MGDPF - Building The Perfect Gold Stock Portfolio

Summary

- While investors can choose to buy a gold stock ETF or the largest producers, I believe a well-diversified basket of quality gold stocks will lead to better performance.

- The objective is to find the best companies with the best prospects in each category, and there are benefits and risks in each category as well.

- Usually, the companies in the "sweet spot" account for at least 50% of the holdings in The Gold Edge portfolio.

- There is a place for senior producers, streaming and royalty companies, and exploration/development stocks.

- Having some exposure to silver is key to building the perfect "gold" stock portfolio.

Gold hit a peak of just over $1,900 back in 2011 and then entered a multi-year bear market, falling to a low of just under $1,100 per ounce by December 2015. Since then, gold has recovered all those losses, driven by incredibly bullish fundamentals, first and foremost, a more than doubling of the money supply in the U.S. (with M2 jumping almost 50% since just before the pandemic) and sharply negative real interest rates. Other supporting factors have also boosted the outlook for the metal, such as declining mine supply (indicating a potential long-term peak in annual gold production), rising central bank demand, the rapidly deteriorating outlook for the U.S. deficit as higher rates increase interest on debt and further add to the total debt, lack of exploration and new discoveries in the gold sector, etc. Fundamentals are telling us gold should head much higher over the next few years and maybe for the rest of the decade. The metal has made two attempts since 2020 to breakout to all-time highs and test a new price range. Both attempts failed. Now, it seems to be making its third attempt, and I don't believe this one will fail-should gold surpass $2,000 again. If it breaches that level, it's likely on its way to $2,500+.

StockCharts.com

There isn't any other sector that's better positioned over the next 5-10 years than gold (and I would include silver in that conversation as well, but that's for another article).

Investors looking for exposure to gold have several options:

1. Physical metal (bars, coins, etc.)

2. Futures

3. ETFs and other gold-backed funds

and

4. Gold mining stocks

Gold stocks provide strong leverage to rising gold prices, as typically, a 10% move in gold translates into a 20-30% move in the miners.

However, over the last few years, we've seen a substantial divergence occur, as the Au stocks have notably underperformed the underlying metal. Instead of ~$1,900 gold, the miners are acting as if gold is at $1,500 or below. The majority of the smaller companies in the sector are trading at just 0.3-0.5x NAV, while the mid to large-cap producers are also priced well below fair value.

The HUI (an index of gold producers) has put in a robust recovery from the lows last September, as it's increased more than 40%. Most gold stocks have seen significant reversals. However, they are still well below the peak seen last year, as the HUI would need to surge another 30% to retest the April 2022 highs. And they are miles below where they traded back in 2011, as the HUI would need to more than double to get back to where it was over a decade ago.

If gold is on the verge of breaking out this year, maybe as soon as this month, then the gold stocks offer investors an opportunity to not only buy these miners at deep discounts to fair value but gain even more upside leverage to rising gold prices than in past bull cycles since the mining stocks are starting from such a low base.

It's quite possible that most stocks in this sector will move up 3-5x from current levels if gold launches to $2,500+, but even sustained prices of $1,800-$2,000 is good enough for a 50-100% increase in most Au stocks, as bearish sentiment was at notable extremes a few months ago and gold companies have only begun to recover.

If gold is about to enter a new phase of the bull cycle, then we are only in the first inning of what will likely be a multi-year run in the gold stocks.

It's why now is a perfect time to discuss what I consider to be the perfect gold stock portfolio.

While investors can choose to buy a gold stock ETF such as the VanEck Vectors Gold Miners ETF ( GDX ) or VanEck Vectors Junior Gold Miners ETF ( GDXJ ), or perhaps, simply load up on the largest producers in the sector-Newmont Mining ( NEM ) and Barrick Gold ( GOLD )-and call it a day, I believe a well diversified basket of quality gold stocks will lead to better performance.

