MAA - BSR REIT: When It Gets This Cheap You Need To Buy

2023-11-29 12:00:57 ET

Summary

- BSR Real Estate Investment Trust is a Canadian entity that owns and manages multi-family residential rental properties in the sunbelt region of the United States.

- Sunbelt state REITs have been under some scrutiny, thanks to an avalanche of supply.

- We examine the long case for BSRT and tell you why we are taking a position on this falling knife.

We have previously covered Mid-America Apartment Communities, Inc. (NYSE: MAA ) on this platform. This REIT owns multi-family apartment communities in United States, some of which are in the sunbelt region. While we felt it was close to a buy point when we covered it back in July , we were not there yet. Our rating on it was neutral and the call to stay out was not wrong.

Seeking Alpha

REITs have collectively been pummeled in the last few months, so MAA is not alone in this pain. Nonetheless, it has broken well below our buy under price from that piece and we consider it a good value buy today. We will however, not be delving into our reasons in this piece as they were laid out in our earlier coverage. Instead, we will check out another multi-family REIT. One that has all its energies focused on the sunbelt and who performance is not dissimilar to that of MAA during this time.

The REIT

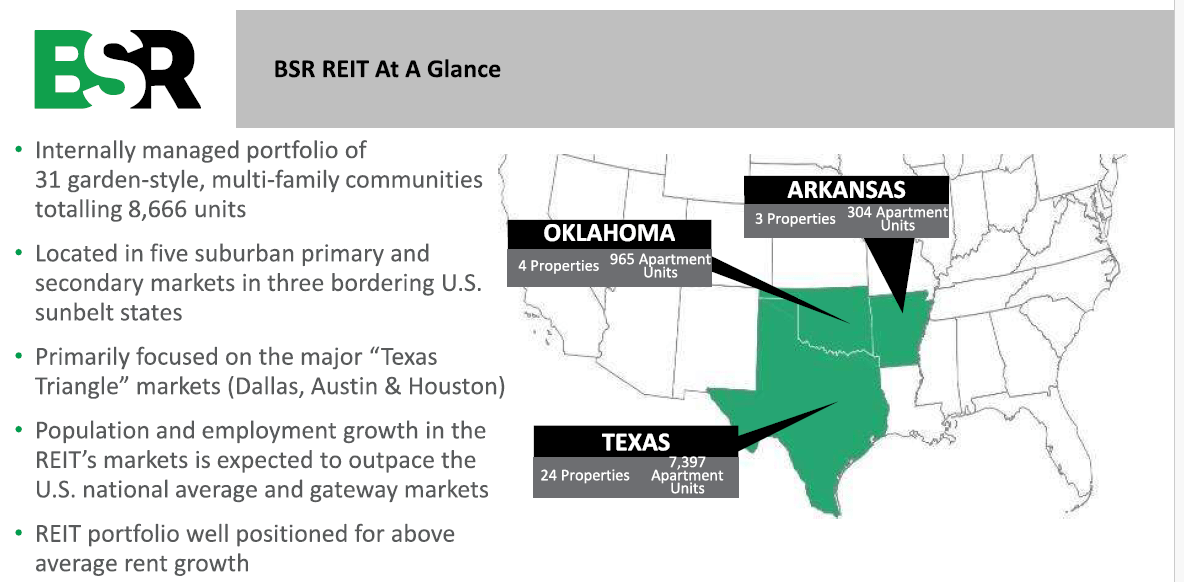

BSR Real Estate Investment Trust (OTMKTS: OTCPK:BSRTF )(TSX:HOM.U:CA) is a Canadian entity, that owns and manages multi-gamily residential rental properties in the sunbelt region of the United States. Texas houses 24 of the 31 properties, comprising 7,397 of its 8,666 units. Oklahoma comes in a distant second in property and unit concentration, whereas Arkansas brings up the rear.

{kind=link}

Nov 2023 Presentation

Looking at the city level breakdown, Dallas contributes over 40% of the net operating income or NOI, followed closely by Austin and Houston at close to one-fourth each. Oklahoma City and Little Rock (other) get credit for the balance.

