BBW - Build-A-Bear Workshop: Attractive Free Cash Flow Overlooked By The Market

2023-12-12 04:49:06 ET

Summary

- Build-A-Bear Workshop is a specialty retailer that allows consumers to customize their own teddy bears/stuffed toys.

- The company experienced a decline in sales after 2008 due to a trend of decline in mall traffic.

- The COVID-19 pandemic forced BBW to invest in e-commerce, leading to the discovery of a new market for teenagers and adults and a reorientation of the physical stores strategy.

- Whilst revenue growth is low, Mr. Market is overlooking Build-A-Bear's free cash flow generation, which is a business's true intrinsic value.

Editor's note: Seeking Alpha is proud to welcome JX Research as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Investment thesis

I believe Build-A-Bear Workshop ( BBW ) is a small-cap company that has been overlooked by Wall Street and institutional investors, resulting in an incorrect impression that they are merely a mall-based retailer. BBW is now rethinking its physical store strategy and expanding its total addressable market size through e-commerce. In my view, the misconception results in misvaluation of the company from its free cash flow intrinsic valuation. Therefore, I have a strong buy rating on BBW with a target price of $44.

What is their business model?

BBW is a specialty retailer that provides a DIY experience to consumers looking to partake in the process of customising their own teddy bears/stuffed toys.

They currently have around 350 corporate-owned stores in operation across the globe, 68 stores through international franchise agreements, and 70 third-party retail stores.

Company 10-K

History of BBW's business turnaround story

BBW was founded in 1997 in St. Louis, Missouri, US by Maxine Clarke, a former retail executive who got the idea of BBW through her young daughter. The idea was a great hit and soon expanded and went public on the New York Stock Exchange in 2004 at $20 per share.

Google finance

However, 3 years after BBW went public, the 2008 house mortgage financial crisis happened. US consumer disposable income was greatly reduced, negatively impacting discretionary goods like stuffed toys. Additionally, there was a broader decline in mall traffic in the US driven by not only the recession but also the rise of e-commerce platforms like Amazon (AMZN). In this period of 2007 to 2019, BBW operated all of its stores in US malls, resulting in a continuous decline in per-store sales and overall revenue. This corresponds to a prolonged period of depression in the share price as shown in the chart above.

Company 10-K

Maxine and her team tried to amend the situation by pushing out more product innovations and collaborating with many other popular toy trends like ZuZu Pets.

However, I believe these product level and promotion attempts by the management have failed to address the fundamental paradigm change to their business model which is a continued decline in traditional US mall traffic.

Maxine announced her retirement in 2012 and brought in a new CEO Sharon Price John and a new management team. The new team with experience from a mix of retailer companies did manage to stabilise the situation but struggled to find a way out of the shrinking mall industry.

Company 10-K

The unexpected turning point happened when 2020 COVID hit.

COVID - The Unexpected Turning Point

The black swan event forced BBW to quickly adapt and invest in e-commerce, transitioning their DIY experience onto the digital platform. Although BBW has always had an e-commerce platform, it was never seriously focused by the management given it is hard to deliver the same in-store experience online.

To their surprise, the e-commerce transition showed them an unexpected opportunity to break into a new market. During COVID, many teenagers and adults were shopping online as well and had purchased from their website. I observe that this demographic is completely different from BBW's historical target which was 4-12 years old kids. As society recovered from COVID restrictions and people went back to BBW's in-person stores, the online demand in fact persisted. In 2023, e-commerce now accounts for about 20% of their net retail sales revenue.

As one can see in their latest investor presentation, the online market highlights a new addressable market that was previously not targeted by BBW.

{kind=link}

70% of purchases online were made by teens/adults who are collectors or gift givers. BBW was quick to capture this trend and opened a series of more mature product options through age-restricted websites like Bear Cave and Build-A-Bear Giftshop.

I argue they can leverage their strong cultural presence in the US and produce pop-culture-related products. For example, Friends and Ted Lasso collaboration products.

{kind=link}

I believe BBW's e-commerce success isn't a fad. It underscores a way to continue to leverage Build-A-Bear's deep emotional connection with its customers even as they grow older and become teenagers or adults.

{kind=link}

I observe that many of the kids who bought their first Build-A-Bear 20 years ago are now young parents or starting their own families. The e-commerce websites and continued digital promotion provide a way for them to reconnect with the brand and pass on the Build-A-Bear experience to their kids who are now 4-8 years old.

Apart from digital innovation, I argue COVID also enabled Build-A-Bear to rethink its physical store business strategy. It has shut many of its non-profitable stores and opened many different new stores at tourist locations like the NBA Hall of Fame, resorts, and cruise ships. They've also promoted the store-in-store model, opening pop-up stores at malls or Walmart. There are also now BBW vending machines at airports, providing advertisement value, and convenience to travellers.

