IGF - BUI: Better Than Expected But Interest Rates Will Be A Drag On Performance

2023-10-05 17:29:16 ET

Summary

- BlackRock Utilities, Infrastructure & Power Opportunities Trust invests in overlooked utilities and infrastructure companies that generate strong and stable cash flows.

- The BUI closed-end fund has underperformed the market, with shares down 17.37%, but the share price performance does not reflect the income generated from dividends and distributions.

- The fund pays a current yield of 7.61% and provides a way to obtain a positive real yield without venturing into fixed-income investments.

- The fund did manage to fully cover its distribution during the first half of 2023, but the current struggles in the utility sector could pose challenges during the second half.

- The fund is currently trading at a discount to net asset value.

The BlackRock Utilities, Infrastructure & Power Opportunities Trust ( BUI ) is a closed-end fund, CEF, that invests in the utilities and infrastructure companies that are critical to modern life. Despite their importance, many people overlook these companies because they lack the "cool" factor of big technology firms or media companies and are not in their faces as shopping destinations like Walmart ( WMT ) or Target ( TGT ). However, nearly everybody in the developed world uses the services provided by utilities and infrastructure firms on a daily basis, usually before breakfast.

Fortunately, the fact that many of these companies are overlooked does not mean that they do not make money. In fact, one of the appeals of these companies is that they generate very strong and stable cash flows and pay the majority of their cash flows out to their investors in the form of dividends or distributions. This tends to result in them having high yields, and the BlackRock Utilities, Infrastructure & Power Opportunities Trust certainly exemplifies this with its own 7.61% current yield. That makes this fund one of the few ways to obtain a positive real yield today without venturing into the fixed-income space.

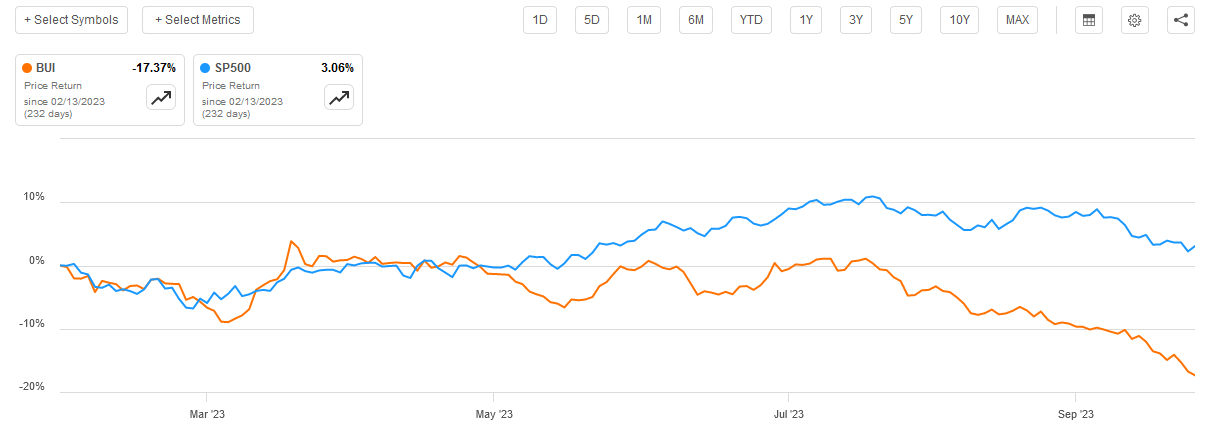

As regular readers may recall, we last discussed this fund back in February 2023. The fund has, unfortunately, not delivered a particularly good performance in the market. The fund's shares are down by 17.37%, which represents a significant underperformance against the S&P 500 Index ( SP500 ):

