BSTZ - BSTZ: Attractive Discount For This Beaten Down Tech Fund

2023-03-13 21:32:01 ET

Summary

- Interest rates have continued to wreak havoc on growth plays such as BSTZ.

- With the expectation that the Fed may have to go higher for longer, it can still put some uncertainty on this fund.

- Despite the risks, I continue to find BSTZ attractive at the current discount for a long-term investor.

Written by Nick Ackerman, co-produced by Stanford Chemist. A version of this article was originally published to members of the CEF/ETF Income Laboratory on February 28th, 2023.

BlackRock Science and Technology Trust II ( BSTZ ) invests in a portfolio of technology investments in the public and private markets. With growth investments under significant pressure from higher interest rates in the last year, the results haven't been pretty. Despite this, I continue to believe BSTZ is an attractive name for a longer-term investor that can withstand volatility. Even better, it's at a more attractive price as tech got wrecked.

Our last update was in August 2022; BSTZ was relatively more attractive than the BlackRock Science and Technology Trust ( BST ), BSTZ's predecessor. BST tends to hold weightings more towards larger-cap tech plays with less of an emphasis on private investments. However, BST has incorporated smaller, more speculative names over the last couple of years. This has meant some portfolio overlap. However, BSTZ's average holding market cap comes to $43,336.1 million, whereas BST carries a portfolio with an average market cap of $523,992.0 million.

Since that time, interest rates have continued to pressure the fund's performance. Below is the comparison to the SPDR S&P 500 ( SPY ). This isn't a direct benchmark but can provide some context for the broader market moves.

YCharts

Given the continued pressure, uncertainty and more speculative nature of the smaller growth names, I still only view this as a more long-term investment. That being said, the discount remains attractive as the price comes down. On top of this, while the Fed is expected to keep interest rates higher for longer, we should still be closer to the end of rate hikes rather than the beginning.

The Basics

- 1-Year Z-score: -0.62

- Discount: -15.55%

- Distribution Yield: 11.57%

- Expense Ratio: 1.31%

- Leverage: N/A

- Managed Assets: $1.574 billion

- Structure: Term (anticipated liquidation date around June 26th, 2031)

BSTZ's objective is "providing total return and income through a combination of current income, current gains and long-term capital appreciation." To achieve this, they will "invest at least 80% of their total assets in equity securities issued by U.S. and non-U.S. science and technology companies in any market capitalization range, selected for their rapid and sustainable growth potential from the development, advancement and use of science and/or technology."

They also utilize an options strategy to help generate additional returns. At this time, the fund is 26.78% overwritten. This is on the lower end and indicates they are more bullish. Writing calls against positions in their portfolio is a slightly defensive strategy. This is slightly above the overwritten portion that it was running earlier in 2022 .

The options played a role in the fund to help negate some of the downward pressure. That being said, it's only a slightly defensive strategy that isn't able to reverse all the losses we experienced with the fund.

Performance - Interest Rate Pressures

Interest rates significantly impacted BSTZ and its portfolio of growth names. As mentioned at the open, we should be getting closer to the end of the rate hiking cycle. Stabilization would provide this fund with a significant boost or at least stop pressuring the fund to the downside.

Interestingly, as we've been looking at preferred and other fixed-income funds, we see a similar trajectory. When the 10-Year Treasury Yields started to descend, we saw a sharp recovery in BSTZ. However, as soon as yields started climbing once again, we saw the same trend we experienced over the last year, the price coming down under significant pressure.

The below chart shows price performance only, not total returns that would factor in the fund's distributions.

YCharts

Perhaps inaccurately, this is why some have been labeling tech/growth investments as long-duration assets. While duration pertains to debt investments, we've seen similar trends in BSTZ compared to debt investments. So calling them a long-duration asset isn't totally off the market, at least with the general idea.

