BUI - BUI: Reasonable Buy At This Level (Rating Upgrade)

2023-07-25 13:16:00 ET

Summary

- The BlackRock Utility & Infrastructure Trust (BUI) is evaluated as an investment option, with the fund's objective being to provide total return through income, gains and long-term capital appreciation.

- Despite a 2% drop in total return, BUI has moved into discount territory, which is generally a good buying opportunity for investors interested in total return.

- The fund's performance is diverging from the broader market, with the Utilities sector being the second-worst performer year-to-date, which could be a buy case for contrarian thinkers.

Main Thesis & Background

The purpose of this article is to evaluate the BlackRock Utility & Infrastructure Trust ( BUI ) as an investment option at its current market price. The fund is managed by BlackRock, and its objective is to "provide total return through a combination of current income, current gains, and long-term capital appreciation". BUI seeks to achieve this objective by investing in equity securities issued by companies in the Utilities, Infrastructure, and Power business segments and by utilizing an option writing strategy.

I wrote about BUI almost four months ago when I saw a chance to take some profit and moderate my outlook. Looking back that was a timely call. The broader market has continued to rally while BUI has taken a bit of a loss:

Fund Performance (Seeking Alpha)

In total transparency, I expected gains, but have been surprised just how well the fund has performed. I did not anticipate a 13% move in such a short time frame, but it was a welcome development all the same!

Value Has Returned

A key point to me when I review this fund is the premium or discount to NAV. This is critical because over time I have found BUI is a decent trading vehicle. There are often very clear buy and sell signals to me that have worked over time. While some funds tend to trade at premiums (and often large premiums) for extended periods, that often is not the case with BUI. And the flip side is also true. Discounts don't always last for long, so they generally signal reasonable buy-in points.

This is relevant now because BUI's valuation has shifted markedly since my last review. The premium was in excess of 4%, which I found too pricey. Today, despite only a 2% drop in total return, BUI has moved in to discount territory:

{kind=link}

This is a fairly straightforward metric, so there isn't much else to say about it. The discount to NAV is attractive and generally represents a good buying opportunity for investors interested in total return. That has been the case over time and I believe it will turn out to be true at this moment too.

Utilities Diverging From Broader Market

My next point is a buy case but for more of a contrarian thinker. What I mean is, this may not register as a positive for everyone even though it does for me. What I am referring to is the gap between how the broader equity market has been performing and the underlying Utilities sector. Through 2023, "stocks" are up by leaps and bounds - but this is not all inclusive. Tech, and namely the largest Tech names, had led the way while other sectors have struggled.

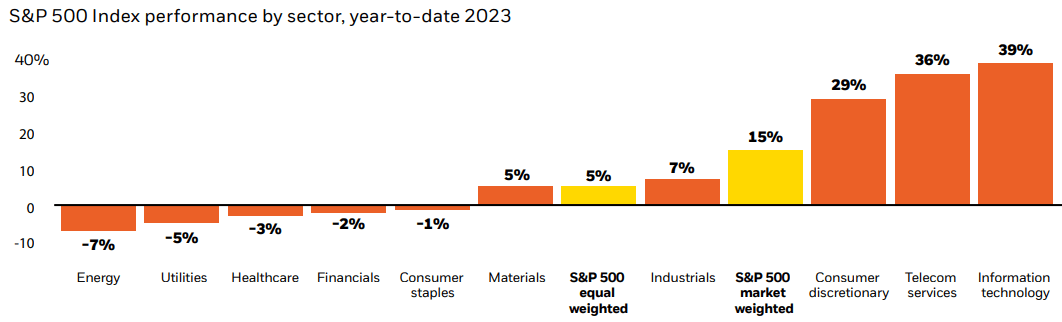

Case in point is Utilities. It is actually the second-worst performer year-to-date, which is not entirely comforting:

YTD Returns (By Sector) (Bloomberg)

{kind=link}

This is where I bring perspective in to it. Personally, I see value here. The market has been getting a bit carried away (in my opinion) and could be due for a correction. If so, I expect the high-flying sectors to get punished disproportionately. By contrast, areas that investors have shunned - such as Utilities - could get a bit of a boost from a sector rotation. We saw that play out in 2022 and then a reversal of the trend in 2023. Case in point is both Energy and Utilities. The laggards this year were the winners last year. It is very easy to surmise a similar rotation could occur again as we push deeper into the year.

Of course, this contrarian viewpoint is not universally shared. A momentum or swing trader may not see the value. They see losing sectors as places to avoid, not buy. And in fairness that would have worked out in 2023. For those "chasing" Tech returns, they continue to be rewarded. I am of the opinion that all good things won't last. Tech's out-performance has to even out at some point and I expect Utilities will be there waiting to pick up the slack when it does. The good news is BUI is a great way to play this idea.

