BTBIF - BTB REIT: Why The Market Is Wrong About This Value Play

2023-08-03 08:35:08 ET

Summary

- BTB REIT offers a yield of ~9% with an FFO payout ratio of ~60%.

- BTB REIT is undervalued relative to historical P/B ratios due to a high proportion of office properties.

- BTB REIT has office properties that are 'off downtown core' which have performed better than downtown office properties.

- BTB REIT has $0.35 per unit in one potential densification opportunity, with 6 other potential developments in the pipeline.

All figures are listed in unless otherwise stated.

All financial data has been sourced from Capital IQ unless otherwise stated.

Price as of Writing: $3.26

Dividend Yield as of Writing: 9.20% ($0.30 per share)

Investment Thesis

BTB REIT ( BTB.UN:CA ) has been discounted by the market because of the weight that office properties make up in their portfolio. However, I feel that BTB represents a compelling investment opportunity due to its strategic shift towards industrial properties, a high dividend yield that is well-covered by FFO, a portfolio that is anchored by excellent tenants, and a densification opportunity that has been overlooked by the market.

Strategic Shift Towards Industrial Properties

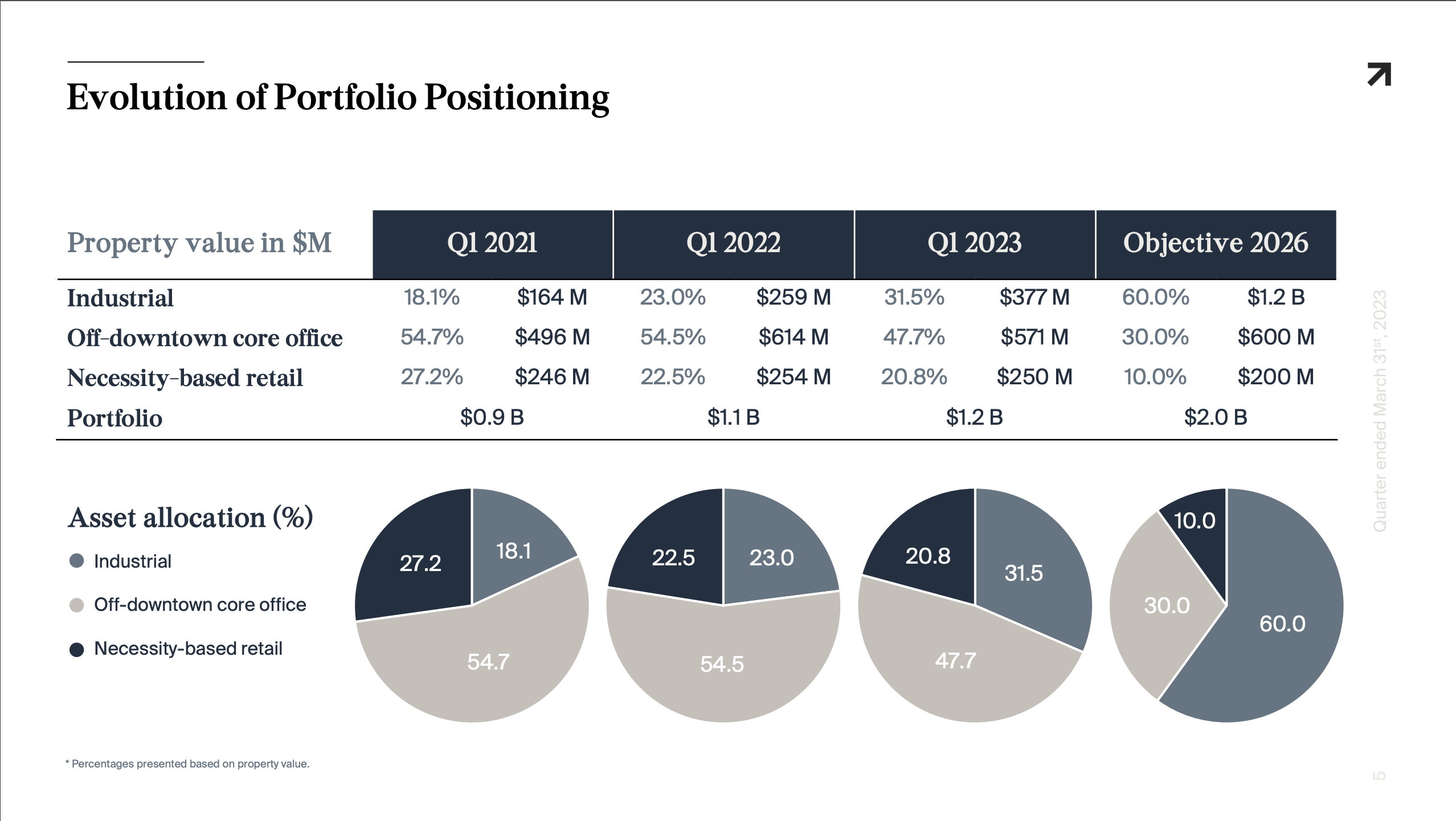

Since the outset of 2021, BTB has been keen on its commitment to bolstering its portfolio with industrial properties. In Q1 2021, industrial properties accounted for 18.1% of the portfolio, whereas, by Q1 2023, this figure surged to 31.5% – a 13.4% increase. The strategic vision is to achieve an ideal portfolio mix comprising 60% industrial properties, 30% office spaces, and 10% retail.

Evolution of Portfolio Positioning (Q1 Meeting Presentation 2023)

{kind=link}

