BBW - Build-A-Bear Workshop: 2 Reasons Why We Are Turning More Optimistic In 2023

Summary

- Build-A-Bear's efficiency and profitability improving in 2022 despite the challenging macroeconomic environment.

- The improving consumer sentiment, along with decreasing energy and raw material prices, may generate tailwinds for the firm.

- Despite the substantial increase in the share price, the valuation still appears reasonable.

- For these reasons, we upgrade our rating to "buy".

Build-A-Bear Workshop, Inc. (BBW) operates as a multi-channel retailer of plush animals and related products. The company operates through three segments: Direct-to-Consumer, Commercial, and International Franchising.

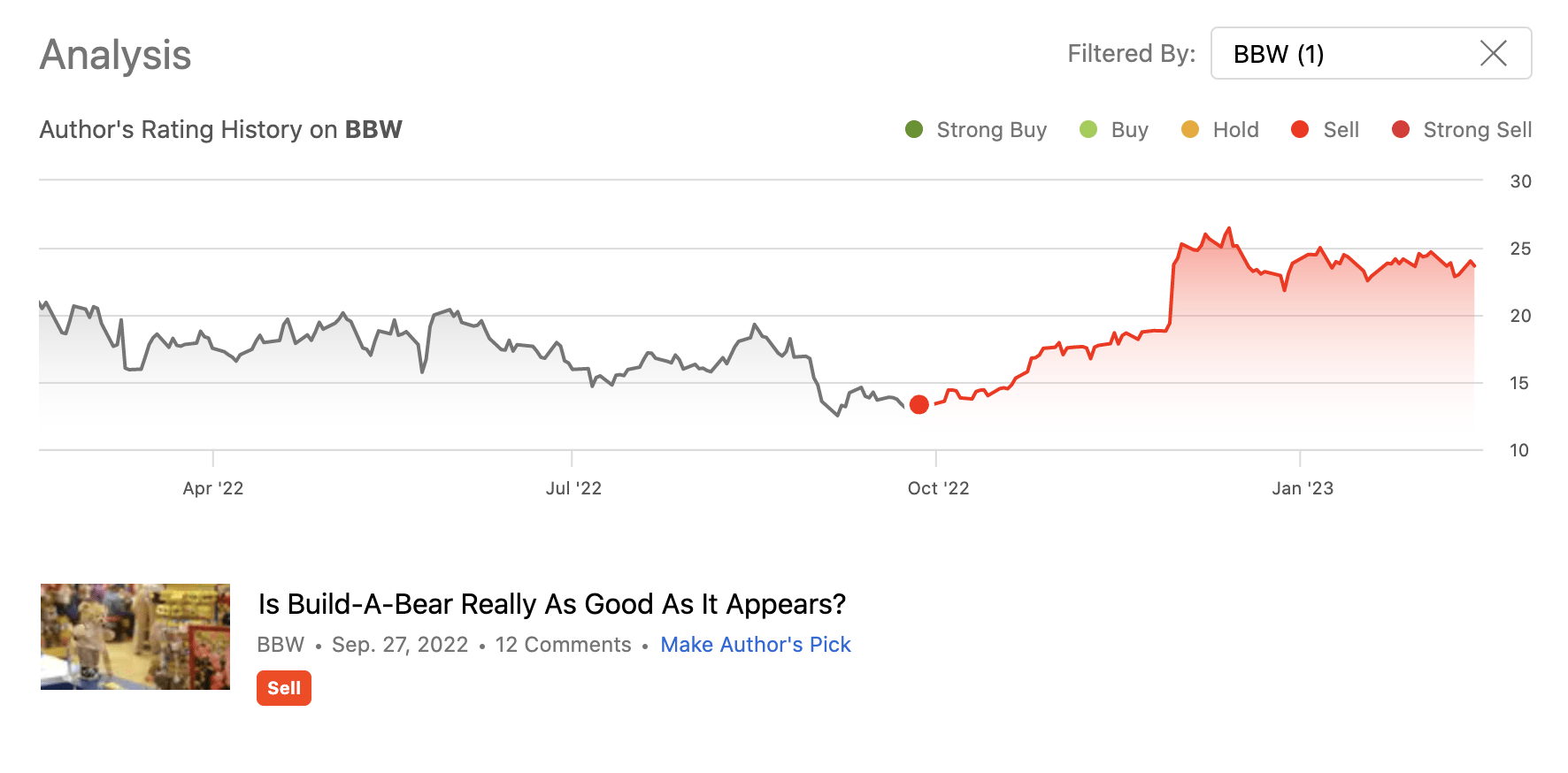

We have written an article about BBW in September, 2022 on Seeking Alpha, rating the stock as a "sell" back then, despite the strong quarterly earnings report in the prior period. Since then, the stock price has increased by as much as 80%.

