BUI - BUI: After A 13% Pop The Bull Thesis Has Moderated (Rating Downgrade)

2023-04-01 04:11:44 ET

Summary

- BUI is a fund I have suggested (and owned) for many years. It is a more active play on the Utilities and power sectors with an above-average income stream.

- Going into 2023, I suggested the fund was ripe for a move higher. This turned out to be correct, to a larger degree than I expected.

- At current valuations, I think caution reigns here. The fund's discount to NAV has evaporated and valuations across the sector remain rich.

- Many view funds like BUI as bond proxies. With treasuries yielding more than the average utility stock, a broad rotation could be underway.

Main Thesis & Background

The purpose of this article is to evaluate the BlackRock Utility & Infrastructure Trust (BUI) as an investment option at its current market price. The fund is managed by BlackRock, and its objective is to "provide total return through a combination of current income, current gains and long-term capital appreciation". BUI seeks to achieve this objective by investing in equity securities issued by companies in the Utilities, Infrastructure, and Power business segments and by utilizing an option writing strategy.

I wrote about BUI four months ago when I saw a compelling buy thesis. In total transparency, I expected gains, but have been surprised just how well the fund has performed. I did not anticipate a 13% move in such a short time-frame, but it was a welcome development all the same!

Fund Performance (Seeking Alpha)

As you can see, this was a hefty return and vastly out-performed the S&P 500 during the same time period. This is good news for current holders.

Unfortunately, I can't get complacent here. Such a large, short-term gain raises a red flag for me and suggests buying in now may be a bit late to the game. I don't see a likely scenario where this type of out-performance continues in Q2 so I believe a downgrade to "hold" makes sense at these levels. I will explain the rationale behind this thesis below.

Valuation Has Risen Markedly

I will start the discussion on a key factor for my rating downgrade. This is the fund's valuation, which at first glance is a bit of a warning sign. At time of writing, BUI has a premium to NAV above 4%, as shown below:

{kind=link}

This is in no way an outright "sell" signal or a major cause for concern. Afterall, many CEFs, including BUI, can trade at higher premiums than this.

But readers need to recognize this is a fund also often trades at a discount to NAV. That is central to the "hold" thesis now. I wouldn't recommend buying this fund at any given time, but rather to be patient and wait for the right time. That was true in December, when the fund had a discount to NAV just under 6%. Clearly, buying then would have paid off, and the valuation was a central part in that.

The ultimate takeaway here is simple. BUI was cheap before and it isn't now. From this standard alone, one should be less bullish, and that is precisely the line of thinking I have at the moment.

The Sector Looks Expensive Relative To Bonds

The valuation story extends further beyond just BUI in isolation. The Utilities sector is often seen as a "bond proxy" because it tends to be favored by income-oriented investors, is less volatile, and yields more than treasuries. That is generally the case, and is why I have favored exposure to this sector since I began my investment career over fifteen years ago.

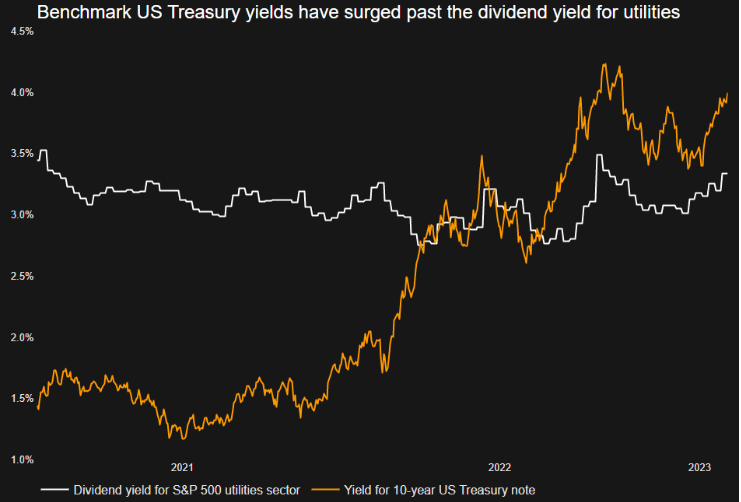

But, again, one has to constantly evaluate this sector in relative terms. If it is a bond proxy for some, then we should evaluate how the sector compares to bonds over time. For example, over the past few years when rates were low and treasury bonds offered little income, Utilities were a strong bet. Today, however, the story has changed. The Federal Reserve has been pushing rates up aggressively to the point where investors can get yields on treasuries that are almost triple what they were not long ago. As a result, the benchmark treasury yield has gotten larger than that of the broader Utilities sector:

Relative Yields (Treasuries vs. Utilities) (Reuters)