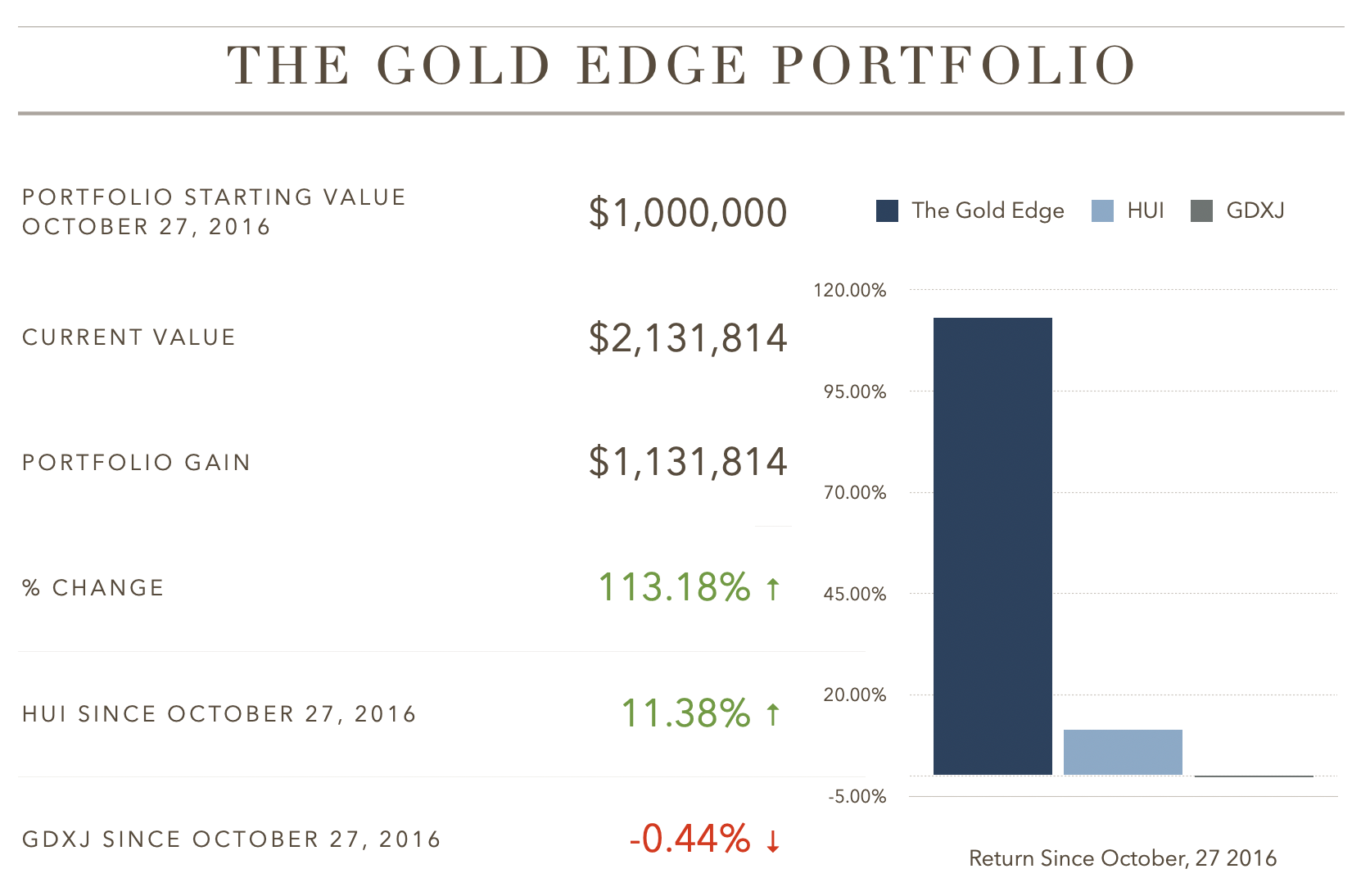

This is evidenced by the performance of The Gold Edge portfolio since its inception until the end of 2022, as while the HUI and GDXJ have gone basically nowhere, the portfolio is up over 100% and has consistently beat the benchmarks. As a side note, there are other factors involved that lead to outperformance in this sector, including knowing how to play/spot the divergences, but I will also save that discussion for another article that I plan to release next week (which will likely be a series or two-parter). So be sure to follow me if you want those sent to your inbox.

{kind=link}

Diversification

The perfect gold stock portfolio starts with a well-diversified portfolio.

Gold mining is capital-intensive and filled with risks and uncertainty. It's not like buying your average Dow stock or trillion-dollar tech stock. Apple ( AAPL ) isn't going to warn that it found a major flaw in the iPhone and will be forced to shut down production, or that its operations in a foreign country were confiscated by the government, or that it was denied permits for a new plant that is key for its future, etc. Now, similar events don't happen to mining companies on a regular basis; that wouldn't be a correct portrayal of this sector. But building a gold mine is a multi-year process that requires many steps along the way, and then operating the mine is an entirely different challenge. Everything has to go right, or at least somewhat right. But occasionally, things don't go right. That's why it's critical to spread the risk across many gold plays, not just one or two.