{kind=link}

Today, we are taking a look at BBW's stock once again, as we believe that our outlook has turned out to be overly pessimistic in 2022. We will be analysing the company from a profitability and efficiency point of view, and comment on how potential changes in the macroeconomic environment may impact these factors.

Net profit margin

Net profit margin is a well-known and widely used profitability measure. It is the ratio between the net profit and revenue. It essentially indicates, how much profit the firm has left after accounting for all its costs.

The following chart shows the company's net profit margin over the past five years.

Despite the sharp drop in 2020 at the beginning of the pandemic, the firm's net profit margin has improved significantly over the past years. We believe, it is particularly appealing that BBW managed to maintain its margin at a relatively stable level, considering the challenging macroeconomic environment.

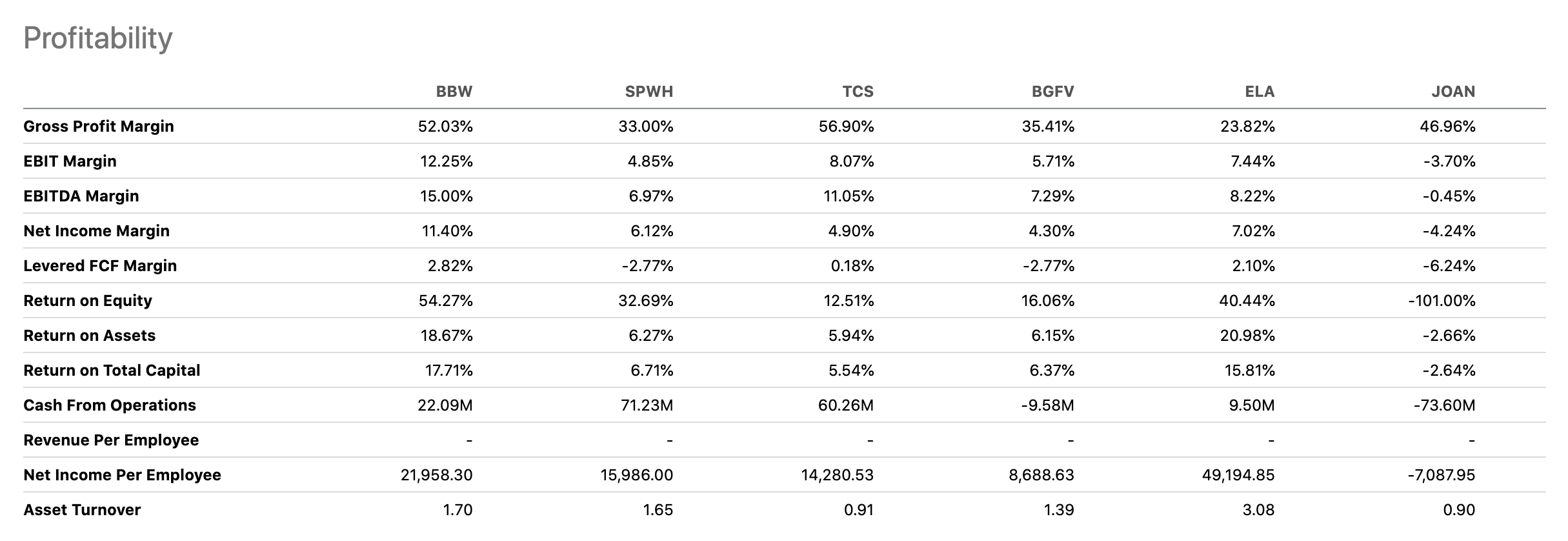

Further, comparing the 11.4% margin with several of BBW's peers, also paints an appealing picture. BBW's net profit margin is materially higher than its peers'.

{kind=link}

But the main question that we need to answer now: Is the net profit margin likely to remain stable or expand further in the coming quarters?

Let us approach this from two perspectives:

1.) Improving macroeconomic environment

The macroeconomic environment has improved substantially since our last writing. Consumer confidence has improved, energy prices have fallen, along with raw material prices and freight costs, and inflation has also slowed somewhat, despite remaining elevated.

In our opinion, these improvements are likely to have a positive impact on BBW's financial performance going forward. The decreasing energy and raw material prices may lead to lower cost of goods sold (as a percentage of revenue), potentially leading to a margin expansion.

2.) Inventory management

In our previous article, we have placed an emphasis on inventory management and our view has been quite bearish. While the inventory levels remain elevated, the rate of increase has slowed substantially, which is a positive sign.

