VICI - Build A Sucker Free REIT Portfolio

2023-04-24 07:00:00 ET

Summary

- Before you get angry for calling you a sucker, let me be clear, all of us have a weak spot.

- As legendary investor Warren Buffett once said, “Look around the poker table. If you can’t see the sucker, you’re it."

- My best advice is to stay clear of the “sucker yields” and instead to accumulate shares in REITs like O, ADC, and VICI – all overweight positions for me.

In sports betting, a sucker bet is basically exactly what it sounds like, a bet that only a real sucker would take, and it refers to whether a gambler is playing their odds correctly.

One example of a sucker bet in blackjack is splitting 10s. If you get two of any number in blackjack, you can split the hand for an additional wager, and you play two separate hands.

Splitting two 10’s can have a massive upside, but in the long run, you are only worsening the odds.

In the investing world, there’s another “sucker” term we use called the “sucker yield” and similar to the “sucker bet” it stems from the same concept in which the investor is not playing their odds correctly.

Before you get angry for calling you a sucker, let me be clear, all of us have a weak spot. Probably many of us actually. As legendary investor Warren Buffett once said, “Look around the poker table. If you can’t see the sucker, you’re it."

As a true measure of safety, investors should always analyze at least these three aspects beyond just yield:

- The dividend’s underlying safety.

- The dividend’s ability to grow from current figures.

- The stock’s overall merit

High yields can be enticing but one must do their due diligence to make sure the business model, earnings, and the dividend payout are sustainable.

A high yielding stock is tempting, but if the dividend cannot be sustained, you may not receive the yield you were expecting when all is said and done.

That and typically the stock price does not fare well when a company cuts their dividend, especially if it’s an income investment like REITs, BDCs, and MLPs. So before jumping into a mouth-watering yield, you should make sure that the business fundamentals support the payout.

I mean, who wouldn’t want to receive a 13.31% dividend yield, or an 18.84% dividend yield like City Office ( CIO ), AFC Gamma ( AFCG ), or Global Net Lease ( GNL )?

But as I’m sure most of you know, there is no free lunch, and a high yield implies that the market has priced in a high level of risk.

As seen below, CIO pays a 13.31% yield, but they currently have a payout ratio of 119.40%. Funds from operations (“FFO”) are expected to fall by -11% in 2023. Is that 13.31% yield sustainable?

I’ve included a few of the companies on our Dividend Cut Watchlist for some examples. At iREIT we are constantly monitoring the payout levels to see if there is a potential dividend cut around the corner.

iREIT

Dividend Safety Screener

In general, REITs have a spread business model.

In order to make acquisitions that are accretive to earnings the properties cap rate (net operating income / property market value) must exceed the company’s weighted average cost of capital.

In other words, the yield received on the property (cap rate) needs to be greater than the cost associated with raising the capital for the purchase. Below I’ve listed the investment spread for each company in this article:

iREIT

Now let’s look at three “sucker free” REITs that pay a high yield and have a healthy payout ratio. The first on the list is none other than the king of the triple-net-lease sector – Realty Income.

Realty Income ( O )

Realty Income is a triple-net-lease real estate investment trust (“REIT”) that was founded in 1969 and went public in 1994. They own or have an ownership interest in 12,237 properties that are primarily free-standing, single tenant buildings.

Realty Income has domestic properties in all 50 States and international properties in the United Kingdom, Spain, and Italy. They have an occupancy rate of 99% and a weighted average lease (“WALT”) term of approximately 9.5 years. Realty Income primarily invests in retail properties, but also has industrial properties that makes up 13.3% of their portfolio and gaming properties that makes up 2.9%.

Realty Income - Investor Presentation

Dividend

Realty Income is a Dividend Aristocrat that has increased the dividend for 28 consecutive years and has delivered a compound annualized growth rate (“CAGR”) of over 4.4% since 1994.

Since going public they have paid 632 monthly dividends and have increased the dividend over the last 101 consecutive quarters. As far as the dividend goes, Realty Income has an excellent track record and has never paid a “sucker yield”.