But let's discuss the definition of "diversification," as much depends on how much one is allotting to this group.

If an investor only wants 5% of their portfolio in Au miners, then it would be difficult (perhaps even foolish) to recommend buying 20+ gold stocks. 5% total exposure isn't going to move the needle enough, and at that point, it's worth taking more risk.

This article isn't for the "five-percenters," but it's still wise to choose at least three or four gold stocks instead of just one, and some of my basic principles of composition discussed below could be helpful for these individuals.

For me, owning a basket of at least 20 gold stocks is ideal. But the concentration of holdings depends on one's preferred exposure level or willingness to own and follow more than a few holdings. The less exposure, then I believe one can get away with a lower concentration, the more exposure, then a higher concentration is best to keep the risk/reward in balance.

I would rather own more gold stocks than less, but too many holdings can lead to a more indexed approach, which will likely impede performance. It's a fine line; the goal is a true goldilocks amount of stocks (not too few, not too many, but just right). What that amount is for each individual investor depends on how much they plan to allocate to this sector.

The Warren Buffet logic of why would an investor buy a stock that's their 20th favorite instead of buying more of his/her top choices with long-term competitive advantages doesn't apply here.

All of these gold companies are producing the same end product and selling it at the same price (roughly). There is no real competitive advantage, and it's all about who is extracting the gold in the most economical way and with the lowest risks (jurisdictional, operational, etc.). There are more than ten gold stocks that fit that bill. I see no reason to place a limit on these options.

Besides, it costs nothing to buy a stock these days. There isn't a strong argument for having less diversification in gold stocks.

Of course, there will be a number 1, a favorite, and a number 10 or 20. That's where the importance of weighting comes in. Proper weighting is determined by the overall risk/reward of each holding. I will go into more detail below as I discuss the different sub-sectors.

The Approach To Composition

There are several sub-subsectors of gold stocks:

- Senior producers

- Small and mid-cap miners

- Streaming and royalty companies

- Micro-cap exploration/development stocks.

The objective is to find the best companies with the best prospects in each category, and there are benefits and risks of each category as well. Let's explore further.

The Sweet Spot

I want to start with the small and mid-cap gold stocks, as those are what I consider to be the sweet spot of the market. What I mean by that is these companies typically offer the best risk/reward and have other favorable characteristics.

While not the traditional definition of a small or mid-cap stock (as the gold stock sector is minuscule compared to the world of trillion-dollar market cap behemoths we now live in), the general market cap range for the companies in this category is ~$500 million to ~$5 billion.

Most are diversified enough and their respective mines have a solid operating track record that the risks are well understood and somewhat mitigated by the number of mines in production.

Typically, they will produce anywhere from 150,000 to 1 million ounces of gold per year, and most are more towards the middle of that range.

They also usually have good liquidity and trade on U.S. and Canadian stock exchanges, making them easily accessible to investors in North America and those abroad that want to invest in foreign securities.

The group is prone to underperform the large-cap senior producers on the downside, but they do the opposite in a gold bull market. What's also appealing about this group is they have first-mover advantage when gold begins to run.

The sector is cyclical, and the individual companies in this sweet spot also go through their own cycles and are impacted more than the senior producers. Often, at any given time, many small and mid-caps have bullish catalysts on the horizon that will make a notable impact on production and cash flow, yet the market typically won't price in these catalysts until after they've hit. So there are always opportunities to gain exposure to companies in this group at compelling discounts to fair value.

The senior producers also go through their own cycles, but the up-cycles typically don't move the needle as they do for their smaller peers.

A 4 million-ounce gold producer with a 500,000-ounce project coming online will get a lift in its share price, all else being equal, but not like a 300,000-ounce producer that's bringing a new 100,000-200,000-ounce gold mine into production.

Most of these small and mid-cap gold companies still have plenty of runway to grow in size and scale, and they haven't come close to hitting their limits yet.