{kind=link}

BBW is well-known that 80% of visits to experience locations are Planned and the top occasion is a birthday. There are over 50mn annual visitors to experience locations each year with strong purchasing power ( Link to investor presentation).

Company investor presentation The US Toys Association

{kind=link}

From a broader toys industry perspective, we can see incredible growth in the Plush segment. According to the US Toys Association , from 2021 to 2022, the industry size grew by 31.1%. As other toy segments declined or remained flat, plush continues to grow. I think this may explain some of the revenue growth outperformance BBW demonstrated against other publicly listed toy companies like Mattel (MAT) and Hasbro (HAS) in earlier quarters of 2022.

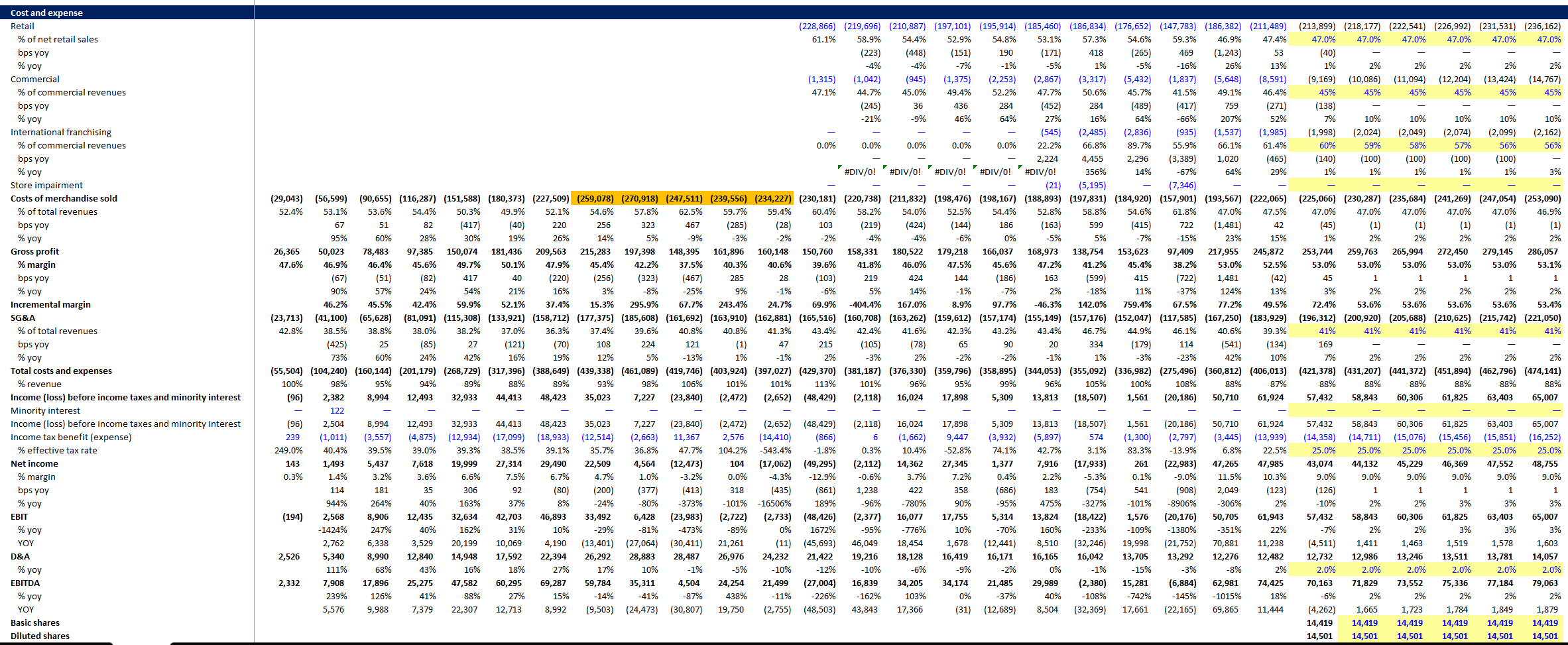

Let's talk numbers - profitability

Company 10-K, author's calculation

BBW is a lucrative business, most of its inventories are sourced from suppliers in China and Vietnam. Although the standard bear costs around $20-35 USD (AUD $30~) as per my estimate, there are many options for accessories or customisations that allow higher revenue per transaction. Accessories like outfits, shoes, and sunglasses can cost between $10 and $35. There are also customisation options like adding scent, voice message, and heartbeat device that can cost $10-20 extra. You can easily see how the price can quickly snowball for parents without even noticing.