With the pandemic forcing many consumers to shop from home, the growth in the e-commerce business soared. In 2017, total revenue in Canada was $27.58 billion which has soared to around $55.72 billion in 2023 - a CAGR of ~12.45%. The surge in growth from e-commerce caused industrial properties to soar in value as the demand for the properties increased. In Q2 2022, availability was at an all-time low of 1.6% and rents had increased 24.2% YoY. BTB noticed this trend and started moving quickly to acquire industrial properties as growth is expected to continue. The e-commerce space is projected to increase revenue at a staggering 10.55% CAGR from 2023-2027. While industrial supply has been increasing over the past quarters, national availability is still only at 2.1% - well below the 15-year average of 4.8%.

In my opinion, the shift to industrial properties should prove to be a lucrative one, as these properties have lower tenant turnover and lower maintenance costs. What I think the differentiating factor here is that BTB should be able to dispose of some of their current office/retail properties in order to fund the acquisitions of industrial properties. By doing so, they aren't taking on large amounts of external debt, and it gives them the operating flexibility to take on debt when opportunities arise. Flexibility is something that I think will prove useful as cap rates continue to expand across Canada, driving down prices of different properties.

High Dividend Yield that's Well Covered by FFO

BTB pays a current annual dividend of $0.30 making the yield around 9% per year. BTB also offers a DRIP plan whereby dividends used to repurchase units are discounted by 3% at the market price.

I believe that this extra 3% makes a huge difference in the long run, as any price appreciation that occurs on the units that have been reinvested will be 3% higher.

Not to mention that BTB's dividend is well covered by FFO - a key indicator of dividend safety for REITs. The FFO payout ratio has decreased from 63.5% in Q4 2022 to 55.1% in Q1 2023. BTB is also one of the highest-paying REITs on the Canadian stock market making its yield hard to pass up.