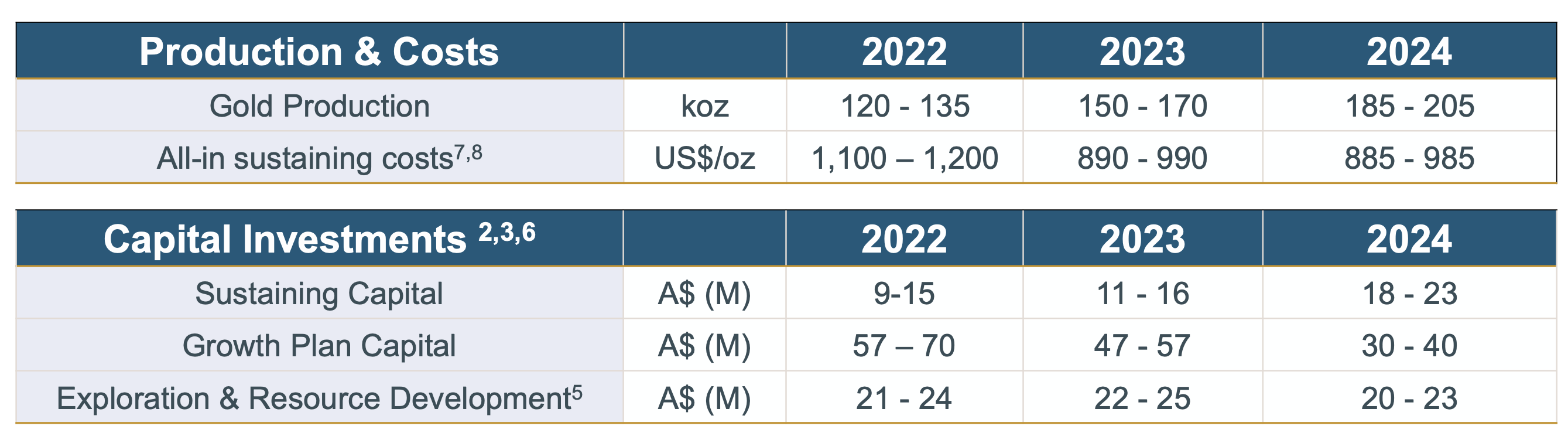

One example is Karora Resources ( KRRGF ), which I discussed in an article earlier this month. KRRGF is on the low end of the market cap range of this group, but the company is growing rapidly in size, as it's estimated that output will climb from ~132,000 ounces of gold production in 2022 (just reported last week) to ~160,000 ounces this year and increase to potentially over 200,000 ounces in 2024. AISC is expected to decline to under US$1,000 per ounce as production rises. You won't ever see a senior producer grow this fast unless they acquire a rival.

{kind=link}

The continued growth of KRRGF and bullish outlook are why the shares have reversed aggressively since the lows and almost doubled over the last three months, which is 3x the performance of the HUI and GDXJ.

Karora isn't as diversified as other small and mid-caps, but there are many other examples.

Usually, the companies in this "sweet spot" account for at least 50% of the holdings in The Gold Edge portfolio (which currently contains 25 stocks).

I pick the best 10-15, looking at all facets (quality of assets, management team, valuation, balance sheet strength, growth, potential bullish catalysts, jurisdictional risk, diversification, etc.), then apply the proper weighting according to where I rank these picks (usually a range of 3-6%, where the lower rated picks get a lower weighting, and vice versa) and use that as my base. Then I build off that base by adding senior producers, streaming and royalty companies, and exploration/development plays to the mix.

Senior Producers

I discussed in a recent article on Agnico Eagle ( AEM ) my issue with simply buying the top senior producers and calling it a day:

As the rebound in gold and the miners gains steam, I'm seeing more pro-gold articles across various financial websites that are recommending investors buy Newmont ( NEM ) and Barrick Gold ( GOLD ). These are the two largest gold producers in the world-both in terms of output and market cap-and they are the go-to names for most investors because of their familiarity and size. Rarely in these articles is there in-depth, compelling analysis of these companies that explains why NEM and GOLD should be purchased, both in general terms and over every other gold miner.

I don't want to call it lazy analysis; I'm quite bullish on Barrick, and Newmont's relative value is now lower after its waterfall decline since last spring. But gaining exposure to rising gold prices isn't about buying the two largest gold mining companies in the world and calling it a day, as that's a plain vanilla strategy and overlooks critical elements that might act as bearish catalysts, leading to underperformance.