Realty Income - Investor Presentation

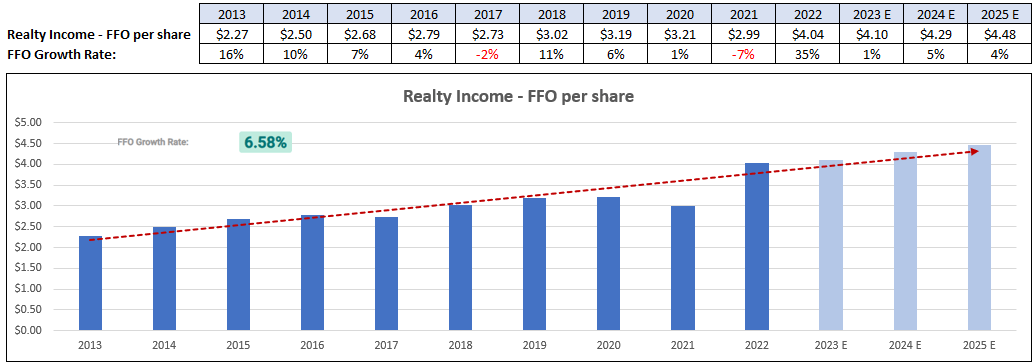

Funds from Operations

Since 2013 Realty Income has had a positive cash flow each year and increased its FFO per share each year except for in 2017 and 2021. FFO increased by 35% in 2022, but that is expected to normalize with projected growth rates of 1% in 2023 and 5% in 2024.

Overall, Realty Income has an average FFO growth rate of 6.58% since 2013. The consistency and growth of their FFO shows that their business model is successfully being executed.

{kind=link}

Adjusted Funds from Operations ((AFFO))

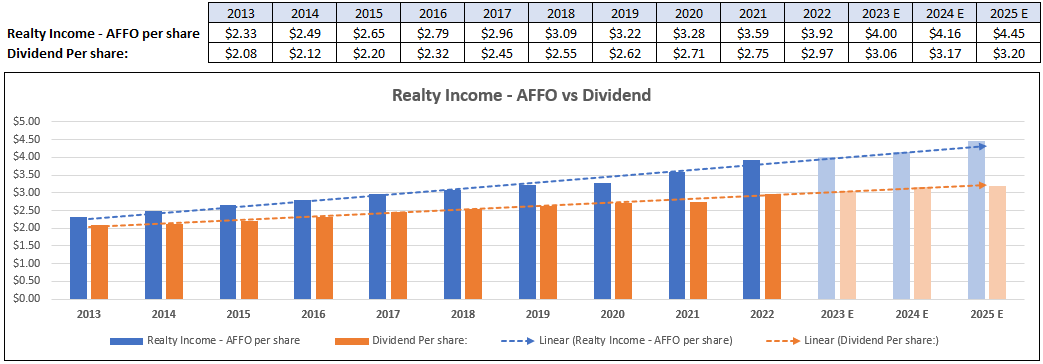

There is no standardized definition for AFFO, but a general guideline to calculate AFFO is to take FFO and deduct recurring capital expenditures and straight-line rent.

AFFO can be looked at as a close proxy to free-cash flow since it is funds available for investment and / or distribution after accounting for all expenses. In order for the dividend to be sustainable over the long term, the AFFO payout ratio needs to be under 100% and preferably under 85-90%.

Corporate Finance Institute

Realty Income’s AFFO has covered its dividend payout each year since 2013. Observing the trendlines below shows that the gap between their AFFO and dividend payout is widening or put another way their AFFO covers the dividend by a wider margin now than it did in the past.

{kind=link}

Payout Ratio

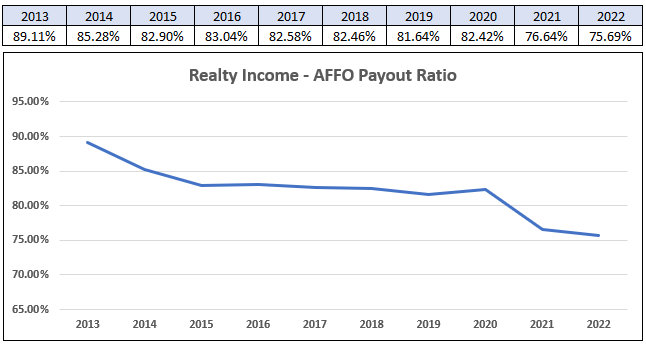

Realty Income pays a 4.91% dividend yield that is well covered by their AFFO with a payout ratio of 75.69% in 2022. This metric has been improving over the last 10 years going from 89.11% in 2013 to its current payout ratio of 75.69%.