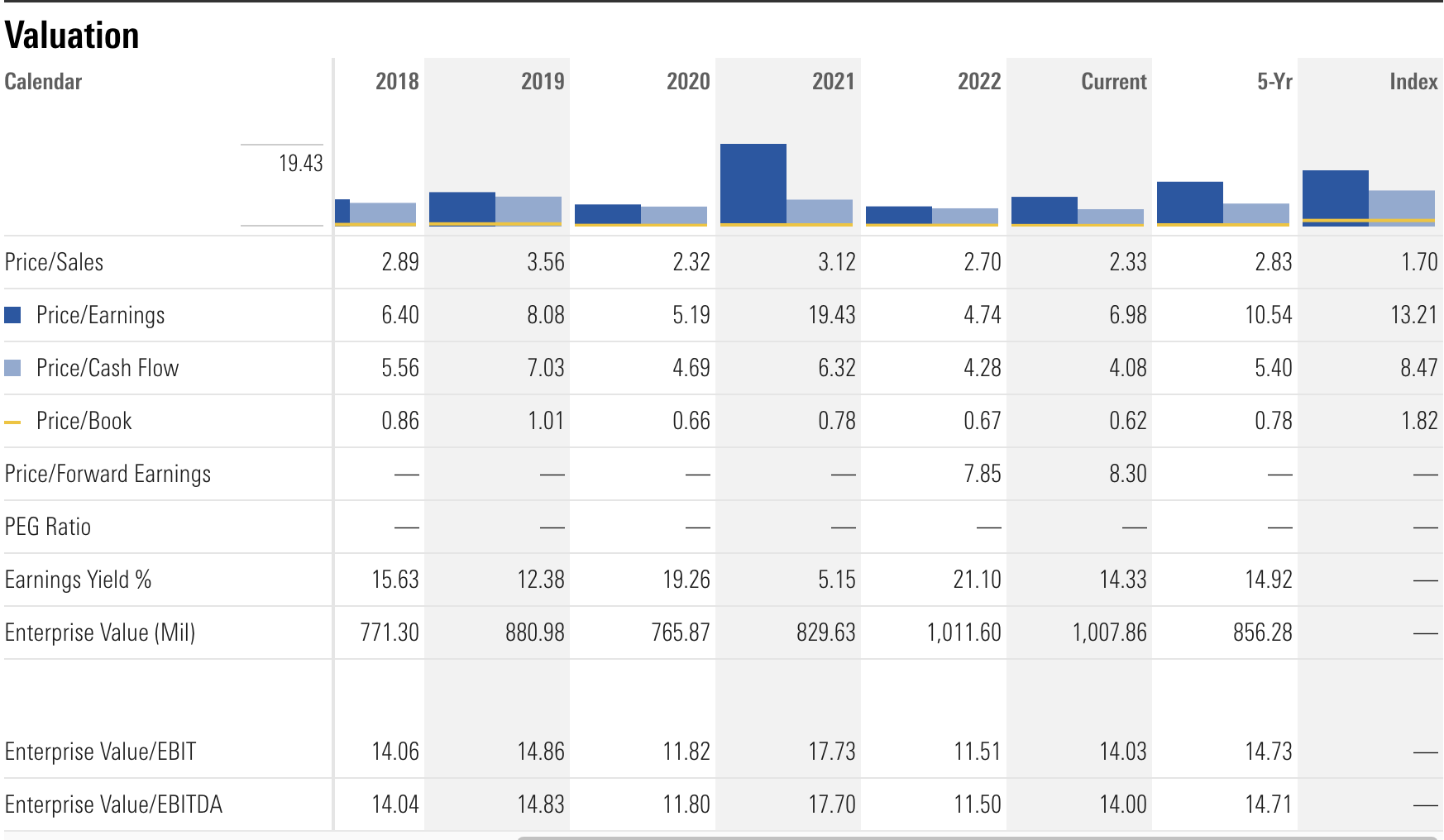

Given the safety of the dividend and the high yield, I feel that BTB has been unfairly valued. As evidenced by the current P/B multiple of 0.62. Over the past 5 years, the average has been 0.78 which would imply a price of $4.24 making the upside around 26.57%. In the meantime, you get paid to wait as you collect the sizeable yield:

P/B Multiple (Morningstar Canada)

{kind=link}

Portfolio Anchored by Excellent Tenants

One of the biggest oversights I feel the market is missing is in the quality of BTBs tenants. The Government of Canada and the Government of Québec are the largest tenants making up 10.1% of total revenue and 9.8% of total leasable space. Followed by other major companies including Walmart, WSP, and Desjardins the market shouldn't be concerned with rent collection or the worry that these companies won't renew their leases. In total, 28.7% of BTBs total revenue is provided by Government agencies and public companies.

One concern that could be brought up is the transition from office properties and increasing vacancy rates. BTB has a different set of office properties. Different from downtown offices, suburban offices are better suited for hybrid work models, commutes are shorter, and they provide greater flexibility of space to manage the reversal of office densification.

I believe that with immigration increasing at an unprecedented rate, construction slowing dramatically in the office space sector, and a growing shift of companies considering suburban offices closer to the homes of their employees there is the potential that these office properties actually outperform other sectors.

CBRE stated that rents in Class A suburban office buildings are up 7.8% since the first quarter of 2020. Combine this with the fact that office properties in suburban areas had a vacancy rate of 15.8% in Q4 2016 (the peak before COVID) compared to a rate of 17.1% in Q2 2023 (an increase of 2.3%) the rush to dump office properties seems overblown. BTB isn't missing out on this. In the most recent quarter, BTB reported an average renewal rate of 4.2% on 33,826 square feet. I feel confident that BTBs office property exposure is safer than the market is currently pricing:

Densification Opportunity

In the first quarter of 2022, BTB REIT entered into a conditional agreement to develop a residential component on one of its retail sites where about 900 residential units could be built with the potential to bring BTB around $30 million in proceeds. As BTB works towards completion, it would add around $0.35 per unit in value. Not only that, there are 6 other redevelopment opportunities within the portfolio.

Conclusion

Given the points that I have laid out, I believe that the market is unfairly pricing BTB at a discount due to their high proportion of office assets. Getting in now presents the perfect opportunity to capture a high dividend yield and the potential for future growth.

For further details see:

BTB REIT: Why The Market Is Wrong About This Value Play