Despite the sell-off the fund faced, the fund has still provided fairly strong results since its inception. This would be thanks to the distributions the fund had along the way, albeit significantly off where the fund's results were at through 2021.

YCharts

What has also happened is the fund's discount has opened up due to this uncertainty and sell-offs. It's off the lows we saw in 2023 but still down substantially from the average discount.

The caveat is that this fund isn't all that old, and when it launched, we were thrust into COVID. That ultimately saw the fund perform exceptionally well as all sorts of speculative names rocketed higher. So the average here might not be as reliable as a gauge as we've historically seen with CEFs being mean-reverting.

Distribution - Options Helped, But Risk For A Cut Remains

Since the original publication, BSTZ has cut its distribution. Here's what I was looking at prior to the cut being announced and why I believed it was at risk. Until a market turnaround, it will remain at risk too. The new distribution rate works out to 11.57%, and the NAV rate is 9.63%.

While I'd love to say how safe the fund's distribution yield is, I don't think we can cozy up to the current payout at a 13.14% distribution rate and a NAV rate of 11.37%. It's true; thanks to the significant discount the fund actually has to earn much less than the yield shareholders can receive, it's still really elevated.

BlackRock tends to refrain from cutting its distributions, which can benefit some investors if it's helping support a higher valuation. In this case, the fund is still trading at a large discount, so that a distribution cut could have a minimal impact. That being said, given their short history, they also probably don't want to be too quick to adjust it lower, either.

{kind=link}

BSTZ Distribution History (CEFConnect (reflects the distribution cut))

A CEF that raises its distribution over time is quite rare. If the market recovers significantly this year, the elevated yield could moderate. We've already seen how sharp a reaction can occur when yields drop. So it appears they will still be holding out for the potential rebound. As they do, it can erode some of the fund's current capital base away by sustaining the distribution as things remain pressured.

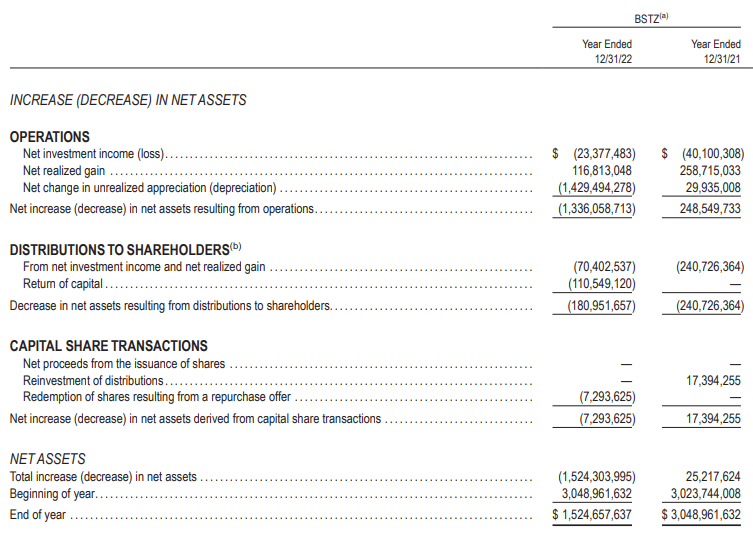

A silver lining here is the options writing strategy the fund implements. Hot off the presses is the latest annual report . The options contributed to over $100.5 million in realized gains for the fund. That accounted for 55.5% of covering the fund's distributions in the prior year.

BSTZ Realized/Unrealized Gains/Losses (BlackRock)

They even came up with around $16.559 million in gains on their underlying investments. Worth noting is that despite the sizeable drop in the fund, it has most recently closed above its inception NAV of $20 at $20.27. So it's essentially flat, but that doesn't count all the distributions the fund paid along the way either.

That being said, it clearly wasn't enough to offset the massive $1.432 billion in unrealized losses. Those are the aggregate losses the underlying portfolio experienced through 2022.