{kind=link}

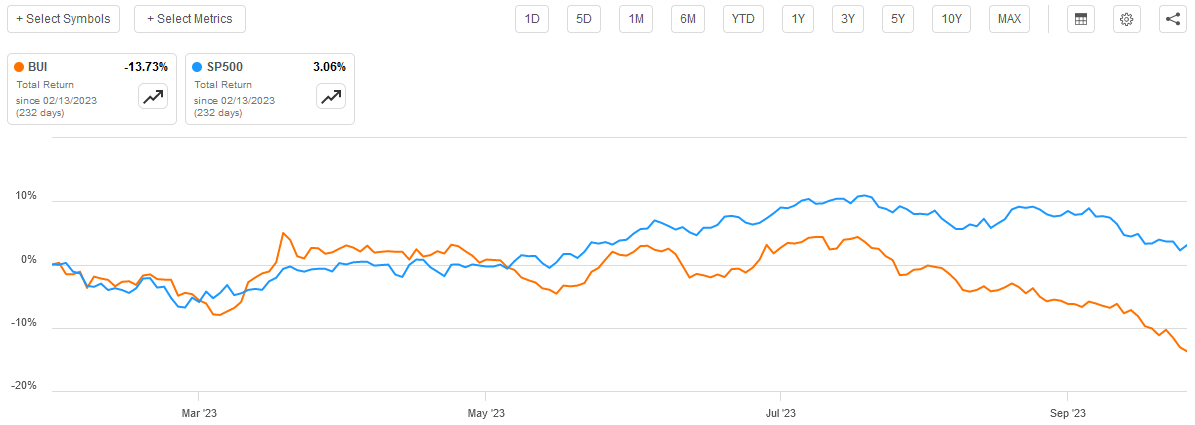

However, as I have pointed out numerous times in the past, the share price performance of closed-end funds does not really reflect how well the fund's investors have done since a substantial portion of the investment returns provided by these assets are in the form of direct payments to the shareholders. These payments are sometimes sufficient to offset the declines in the fund's share price. That was not the case here, as investors who purchased the fund on the day that my previous article was published still lost 13.73% of their investment, so they made out much worse than an investor who purchased the S&P 500 Index at the same time:

{kind=link}

This is quite disappointing, but we can see that most of the losses came in the past two months as the market finally started to wake up to the reality that high interest rates will likely be with us for a considerable amount of time. This is just one of the many things that has changed in the overall market environment since mid-February so let us revisit this fund and see how our thesis holds up today.

About The Fund

According to the fund's website , the BlackRock Utilities, Infrastructure & Power Opportunities Trust has a primary objective of providing its investors with a high level of total return. As is usually the case, the fund's website goes into much greater detail:

BlackRock Utilities, Infrastructure & Power Opportunities Trust's investment objective is to provide total return through a combination of current income, current gains, and long-term capital appreciation. The Trust seeks to achieve its investment objective by investing primarily in equity securities issued by companies that are engaged in the Utilities, Infrastructure, and Power Opportunities business segments anywhere in the world and by utilizing an option writing (selling) strategy in an effort to enhance current gains. The Trust considers the 'Utilities' business segment to include products, technologies, and services connected to the management, ownership, operation, construction, development or financing of facilities used to generate, transmit, or distribute electricity, water, natural resources or telecommunications and the 'Infrastructure' business segment to include companies that own or operate infrastructure assets or that are involved in the development, construction, distribution or financing of infrastructure assets. The Trust considers the 'Power Opportunities' business segment to include companies with a significant involvement in, supporting, or necessary to renewable energy technology and development, alternative fuels, energy efficiency, automotive and sustainable mobility, and technologies that enable or support the growth and adoption of new power and energy sources. Such companies may include, among others, electrical equipment producers (such as wind turbine manufacturers), producers of industrial or specialty chemicals (such as building insulation producers), and semiconductor and equipment companies (such as solar panel manufacturers). Under normal market conditions, the Trust invests a substantial amount of its total assets in foreign issuers, issuers that primarily trade in a market outside the United States or issuers that do a substantial amount of business outside the United States. The Trust may invest directly in such securities or synthetically through derivatives.

As the above statement from the webpage suggests, the fund invests primarily in common equity securities. In fact, as of the time of writing, 97.64% of the fund's assets are invested in common stock along with a relatively small allocation to cash:

CEF Connect

As such, the emphasis on total return makes sense. After all, common equities are by their very nature total return vehicles since investors purchase them primarily to earn income through the receipt of dividends or distributions as well as benefit from capital gains as the issuing company grows and prospers.

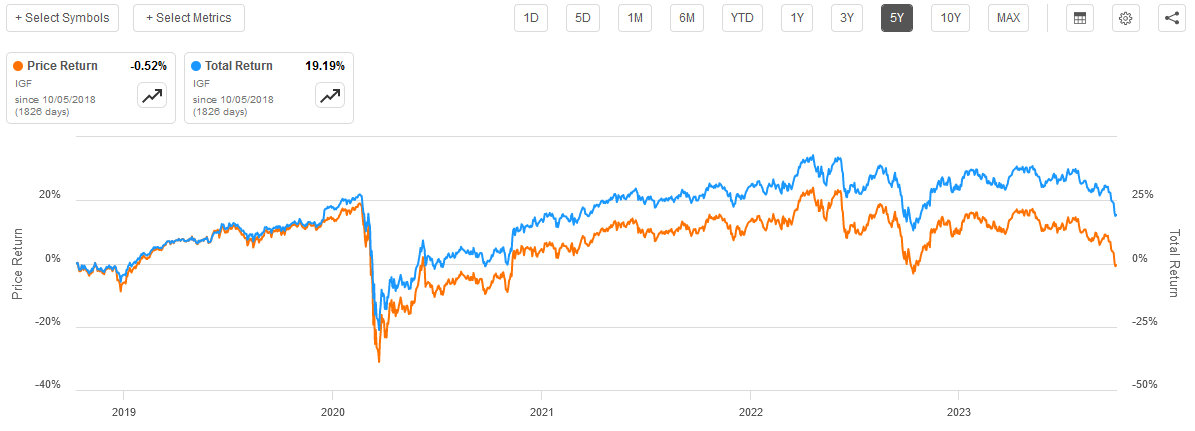

In the case of many infrastructure companies though, the company primarily delivers its total returns via direct payments to the investors. We can actually see this by looking at the iShares Global Infrastructure ETF ( IGF ), which tracks an index of infrastructure companies all over the world. Over the past five years, the exchange-traded fund's share price has actually gone down by 0.52%, but investors in the fund actually made 19.19% over the period once the distributions and dividends are included:

{kind=link}

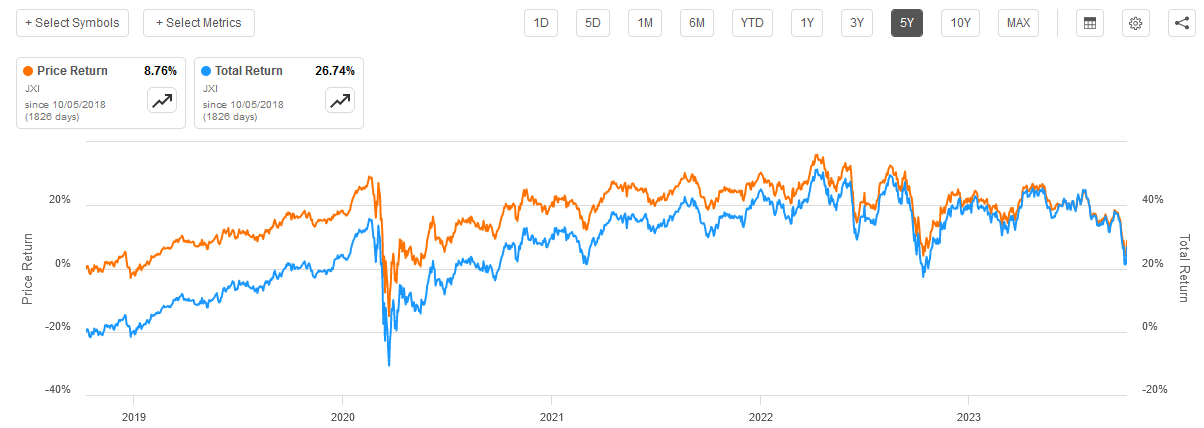

This shows us that dividends and distributions play a significant role in the investment performance of most infrastructure companies. The same is true of utilities, although not to the same degree. As I have pointed out in various articles on utility companies, they usually target earnings per share growth of 5% to 7% annually along with a 3% to 4% dividend yield for a total return in the 9% to 11% annual range. However, internationally the dividend does play a substantial role in their total return. As we can see here, the iShares Global Utilities ETF ( JXI ) saw its price appreciate by 8.76% over the past five years but it still managed to deliver a 26.74% total return over the period:

{kind=link}

The reason that this is important is that it shows us that the BlackRock Utilities, Infrastructure & Power Opportunities Trust will be generating a significant portion of its total return through dividends and distributions paid by the stocks in its portfolio. The share price appreciation of the assets in the portfolio will probably still play a meaningful role, but not nearly to the same extent as we would see in most broad-based common stock funds.

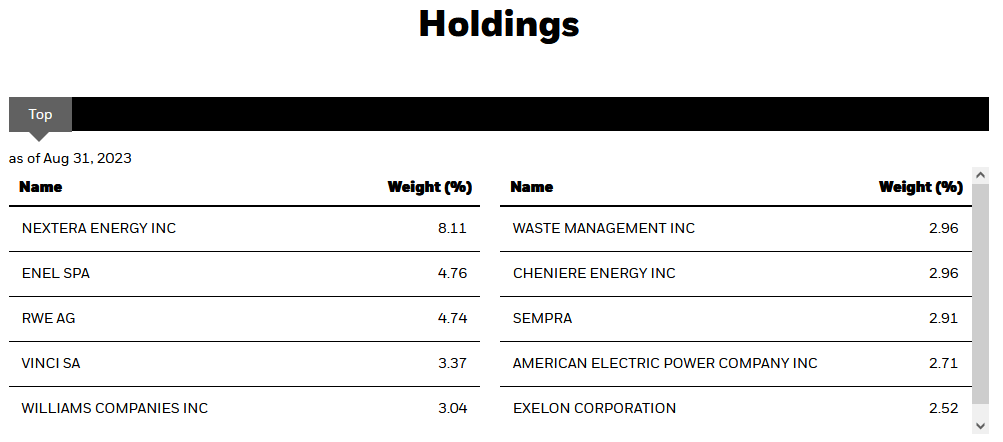

As regular readers are no doubt well aware, I have devoted a considerable amount of time and effort to discussing various utilities and energy infrastructure companies in my investing group and on Seeking Alpha over the past several years. As such, the largest positions in the fund's portfolio are likely to be familiar to most regular readers. Here they are:

{kind=link}

I have never discussed Enel ( ENLAY ), RWE ( RWEOY ), Vinci ( VCISF ), or Waste Management ( WM ) before, but their business models are quite similar to the other utilities that we see among the fund's largest positions. The sole exception to this would be Waste Management but considering that company's presence throughout a good portion of the United States, many American readers are likely going to be at least somewhat familiar with the products and services that it provides.

It is surprising that there are so few companies on this list that are not utilities. As the fund itself states, it invests in companies that are active in the utility, infrastructure, or renewable energy business. The only companies on the above list that are not utilities are The Williams Companies ( WMB ), Waste Management, and Cheniere Energy ( LNG ). However, The Williams Companies may as well be a utility because it transports natural gas to electric and natural gas utilities all along the East Coast, acting very much as a utility for utilities. It also enjoys the general stability in terms of cash flows that we typically expect from utilities.

In fact, this is a hallmark of every company on this list, and of the utility sector in general. After all, for the most part, utilities provide a product that is generally considered to be a necessity for modern life, so most people usually prioritize paying their utility bills ahead of any discretionary expenses. This allows these companies to enjoy considerable resilience in the face of recessions or other macro-economic problems, which is exactly the kind of thing that investors should be able to appreciate right now considering the sheer volume of disappointing economic statistics that are coming out right now.

In fact, it was recently revealed that 84% of corporate Chief Executive Officers expect that the U.S. economy will enter a recession next year, a sentiment that 69% of American consumers also share. When we consider how dependent the American economy is on the willingness and ability of consumers to spend, this may become a self-fulfilling prophecy as consumers determine their spending habits based on their views of economic conditions.

This could explain why recent credit card data suggests that consumer spending has been declining for five straight months. As American consumers prepare themselves for a recession, they may end up causing one. As such, a good argument could be made for investors to put their assets into things that will prove resilient in the face of such a recession. The companies in which this fund is invested would be a good example of that.