I would define a senior producer as any company with output of at least 2-3 million ounces of gold and that has a market cap of $10+ billion. There are several companies in this space that blur the lines between being a mid-cap and senior, but even if you count a few of them in the latter classification, there are still less than 10 companies in total to choose from in this category.

Having a gold stock portfolio overloaded with mostly large-cap senior producers is the surest way to, at best, an inline performance during a bull run and, at worst, an inferior performance if one or two stumble.

There are some very compelling options in this group, but it's critical to be selective and not just choose the biggest. Sometimes the biggest are some of the best options, but that's only half true today (GOLD>NEM).

Again, much depends on how each of these companies is positioned over the short and medium-term, given the combination of production, costs, cash flow, and valuation.

The best-of-the-best in this category is AEM. Production has now increased to ~3.7 million ounces with the acquisition of the other 50% of the Canadian Malartic mine, and it's now the third-largest gold miner in the world. The company checks off all of the boxes, and if I could only own one gold stock, it would be the one I would choose without hesitation. Agnico Eagle is a top pick of mine, but it doesn't account for a significant percentage of my gold stock portfolio.

{kind=link}

Typically, I have 3-4 seniors at max in the portfolio and usually at no more than 15-20% of the total weighting. Anything higher, and I run the risk of performing in line with GDX and the HUI.

Gold Streaming And Royalties Companies

When it comes to generating long-term shareholder value, there is no better sub-category than the gold (and silver) streaming and royalty companies. If you take the three largest in the space-Franco-Nevada ( FNV ), Wheaton Precious Metals ( WPM ), and Royal Gold ( RGLD )-and compare their respective 10+ year performance against the rest of the sector, the difference in returns is night and day. FNV has been the stalwart of the group, having increased by 250% since 2011, while the HUI is down over 50%.

Streaming and royalties companies gain exposure to mines by purchasing a percentage of production at a fixed cost, and so they don't have the same risks as the producers since they don't operate mines, develop projects, or explore for gold. As a result, they aren't subject to the inherent capital risks of this sector like producers. Such things as cost overruns on a project, higher than expected all-in sustaining costs, inflation, etc., have no impact on the streamers/royalty companies as they're not responsible for any CapEx, and their costs are set from the onset.

FNV, WPM, RGLD, and others in the category are also incredibly well-diversified and own dozens and dozens of producing streams and royalties. Or, in the case of FNV, it owns over 100 assets that currently generate cash flow.

The problem with the group is:

1) They almost always trade at an aggressive premium to fair value, as optionality, low risk, ~80% margin, dependable cash flow, etc., get baked into the cake.

2) They typically don't outperform during bull cycles precisely because of their already elevated valuations, as most producers are trading well below fair value at the start of a bull market. Since the lows last September, GDXJ has outperformed this trio, and FNV has been a clear laggard.

There are certain times when the risk/reward in the larger cap streaming/royalty companies becomes compelling, but it's the smaller peers that have been the clear values lately. That's been my focus over the last year or two.

If I find an undervalued streaming/royalty play with a well-diversified portfolio of quality assets, it's time to buy aggressively.

An example would be Maverix Metals ( MMX ), which I bought last year because of its underperformance, plethora of premium quality producing assets and near-term growth projects, and valuation. MMX recently announced it's being acquired.

Usually, I will have 1-2 streaming/royalty stocks in the portfolio, possibly more if there is better value in the group, but that's rare.

While I find the business model tremendously appealing as an investor, the lofty valuations have been an impediment.

Still, I think owning at least a couple of the more fairly valued streaming/royalty stocks is the right strategy and part of a perfect gold stock portfolio, and I typically have 5-10% exposure to this category.

More Alpha

Gold exploration and development stocks are by far the riskiest category, but they also can generate substantial returns, especially in bull markets. During bear markets, they can decimate a portfolio.

Exploration companies that drill for gold deposits require a constant stream of fresh capital. Since it takes years to drill and define a mineable deposit and most explorers fail to find anything of significance, taking on debt is not an option because nobody will provide debt financing to an explorer since the chances of getting repaid are practically nil.

Explorers always have to keep advancing their projects, and shareholders are the ones who keep footing the bill.

During bear markets, exploration stocks are the worst performers on average, as they have zero cash flow and continue to dilute their stock. It can turn into a vicious cycle as these companies end up needing to do equity offerings after their stock has lost considerable value, which means less money can be raised at the same cost (i.e., amount of shares) as before.

