TTEK - Bullish Outlook For Copper: Navigating Asymmetric Supply-Demand Dynamics In The Future

2023-03-20 11:00:00 ET

Summary

- Global demand for copper is set to increase, as emerging markets and western nations are looking to become less dependent on fossil fuels and invest in green energy.

- