BBW - Build-A-Bear Workshop: Turnaround Story Keeps Getting Better

2023-03-24 11:46:05 ET

Summary

- FY22 proved to be a strong year even after the year we had.

- Further growth can be achieved through digitization and further promotional initiatives.

- The financials of the company are pretty good, although I'm slightly skeptical of profitability and efficiency metrics.

- With conservative assumptions modeled for the next decade, the company is still a buy at these levels, but the uncertainty of the global economy may present a better entry point.

Investment Thesis

With the great turnaround story of Build-A-Bear Workshop (BBW), I wanted to take a closer look at how the company did at the end of '22, what has improved, what can be improved going forward and how can the company continue its turnaround story. With the plans of further digitization, I model that the company will be able to improve its gross margins by around 2% and if the company manages to retain such a free cash flow as they have right now, the company is a buy at current levels and may reward shareholders further if everything is going to go the management's way. Even with my conservative approach to the model, the company has still room to grow.

Financial Year-end Results

So, the company had quite a good '22, unlike many other companies that saw revenue declines from the prior year, the company had an acceptable double-digit growth of 14%. The company did see a decline in demand for their e-commerce segment of around 8%, however, the management put this into perspective a little more by telling us that the e-commerce business is up around 138% compared to pre-pandemic levels. Commercial and international franchise revenues are up 58% from the prior year. The company opened another 9 stores during the year, which from looking at the figures from prior years, is not too small. Sometimes the company adds less, sometimes more over the year.

Outlook and Further Growth

The management made my job a little easier by giving me what they see as a possibility for '23. The company expects to grow revenues at 5%-7%, pre-tax income growth of 10%-15%, CAPEX does be in the range of $15m-$20m, D&A $13m-$14m, and taxes at 25%. This gave me a good starting point for my model. Of course, I did not take these figures at their face value, because I like to be more pessimistic and more conservative in my estimates.

The company currently operates almost 500 stores, between corporately managed, third-party retail and international franchises. The management is aiming to open another 20-30 locations in the second half of the year, however, no mention of how many will be closed as usually there are stores closed every year for one reason or another

I see two major growth catalysts that could propel the company's revenues by broadening the customer base further, which includes teens and adults, not just families with kids. Both catalysts are related: further digitization in the e-commerce space and more promotional initiatives that would attract more grownups and young adults.

Digitization

Digitization for the company will have a huge impact on its revenues and improve margins if the company manages to implement it correctly. With streamlined experience on their website, which stores data, and using machine learning models to predict and adapt to what the customer needs from the retailer will help attract a new kind of customer that is not just a family with kids, but also adults and teens. All of that data is already paying off, in their most recent report, the CEO said that they are looking into opening locations not only in tourist-heavy areas anymore but also see synergies of opening localized stores where people live because once a person gets to experience the building of a bear in one of their touristy areas like a funfair or other similar location, the person would be interested in having a Build-A-Bear location close to where they live, so they could buy one for a special occasion like a birthday or Christmas. This opens the field quite a bit to where they can put a store and scale further.

It's been a while since I needed to purchase something that I wasn't able to get online. From buying gifts to impulse buys. Adults and teens make up around 40% according to the transcript , which is a lot of millennials like me, who prefer to shop online, and generation Y is not far behind us in that sense. Everyone's on their phones buying stuff on Amazon ( AMZN ) or ordering food. A streamlined, responsive, and easy-on-the-eyes website or application is a must in this age. Unfortunately, right now, the website is not very appealing to the eyes. I dabbled in running a Shopify ( SHOP ) store some time ago and Build-A-Bear has all the same functionalities as my old store, and I was kind of hoping that at the end of the website, it would say "powered by Shopify". One good thing I found on the website is the 3D workshop where you can build a bear from scratch, but that also was very janky. I currently reside in Mexico, and I wanted to buy an axolotl stuffed animal, I saw they are selling it and it is very popular, however, it is not available in the 3D workshop to see what it would look like. The website needs a lot of improvement in my opinion.

There are certainly ways of improving on this aspect, and I'm not surprised that there were declines in this segment's revenue. It needs a lot of work to attract a larger customer base, but it looks promising as the management is going to be working on optimizing the performance over the next while.

Promotional Initiatives

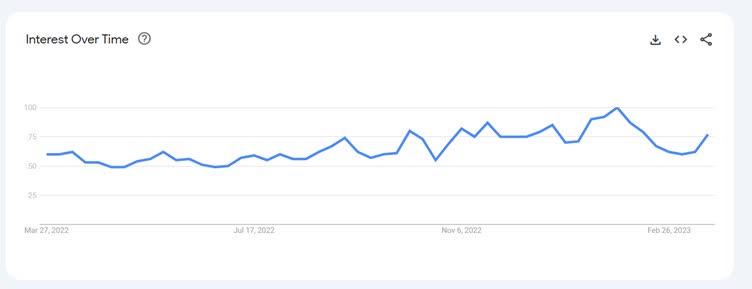

This next catalyst goes hand in hand with digitization and I believe there is some potential for a cross-promotional activity to attract a larger customer base. Platforms like TikTok, Instagram ( META ), and YouTube ( GOOG ) have seen quite an explosion in people sharing their bears and experiences in stores, garnering millions of views, which turns into billions of clicks a year. The reach is huge and there is potential as Google trends have shown a steady increase over time of building-a-bear searches online, with a recent dip that seems to be picking back up.