With this fund, they don't have any net investment income. Meaning that the entire distribution relies on capital gains to be funded. This isn't unusual for a tech-focused fund, whether from BlackRock or elsewhere.

{kind=link}

BSTZ Annual Report (BlackRock)

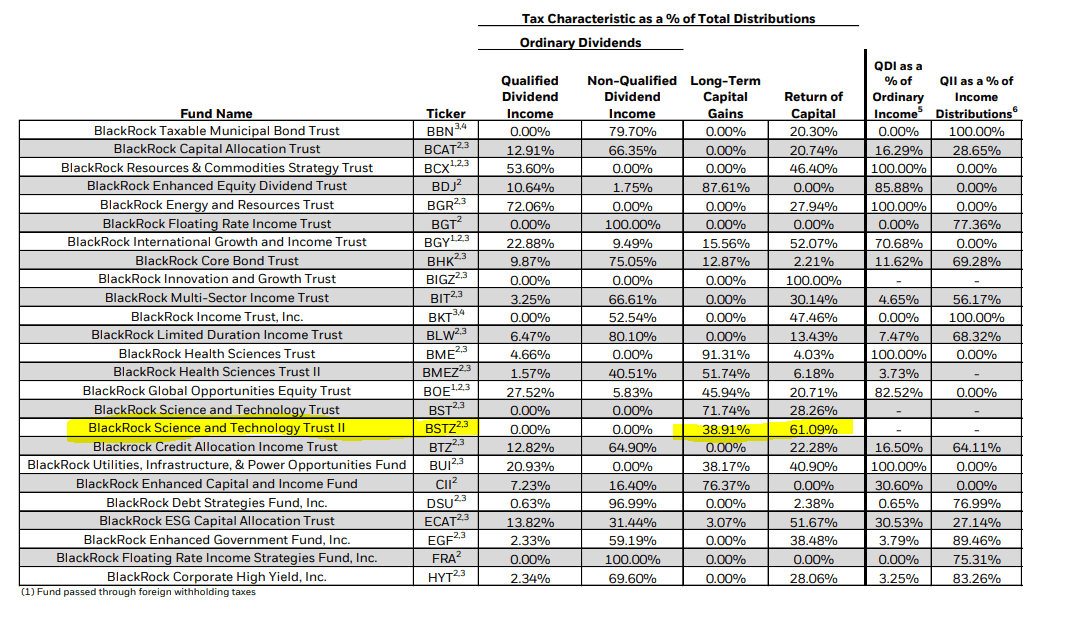

Given the sizeable losses for the year and the lack of realized gains in the portfolio, it's only natural that we see return of capital in its distribution for 2022 . In this case, it would be considered destructive ROC as the NAV declined.

{kind=link}

BSTZ 2022 Tax Classification Breakdown (BlackRock)

BSTZ's Portfolio

While the options writing in their portfolio is an active part of their portfolio, that wasn't the only moving piece. The turnover rate for the last year was 47%, a sizeable bump from 18% in the prior year. Interestingly, it was similar to the 2020 turnover rate we saw 2020 at 45%.

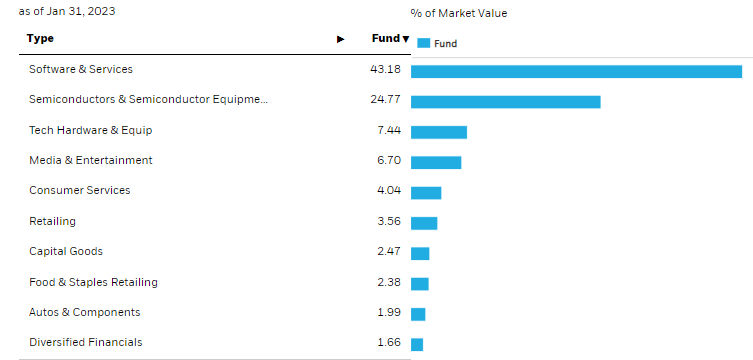

The portfolio remains dominated by tech-oriented companies, with software and services being the largest allocation in their portfolio by a considerable amount. Another large slice of the pie is in semiconductors and semiconductor equipment, which has been facing significant headwinds with a glut in personal electronic chips.

