HRUFF - BTB: 10% Yielding Diversified REIT

2023-10-11 12:39:11 ET

Summary

- BTB Real Estate Investment Trust is focused on reducing its office sector footprint.

- The REIT currently has 75 properties spanning 6.1 million square feet, valued at $1.23 billion.

- The office portfolio occupancy is dragging down the overall committed occupancy rate, and lease maturities in the office portfolio pose a challenge in the next few years.

- The REIT does have the best possible financing in place though for the current situation and the distribution looks sustainable.

All values are in CAD unless noted otherwise.

BTB Real Estate Investment Trust ( BTB.UN:CA ) is an owner and operator of office, industrial and retail properties. It is a predominantly internally managed, diversified REIT that is trying hard to reduce its office sector footprint.

Q2-2023 Presentation

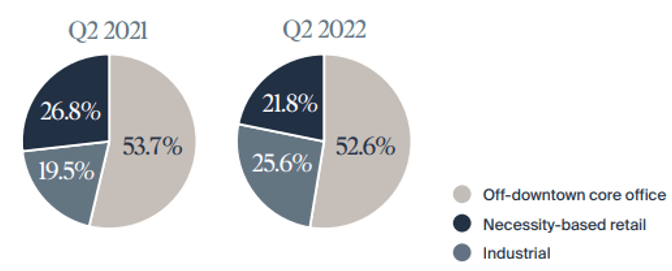

The REIT is making progress toward this goal and that can be seen by comparing the current numbers from above to its portfolio composition from the last couple of years.

{kind=link}

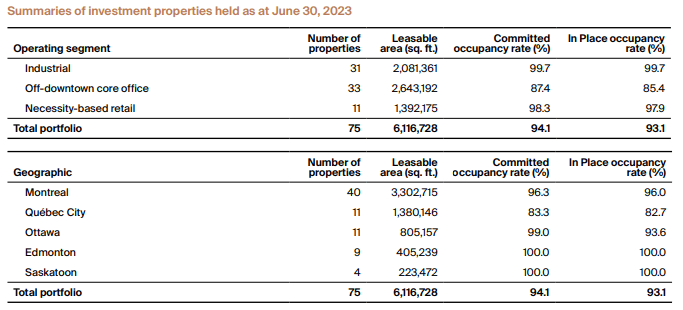

Coming back to the present, BTB has 75 properties, spanning 6.1 million square feet, with a valuation of $1.23 billion. While predominantly Montreal-based, the properties are also located in Edmonton, Saskatoon, Quebec City, and Ottawa.

Q2-2023 Financial Report

The office portfolio occupancy created a drag on the industrial and retail side, resulting in a 94.1% overall committed occupancy rate, at the last reporting date.

{kind=link}

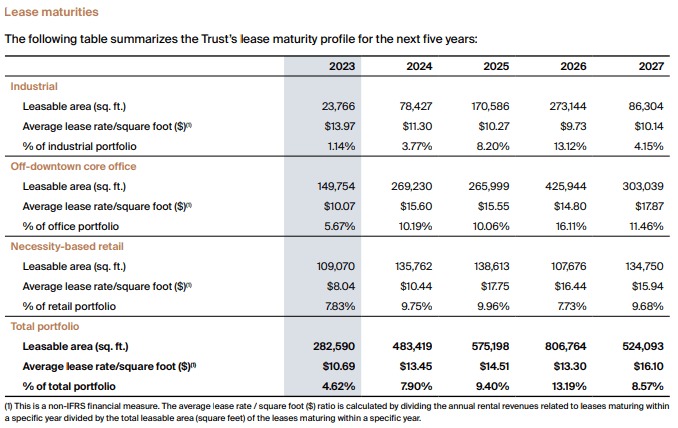

The office portfolio is also responsible for Quebec City bringing up the rear amongst its geographical peers. The weighted average lease term of the overall portfolio is 6.1 years. We can see that BTB has quite a bit of leases coming up for renewal in the next three years.

{kind=link}

While it may look like BTB will have its work cut out for itself, particularly in its office segment, it does give the REIT an opportunity to replace the in-place rents with the higher prevailing market rents in retail and industrial. BTB claims that even their office rents are currently below market. Management provided some color on this during the earnings call.