Google Trends of BBW (Google Trends)

{kind=link}

The company needs to do more digital promotion and they have quite a few in the pipeline right now with the most notable one an undisclosed documentary about the rise of the company which should be released sometime this year and another big one is slated to be released in time for the holiday season is the company's first animated Christmas feature called "Glisten and the Merry Mission", which boasts stars like Chevy Chase, Billy Ray Cyrus, and Michael Rappaport. This will certainly sell a good number of plush toys when it comes out.

The company's ability to attract adults and teens would be great if they keep continuing with cross-promotional products, for example, bears that are from popular films and tv series, I know a few people who would like to have a plush animal that's from Breaking Bad or Game of Thrones, just for that nostalgia (maybe they have done these already and I missed them, I don't know). I know these shows are a bit outdated, but the idea is there, keep up with pop culture which will attract some customers.

Overall, there is a lot of promise in the promotional space for the company. With a very recent release of Build a Bear Tycoon on Roblox ( RBLX ), metaverse possibilities are opening for the company to promote itself further and reach more customers.

If the company can execute digitization and promotional initiatives, coupled with more store locations, there is a good amount of growth left in store.

Financials

In the last 10 years, the company's revenues have not been growing much, culminating at a bottom during the pandemic lockdowns where the company saw a 25% decrease in revenues, only to come back very strong the next year with 61% revenue increases. Over those 10 years, the company grew on average by 2% a year. The share price soared from around 90 cents or so to as much as $25 a share. Let's see what the balance sheet is saying to us right now.

I like that they have been able to generate positive un-levered free cash flow for at least 5 years now and with no debt on the books, the company seems to be very liquid and is not going to be in any trouble anytime soon.

