BBW - Build-A-Bear Workshop: A Massive Opportunity To Beat The Market

2023-11-13 17:39:31 ET

Summary

- Build-A-Bear Workshop presents a massive opportunity with the potential for the stock to double or even quadruple.

- The company has implemented strategic moves towards tourist locations and third-party retail models, leading to growth and profitability.

- BBW's niche positioning, high margins, and strong returns on capital make it an attractive investment option.

- It's a profitable, high-quality company, currently available at a bargain price.

My Thesis

I believe Build-A-Bear Workshop, Inc. ( BBW ) presents a massive opportunity. In short, I foresee the stock doubling, if not more. The reasons are compelling: it boasts high profitability, strong returns on capital, a growth trajectory in both top and bottom lines, excellent management with a commendable recent track record, and a robust brand.

Most notably, it's currently trading at a true bargain price. In the best-case scenario, I anticipate it could quadruple, and in the worst case, at least double.

The Business

Build-A-Bear Workshop stands as an iconic brand that has recently transformed into a multigenerational favorite. Its unique service appeals not just to kids but also to teens and adults. As its name suggests, the Build-A-Bear Workshop provides an immersive experience - imagine stepping into one of its stores and being greeted by a colorful, enjoyable adventure. Here, children have the liberty to choose clothes, names, and more for their bear or other stuffed animals before filling them. This process fosters strong emotional connections to the brand, especially among kids.

Moreover, the management has undertaken operational efforts, which I'll discuss shortly, greatly benefiting their bottom line.

One significant strategy involves the shift towards more tourist-centric locations. Recognizing that the traditional mall setting, while still operational, wasn't yielding the desired results, BBW, under the leadership of their turnaround CEO Sharon John, has been opening more locations in tourist areas. This move transforms the BBW experience into a part of a trip, allowing visitors to connect with the brand during their excursions and then continue their experience at their local BBW store. Notable examples of these tourist-centric locations include Carnival Cruise Line, Great Wolf Lodge Resorts, Landry's, Beaches Family Resorts, and Kalahari.

This shift towards tourist locations intertwines with another strategic move - adopting a third-party retail model. This model proves more profitable, requires less capital, and shows faster growth. BBW aptly describes this approach in their 10-K report:

"The third-party retail model is capital light for us, with the partner company building out and operating the workshops including providing the real estate location and covering the cost of labor and inventory, which is purchased on a wholesale basis. These locations are heavily weighted to the hospitality industry, which allows us to further advance our focus on experience location expansion in non-traditional and tourist areas, as well as shop-in-shop arrangements within other retailers' stores."

The non-traditional retail segment has experienced robust growth, now accounting for 35% of BBW's retail locations.

Furthermore, BBW has made strategic moves towards e-commerce, recognizing the significance of a digital presence. By 2022, e-commerce sales are already constituting 20% of total sales. This online platform is particularly important as BBW can utilize its physical locations for digital purchases and in-store pickups, thereby attracting customers to experience its unique retail spaces.

These operational objectives have significantly contributed to the evolving customer base. Now, teens and adults make up 40% of BBW's customer demographic. The brand has effectively attracted these demographics through savvy marketing strategies, including lucrative brand partnerships such as Disney, SpongeBob, and more. To further expand its reach, I suggest BBW considers attracting Gen Z customers through marketing approaches similar to Crocs, Inc. ( CROX ). By engaging with influencers and embracing unique and quirky collaborations with other brands, BBW can create distinct and appealing products. Crocs, for instance, has collaborated with unexpected brands like KFC and Shrek, drawing significant attention from Gen Z.

Furthermore, BBW has taken innovative strides to boost brand awareness, such as the introduction of BBW vending machines, notably present even in airports. Even if a child doesn't make a purchase from the machine, the mere encounter often sparks the desire to buy a bear later on.

What stands out about BBW is its niche positioning. Due to its distinctiveness, it faces no direct competition. This unique experience proves to be effective, and the company safeguards it through extensive patent and trademark efforts, securing its position until 2032.

Growth

While BBW's growth trajectory hasn't always been consistently robust since its inception, recent years, particularly following the post-COVID period, have shown a more stable and impressive upward trend.

In the last quarterly results announced in August , BBW achieved an 8.5% growth in its top line and has projected a full-year guidance of 5-7%. This growth is commendable, but what's even more noteworthy is the operating leverage BBW has generated. Anticipating a 10-15% pre-tax income growth for the year, BBW's operational efficiency is proving to be a significant driving force. Despite a solid 7% CAGR in the last 5 years, what sets BBW apart is its ability to enhance efficiency, resulting in substantially higher free cash flow growth. This is largely attributed to its margin expansion, transitioning from negative FCF in 2019 to a 12% margin in the last quarter.