Matt Kornack

Just with regards to the lease maturity profile, I mean, you're sitting at pretty low in-place rents on both necessity-based retail and the off-downtown core office portfolios. I mean, do you believe that, that provides a bit of upside in 2023 in terms of where spreads will be. And then as we look into '24, I mean still office here at [$15] rents and necessity-based retail is just a tad over [$10] like I'm just trying to think, A, how that helps from a tenant retention standpoint? And B, kind of what the opportunity is there from a lease standpoint.

Michel Léonard

I'll give you an example. We have a government lease that's coming to maturity. It's a substantial lease that right now, the government is paying $6 net for part of the space and $1 net for the other part of the space, which is a lease that was in operation when we had acquired that property was a long-term lease. And right now, the renewal rate is for part of the majority of the space at $10 net. And the other part, I think, is at $4 or $5 net, so a substantial increase is coming our way in the form of that government lease, which is roughly 60,000 square feet.

Source: Earnings Call Transcript

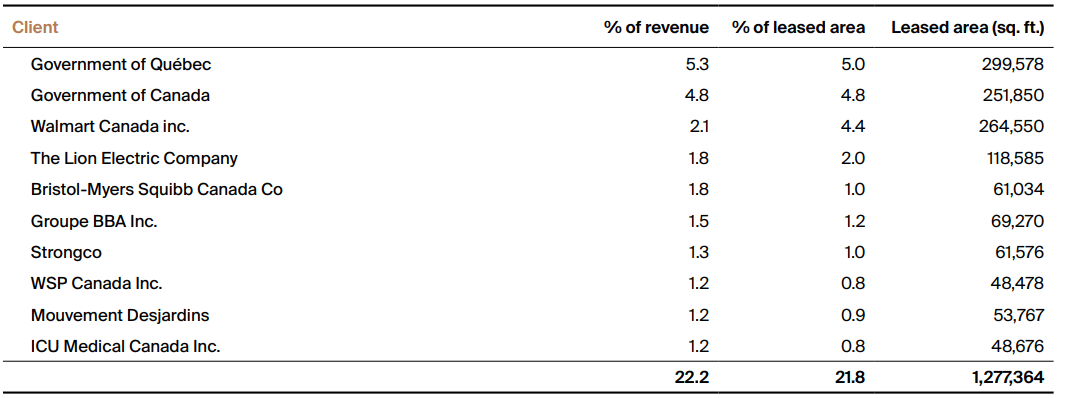

Around 22% of BTB's revenue comes from its top 10 tenants, which includes several solid names like Walmart Inc. ( WMT ) and Bristol Meyers Squibb Company ( BMY ). Over 10% of the revenue being sourced from government tenants does not hurt either.

{kind=link}

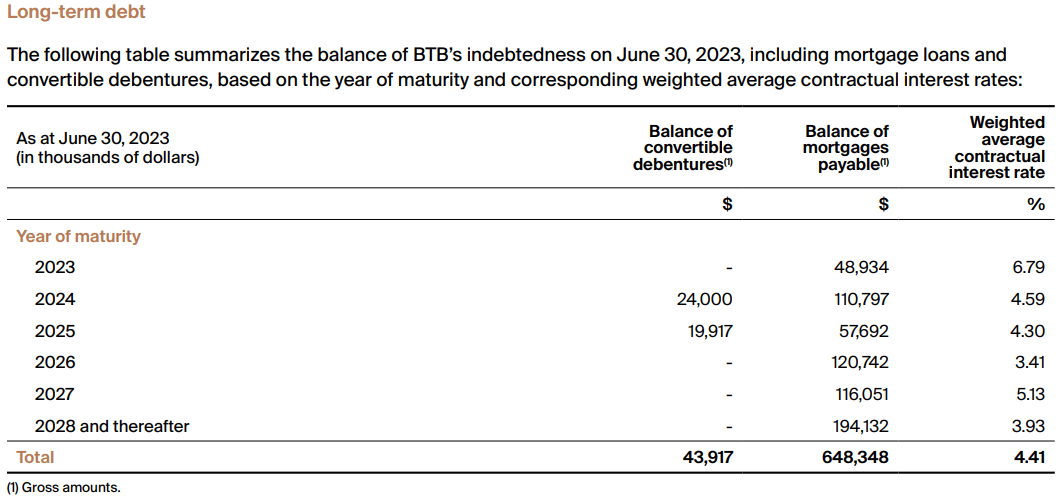

What does hurt is the rising interest rates on their close to $700 million debt, most of which is made up of mortgages.

