BCC - Builders FirstSource: Declining Commodity Price And Housing Demand

2023-09-26 02:14:58 ET

Summary

- Builders FirstSource is facing challenges as the lumber industry bounces back from pandemic disruptions, leading to a decrease in commodity prices and affecting revenue.

- Mortgage rate increases and weakened housing demand are expected to have a detrimental effect on BLDR's revenue.

- The Company's sales have experienced a significant downturn, primarily driven by reduced commodity prices, and its adjusted EBITDA margin has declined as well.

Summary

This post is to provide my thoughts on Builders FirstSource ( BLDR ) business and stock, I recommend a hold rating due to my expectation that I foresee challenges arising as the lumber industry bounces back from pandemic disruptions, causing a decrease in commodity prices and subsequently affecting revenue. Anticipating the Federal Reserve's choice to maintain rates, mortgage rates are likely to remain elevated, diminishing housing demand and having a detrimental effect on BLDR's revenue. The decrease in revenue due to these circumstances has led BLDR to intensify efforts to reduce operational leverage, which is adversely affecting their margins.

BLDR stands as a prominent provider and producer of construction materials, fabricated components, and construction services to professional homebuilders, sub-contractors, remodelers, and consumers. They offer a comprehensive solution to customers by overseeing the manufacturing, supply, and installation of a wide range of structural and associated building products. Over the past five years, BLDR has witnessed impressive revenue growth at a CAGR of 24%. This growth was notably fueled by the exceptional performance in 2021 when lumber prices soared due to pandemic-induced shortages. However, it's unlikely to see a repeat of such exceptional growth since the current lumber prices have stabilized to pre-COVID levels post-disruption. As evidenced in 2022, revenue only increased by 14% year-over-year, falling considerably short of the CAGR. Regarding the adjusted EBITDA margin, it received a boost from the pandemic-induced shortages, where the unusually high revenue allowed BLDR to increase operating leverage, thereby improving margins. With the anticipation of a revenue slowdown, it's expected that BLDR will reduce its operating leverage, consequently leading to a decline in margins.

Investment thesis

In the second quarter of 2023, sales experienced a downturn of approximately 35% compared to the same period last year, amounting to a total of ~$4.5 billion. This decline was predominantly driven by the adverse effects of reduced commodity prices. The core organic sales also saw a significant drop of ~22% year-on-year. The primary contributor to this year-on-year decline was a substantial 31% decrease in single-family sales, partly offset by a notable 30% upturn in multi-family sales and a modest 5% increase in R&R sales. Within the core organic sales, value-added products observed a dip of roughly 20% year-on-year, constituting approximately 53% of the total sales compared to 43% in the second quarter of 2022.

Since the start of 2023, the trajectory of lumber prices has remained relatively stable. However, from the month of July onward, a downward trend has become evident, plummeting from its peak of $534 to the current price of $482, marking a decline of approximately 10%. This low lumber prices can be attributed to the recovery in the lumber supply chain, previously disrupted by the pandemic. As this recovery gains momentum, it is foreseeable that the headwinds from reduced commodity prices will persist, exerting pressure on overall revenue.