In order to bring back inventories to historic levels, however, the firm may need to use promotional activity and discounting, which could hurt the margins. This negative impact may partially/fully offset the tailwinds from the macroeconomic factors.

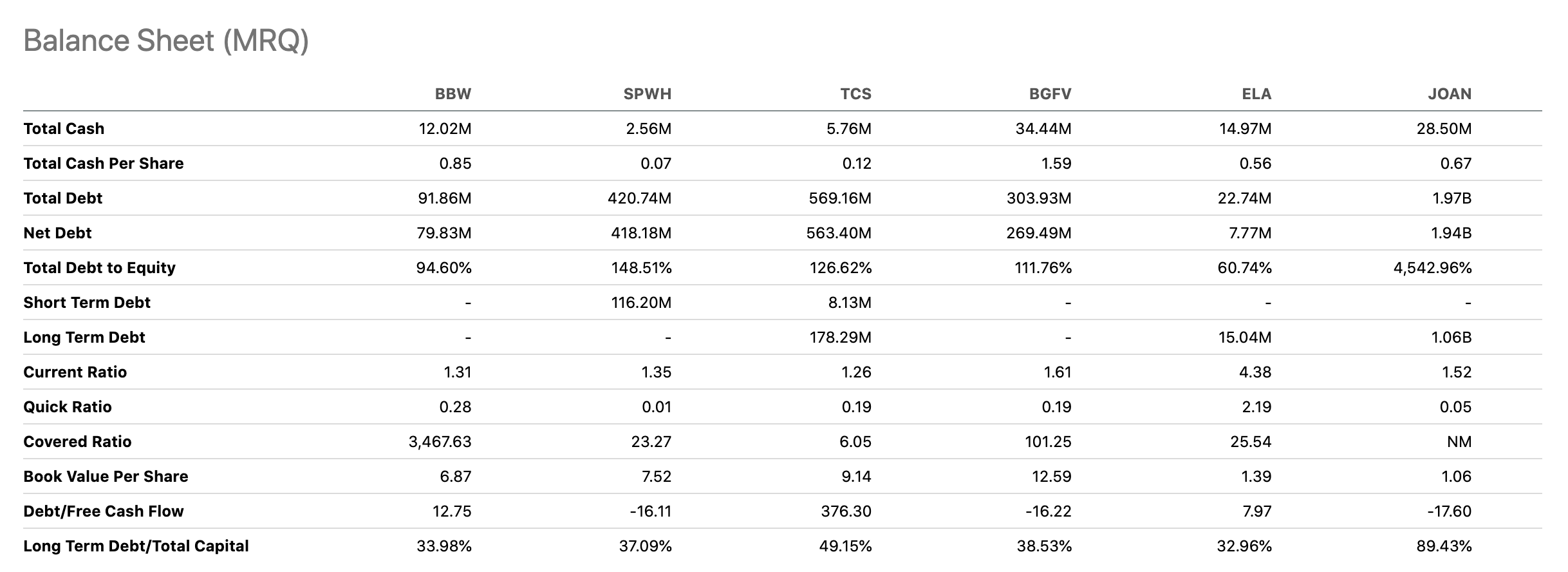

Another reason, why we would like to see inventory levels decreasing is the liquidity. We definitely like that BBW's current ratio is above 1. It means that the firm has enough current assets to cover its current liabilities. On the other hand, the quick ratio is far below 1. The difference between the quick- and the current ratio is that the prior excludes inventory from the calculation. A reduction of the inventory could potentially lead to better liquidity and more financial flexibility.

At this point however we also need to note that it is not uncommon to have quick ratios below 1 in the sector. In fact, BBW's quick ratio compares quite favourably to its peers'.

{kind=link}

All in all, BBW has performed much better in 2022 than we initially expected. Also, the improving macroeconomic environment may generate further tailwinds for the firm in the quarters to come. For these reasons, we believe that an upgrade is warranted.

Asset turnover

Asset turnover, or sometimes called asset utilisation, is an efficiency measure. The higher the reading, the more effective the company is in generating revenue with its assets.

Efficiency has been declining rapidly in 2019 and 2020, primarily as a result of declining sales and the rapid jump in net PP&E in 2020. Since then, however, the trend has changed, and BBW is almost back at its pre-pandemic efficiency levels.

At this point, we often like to take a look at sales, to understand what has been the driver of the improvement. Sales have been growing gradually in the past quarters, but accounts receivable have grown at a faster pace. This could be a warning sign. It may indicate that BBW is using more aggressive accounting or may be selling more on credit. Such actions are normally at the expense of the future performance, as they may be "pulling forward" demand from future periods.