Q3-2023 Report

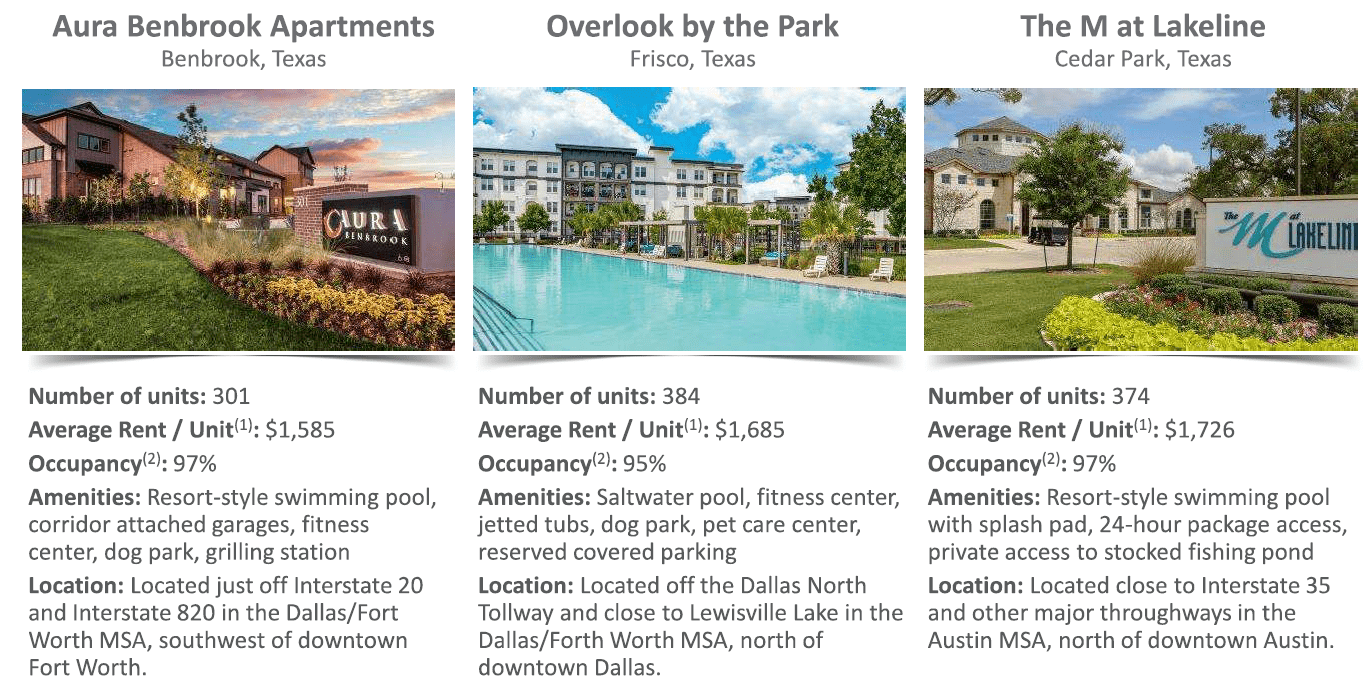

This REIT commenced operations in May 2018 and thus is a fairly new entrant to the multi-family market. Around 36% of the interest is held by founders of this REIT . BSRT's portfolio comprises properties that are located in suburban areas with low density. These properties caters to clientele that want more than a cookie cutter, garden walk up unit. BSRT tenants enjoy amenities like nature trails, clubhouses, dog parks, resort style pools and splash pads, playgrounds, private work pods and barbecue grilling stations.

{kind=link}

Nov 2023 Presentation

Besides the 31 income producing properties, BSRT also owns one property that is under development in Austin. The REIT is on course to complete this 238 unit community in early 2024 and expects to have it leased out by the same year end. The management is pretty disciplined and does not pursue growth just because it has a relatively small portfolio due to its recent beginnings. The earnings call showed their commitment to the cause.

So to us, it's pretty simple. We've said and we've always said this, if we see a stabilized cap rate about 150 basis points on top of our cost of debt, we will pursue that. We see a lease up about 275 to 200 basis points on top of our cost of debt, we'll pursue that acquisition. And if we see a development sitting around 250, on top of our cost of debt, we will pursue that development. To-date and this year, and since our last acquisition in December of '21 we simply just have not seen those spreads on yield that generate -- that drive returns for our investors.