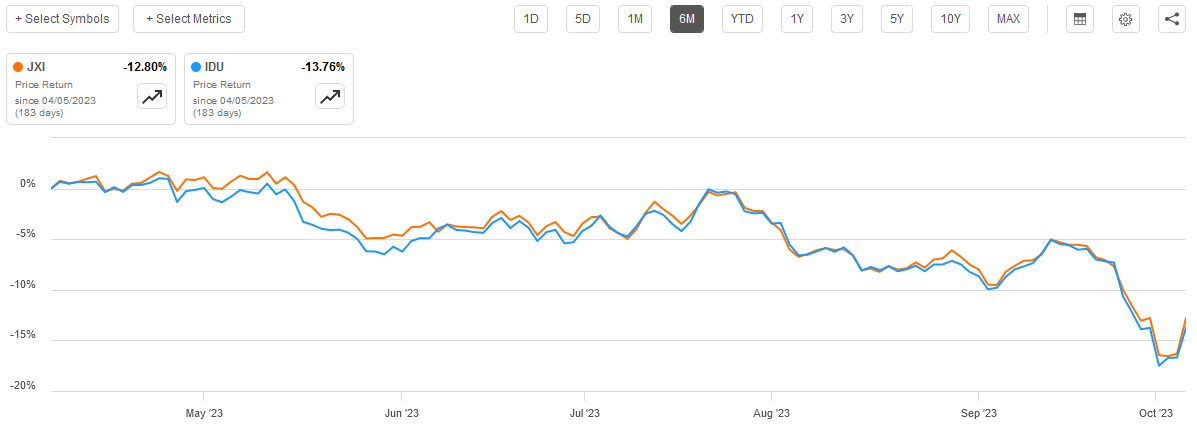

Unfortunately, utilities have been underperforming by quite a lot over the past few months. As we can see here, the U.S. utilities index ( IDU ) is down 13.76% and the global utilities index is down 12.80% over the past six months:

{kind=link}

One of the biggest reasons for this is that utilities are sometimes thought of as "bond substitutes" by investors. These companies tend to be incredibly stable and have higher yields than many other sectors in the market. Thus, they are bought for yield more than for growth considering that most of them only grow their earnings per share at single-digit percentage rates. As everyone reading this is no doubt well aware, bond yields have been rising significantly since mid-July or so as it become increasingly apparent that the Federal Reserve's fight against inflation has not come anywhere close to an end and the central bank would almost certainly be forced to keep yields "higher for longer."

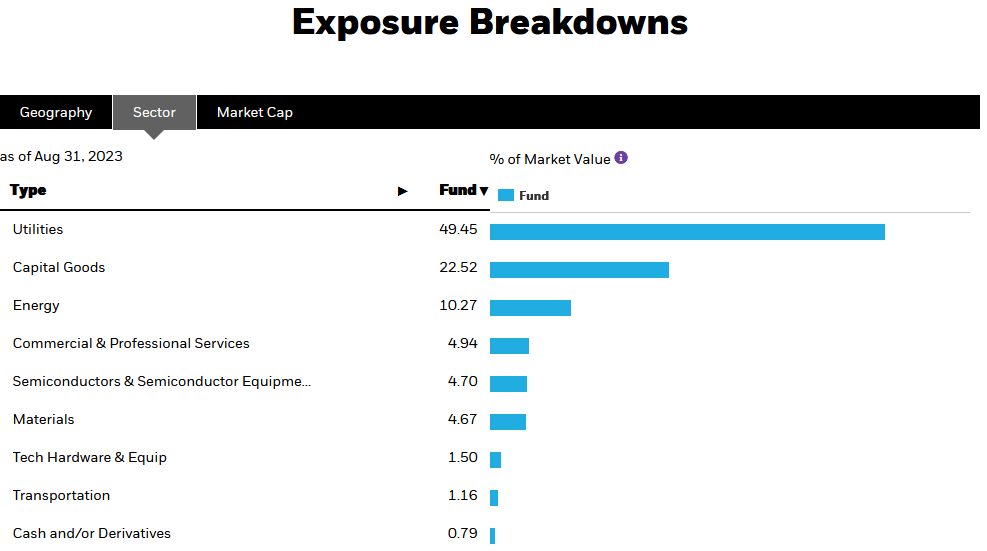

Infrastructure companies, especially energy infrastructure companies, have generally held up much better both because of strength in energy prices and the fact that their yields are substantially higher than those of utilities. Unfortunately, this fund's portfolio is mostly weighted towards utilities, with the sector accounting for fully 49.45% of the fund's total assets:

