BSTZ - BSTZ: A 10.8% Yield From Venture Capital And Tesla

Summary

- BSTZ is paying out a 10.8% yield from its portfolio of private startups, tech stocks, and semiconductor companies.

- The CEF recently cut its monthly dividend payout by 16%.

- This was a forced move with return of capital ramping up in recent months on the back of the pertinent stock market pullback.

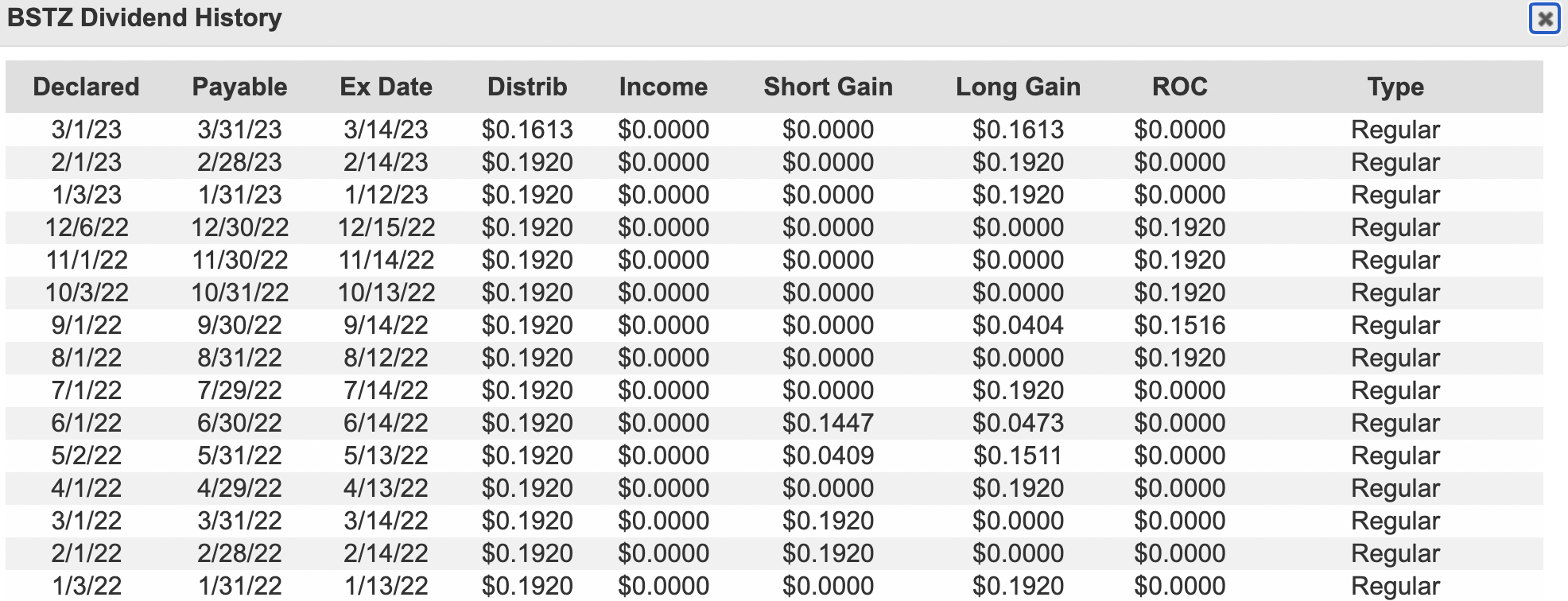

BlackRock Science and Technology Trust II ( BSTZ ) last declared a monthly dividend of $0.1613 per share , a 16% decrease from its prior payout and for an annualized 10.8% yield. This fat yield paid monthly is incredibly enticing and around 120 basis points more than the yield available on BSTZ's sister fund BlackRock Science and Technology Trust ( BST ). What's the catch? And how is a closed-end fund focused on investing in high-growth but likely unprofitable private startups able to maintain a nearly 11% yield?

BlackRock Science and Technology Trust II

Even more jarring is BSTZ's insistence on using code names to describe its private investments. Tesla ( TSLA ) forms 3.87% of the portfolio, Wolfspeed ( WOLF ) is 3.03%, and Marvell Technology ( MRVL ) forms 2.55% of the $1.657 billion BSTZ which went public in the summer before the pandemic. The first step in going long the yield would be discerning what these projects are and whether the underlying companies are the types of businesses you'd want to allocate your capital to.