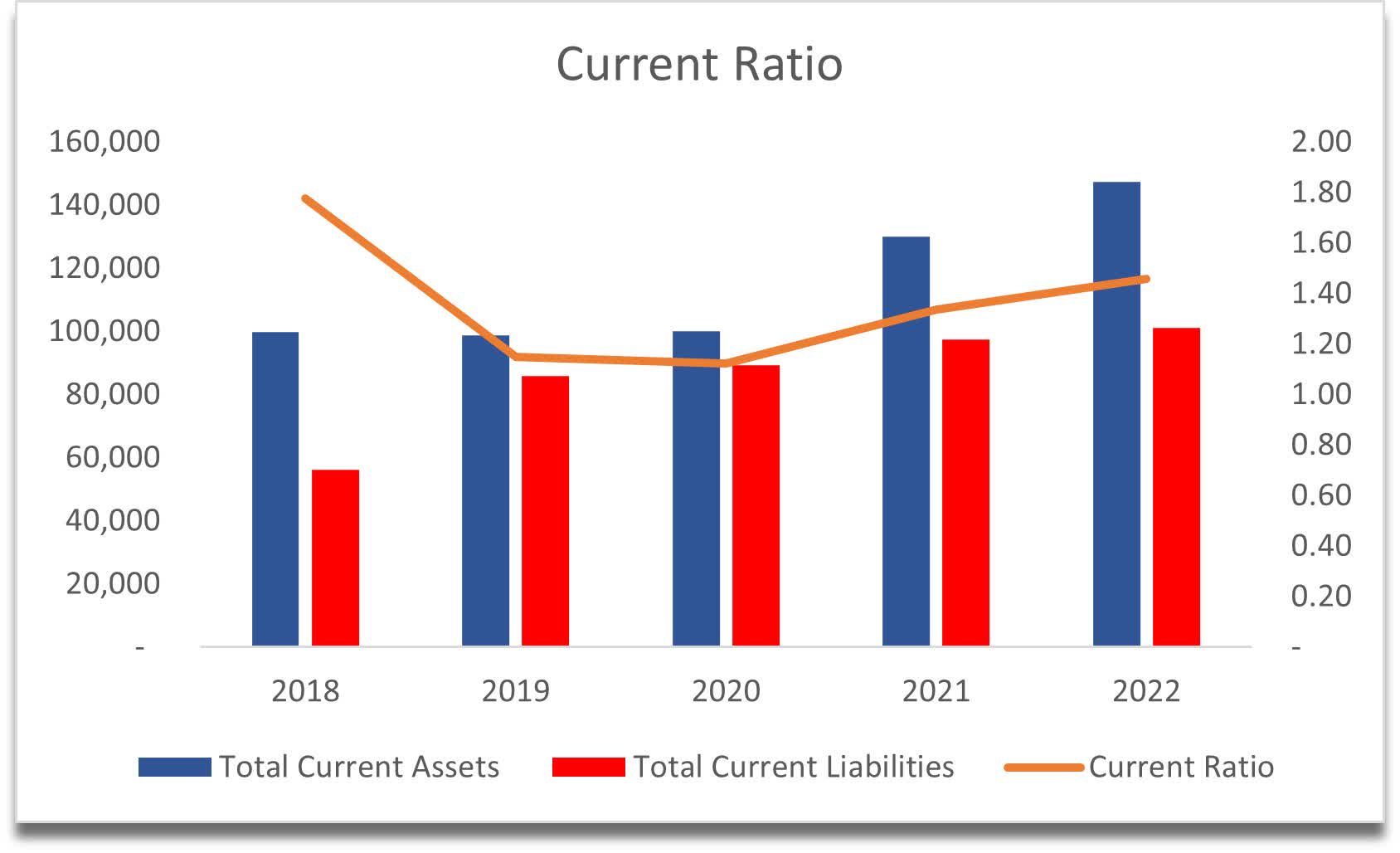

Speaking of liquidity, the company has an acceptable current ratio that has improved in the last couple of years also and if it gets to around 2.0, that would signal to me the company is being managed quite efficiently.

Current Ratio (Own Calculations)

{kind=link}

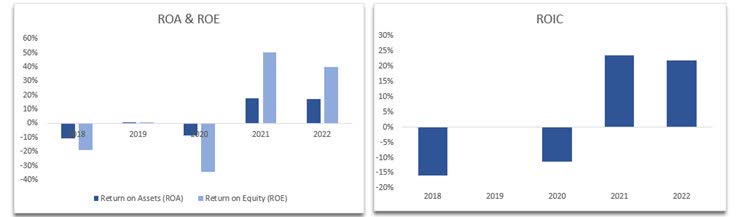

The next few metrics make me a little skeptical. We can see a big turnaround in profitability and efficiency metrics since the pandemic. These metrics were quite deep in the negatives even before the lockdowns and now they are very much acceptable. I'm talking about ROIC, ROA, and ROE. The company somehow managed to turn around quite quickly right after the pandemic. Is this a long-term trend or will we start to see efficiencies and profitability come back down in the next couple of years? I hope not.

ROIC, ROA and ROE (Own Calculations)

{kind=link}

A strong balance sheet with no debt tells me that the company is being managed well and if the above metrics can keep above 0 then I would become less skeptical because I do not see any other potential red flags here.

Valuation

For my model, I will keep it simple. I will piggyback off what the management expects from '23 and will assume more conservative estimates. As I mentioned earlier, the management expects revenue growth of 5%-7% for the year. For my base case, I went with 5% in '23 and '24, then seeing that in the last 10 years, the average growth has been around 2%,I will linearly grow down these estimates to 1% in '32, which will give me an average growth rate of 3.15% for the next decade. I assume a little better growth because of digitization improvements. On the optimistic side, the average growth will end up being 5.2% and for the more conservative case is 1.2%. I couldn't give higher growth numbers than that because a lot of the years in the past the company has experienced negative growth and I like being more conservative to test the company.

I also assume a slight margin expansion over the decade of around 2% in gross margins in my base case. I reason that the company will become more efficient through digitization, but not by much to keep it conservative. In the optimistic case, the margins improve by an additional 100bps and in the conservative case the margins are 100bps worse than in the base case.

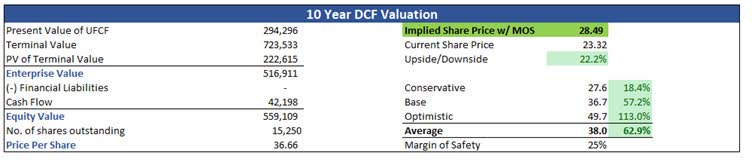

On top of these conservative estimates, I also like to add a margin of safety of 25% to the final intrinsic value. With everything inputted in the model, the implied intrinsic value of Build-A-Bear Workshop is $28.49 which implies a 22.2% upside from current valuations.

DCF Valuation (Own Calculations)

{kind=link}

Conclusion

There is potential for the company to become very popular among all sorts of demographics if they execute on the promotional and digitization side of things. It seems that the pandemic got them scrambling for new ideas on how to dig themselves out of the rut they have been in for a while. Let's hope that what we are seeing right now is the new norm, where margins keep improving and the company can expand further into what hopefully will be profitable areas in the world.

I feel the above assumptions of mine are quite conservative and I would like to see the company beat these over the long run, which would make the company even more attractive, coupled with a big improvement in profitability and efficiency, which I hope are not flukes for the last two years, we have ourselves a good contender for a long-term hold.

There are risks of course. The company goes back to being unprofitable, the popularity wanes and people don't buy the bears anymore. In terms of volatility, the global economy has been on a rollercoaster for a while, and I don't believe we're not out of the woods yet. There may be an even better entry point if the inflation persists for much longer than anticipated, the stock market will be volatile and will affect the company's share price in the short run. If you are ok with the risk as I am, I will be looking at starting a new position shortly and keep it for the long haul, unless something materially changes in how the company operates which will affect my thesis. If that happens, I will re-assess and do what is right accordingly, whether that is to sell the stock or add further.

For further details see:

Build-A-Bear Workshop: Turnaround Story Keeps Getting Better