{kind=link}

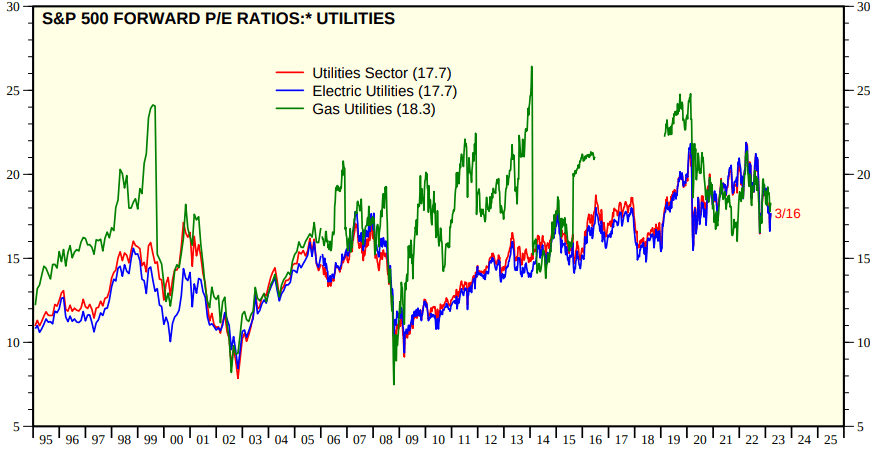

Similar to BUI's individual valuation, this speaks volumes about the Utility sector's valuation. Of course, this dynamic with treasuries is two-fold. The yields on bonds are rising because of the Fed. But the Utility sector has not kept pace in terms of current yield because investors have been bidding up share prices. This is "good" for current holders, but limits the go-forward opportunity. For support, consider that the sector is trading above its historical norm in terms of price-to-earnings ratio:

Sector Valuations (Forward P/E Ratios) (Refinitiv)

{kind=link}

This backdrop is important. We have to remember low interest rates allowed stocks in this sector to pay high dividends relative to bonds and that yield premium resulted in inflated valuations. This story started to unravel in 2022 and has continued into 2023. Of course, there are growth and quality factors to consider in the Utilities space that suggests valuations are not suddenly going to reverse sharply. Hence why I will continue to own exposure.

However, as inflation and rising interest rates have risen, the investment climate is not nearly as attractive. Furthermore, the marked rise in energy prices for American (and European) households could lead to increased scrutiny for utility providers. Regulators have allowed for consumer price increases to account for inflation and higher input costs, but a more consumer-friendly regulatory environment could be less agreeable to this going forward. Time will ultimately tell, but it proves a headwind worth mentioning.

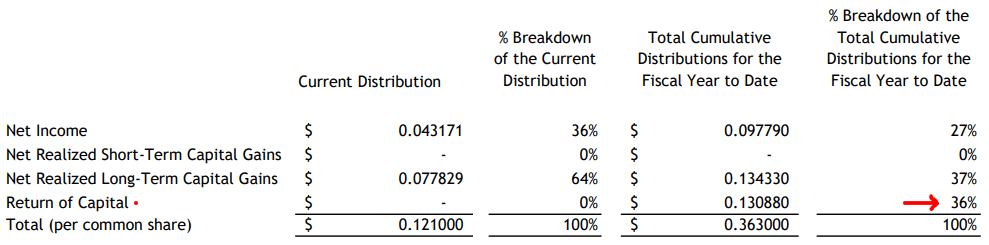

BUI's Yield Beats The Sector, ROC A Concern

Shifting back to BUI specifically, I continue to have concerns around the fund's distribution. This was an item I brought up in December, so I won't repeat myself too much here. But suffice to say I am worried about the sustainability of the current yield because of the heavy reliance of return of capital to pay it. This is often a signal to precedes a distribution cut among CEFs.

The good news is this metric has seen some improvement since my last article. So that is a step in the right direction. The problem still is that the improvement may not be enough. For example, in December the level of ROC that BUI was utilizing to pay its distribution was above 40%. That figure now sits at 36%, which is an improvement but is still much too high for my liking:

BUI's Income Metrics (BlackRock)

{kind=link}

What this is showing is BUI is not earning enough classified "income" to cover its stated distribution. This is something to keep a close eye on, as I have been, and I am indeed pleased with the progress made over the past quarter.

But simply put, that progress may not be enough. While BUI's structure of utilizing options rather than reverse repos (like many CEFs I follow) make this less concerning on the surface, the fact is that a long-term trend of using ROC to keep a distribution level constant is not a positive thing. I'm hopeful that the next few months bring about an even stronger figure here, but hope is not a strategy. I have to use this as support for my less bullish rating for now.

This Sector Is More Exciting Than Ever Before

My last topic is one I want to emphasize because I think readers need to understand my desire to own the Utilities sector (through both BUI and the Vanguard Utilities ETF ( VPU )) extends beyond just looking for dividends / income. The utility and power generation spaces are more interesting to me now than they were when I first started buying into them, and I am optimistic on the future growth potential of these areas.