{kind=link}

The 4.41% in weighted average contractual interest rate at June 30, 2023, used to be 3.81% at the end of Q2-2022. The majority of this REIT's mortgages ($560 million of the total $648 million) enjoy a fixed rate via swaps, the weighted average for which increased by 23 basis points from 3.62% at June 30, 2022, to 3.85% at June 30, 2023. The variable portion of the mortgages, however, witnessed a 337 basis points increase from 3.61% at June 30, 2022, to 6.98% at June 30, 2023. We expect to see this number rise in the subsequent quarters as we do not believe Bank of Canada is done yet, just like its counterpart across the pond. The weighted average term for the total mortgage loans was 3.6 years at the end of Q2-2023.

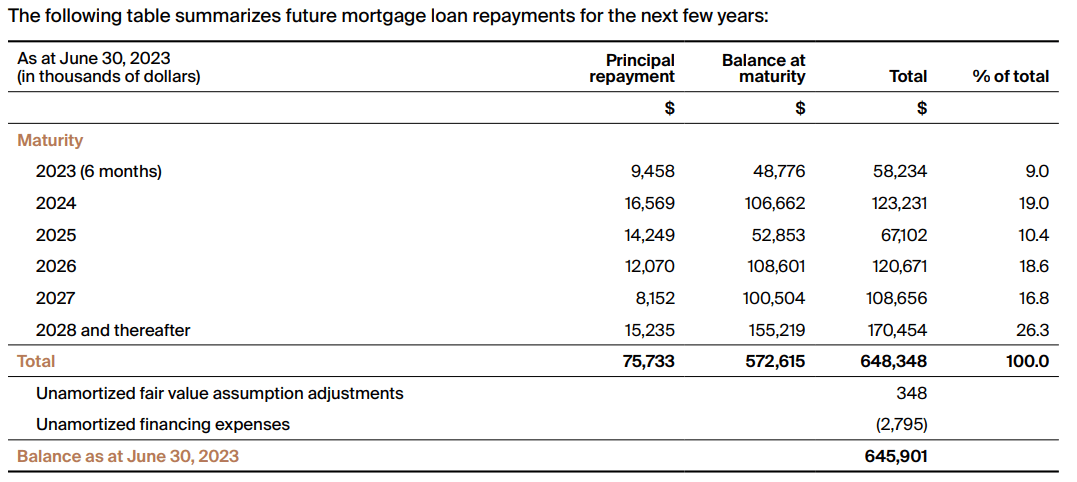

At the end of Q2-2023, BTB had around $3.7 million in cash and close to $24 million available to borrow on its credit facility, with an option to increase by $10 million. This sets up the REIT to take care of its principal repayment obligations for the next little while.

{kind=link}

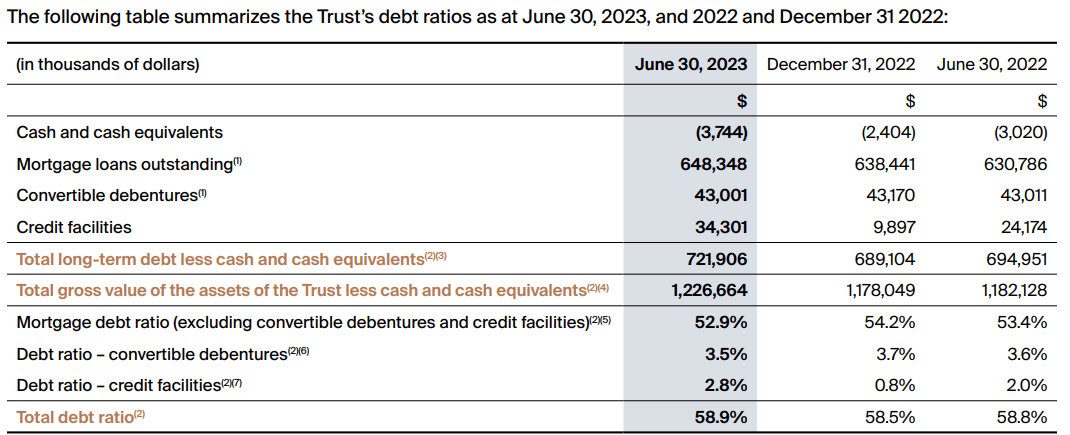

We are assuming that it will have no problem in refinancing its debt. As far as acquisitions to increase its industrial foothold, BTB might do this via additional mortgages. Whether they should increase their debt ratio or not in this market is the bigger question.