{kind=link}

BSTZ Sector Allocation (BlackRock)

When looking at the geographic exposure, we can see the fund isn't afraid to invest outside the U.S. However, U.S. exposure remains the largest and in a dominant position of nearly 60%. One notable jump was from exposure to China earlier in the year when it was a 3.38% weighting. A jump to 12% might not constitute a significant weighting, but the relative increase was meaningful. With a higher allocation to China, geopolitical risks can become an issue.

BSTZ Geographic Exposure (BlackRock)

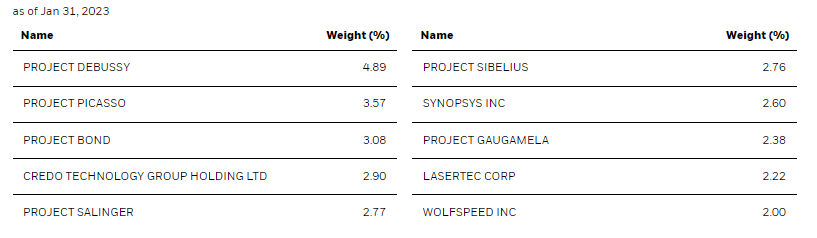

Looking at the top ten holdings, we see a notable name that no longer is a large position. That is Project Kafka (aka Klarna (KLAR)).

{kind=link}

BSTZ Top Ten Holdings (BlackRock)

This was listed as the fund's "largest detractor from relative performance." This had been a hot name that was getting some lofty valuations. Essentially, a poster child of 2020's insane valuation of private investments. Klarna had its valuation cut by 85% in 2022.

At the individual position level, the Trust’s off-benchmark position in privately held buy-now-pay-later company Klarna Inc. was the largest detractor from relative performance.

Depending on how you look at this investment, it's either a really bad or mildly bad investment. The reason is that they picked it up for a cost of $23.355 million. The value at the end of 2022 was almost $16 million. So the actual losses here weren't as dire relative to the cost, but that also means they couldn't capitalize on the investment since, at the end of 2021 , it was listed as the same cost. However, the value was listed at nearly $118.6 million. This likely wasn't the manager's fault either, as these pre-IPO and private names often come with restricted positions. 33.4% of the fund was considered restricted securities at the end of 2022

This brings up a main point on BSTZ for investors; private investments can mean a discount is warranted to some degree due to uncertainty. The valuations might not always be accurate until a funding round is done. Then, a true valuation can become known.

Something is only worth what someone is genuinely willing to pay for, which means that level 3 investments can be ambiguous. They can value it how they'd like with all the assumptions in the world, but a funding round could come through and significantly change the assumptions.