Source: Q3-2023 Earnings Call Transcript

Portfolio As Of Q3-2023

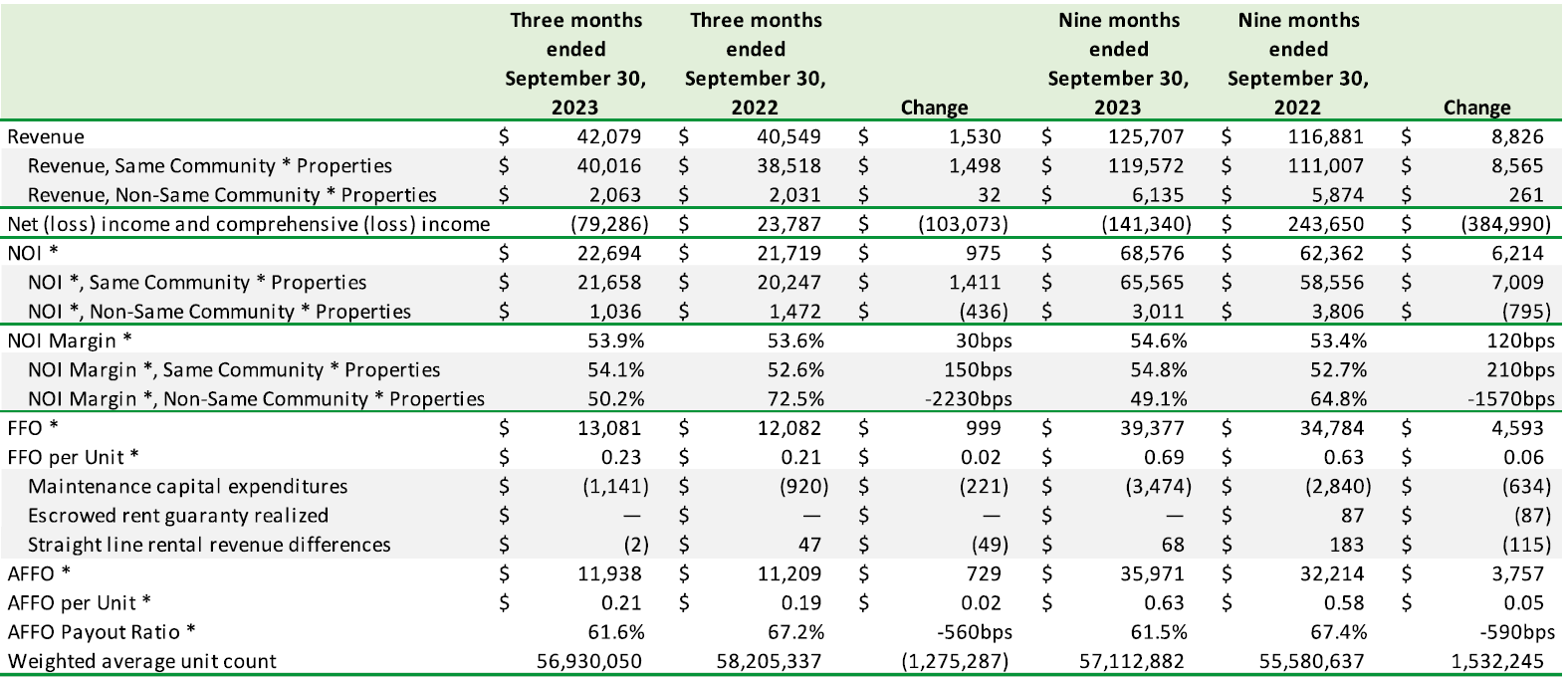

The 2.7% overall growth in rental rates resulted in a 3.8% increase in the revenue. The increase in the rates from lease renewals was the primary contributor to the overall growth number.

{kind=link}

Q3-2023 Report

The Texas Property Tax legislation noted earlier in this piece, along with revised assessments resulted in a lower real estate tax expense. While there were offsets to this in the form of higher insurance and other operating expenses, the year over year total net operating income or NOI still came out ahead by 4.5%. Impressively, and unlike most the other REITs that we have covered, the income generated by the interest rate swaps more than offset the higher interest expense and the funds from operations or FFO beat the prior year by 8.3%.

