price, unless it is actually distressed/defaulting. In reality, companies are not going to wait until the actual maturity date for the bonds but will try to re-finance a couple of months ahead of time.

Conclusion

BSJO is a fixed income exchange traded fund. The vehicle holds high-yield corporate bonds and has a termination date of December 15, 2024. The vehicle does not maturity match the entire collateral pool, with roughly 15% of the collateral having a maturity date that is 6 to 7 months after the fund's termination date. This structuring aspect introduces a slight market risk in the fund, a risk that will keep diminishing as we approach the fund's maturity date.

We like this name because its duration and credit spread sensitivity will keep decreasing as time passes by. As the underlying bonds approach maturity, they will 'pull to par'. As compared to regular unconstrained high-yield funds such as JNK, BSJO will have less volatility and much shallower drawdowns going forward. The closer the maturity date, the lower the vol and drawdown.

The main risk factor here is lack of very significant granularity and probability of default. We like names where no single issuer is above 1.5% of the collateral pool. That is not the case here. If we do get a significant recession the probability of default will become important, even if the fund is fairly conservative being overweight BB names. The mitigating factor for this risk is Invesco as the asset manager. Invesco is a premier fixed income manager with an unparalleled research and analytics platform, and we feel the credits chosen represent robust names in the HY space.

If we experience a soft landing, an investor is looking at an annualized yield of 7.66% (the portfolio yield) with a very low volatility and drawdown profile when compared to JNK. If we have a full-blown recession, but the fund does not experience any actual defaults in 2024 then again BSJO is net superior to JNK given its lack of volatility and 'pull to par' aspect.

At this juncture in the economic cycle, it is hard to predict a soft landing versus an outright recession , but in either scenario we feel BSJO represents a good risk/reward as time passes, helped by the significant fixed income research capabilities coming from Invesco. We are a Buy for the name here, preferring this fund over an unconstrained HY one like JNK.

For further details see:

BSJO: Decreasing Risk, Increasing Rewards As Time Passes