Dropping Inflation A Tailwind For This Sector

The next topic is what I see as a clear-cut benefit for Utilities, and BUI by extension. This is especially true for this fund given its "infrastructure" and "power" objectives as opposed to a straight-line Utility sector SPDR. The point I am referring to is declining inflation. This is disproportionately positive for the Utilities sector because it is often seen as a bond proxy. As yields/Fed rates drop, that makes the yield from utility companies more attractive. In fact, this sector has a pronounced inverse relationship with Fed rates compared to other sectors. In this regard, recent CPI declines here at home are especially comforting:

Inflation Metrics (US) (S&P Global)

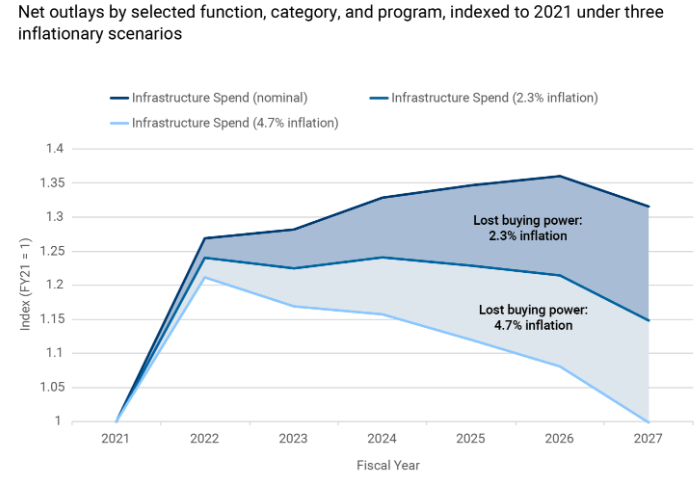

In normal cycles this is a general positive for utilities, and it is certainly the case here as well. But in this environment there is a second reason this makes me bullish. This has to do with the recent government spending that was passed - much of which is going to "infrastructure" and other "clean" energy projects that will flow directly into the underlying companies in BUI's portfolio.

This was always "good" news - and a general boon for the sector. But rapid inflation limited the positive impact. This is because legislation was passed with fixed amounts. As inflation eats away at that buying power, so too does the benefit to the projects and companies those funds were designated for. With inflation moderating, the value of those dollars will be higher than they otherwise would have been (if inflation continued at its same pace, or higher):

Inflation's Impact on Government Expenditures (estimated) (Brookings)

{kind=link}

This is a big deal because a stronger dollar means higher "real" profits for the companies that are receiving these funds or delivering these projects.

Of course, the government could always write new legislation and spend more to make up for the inflationary impact of the prior legislation. But how realistic would that be in this climate? With a split Congress and a presidential election next year, the chances of both parties working together to pass a meaningful bill in this regard is pretty small. So I view the inflation tailwind as ultra-important given this reality.

BUI's Use Of Options Writing Preferable To Leveraged Borrowing

A final point to emphasize is BUI's call-write strategy that allows the fund to collect premiums from expired options. This options strategy is a much safer way to amplify returns than the borrowing that is common among other CEFs. Those funds have been hammered by an inverted yield curve - driven by rising short-term borrowing costs and fewer opportunities for yield "pick-up" at longer maturity dates. While that strategy can pay off big in periods of low rates and quantitative easing, it can be painful in other climates like the one we have been in during the past 18 months.

Of course, BUI's strategy limits upside since the options go into the money when stock prices rise above the strike price. This means that BUI's upside is capped as the buyers of those options exercise them. But I am willing to take this type of risk rather than the excess losses that leveraged borrowing in other forms can contribute to.

I highlight this attribute because my followers know I have been very cautious on leverage over the past year. I have moved out of bullish ratings from many CEFs that I used to favor. So I don't want to sound contradictory by recommending BUI - but I am doing so because it is a CEF with a different type of strategy and one that I view positively at the moment.

Bottom Line

Utilities are more exciting than they used to be. This is especially true for funds like BUI that are not just traditional utility plays - it owns foreign companies and other interesting companies like Waste Management ( WM ), one of my personal favorites.

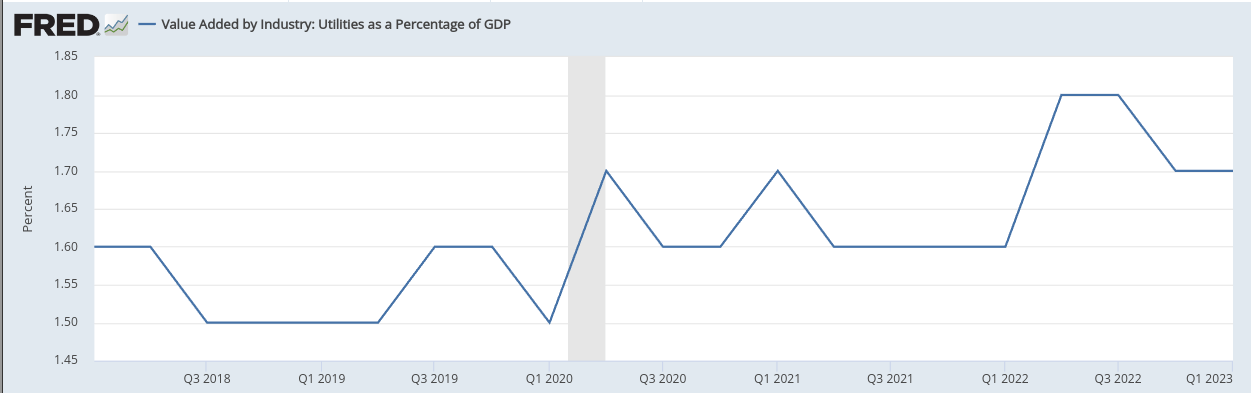

Looking ahead, the Utilities sector will continue to benefit from government plans to alter the energy and utility grids around the country. This is also a theme being played out in Europe to which BUI has exposure. Further, this is an arena that continues to grow in importance to the American economy:

Utilities Sector As A Percentage of GDP (St. Louis Fed)

{kind=link}

My takeaway from all this is that I like this sector's exposure and I like playing it through BUI when the right opportunity presents itself. I believe it is indeed presenting itself now and there are justifiable reasons for upgrading my outlook on this fund to "buy" at this time.

For further details see:

BUI: Reasonable Buy At This Level (Rating Upgrade)