During my in-person due diligence at a local Build-A-Bear Workshop, I purchased an original timeless teddy bear (AUD $35) with a suit & tie accessory outfit (AUD $30) and that cost me $65 dollars in total. The parents in front of me paid AUD $80 for a bear.

The flexibility in accessories provides multiple pricing entry points suited for consumers with a wide range of purchasing power.

Since its turnaround, the business has achieved incredible capital allocation efficiency. In 2022, its return on equity ((ROE)) is 45% and its return on invested capital ((ROIC)) is at 27%.

The incremental margin for its gross profit in 2021 is 53% and in 2022, 52.5%, highlighting the sustained high margin for BBW's sustained revenue growth.

Trailing twelve months operating margin is currently at around 9%, a decline from 2022's 13.37%. A result of higher operating expenses due to inflation and wage increases.

Valuation - Summary

Author's calculation, company 10-K

My historical multiples in the summary sheet are more for sense check. It doesn't mean much since the enterprise values or prices are current ones. The forward-looking multiples are more insightful.

BBW is valued cheaply at around 7x forward P/E right now which I think is not justified given its strong return on equity and potential long-term earnings growth.

The company has strong free cash flows and it is trading at an incredible 19% free cash flow yield as of now.

The valuations are guided by conservative forecasts of a 2.3% annual growth rate going into the future and a stable margin similar to today's.

Valuation - Free Cash Flow

I'm more a fan of free cash flow than a relative valuation approach. As a value investor, measuring intrinsic value is more important than using market price as guidance especially when Build-A-Bear is a unique company with no direct comparable peers.

Under the key assumptions I mentioned above, below are the free cash flow calculations.

Author's calculations, Company 10-K Author's calculations, company 10-K Author's calculations, company 10-K Author's calculation

{kind=link}

{kind=link}

{kind=link}

{kind=link}

This provides us with a target price of $43.

Author's calculation, Seeking Alpha data, company 10-K

Valuation - Multiples

As you can see in the summary page, my earnings forecasts are, in fact, more bearish than the sell-side consensus views, especially from an EPS perspective.

If we attribute a multiples expansion to BBW's earnings growth prospect in the future, the company is quite undervalued.

The US equity market right now (S&P 500) trades at a forward P/E ratio of 17x. I think it is plausible to make the case that BBW has the potential to expand to 12x P/E 12 months from now if the market realises the earnings growth prospect from BBW and attributes a higher multiple.

Koyfin

To put it into perspective, 12x P/E NTM is plausible given it historically traded at a range of 12x to 20x excluding negative or volatile earnings periods.

Author's calculation

Share buybacks driving EPS growth

Company 10-K

As of Jan 28, there is $46.5 million worth of funds left for the share repurchase program which is about 14% of its current $345 million market cap. Whilst this is a good sign that they are returning shareholder money through buybacks, it is unclear whether it is beneficial in reducing the number of floating shares and reducing liquidity given it is already thinly traded.

3 main risks:

Why is it so cheap - no free lunch

Build-A-Bear is cheap from an intrinsic free cash flow valuation perspective, but I think the current market doesn't favour companies with low growth like BBW (3-5% according to management's downgraded guidance from Q3 earnings call).

Given the fact that Build-A-Bear is a small-cap company with only $350 million market cap, there isn't much attention from institutional investors or Wall Street analysts. There are currently only 3 research brokers covering BBW and they are all regional boutiques. The latest price target from DA Davidson is $38, a cut from the previous $42 price target.

The stock has low trading volume, resulting in low liquidity. The price does become quite volatile due to this. Without enough market participants looking at this stock, it is difficult to achieve a price correction.

The potential for recession may hurt consumer spending

There is still the risk of recession and a drastic decline in consumer discretionary spending next year. However, toys have historically been surprisingly resilient against recession relative to other discretionary goods and the current price seems to be low enough to compensate for that risk. To investors, it's the price of risk that matters the most.

Key man risk - BBW CEO

The current CEO has led the multi-year turnaround effort from 2012 onwards. It is unclear whether the business can be run efficiently and to the same standard without her leadership.

Conclusion

I continue to see strong fundamentals in the Build-A-Bear workshop despite slow top-line growth. There may, in fact, be positive surprises in Q4 as they release their first-ever Build-A-Bear Christmas movie with a local US cinema franchise. The movie will also be available on all streaming platforms along with movie-themed stuffed toys.

From a valuation perspective, there is a clear mis-pricing by the market but it is unclear when price correction will happen.

Therefore, I maintain a strong buy rating and expect pricing correction to occur either in the form of a potential private equity takeover or as the Build-A-Bear workshop continues to perform steadily over the next 2 years, the market may finally pay attention to this gem.

For further details see:

Build-A-Bear Workshop: Attractive Free Cash Flow Overlooked By The Market