{kind=link}

Investor Takeaway

Realty Income pays a monthly dividend that is definitely not a sucker yield. They have consistently delivered earnings and dividend growth while maintaining a conservative payout ratio that has been improving over the years.

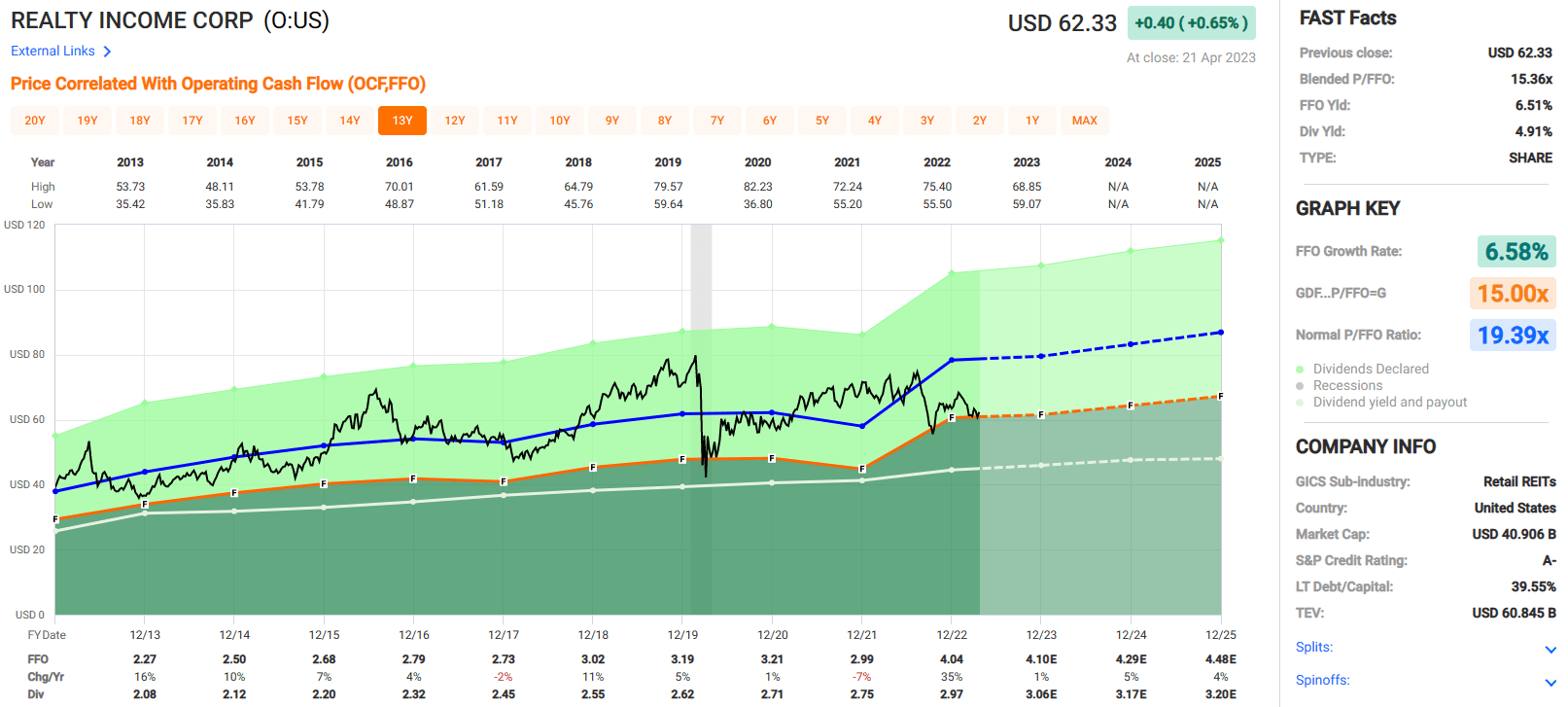

Currently the stock is trading at a P/FFO multiple of 15.36x which is well below their normal P/FFO of 19.39x. At iREIT we rate Realty Income a BUY.

