BBW - Build-A-Bear Workshop: Strong Capital Allocation And Growing Prospects

2023-04-06 10:47:09 ET

Summary

- Build-A-Bear Workshop, Inc. has just returned a 6.3% dividend this month.

- Build-A-Bear Workshop is pressing ahead and succeeding with its digital marketing strategy.

- Build-A-Bear Workshop is less sensitive to an economic downturn than many of its retail peers.

Investment Thesis

Build-A-Bear Workshop, Inc. ( BBW ) is outperforming expectations. Despite the challenging environment where many retailers are struggling, with customers being more price-conscious, Build-A-Bear Workshop is still delivering solid growth. Do you know why?

Because Build-A-Bear Workshop's business model is not for the price-conscious consumer. It's about selling an experience to households that can afford it.

Paying mid-single digits P/E for a business that's clearly succeeding in evolving its digital marketing efforts and delivering omnichannel value strikes me as a compelling investment opportunity.

Strong Prospects Despite The Challenging Macro Environment

What BBW sells is an emotional connection. That's why the business has succeeded with its turnaround efforts, and the share price is on the cusp of crossing into a multi-year high.

Meanwhile, the macro environment remains brutal. Consumers are feeling the pinch and are extremely price sensitive.

Also, consumers are shopping more online and have fewer reasons to purchase offline. Indeed, as you know, since the pandemic consumers have increasingly resorted to shopping online, rather than to return to shopping malls. And with reduced footfall through shopping malls, this is yet another reason why BBW should be struggling . And yet, the facts appear to contradict that narrative.

And the reason why BBW has succeeded in continuing to grow its top line is that BBW has been able to evolve its prospects through a digital strategy alongside its focus on seeking out prime retail locations. On this front, this is what BBW stated on its earnings call :

[...] we continue to expand our digital marketing capabilities to more efficiently reach a diversified and broadened consumer base to acquire new guests and increase the frequency of repeat purchases.

This calculated action has led to a significant increase in our total addressable market beyond families with younger children to include teens and adults, which currently represent approximately 40% of our end users.

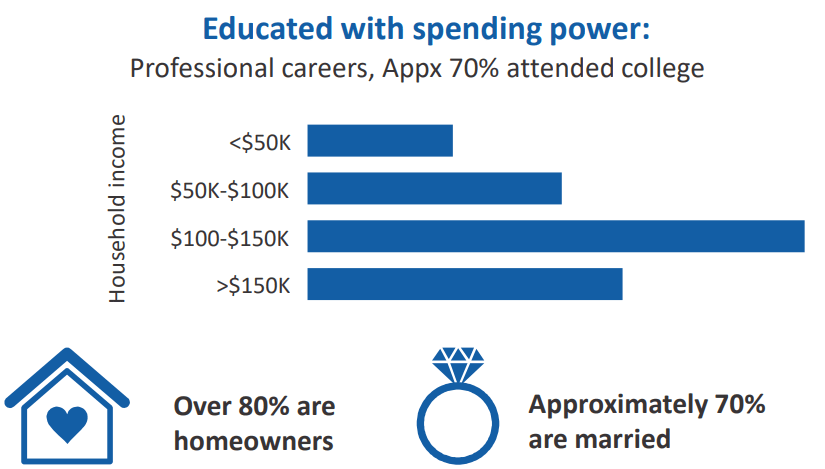

Similarly, consider BBW's customer demographics.

{kind=link}

Its typical customer has strong spending power. Reinforcing that its customer base isn't looking for a bargain, but rather to pay for an experience.