Exploration stocks also don't have much liquidity/volume and are thinly traded issues, often without a listing on any major U.S. exchange. A fund or investor looking to sell a substantial amount of shares can create a freefall in the stock because there aren't enough buyers on average to soak up all of these shares hitting the market.

Bearish sentiment usually hits these stocks the hardest, and at the end of a down cycle, it's not uncommon for the explorers to have lost 70%, 80%, or even 90%, of their value from the top.

During bull markets, the exploration stocks come alive again, and many eventually make up for their underperformance and begin to notably outperform. It's common to have stocks in this sub-sector increase by several hundred percent on average and possibly even increase by 1,000%+ for some.

However, in the early stages of a bull market, the explorers typically lag well behind the small to large-cap producers. Which is what we are seeing happen now.

I'm always careful about how much exposure I have to explorers. Anybody overloaded with exploration stocks over the last few years has likely suffered tremendous losses-unless they had one or two big winners to bail them out.

Over the long-term, a strategy focused mostly on exploration stocks is a losing strategy, or a Vegas-like strategy where it's more high-risk gambling than a sound investment plan. Some could win, most will lose, and big.

The way I approach explorers is I consider them more "sprinkle-in" options and will pick a few that I think have the best chance of becoming developers and actually getting their projects built. That typically means avoiding early-stage explorers that don't have many successful drill intercepts and focusing on the ones that have already made a discovery but are still defining the deposit(s).

The advanced-stage developers are risky but much safer than an exploration company still drilling targets. I prefer developers that already have at least a Preliminary Economic Assessment (PEA) on their project, as that gives me a rough idea of the output and economic potential of the asset. The ones in the more advanced state that have completed Feasibility Studies are the most de-risked, and it's a group I usually don't mind weighting higher in the portfolio.

One example would be Marathon Gold ( MGDPF ), which plunged 70% last year but is well-positioned for a recovery, as I discussed in a recent article . I feel more confident weighting MGDPF heavier than other exploration/development plays as the company is now constructing its Valentine Gold mine in Newfoundland, Canada, and trading at a deep discount to fair value, but it's vital to not get too aggressive on stocks like this as the risks are still high and extremely negative news could result in another 70% plunge.

A perfect gold stock portfolio will contain at least a couple of exploration/development plays. However, in the current bull cycle, this category of gold stocks has become immensely undervalued (you have some explorers where the land alone is worth their market cap), and I have more exposure to this group than normal. Usually, I will hold 2-3 from this group at a 10% weighting; now, I have 5-6 at a ~20% total weighing.

What About Silver Miners?

Silver has slightly different supply/demand characteristics compared to gold, as silver is both a precious metal and industrial metal. However, in a gold bull market, the duo moves higher in tandem, and silver always outperforms by a wide margin during the later stages.

Unfortunately, there aren't many quality silver mining stocks like there are gold, as silver is often a by-product credit that is produced by some of the largest base metal and gold mines in the world.

There are very few pure-play silver miners, and on average, the quality of this group is sub-par.