{kind=link}

It is this exposure to the utility sector that has been primarily responsible for the fund's poor performance over the past several months. Unfortunately, though, it probably will not improve until interest rates begin to decline, and it is uncertain when that will occur. Fortunately, the fund's yield is decent so at least investors should be able to get a certain amount of income from it while waiting for the assets held by the fund to recover. Of course, this happy scenario assumes that the fund's distribution is sustainable, which we will attempt to determine later in this article.

Distribution Analysis

As just mentioned, many investors buy utilities and other infrastructure companies primarily for the dividends that they pay out. Admittedly though, utilities are not really as good at this as would be thought because the U.S. utilities index yields 3.09% and even the global utilities index only yields 3.85%. While both of these yields are better than the S&P 500 Index, they are worse than ten-year U.S. Treasury bonds (US10Y) right now, let alone the 7%+ that can be easily obtained from most energy infrastructure companies.

Nonetheless, utilities are frequently bought for their yields. The BlackRock Utilities, Infrastructure & Power Opportunities Trust invests in a portfolio of utilities and other infrastructure companies and collects their distributions and dividends. It then pays these out to its investors along with any capital gains that it manages to realize, net of the fund's own expenses. The presence of the realized capital gains in the pool of incoming money that can be distributed allows the fund to boost its yield somewhat relative to what it would be able to accomplish with just dividends. As such, we might assume that the fund has a fairly high yield today.

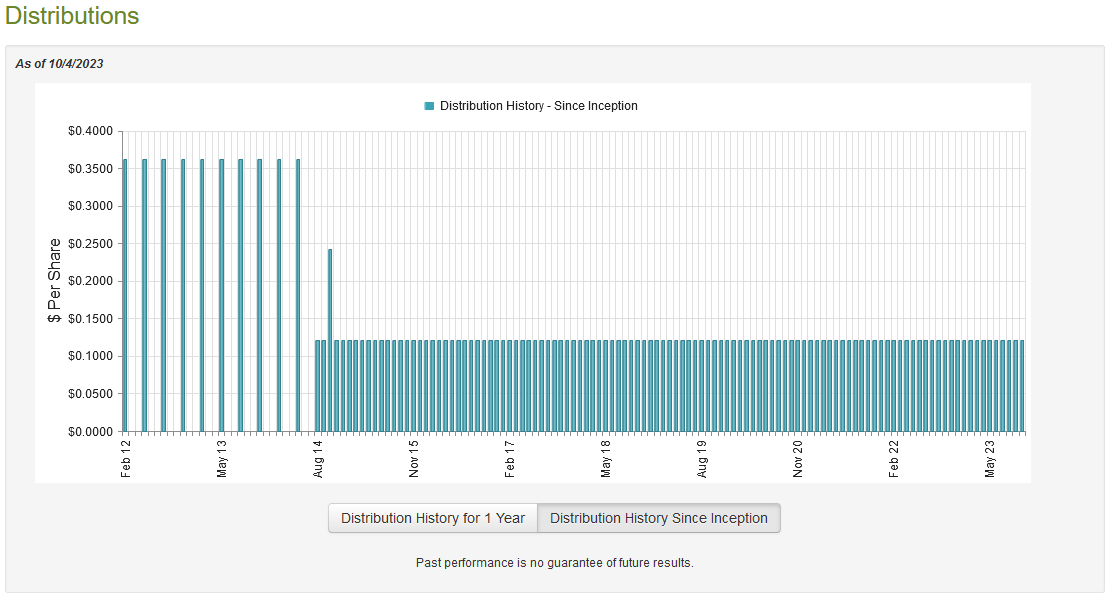

This is certainly the case, as the BlackRock Utilities, Infrastructure & Power Opportunities Trust pays a monthly distribution of $0.1210 per share ($1.452 per share annually), which gives it a 7.61% yield at the current price. The fund has been remarkably consistent with respect to its distribution over the years, as it has never cut it:

{kind=link}

There may be some investors who notice that the distribution fell back in 2014, but this was not a cut. The fund changed from a quarterly distribution of $0.3625 per share to a monthly distribution of $0.1210 per share ($0.3630 per share quarterly) so it actually increased its distribution by $0.0005 per quarter. The monthly distribution is better anyway since it allows for more frequent compounding and better aligns itself with the fact that most investors' bills are due monthly. Overall, this very strong track record is likely to appeal to any investor who is seeking a steady source of monthly income to use to pay their bills. It also speaks well to the relative financial stability of most of the companies in which this fund invests.

However, as is always the case, we want to investigate the fund's finances in order to determine how well it can actually sustain its distribution. After all, we do not want to be the victims of a distribution cut that reduces our incomes and probably causes the fund's share price to decline more than it already has.

Fortunately, we have a relatively recent document that we can use for the purpose of our analysis. As of the time of writing, the fund's most recent financial report corresponds to the six-month period that ended on June 30, 2023. This is a much newer report than the one that we had available to us the last time that we discussed the fund, which is quite nice. After all, the first half of this year presented a very optimistic market in which we experienced something of an artificial intelligence bubble. The prices of many things went up, providing the fund with the potential to realize some capital gains. This report should give us a good idea of how well it managed to take advantage of the conditions.

During the six-month period, the BlackRock Utilities, Infrastructure & Power Opportunities Trust received $8,260,404 in dividends and $6,756 in interest from the investments in its portfolio. When we subtract out the amount that the fund paid in foreign withholding taxes, we get a total investment income of $7,806,087 during the period. The fund paid its expenses out of this amount, which left it with $5,083,322 available for shareholders. As might be expected, this was nowhere close to enough to cover the amount that the fund paid out in distributions, which was $16,221,897 during the period. At first glance, this could be quite concerning as the fund was not able to completely finance its distributions out of net investment income.

With that said, there are other methods that the fund can use to obtain the money that it needs to cover the distribution. For example, it might be able to realize capital gains that can then be paid out to the shareholders. Capital gains are not considered investment income, but they still obviously represent money coming into the fund. Fortunately, this fund enjoyed significant success at this task during the period.

The BlackRock Utilities, Infrastructure & Power Opportunities Fund reported net realized gains of $15,406,383 alongside $8,875,104 net unrealized gains. Overall, the fund managed to increase its net assets by $16,604,320 after accounting for all inflows and outflows during the six-month period. Thus, this fund clearly did manage to cover its distribution and had a substantial amount of money left over.

In fact, depending on how much of these unrealized gains the fund managed to convert into realized gains prior to the recent utility sector weakness, it has enough to cover its distribution for the entire year. Overall, the fund probably will not have too much trouble paying the distribution for another six months or so, but we should certainly keep an eye on its finances to ensure that it remains in good shape.

Valuation

As of October 4, 2023 (the most recent date for which data is currently available), the BlackRock Utilities, Infrastructure & Power Opportunities Trust has a net asset value of $19.62 per share but the shares currently trade for $19.10 each. This gives the fund's shares a 2.65% discount on net asset value at the current price. That is slightly worse than the 2.94% discount that the shares had on average over the past month, but it is still a very reasonable price to pay for the fund. Overall, today's price is quite acceptable if you want the funds.

Conclusion

In conclusion, the BlackRock Utilities, Infrastructure & Power Opportunities Trust provides an easy way to obtain exposure to utilities and infrastructure companies from all around the world. Many of these companies enjoy very stable cash flows regardless of economic conditions, so they could be a good place to hide out from any recession that may be on the horizon.

Unfortunately, the rising interest rate environment may continue to pressure shares of utility companies, and by extension BlackRock Utilities, Infrastructure & Power Opportunities Trust. That is a sharp negative since it may mean suffering declining prices of your shares, although the distribution will offset this somewhat. Overall, the fund may be worth considering, but there is a risk right now considering that the market turned against many of the fund's holdings since the time that the most recent financial report was released.

For further details see:

BUI: Better Than Expected, But Interest Rates Will Be A Drag On Performance