{kind=link}

Agree Realty ( ADC )

Agree Realty is a net-lease REIT that in many ways is like a smaller version of Realty Income. ADC was founded in 1971 and went public in 1994. Their portfolio consists of 1,839 properties that cover approximately 38.1 million square feet and are located in 48 states.

ADC’s portfolio is 99.7% leased with a weighted average lease term of approximately 8.8 years and 67.8% of their annualized base rent (“ABR”) comes from tenants that have an investment grade credit rating. ADC primarily targets retail properties that are in e-commerce resistant sectors.

{kind=link}

Dividend

ADC paid quarterly dividends from 1994 to 2020 and then moved to a monthly dividend in 2021. They paid dividends for 107 consecutive quarters before making the change to a monthly schedule and since that time have paid 25 consecutive monthly dividends.

Since 2012 ADC has a delivered a compound annualized dividend growth rate of over 6% and has increased the dividend each year. Plus, over the past 10 years, ADC has averaged an AFFO payout ratio of 76%. Like Realty Income, there is nothing in ADC’s dividend track record to suggest that they pay a sucker yield.

{kind=link}

Funds from Operations

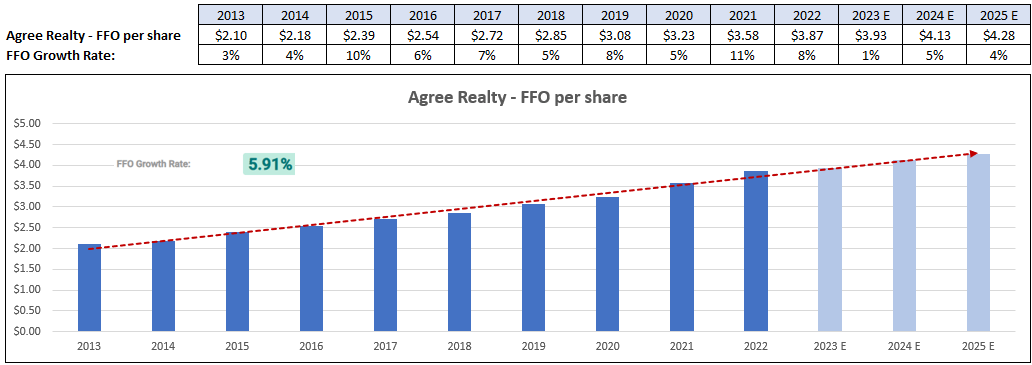

ADC has delivered FFO growth in every year since 2013 with an average growth rate of 5.91% since that time. FFO increased by 8% in 2022, but analysts expect the rate of growth to slow to 1% in 2023 and then increased to 5% in 2024.

Agree Realty has delivered consistent positive cash flow and growth in its funds from operations over the last decade. The consistent growth in earnings shows that ADC has a sound business model and has made investments at an attractive spread that have been accretive to earnings over the last 10 years.