The stuffed animals industry is currently valued at about $8 billion in 2022, with projections suggesting a 4.2% CAGR until 2030. Given BBW's historical performance, along with the strategic marketing initiatives and omnichannel push by the management, I believe BBW has the potential to outpace the industry's growth. Nevertheless, even if it doesn't, the current stock price seems sufficiently low to compensate for this, in my view.

Analysts are forecasting a 4% CAGR for the next three years, closely aligned with the expected industry growth. However, earnings per share are projected to grow at a much faster rate of 10% CAGR.

While top-line growth for BBW might surpass industry projections, historically outperforming analyst expectations, EPS surprises tend to balance between positive and negative directions.

The anticipated top-line growth for BBW could arise from three primary avenues: first, through an increase in store count, exemplified by BBW's plan to open 20-30 new stores solely in the UK. Secondly, the growth in same-store sales is expected to be propelled by improvements in demographics and economic conditions, bolstered by effective management operations like marketing strategies. Finally, the expansion of e-commerce operations is also anticipated to contribute significantly to overall growth.

Profitability

From a company that was previously incurring losses, BBW has undergone a remarkable transformation into a highly profitable entity. The CEO has emphasized that each BBW store is currently operating with profitability. The company boasts strong margins, a particularly positive trait for a retailer. I appreciate the presence of high and stable margins, as it reduces the company's vulnerability to margin erosion. Even if faced with temporary margin pressures due to factors like wage hikes, BBW can sustain its investments for future growth, as well as its capacity for buybacks or dividends without significant stress.

These high margins significantly contribute to impressive returns on capital, which, in my opinion, stand as one of the most crucial factors alongside top-line growth. A recent study by Morgan Stanley indicates that the widening gap between the return on invested capital and the weighted average cost of capital is a substantial driver of outperformance. Furthermore, companies with such high ROIC are scarce in the market trading at low prices. I believe that these robust returns on capital are the primary reason why BBW won't remain at a 15% free cash flow yield for an extended period.

Solvency And Return To Shareholders

I believe BBW is in an ideal financial position, boasting a debt-free status and excellent liquidity with a current ratio of 1.4. The Altman Z-Score stands above 4, affirming strong financial health. Hence, I don't find it necessary to delve deeper into these areas.

While BBW isn't consistently issuing dividends or engaging in buybacks, occasional instances do occur. For instance, in March, a dividend of $1.5 per share was paid , providing an approximate 6% yield based on the current price.

I am inclined to advocate for management to consider initiating share buybacks at the current low price, which I believe would greatly benefit the shareholders and augment overall value. The company holds sufficient cash reserves for such actions, ensuring continued investment in growth while returning value to its investors.

Management

The management of a company stands as one of the most pivotal aspects in assessing its investment potential. I greatly value a management team that embraces a long-term vision, prioritizes shareholders' interests, and demonstrates a commitment to the company's sustained success. Sharon Price John, who has served as CEO since 2013, has been at the forefront of BBW's turnaround. Her leadership and recent initiatives seem well-aligned with the company's long-term health. With her extensive experience and deep connections in the toy industry, she brings valuable expertise to the table.

However, I hold reservations regarding BBW's compensation structure. The CEO's allocation of only 32% of compensation in equity is notably low compared to other successful compounders I've encountered in the past. This trend is also evident among other executives. I believe a higher proportion of equity compensation would better align the executives' interests with those of the shareholders. On a positive note, the directors have a more balanced cash/equity compensation structure, with some holding as much as 60% in equity.

The Main Reason I like The Stock - Valuation

As I review business multiples and ratios in relation to its growth and quality, Build-A-Bear Workshop stands out. With a free cash flow yield of 15%, robust double-digit bottom-line growth, and a return on capital employed exceeding 30%, it seems remarkably inexpensive. The PEG ratio stands at 0.6, while the price-to-FCF ratio sits at 4.9. Frankly, I'm struggling to understand why investors undervalue BBW to such an extent.

Let's delve into a discounted cash flow model, exploring both bullish and bearish scenarios.