{kind=link}

Using simple FFO inversion, we can see that BTB's cost of equity is over 15%. It makes sense for the REIT to go primarily via the mortgage route, despite the rising interest costs. Besides the above sources of liquidity, BTB also has a few properties on the market and they alluded to there being some interested buyers during the earnings call.

Matt Kornack

Okay. And then just, Michel, going back to your comment on the disposition side. And what type of buyer is it that's looking at these assets at this point? Is it high net worth individuals, family offices, et cetera? Or there are some institutional guys looking at this point.

Michel Léonard

Definitely no institution and it's a high net worth and family office that we're seeing that are harvesting these acquisitions.

Source: Earnings Call Transcript

Moving on to distributions, the feature that makes income investors look favorably at REITs. Based on the current price of $3.05 and 2.5 cents in monthly distributions, BTB yields close to a whopping 10%. This was reduced from 3.5 cents a month post COVID-19 and maintained there since then.

Q2-2023 Results

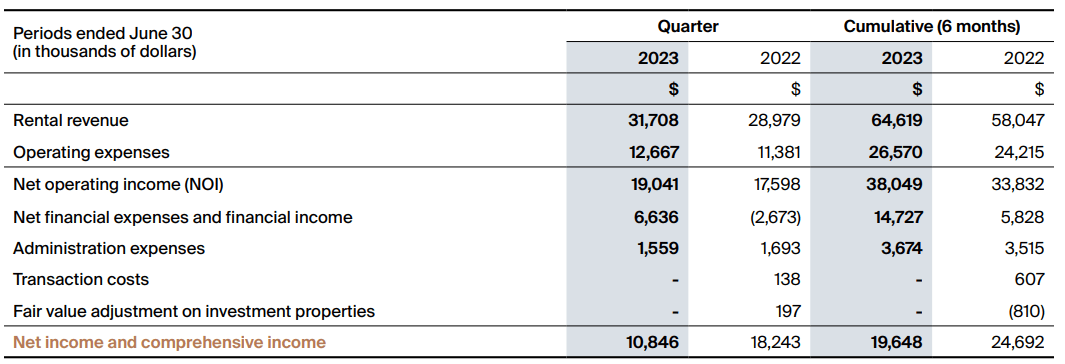

Higher leasing rates achieved on new and renewed leases and accretive impact of net acquisitions since Q2-2022, resulted in close to a 10% increase in year-over-year revenue numbers.