{kind=link}

Adjusted Funds from Operations

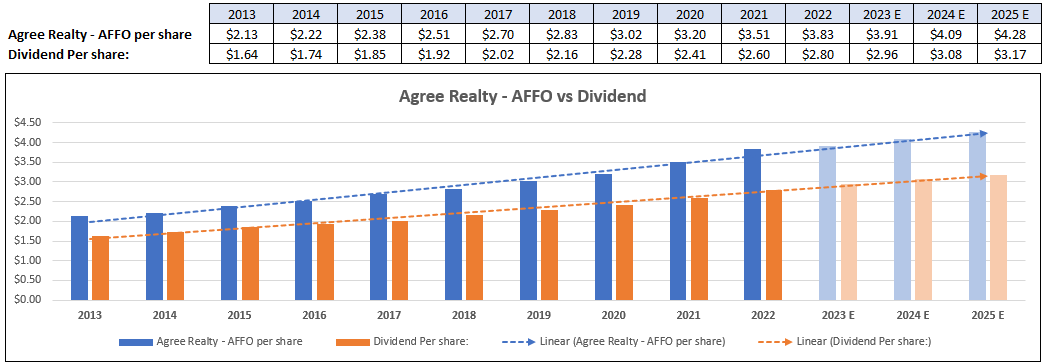

Agree Realty’s adjusted funds from operations have easily covered the dividend since 2013. ADC has averaged a 5.71% AFFO annual growth rate over this time, which has kept pace with its dividend increases. AFFO increased by 9% in 2022 and analysts expect AFFO to increase by 2% in 2023, and then 5% in both 2024 and 2025.

{kind=link}

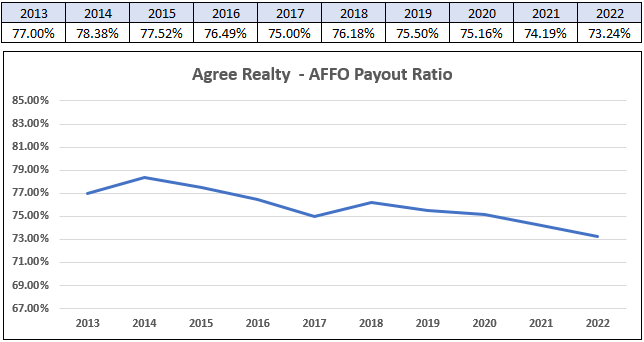

Payout Ratio

Agree Realty has been very consistent with its AFFO payout ratio with it ranging between 73.24% and 78.38% over the last decade. While the payout ratio has been fairly consistent, it has improved since 2013 when it stood at 77.00% vs. the current payout ratio of 73.24%.

As seen in the graph below, their payout ratio has been trending lower and is currently at its lowest level since 2013. This conservative payout ratio gives ADC plenty of room to cover the dividend and provides space for future dividend increases.

{kind=link}

Investor Takeaway

Agree Realty currently pays a 4.35% dividend yield that is very well covered by its AFFO. They have historically delivered strong results in both earnings and dividend growth and I see no reason why they won’t continue to do so.