BlackRock Science and Technology Trust II

{kind=link}

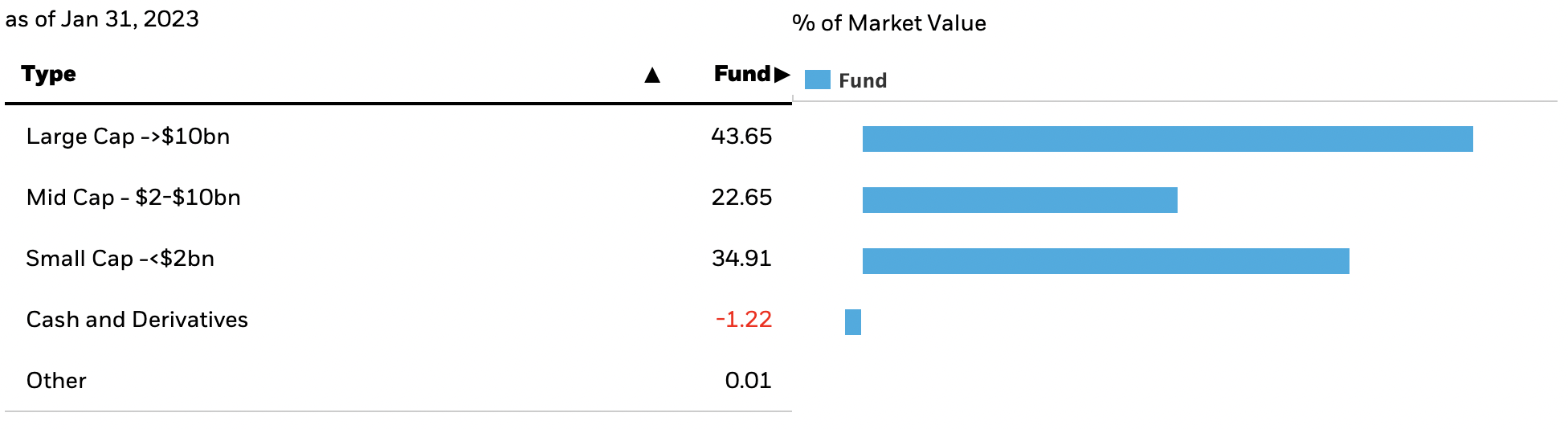

Critically, BSTZ's exposure to small and mid-cap companies forms an aggregate of 57.56% of the fund. Hence, the CEF represents a level of multilayered risk, especially when compared with its sister fund which focuses on larger cap companies and has a smaller VC exposure.

Private Startups, Risks, And Long-Term Capital Gains

BSTZ tilts towards software and semiconductors. The CEF previously had Project Kafka as one of its largest position and a quick look at their recent SEC filings establishes this as Klarna ( KLAR ), the Swedish buy now pay later fintech. There is not much more information on the other projects.

BlackRock Science and Technology Trust II

{kind=link}

Hence, BSTZ investors have to be comfortable with not knowing what they're invested in and will just have to make way with the sectors the CEF has coalesced its investments around. This opens up the next step, which is to establish the direction of the monthly payouts. The most recently declared payout was a 16% decrease from the prior, after what had been an uninterrupted regular monthly payout of $0.192 per share since late 2021. The break with stability was forced by collapsing private market values and a pullback of public tech stocks on the back of rising Fed funds rates.

The CEF had been forced to depend more on the return of capital in recent months, and the cut was likely the only way to prevent this from further eroding its asset base. This forms the third step in whether to go long the 10.8% yield. As a rule of thumb, long-term capital gains are the preferred form of distribution from a CEF, then short-term capital gains, and then ROC.

{kind=link}

Over the last 12 months, the company has paid out a total of $0.9196 from ROC distributions. This is around 40.45% of total distributions of $2.2733 over the same time period. Essentially, for every $1 in dividends earned by BSTZ owners, 40 cents of that comes from their own capital. This is problematic and likely presents one of the most egregious forms of income available to investors.

The CEF is not cheap, charging a gross expense ratio of 1.31% for the privilege of being paid back your own capital. Of course, the risk here for the bulls is that ROC is maintained in future months against what remains muted equity markets. However, the strong performance of Tesla over the last few weeks will likely represent a boost for the CEF, but the larger ROC narrative is not satisfactory.

The Discount To NAV And The End Of The Rate Hike Cycle

With private illiquid companies forming such a large part of the CEF, these are likely held to boost the NAV of the CEF on the mark-to-market changes to their valuation rather than for the distributions. This forms one of the core bullish arguments for BSTZ with retail investors seldom having private market VC-type exposure.

Further, the CEF currently trades at a large 12.44% discount to its NAV. This is an improvement from a discount of nearly 20% as of the end of December last year. The current double-digit discount is still below its historical 3-year average, and a return of this back to the single-digit range is a possible near-term movement that looks likely on the back of a dovish Fed pivot. Inflation is falling, and the market currently expects just two further 25 basis points hikes to the Fed funds rate. This would bring an end to the current headwind and allow underlying valuations to stabilize.

Against this possible catalyst, BSTZ is a hold. I'm not a fan of ROC as a percentage of trailing 12-month distributions being so high at 40%. This is an outsized number that likely renders this fund to be more geared to investors attracted to its highly mystical private startup portfolio. BST likely represents the better marginal purchase here, but I'll pass on both.

For further details see:

BSTZ: A 10.8% Yield From Venture Capital And Tesla