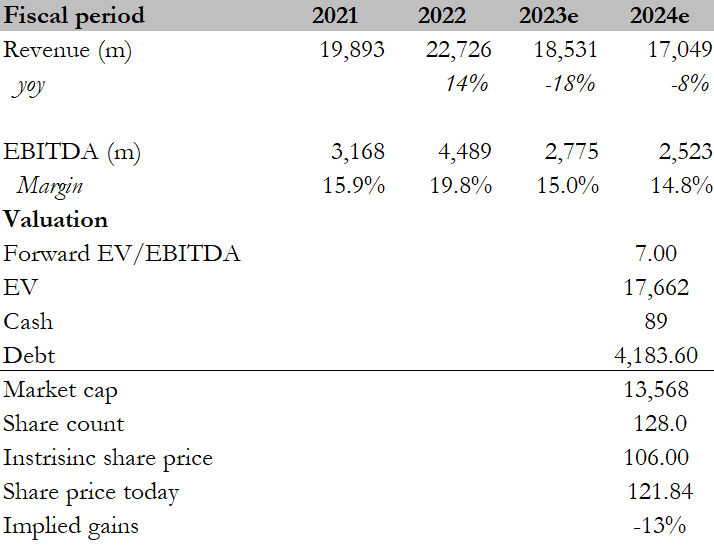

In addition to the rebound in lumber supply, there is a mounting strain on lumber demand due to the declining demand for housing since the start of 2022. As of August 2023, housing demand had reached its lowest point in the post-COVID period, standing at a mere 1.283 million. This figure is the lowest since the Federal Reserve's decision to cut interest rates in response to the COVID-19 recession. Factors such as tightened financial conditions, a surge in mortgage rates, and soaring home prices continue to impede buyers' purchasing power. The recent stance of the Federal Reserve , refraining from raising rates but indicating a likelihood of sustained higher rates, does not bode well for lowering mortgage rates. Consequently, housing demand is expected to linger in a weakened state, negatively impacting BLDR's revenue. This projection aligns with the management's guidance for the fiscal year 2023, where net sales are expected to fall within the range of $16.8 billion to $17.8 billion. This stands in stark contrast to the $22.7 billion recorded in fiscal year 2022, representing a substantial 27% year-on-year decline.

On top of the substantial decline in sales, BLDR reported an adjusted EBITDA of approximately $769 million for the second quarter. The adjusted EBITDA margin also witnessed a decline, settling at 17.0%. This reduction in adjusted EBITDA was primarily driven by lower net sales, including a decline in the sales of core organic products and the deflation of commodity prices. The adjusted EBITDA margin saw a decrease due to the deleveraging of expenses. As previously mentioned, the anticipation of continued weakness in housing demand due to the Federal Reserve's decision to refrain from rate hikes, instead hinting at a prolonged period of elevated rates, will further exacerbate the strain on top-line revenue. With sales weakening due to both weak commodity prices and housing demand, it is expected that BLDR will continue to reduce its operating leverage, consequently compressing the margins. This analysis aligns with the guidance provided by management. The management has guided the fiscal year 2023 adjusted EBITDA to fall within the range of $2.6 billion to $2.9 billion, with the adjusted EBITDA margin falling within the range of 15% to 17%. In 2022, the adjusted EBITDA margin stood at approximately 19%.

Valuation

I believe the fair value for BLDR based on my DCF model is $106. My model assumptions are that as the lumber disruption caused by the pandemic is recovering, I anticipate the headwind on declining commodity prices persistent and continue to put pressure on revenue. The recent indication from the Federal Reserve of a prolonged period of elevated rates does not aid in the reduction of mortgage rates. Therefore, I expect housing demand to remain relatively weak, which will negatively impact BLDR's revenue. In terms of margins, I anticipate that BLDR will continue to reduce its operating leverage, which will have a negative impact on margins as sales weaken due to weak commodity prices and housing demand.

Beacon Roofing ( BECN ) and Boise Cascade ( BCC ) are two of their competitors. BLDR's forward EV/EBITDA multiple of 7.18x is in line with peer's median. While BLDR's EBITDA margin of 19.41% is higher than its peers' median of 17.31%, its leverage ratio (Debt to Equity) of 96.35% is much higher than its peers' median of 84.9%. So, I think BLDR's current forward EV/EBITDA is reasonable. Given the weak revenue and EBITDA margin outlook for BLDR, as mentioned above, I recommend a hold rating.

{kind=link}

Risk

If the pressure on commodity prices continues to worsen, it will drive revenue down even further. If the Federal Reserve increases interest rates due to unexpectedly high inflation, it will mute house demand even further, driving revenue growth even lower.

Conclusion

In conclusion, BLDR faced significant challenges in the second quarter, with a sharp decline in sales driven by reduced commodity prices and a slump in housing demand. The impact on core organic sales and value-added products further intensified the situation. The decline in lumber prices posed a persistent threat to revenue. Additionally, the housing market's weakened state, influenced by the Federal Reserve's interest rate decision, suggests a challenging road ahead for BLDR as the mortgage rate is expected to remain elevated. Management's lowered guidance for fiscal year 2023 underscores these concerns, and it aligns with my lowered expectations and raised caution about future profitability. Given the circumstances, I recommend a hold rating, as investors should be cautious about BLDR's prospects in the current market landscape.

For further details see:

Builders FirstSource: Declining Commodity Price And Housing Demand