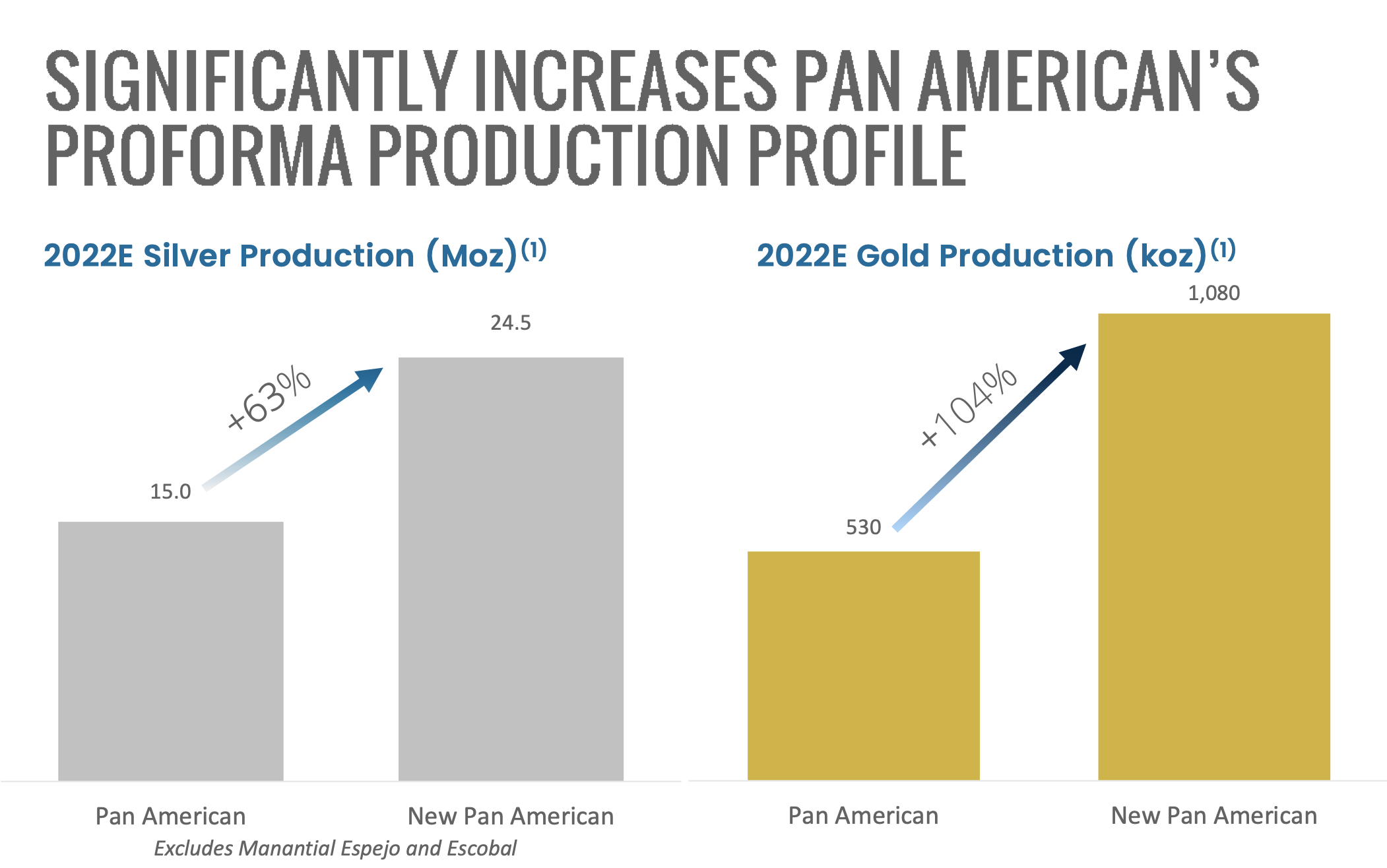

Still, I think having exposure to silver is key to building the perfect "gold" stock portfolio. The good news is many of the gold stocks in the sweet spot of the market discussed earlier also produce substantial amounts of silver. The best example is Pan American Silver ( PAAS ), which, thanks to the acquisition of Yamana Gold's ( AUY ) South American assets, will be producing over 1 million ounces of gold and 25 million ounces of silver annually. PAAS also has the Escobal project that could increase silver output to 45 million ounces per year. The company is already a top 10 silver producer, and it gives investors the best of both worlds.

{kind=link}

WPM also has sizable exposure to silver.

And some of the more interesting developers at this time have strong exposure to silver as well.

I don't view silver exposure on a 100% basis. Meaning I'm not trying to count all of the ounces that each company produces and arrive at an ideal weighting from that data. Rather, my aim is for ~25% of the holdings in the portfolio to have some exposure to silver and provide notable leverage to rising Ag prices. There are times when silver becomes more undervalued/overvalued relative to gold, and it's worth increasing/decreasing exposure to silver.

In Summary

A well-diversified, properly weighted portfolio of gold stocks should outperform the benchmarks and is a better way to approach this sector than buying a gold mining ETF or a few of the large-cap names.

When it comes to composition, the small and mid-caps, along with value streaming/royalty stocks, are there for their typically solid outperformance during gold bull cycles and provide a sturdy base, a few of the best-positioned seniors are there for added strength and stability, and the most promising exploration/development stocks are there for more alpha. Silver exposure is intertwined for extra leverage and outperformance potential.

One doesn't need to load up on highly speculative explorers to generate outsized returns. It's about finding the right balance of risk/reward and understanding the dynamics of these sub-sectors.

For further details see:

Building The Perfect Gold Stock Portfolio