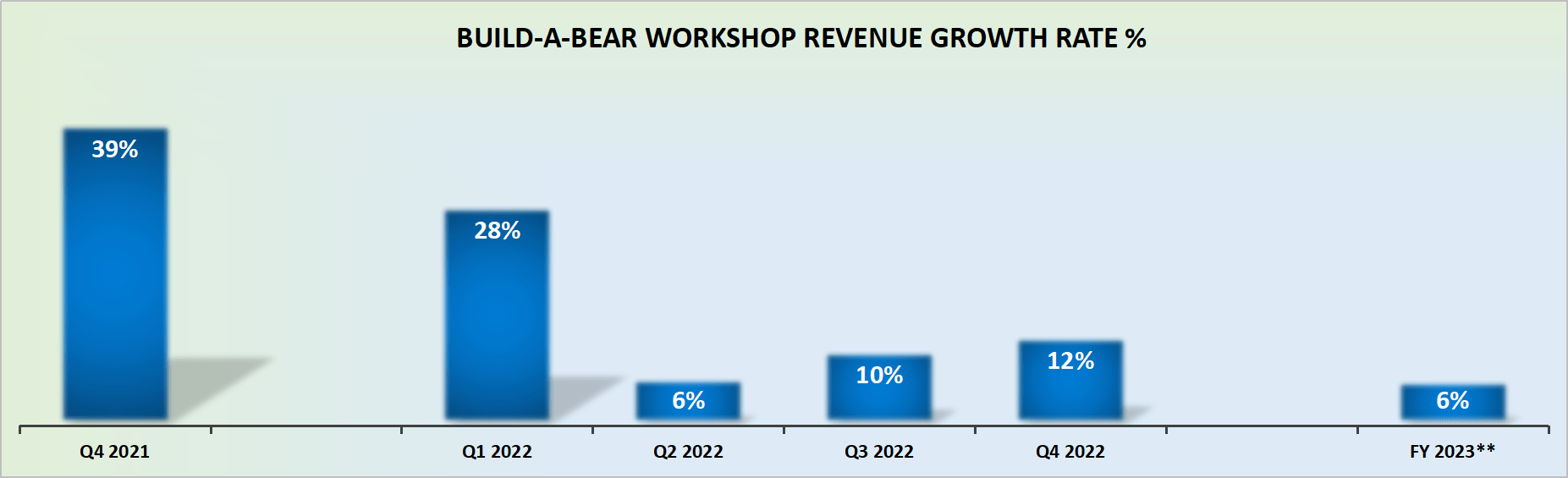

Revenue Growth Rates Remain Solid

{kind=link}

Notwithstanding the tough comparables from fiscal 2021 (not shown), the business is still growing in the mid-single-digit.

When a business can report consistent growth, a lot of great things can happen. First of all, investors love a business with secular growth. Obviously, the more growth the better, but the important fact is to have some growth. Particularly with the stock being cheap enough that investors are not pricing in any growth.

Ready, Set, Capital Allocation

Shareholders on record on March 23, 2023 will be getting a $1.50 special dividend these days. This wasn't a recurring dividend. But getting a 6.3% yield is nothing to sneer at either. Not in this market environment.

Furthermore, BBW has been active in repurchasing its shares. Roughly speaking, it repurchased about 6% of its market cap in fiscal 2022 and BBW declares that it still has a further $46 million worth of repurchases available.

Personally, I'm not a fan of share repurchases, I would vastly prefer more dividends. But getting potentially 6% of your cash returned via repurchases on top of a 6% dividend yield makes this investment very compelling.

Indeed, given that BBW is clearly reporting positive free cash flows and holds more than $20 million of net cash on its balance sheet , I believe more special dividends could come in the next 12 months.

The Bottom Line

The one-line summary is this: Build-A-Bear Workshop, Inc. is cheaply valued with an attractive capital allocation policy.

BBW Q4 2022

The expanded summary is that the key reason why the business is reporting solid growth rates is that it's embracing its digital opportunities to drive profitable revenues through its brick-and-mortar premium location stores.

Build-A-Bear Workshop, Inc. is a business that has plenty of runway to grow and roll out more stores given its positive unit economics. Paying less than 8x EPS for BBW stock is a bargain.

For further details see:

Build-A-Bear Workshop: Strong Capital Allocation And Growing Prospects