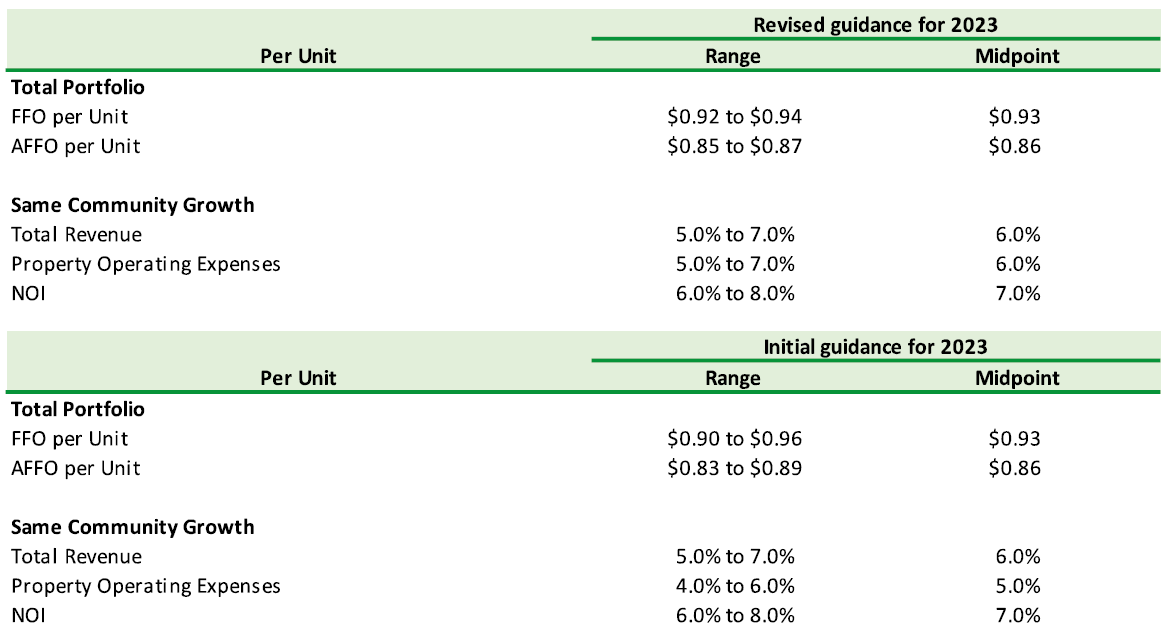

BSRT updated its guidance for 2023 taking into account the $1.4 million in property tax savings, and the higher estimate for interest and insurance expense.

{kind=link}

Q3-2023 Report

The BSRT 8,666 unit portfolio was a little over 95% occupied at the end of Q3.

{kind=link}

Q3-2023 Report

While there was a slight uptick in the numbers compared to last year, the total portfolio occupancy was more or less flat compared to Q2-2023 (95.3%). All the cities, except Austin, had a noticeable rise in the blended lease rate growth in Q3, resulting in a overall 2.7% increase. Management was prodded regarding the elephant in the room during the earnings call and things got worse in Q4, but management expects stability in the new year.

So we have three properties in the Austin market right now that are being impacted by supply. And October, actually, it was new leases were signed at about -- I guess it was a negative 7%. So those properties are being impacted. However, you have to remember that that's just a small percentage of our portfolio. We expect that the first half of next year to probably be similar to Q4. And then the latter half of next year is harder to get because -- Dan is going to speak about, a little bit about the supply and the absorption of it and what we expect to happen in the second half of the year, which is similar to some of the our peers, they've also said that we expect better absorption. So while I can't say right now, what I think is going to happen for the entire year, I can certainly say that things probably will be stable in Q1 and Q2, compared to where we are now.

