BTO - BTO: Breaking Bad And The Easy Fed

2023-11-27 16:33:05 ET

Summary

- John Hancock Financial Opportunities Fund has treaded water since our last coverage.

- The large jump from the late October bottom negated the losses.

- We examine the macro and what it will take for the Fed to ease on the interest rate front.

In our last coverage of John Hancock Financial Opportunities Fund ( BTO ) we compared it to Direxion Daily Regional Banks Bull 3X Shares ETF ( DPST ) and decided that both funds were not deserving of an investment. For BTO, we went with:

BTO is better and investors are likely enamored by the dividend yield. It does better than DPST and this price it is hard to hate it. It gets a 5 on our potential pain scale. But we can generate far better covered call yields while reducing our volatility. That is the way we would go.

Source: Schrodinger's Regional Banks

To be fair to the bulls, the fund has held up since the last article and has been flat while doling out a nice distribution. To be fair to our work on this, we have warned about the risks of this since December 2021 and that longer term caution has also played out.

Seeking Alpha

We examine the setup today and see if the dividend can hold up in the face of the challenges ahead.

The Current Setup

Like funds and stocks of all stripes and shapes, BTO had a phenomenal rally off the late October lows. If you timed that with BTO or DPST, you did really well.

But that is the nature of the beast. Shorter term moves have little to do with longer term fundamentals. Pretty much everyone knows that you cannot expect 200% plus annualized returns from these (or any) investments. The recent rally had a lot to do with the Fed being on hold. More importantly, it also had a lot to do with rate cuts being priced in.

One place where rate-cut bets are showing up is in the bond market, where yields on longer-term bonds have retreated further below those on short-term ones. Treasury yields largely reflect expectations for what short-term rates set by the Fed will average over the life of a bond. As a result, such a move is typically viewed as a warning of a looming recession, with investors betting the Fed will need to slash rates to stimulate growth.

This month’s rally in stocks signals many investors anticipate a more benign outcome. Their hope: inflation falls back to the Fed’s 2% target, growth remains steady, but the Fed cuts rates a modest amount anyway as insurance against an unnecessary slowdown.

Source: Live Mint

This is important for all stocks as all valuation models lean somewhere or other on the risk-free rate. But it is most important for BTO and its regional bank investment theme. Banks of all shapes and sizes are facing increasing funding pressures as the risk-free rate has risen. So far, they have stayed behind the rising yields and only slowly raised rates that they have paid on checking, savings and CD accounts. But the "longer for higher" is slowly eroding that advantage. For banks that don't pay, the customers are exiting stage left, right into money market funds.

ICI

That alongside quantitative tightening, means that bank liquidity is set to contract in 2024. Rate cuts would be a big welcome relief, if it happened.

Our Outlook

This is officially the seventh time that Wall Street is celebrating the end of Fed rate hikes and the beginning of rate cuts. Sure, if you make a faulty prediction often enough, eventually you will be right. From our perspective, we see the weakness in the economy, that could warrant a slightly more dovish stance from the Fed, but this will at best mean no more hikes. For rate cuts to materialize, things would have to really break badly. What does breaking bad here mean? Well, we will show you what it does not mean first. It does not mean a situation where high yield spreads are hitting new lows.

Bloomberg

You are not going to get rate cuts in this environment. The financial conditions have actually eased so much (more negative means easier conditions in chart below), that the Fed may have to hike, even if it does not think it needs to.

Note the sharp drop since the middle of October. So rate cut pricing is just wrong here and the market is going to learn just how wrong in a matter of months. If they somehow materialize, you will tremor at the conditions that actually produce them. The last thing you would be doing is buying stocks because the rates were cut by a percent or two.

BTO's Leverage On Leverage

One thing investors must keep in mind is that the banking model is already extremely leveraged. We generally run debt to equity at 10X in the US system. That might be lower than what some of our European counterparts do, but it is still a levered system. BTO adds some more risk on to that.

CEF Connect

Sure, that 19.47% is low by CEF standards, but it is an added risk and one that can really negatively compound your returns on the way down. To be fair to the managers of BTO, so far this has not happened. Their skill of staying away from the dangerous banks showed in 2023 and BTO's NAV performance has been exceptional relative to KRE, despite BTO using leverage.

But it could happen with a more systemic meltdown and BTO shareholders could see a wide discount to NAV materialize, adding salt on their wounds.

Verdict

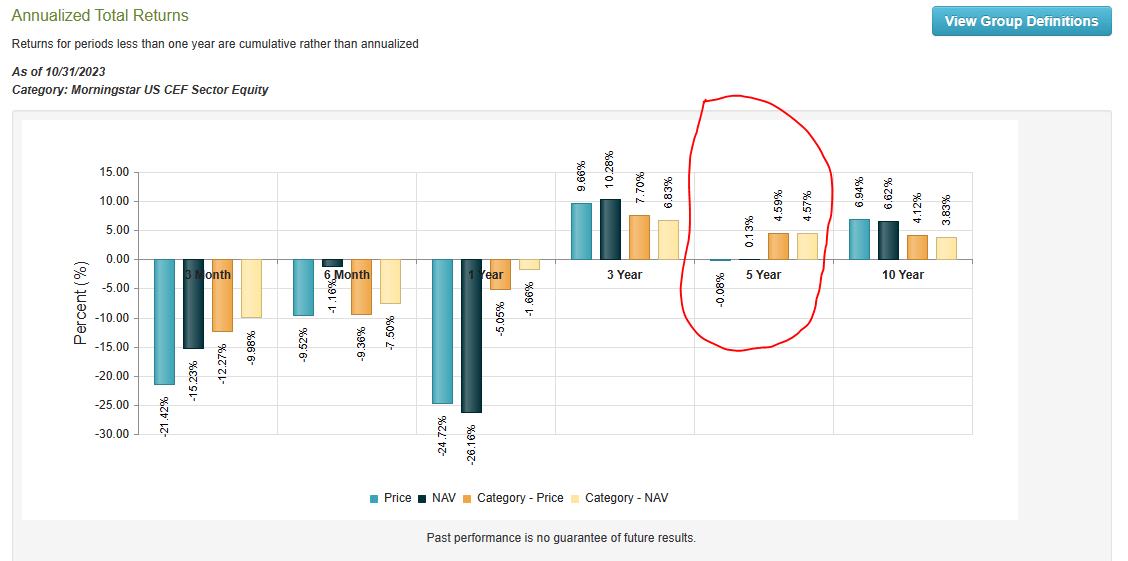

BTO's recent performance has been mediocre.

{kind=link}

That is to be expected as regional banks have struggled. BTO's distribution yield is largely a function of capital gains over time. What we mean by that is that the yield is far higher than the dividend yields of the underlying holdings. If it does not generate enough capital gains, the yield eats the NAV away. As you can see in the chart above, BTO has not matched its current distribution yield via total returns, in 1, 3, 5 or 10 year timeframes. This still does not automatically mean a cut, but the clock is beginning to tick on that. At present, we are leaning on the larger banks and gave our first buy rating to Bank of America ( BAC ) recently. We think this cycle is best navigated by eschewing leverage on leverage and BTO hence remains a "no-go" for us. If we see a real meltdown in regional banks, alongside a wide discount, we might pick up a position.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

BTO: Breaking Bad And The Easy Fed