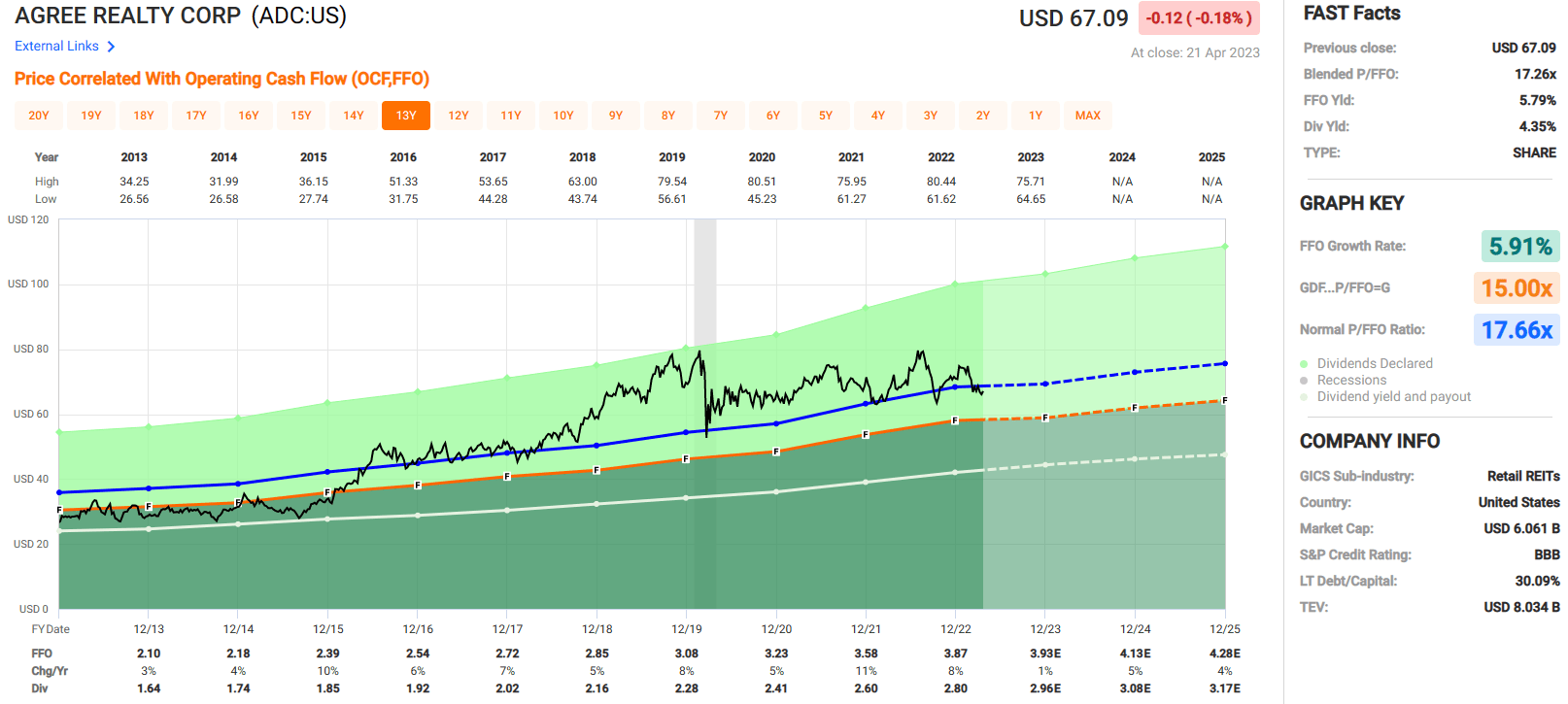

ADC’s dividend is far from a sucker yield and shareholders should have no reason to worry about a dividend cut. The stock is currently trading at a P/FFO multiple of 17.26x, which is in line with its average multiple of 17.66x. At iREIT we rate Agree Realty a BUY.

{kind=link}

VICI Properties ( VICI )

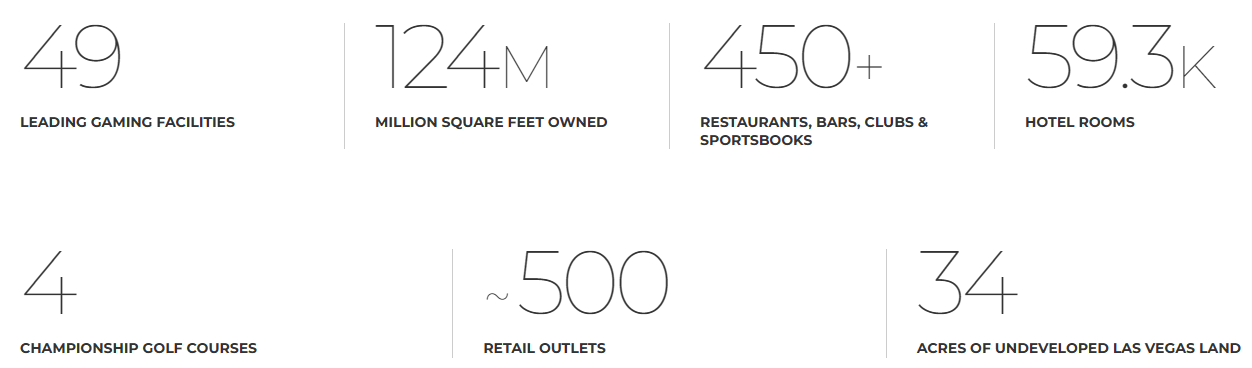

VICI Properties is a triple net lease REIT with a focus on gaming, hospitality, and entertainment properties. VICI focuses on experiential real estate which makes it very resistant to e-commerce. VICI’s portfolio of properties includes well known casinos such as Caesars Palace, MGM Grand, and the Venetian Resort in Las Vegas.

In all they have 49 gaming properties in the U.S. and Canada that cover approximately 124 million square feet and feature around 59,300 hotel rooms and around 450 bars, restaurants, and nightclubs. Additionally, VICI owns 4 championship golf courses and 34 acres of undeveloped land in Las Vegas.