{kind=link}

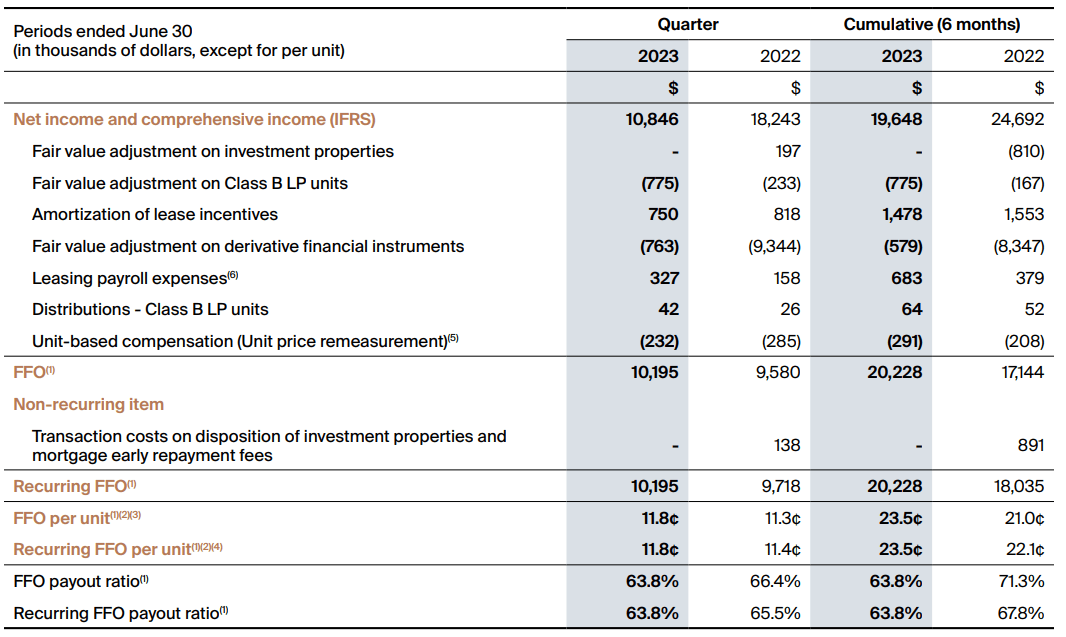

The net operating income or NOI increased by 8.2%, due to rising operating expenses. The higher interest costs cannibalized some bottom line, but the funds from operations or FFO still showed a 6.4% year-over-year increase.

{kind=link}

With the increase in the number of outstanding units compared to the prior quarter, the FFO per unit increased, but by a lower 4.4%.

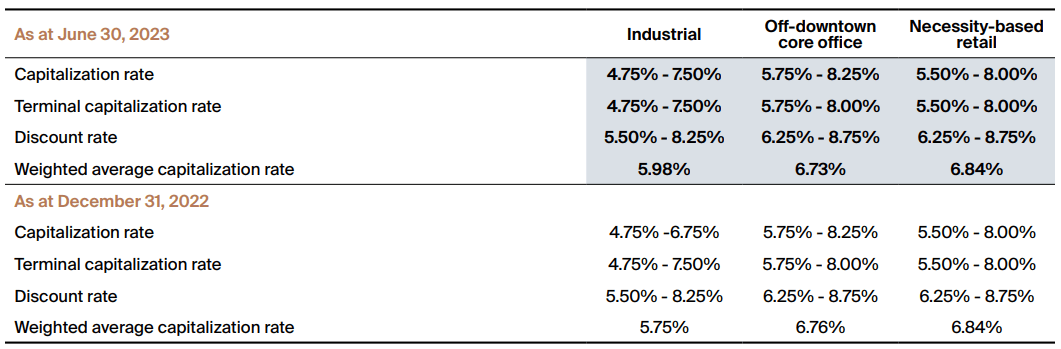

BTB also marked up the capitalization rates of all of its industrial and off-downtown core office portfolios.

{kind=link}

Verdict

BTB is currently trading at close to a 45% discount to its calculated NAV of $5.48 and at a close to 6.5x FFO multiple. The change in strategic direction of moving away from office and into industrial, brings to mind another REIT that is also in the process of diversification. We are talking about H&R Real Estate Investment Trust ( HRUFF ) ( HR.UN:CA ). The yield is considerably lower at 6.4%, and it trades at a slightly higher FFO multiple of close to 8x. The discount to NAV is however deeper at 54%.

It has bigger size, scale, and diversification and can handle the next couple of years better than a relatively smaller BTB.

So if you want a diversified REIT with potential upside, we would choose H&R over BTB. That is the relative call. Getting back to BTB, there is very little existential risk here simply as the debt is all at property level. If you go back to the ZIRP bubble days, a lot of analysts were praising the idea of unsecured debt versus secured debt. Today, it appears clear that secured debt is the real winner as it offers the ability to walk away from an individual bad property for a small loss. BTB has that option on all its properties and hence despite the very high office weighting, this is not an existential risk situation. The weighted debt maturity is also a bit better than what we saw with Artis REIT ( AX.UN:CA ) and that gives it some extra buffer. We rate this a hold and think you are likely to have positive albeit volatile returns from here. The two TSX-listed debentures, maturing in October 2024 (G series) and October 2025 (H series) are a good way to make over 8% for shorter-term investments.

{kind=link}

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

BTB: 10% Yielding Diversified REIT