Source: Q3-2023 Earnings Call Transcript

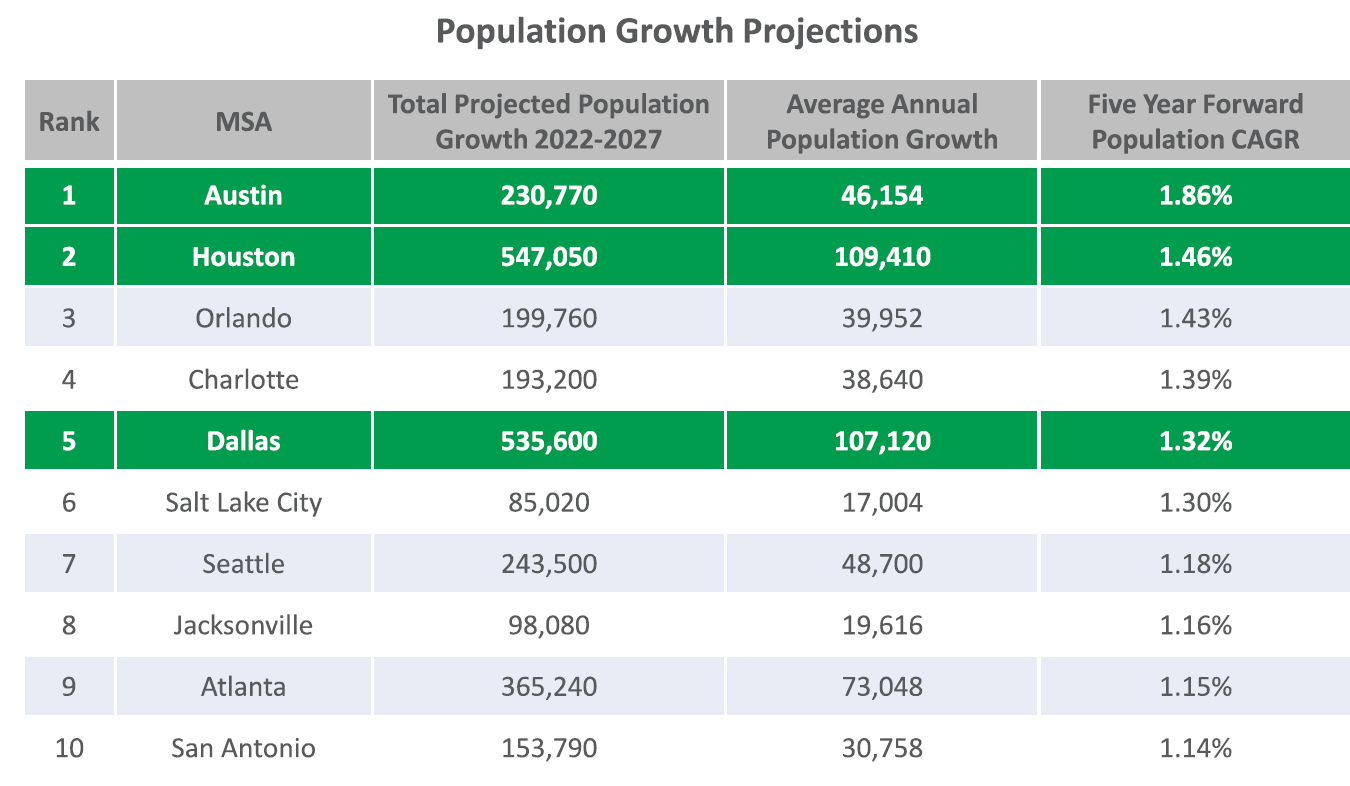

Management expects the supply to continue outpacing the demand until mid next year. The source of their optimism is the dramatic drop in multifamily residential starts that should begin to change dynamics by then. That fed into their confidence for a "positive potential and optimistic outcome" for the tail end of 2024 and next couple of years. We would have to give the benefit of the doubt to the management, especially considering the population growth projections of their key markets.

{kind=link}

Nov 2023 Presentation

The reduction in the property taxes that was recently passed into law will only add to the attractiveness of these cities.

One reason our Texas markets are attracting so many outsiders is the state's highly competitive taxation regime. There has been a very important tax development recently that positively impacts BSR. You may recall that on our last conference call, I noted that the Texas legislature passed Texas State Proposition 4 in order to lower real estate taxes including for multifamily residential rental properties. We were waiting on a constitutional election results in early November to see if the reduction would come into effect. Well, the election happened two days ago, and the tax cut has been ratified. We estimate that it will result in a decrease of real estate taxes for the REIT of $1.4 million and it applies this year.

Source: Q3-2023 Earnings Call Transcript

Debt and Liquidity

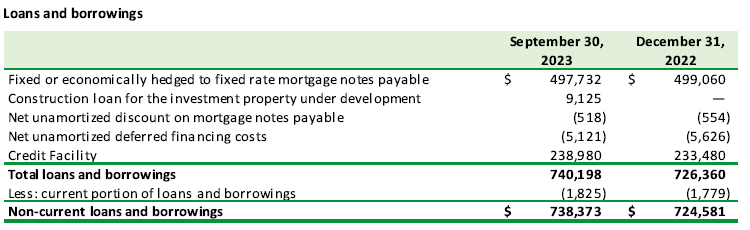

At September 30, BSRT had drawn $239 million from a credit facility secured by 13 of its properties. Additionally, the REIT had $498 million in mortgages and a $9 million construction loan (for the property under development) on its books.

{kind=link}

Q3-2023 Report

Almost all of BSRT's debt effectively enjoys a fixed rate, either directly or via swaps in place. The weighted average interest rate on the mortgages was 3.2%. The credit facility is a different beast as it follows shorter term interest rates, which was 6.9% at the end of Q3, versus 5.9% at the end of the previous year. The debt maturities do no come calling until 2025, when things will get interesting unless the rates start to change course.