{kind=link}

Dividend

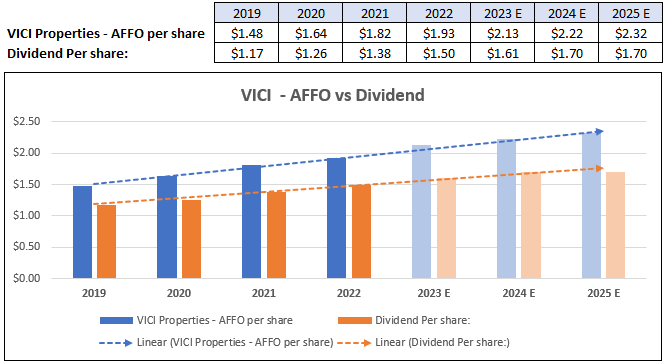

We don’t have nearly the same amount of historical data on VICI as we do with Realty Income or Agree Realty, but from the numbers we have VICI has delivered excellent dividend growth with an average annual growth rate of 10.80% since 2019. Analysts expect the dividend to go from $1.50 to $1.61 in 2023 for a 7.3% year-over-year increase.

FAST Graphs (compiled by iREIT)

Funds from Operations

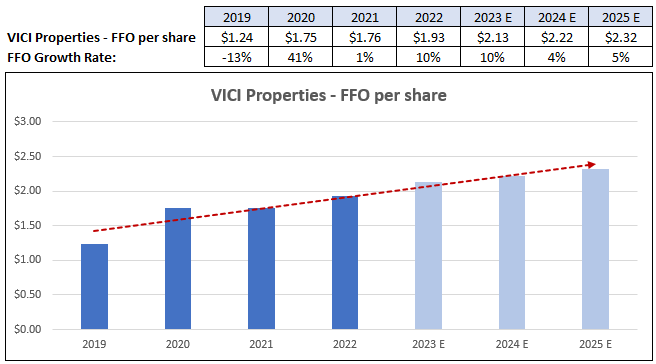

VICI’s funds from operations fell -13% in 2019 but then increased by 41% in 2020. FFO has increased each year since 2020 and increased by 10% in 2022. Analysts expect FFO to increase by 4% in 2024 and 5% in 2025. Since 2019 VICI has an average annual FFO growth rate of 7.16%.

{kind=link}

Adjusted Funds from Operations

VICI’s adjusted funds from operations have covered the dividend each year and have an average growth rate of 7.16% since 2019. Analysts expect AFFO to increase by 10% in 2023, 4% in 2024, and 5% in 2025. The consistency and growth of VICI’s earnings has supported the dividend and all indications point to this trend continuing.

{kind=link}

Payout Ratio

VICI’s AFFO payout ratio increased in 2022 from 75.82% to 77.72%, but since 2019 it has improved from 79.05% to its current level of 77.72%. Even with the slight increase in 2022, the payout ratio is still very conservative and enables VICI to easily cover its dividend and provides room for future increases.

FAST Graphs (compiled by iREIT)

Investor Takeaway

While all 3 companies are net-lease REITs, VICI has a different approach than Realty Income or Agree Realty. The latter two focus primarily on retail properties in industries that are resistant to e-commerce while VICI’s focus is more on experiential real estate that really can’t be replicated online.