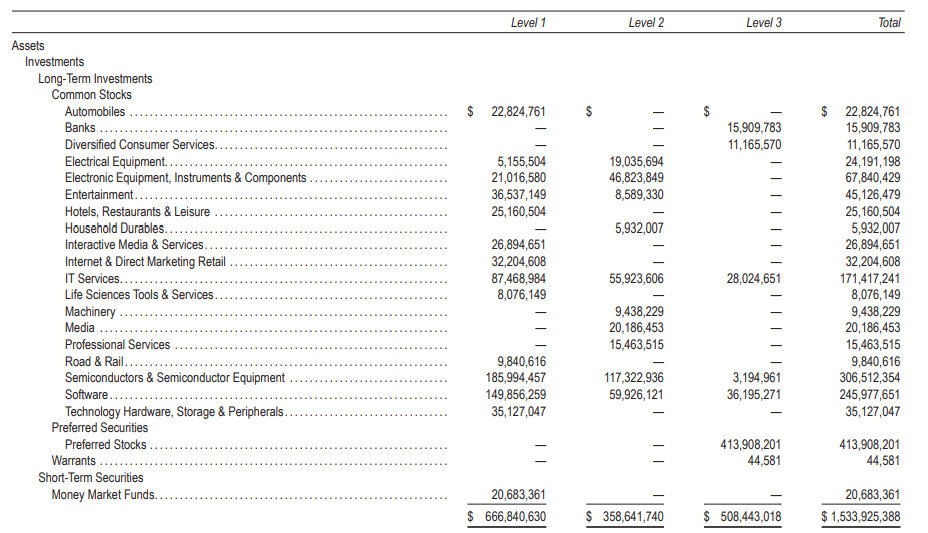

Just over 33% of BSTZ's portfolio was classified as level 3 securities at the end of 2022. Perhaps unsurprisingly, this is also consistent with the restricted portion of the portfolio.

{kind=link}

BSTZ Asset Level Breakdown (BlackRock)

Of course, BlackRock is the largest asset manager in the world and probably knows a thing or two about valuing securities. So my concern is fairly limited in this regard.

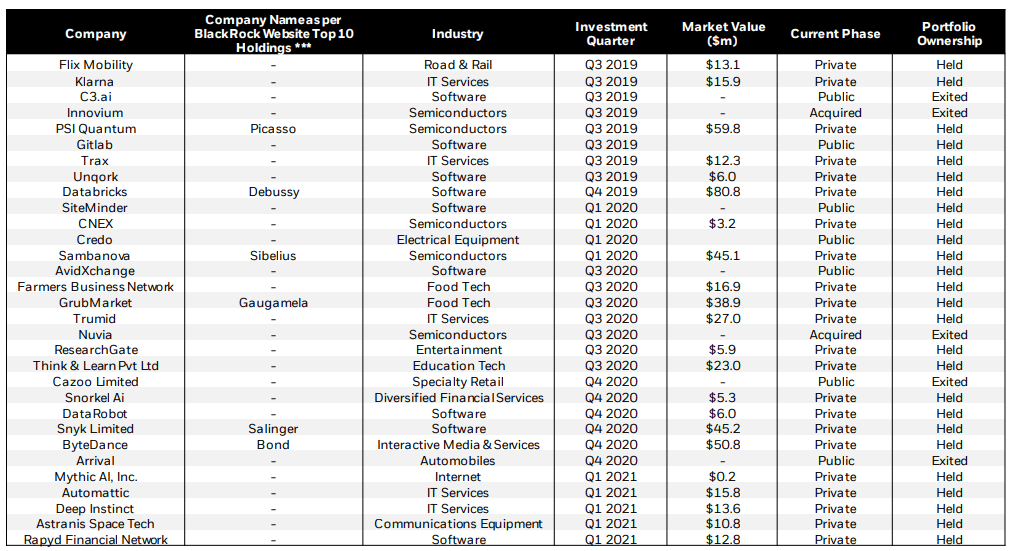

They haven't invested in any new private investments through the entirety of 2022. However, one important change is that they are now identifying the top ten names when they refer to them as "project" holdings. In their latest commentary , they provide the breakdown.

{kind=link}

BSTZ Private Investments (BlackRock)

For what it's worth, we've already broken down several of these previously , but it's a beneficial change nonetheless for greater transparency.

Conclusion

BSTZ has taken the full force of the tech wreck, but I believe it remains an attractive fund for those longer-term investors that can handle volatility. The fund's discount is quite attractive, even with some uncertainty in its private investments. The fund's distribution also makes it much easier to hold, in my opinion. When holding growth investments, you are often at the mercy of only seeing returns when they appreciate. This is one way that we can get some returns along the way that can't be taken away - assuming one isn't reinvesting.

For further details see:

BSTZ: Attractive Discount For This Beaten Down Tech Fund