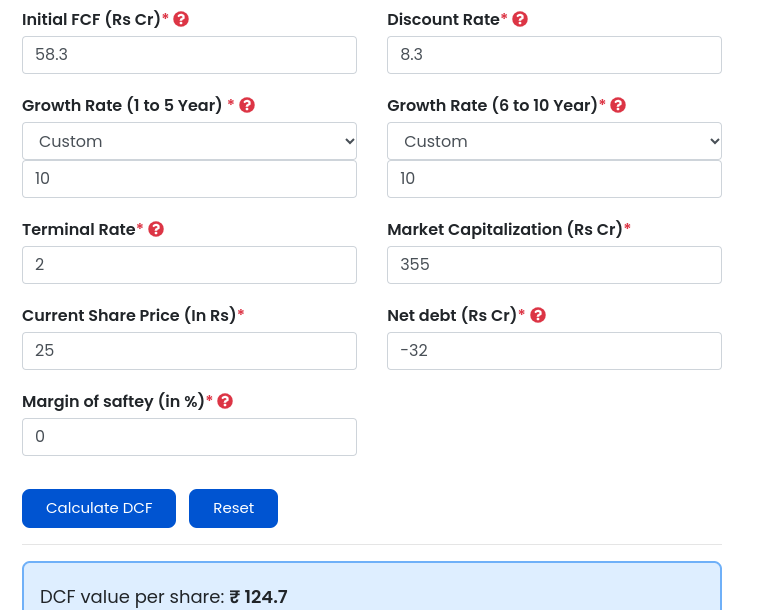

In the bullish case, I'm anticipating reasonable outcomes in the upcoming years. I've set the terminal growth at 2% and a WACC of 8.3%. Utilizing the trailing twelve months' FCF. based upon EPS forecast , I've input a 10% FCF CAGR. This seems plausible, especially considering potential buybacks that could bolster FCF per share. The result suggests a staggering 80% undervaluation, with an intrinsic value of $124. This marks a significant undervaluation.

{kind=link}

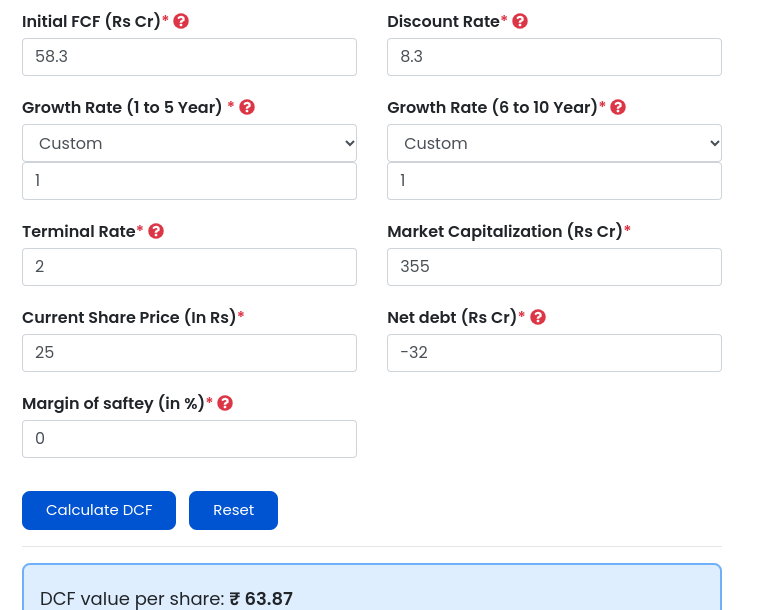

For the bearish scenario, I'm assuming a mere 1% FCF growth, keeping other inputs constant. Despite its improbability given the brand's strength and the ongoing expansion of new locations, even in this pessimistic outlook, the stock remains significantly undervalued by 60%, with a projected stock price of $63.

{kind=link}

This implies that even if the company experiences marginal FCF growth, it remains massively undervalued. I'm at a loss to uncover the reasons behind this substantial undervaluation.

Furthermore, the quant rating stands impressively high at 4.75. Typically, my perspectives and the quant's don't align, making this high rating add to the enigma of the undervaluation.

Risks

BBW has a sweet spot in a niche market, but I don't see strong barriers other than its brand. The high returns might tempt other toy companies to start their own workshops.

There's a risk that the brand might not hold up for adults. Kids always love teddy bears, but adults might just be into it temporarily.

Inflation could be a problem. I'm not sure if BBW can hike prices despite holding onto high margins before.

And if there's a big recession, I doubt people would splurge $20 on teddy bear clothes when they're out of work.

And then there's the mystery of the low stock price. It's a bit worrying not knowing why it's so low.

In short, despite its charm and strengths, these risks might pose some real challenges for BBW's future and value in the market.

Conclusions

BBW's a top-notch company now. It's got solid management, an awesome brand, and a smart strategy, not to mention those high returns on capital.

But what's really catching my eye is the steal of a price. If it was at a 5% FCF yield, I'd probably pass. But at 15% FCF yield and after running the DCF, it's hard to ignore.

So, in my books, BBW looks like a huge opportunity, and I'm giving it a STRONG BUY rating.

I currently don't hold the stock, but I might start a position soon. What are your thoughts on the stock?

For further details see:

Build-A-Bear Workshop: A Massive Opportunity To Beat The Market