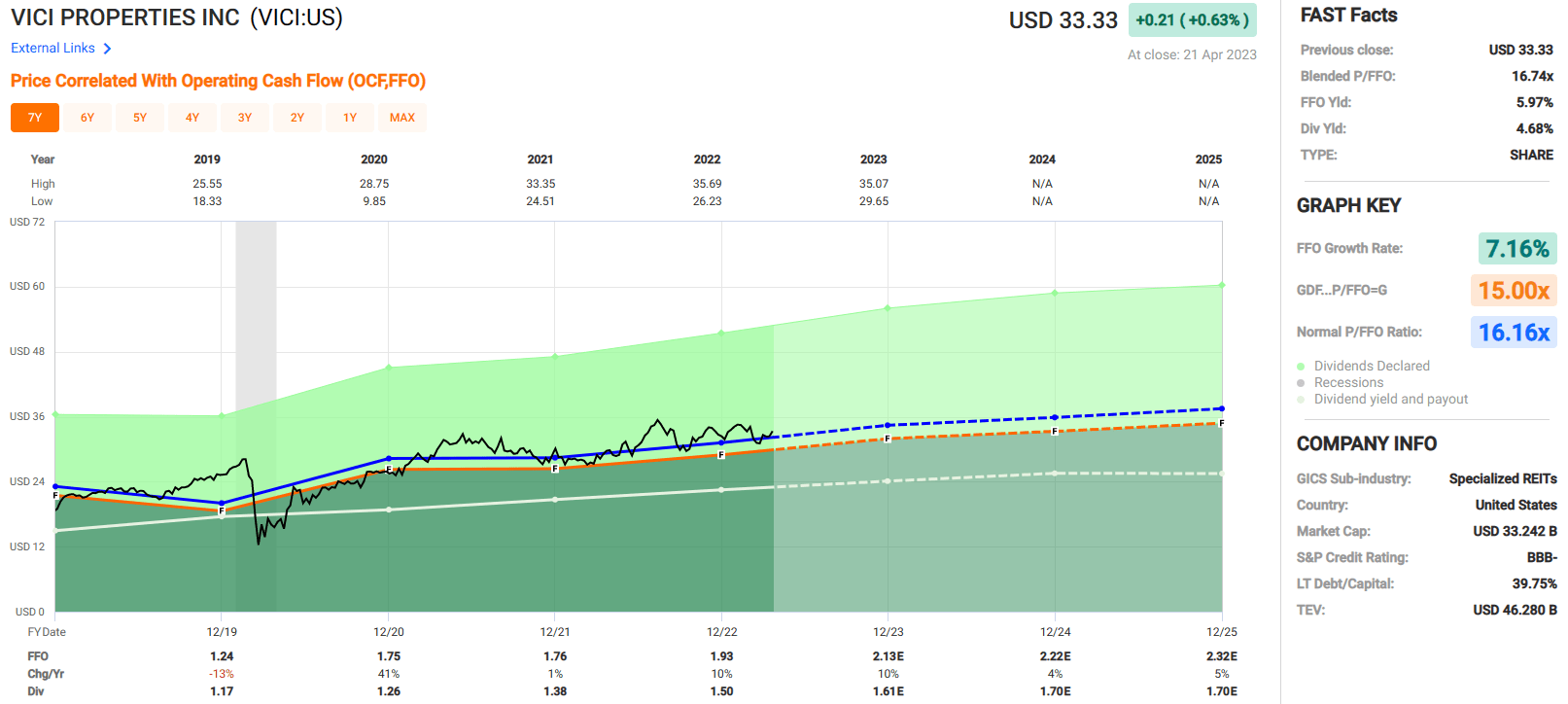

Sure there are online gambling sites, but is that really the same as going to a casino in Las Vegas? Not in my opinion. In its short history, VICI has delivered earnings and dividend growth and has maintained a very reasonable payout ratio. VICI pays a 4.68% dividend yield that is secure and trades for a P/FFO multiple of 16.74x which is just slightly above its normal multiple of 16.16x. At iREIT we rate VICI a BUY.

{kind=link}

In Closing

Real dividend power can’t be calculated by yield, but by overall quality – the kind you can see by studying a REIT's history of dividend payments.

Here are some of the questions you want to ask:

- Has it increased over time?

- How has it funded those payouts?

- Are those methods sustainable enough to continue funding them in the near future?

Looking in the rearview mirror almost always gives clear snapshots of corporate performance and tendencies. And if you see any dividend cuts, it could suggest management isn’t effectively controlling risk.

Again, it’s not always the company’s fault. Sometimes, stuff happens...

My best advice is to stay clear of the “sucker yields” and instead to accumulate shares in REITs like O, ADC, and VICI – all overweight positions for me.

If you’re going to “split 10’s” (using the blackjack analogy) make sure that you limit your hard-earned capital, because the odds are not in your favor…and the house has the best odds (in blackjack the house edge is around 2%, and this is the advantage the casino has over the average player).

Avoid the Sucker Yields folks...

Good luck and Happy SWAN Investing!

For further details see:

Build A Sucker Free REIT Portfolio