The key here is that the electricity, power, and utility spaces are at the forefront of the world's transition away from fossil fuels. While I am still a big believe in fossil fuels in the short-term (and my Energy exposure can attest to that), the future is clearly going to be one of change. Developed nations in particular have governments that are willing and able to spend on upgrading, developing, and building new power sources and structures, and that money is likely to find its way directly into the arms of the underlying companies within the portfolios of BUI (and VPU).

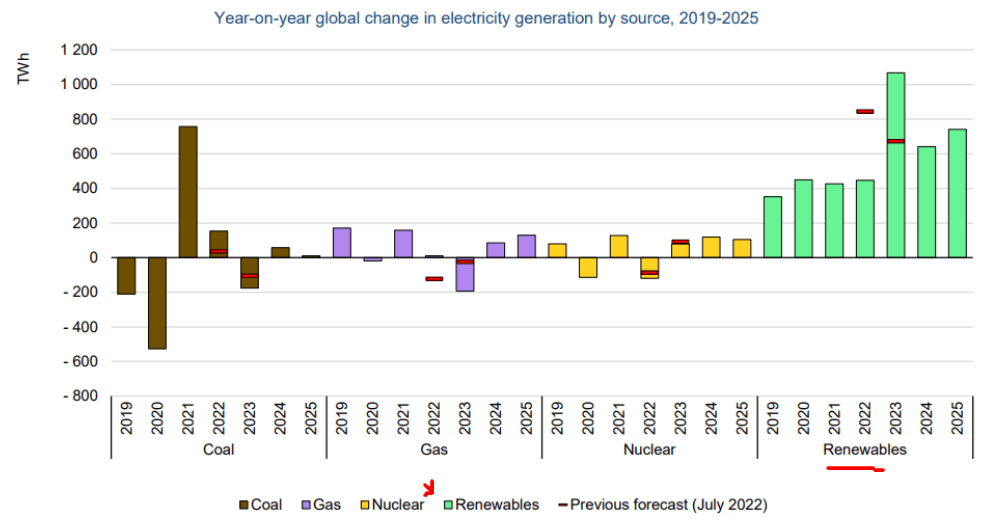

As my American readers are likely aware, spending on "renewables" has become a big component of economic recovery plans. A recent example was the "Inflation Reduction Act", which provided $370 billion in clean energy investments and credits - most of which will probably go to energy and utility companies. That is just one example, with others playing out across Western Europe and more likely to come in the U.S. as well. As a result, the forecast is that renewable energy is going to account for an ever growing share of electricity and power generation in the years to come:

Power Generation Mix (Worldwide) (World Economic Forum)

{kind=link}

I bring this up because I want to remind my followers how committed I am to this space long-term. Yes, this article puts forth a more cautious tone and I stand by that call for the time being. But that longer term trend is positive, so I will be retaining positions and looking to add to them because of this environmental and regulatory backdrop. But I will wait for the price to be right to do so.

Bottom-Line

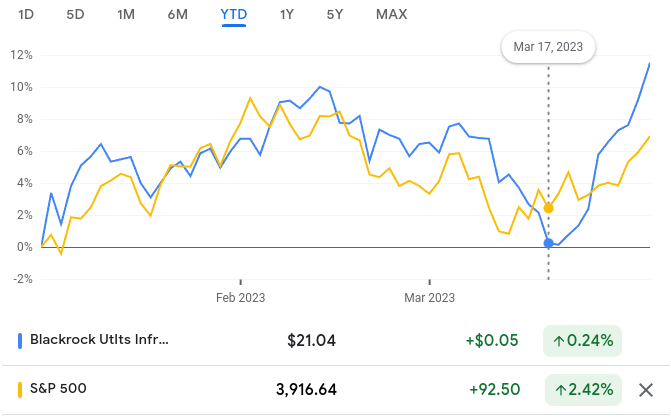

While the market as a whole has been rising in 2023, BUI in particular has been a big winner. This is especially true in just the past two weeks, as the graphs below will illustrate:

Returns Through 3/17 (Google Finance) YTD Returns (Google Finance)

{kind=link}

{kind=link}

This momentum is a welcome sign for investors in the fund, and there is merit to suggesting this bull run could continue. The fund's premium is in single digits, the income stream has been stable while many CEFs have cut over the past year, and the broader Utilities sector is ripe with opportunity.

However - I have concerns. Whenever I see a fund or stock move this much, this fast, I will pause and reflect. After doing so in this case I believe a downgrade to "hold" is the right call because BUI has seen its discount evaporate and the underlying sector is expensive relative to both treasury bonds and its longer term historic average. To me, the right move here is to remain patient and resist the temptation to chase returns. I anticipate a bit of a correction over the next few months, if not sooner, and suggest patient investors wait for such an opportunity to add or initiate to their positions.

For further details see:

BUI: After A 13% Pop, The Bull Thesis Has Moderated (Rating Downgrade)