On the other hand, the improving consumer confidence may have positive impacts on the demand. As sentiment improves, the demand for discretionary, non-essential goods is also likely to start improving. For this reason, we believe that BBW's asset turnover is likely to keep improving in the near term.

To sum up

Our view on the firm in 2022 has been too pessimistic. In reality the firm has performed much better than we expected. The net profit margin and the asset turnover have kept improving, despite the challenging macroeconomic environment.

The improving consumer sentiment, along with the declining energy and raw material prices, is likely to create tailwinds for the firm in the quarters to come.

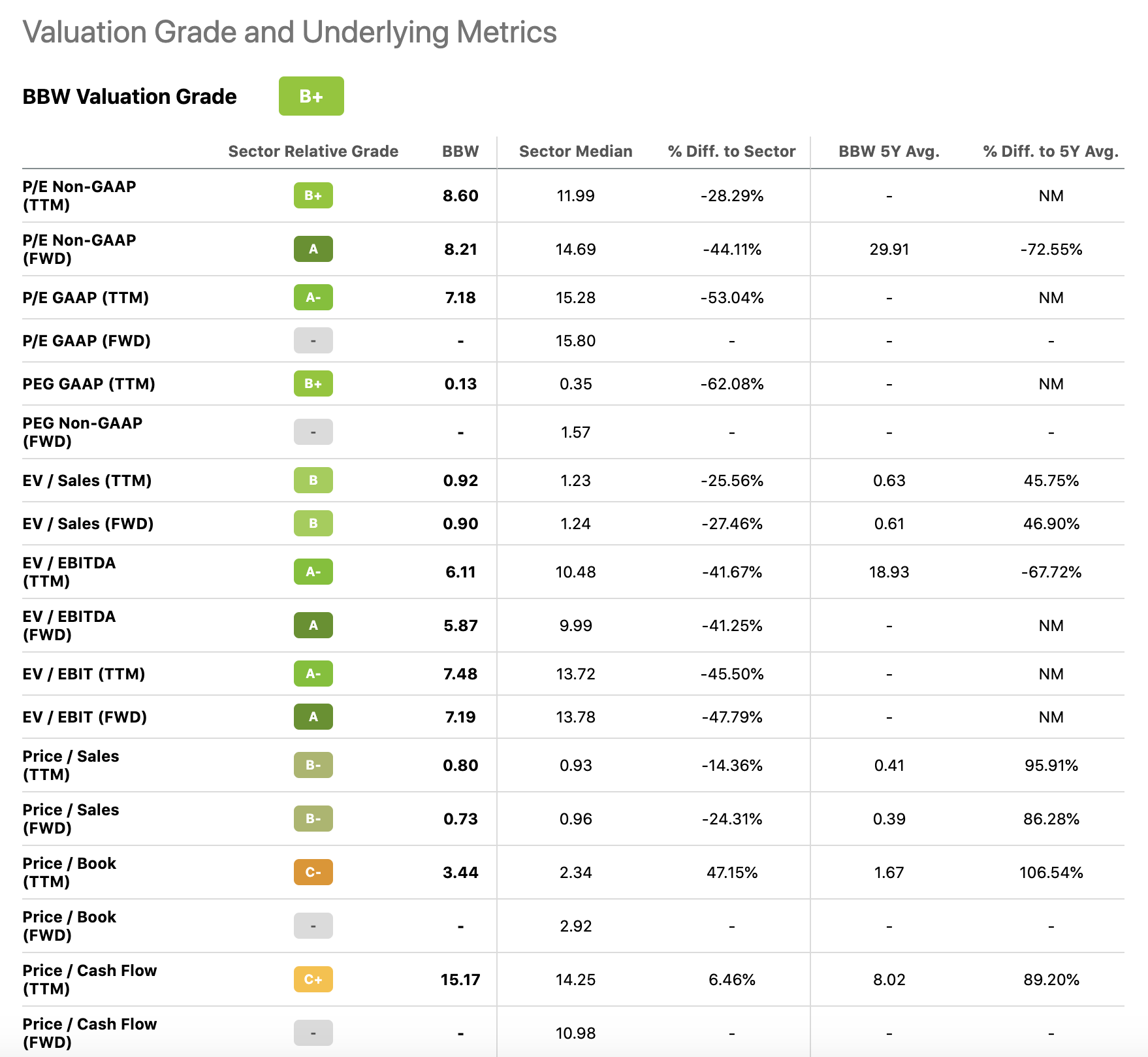

Despite the almost 80% increase in the share price since our last writing, the stock still appears to be valued attractively compared to the consumer discretionary sector median.

{kind=link}

For these reasons we upgrade our rating to "buy".

For further details see:

Build-A-Bear Workshop: 2 Reasons Why We Are Turning More Optimistic In 2023