{kind=link}

Q3-2023 Report

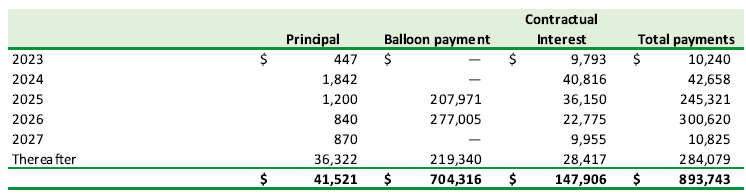

This residential REIT also had $40 million in outstanding convertible debentures at the reporting date, that bore an interest rate of 5%. These pay interest on a semi annual basis (March 31 and September 30) and are redeemable by the REIT ( subject to conditions being met ) until September 30, 2024. After that date, its fair game for BSRT as far as redemption goes.

On or after September 20, 2024, the convertible debentures are redeemable by the REIT, in whole or in part, at a price equal to the principal plus accrued and unpaid interest. Additionally, the REIT may, at its option, elect to satisfy its obligation to pay all or any portion of the redemption by issuing Units to the holders at a value of 95% of the current market price of the Units on the redemption date.

The conversion price on these is $14.40/unit, making redemption by the REIT or an accretive conversion by the unitholders a pipe dream at the moment. These debentures mature on September 30, 2025.

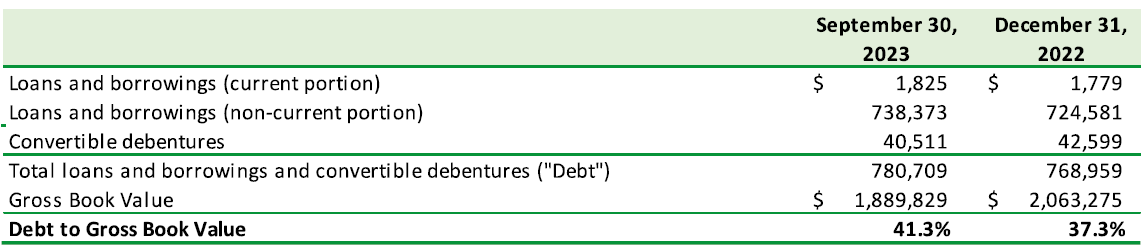

The overall debt to gross book value increased from 37.3% at December 31, 2022 to 41.3% at September 30, 2023. This was more a function of reduction in the fair market value rather than an increase in borrowings.

{kind=link}

Q3-2023 Report

At September 30, the average term on the total debt of this REIT was 4.1 years. In terms of dry powder, BSRT had $3.9 million in cash and $196.2 million available on the aforementioned credit facility. Additional borrowings could also be had by using the unencumbered properties as collateral.

Dividends

BSRT paid 4.17 cents in monthly dividends for years (maintained during pandemic) before raising it to 4.33 cents in February 2022. There has been no change since then.

{kind=link}

Seeking Alpha

Considering that it currently trades at $10.33, it yields its unitholders around 5.03%. MAA is also in the vicinity, yielding around 4.52% (quarterly dividend $1.40, current price $123.89). The third wheel and one that does not appear to respect their personal space, is the 10 year risk free rate at 4.39%.

While investing in a REIT, investors hope to participate in the long term growth of the business. However, when the spread with the risk free counterpart is low, it is tempting to sit on the sidelines earning a solid yield over the short term, until the tide appears to be changing course.

Verdict

BSRT has not traded at this big a discount to its tangible book value in a long time.

Management has also put its weight behind their valuation (weighted average capitalization rate 4.9%) by choosing to buy back units with the excess liquidity.

{kind=link}

Q3-2023 Report

The buybacks have been at an average price of around $13.50 over the 12 month period. The lack of accretive acquisitions has played a role in the allocation of funds for the above purpose.

We are constantly reviewing our capital allocation options. As long as our units are trading at a significant discount to NAV buybacks remain an attractive option that we can capitalize on when opportunities arise. Conversely, if we see property acquisition opportunities at cap rates, even approaching our implied trading cap, we will equally capitalize on the same.

Source: Q3-2023 Earnings Call Transcript

While BSRT is no stranger to trading at a discount, the 55% discount to IFRS values seems a tad pessimistic. If or rather when, the discount "normalizes" to even 35%, we are looking at the potential for 44% capital appreciation. Of course we are assuming property values stay static, but since NOI is moving up, it is a fair gamble that property values will cycle back to at least this point over the medium term. The 11X FFO for residential REIT is also extremely cheap, even accounting for where risk-free rates are. We rate this a buy and will be purchasing a few units soon.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

BSR REIT: When It Gets This Cheap, You Need To Buy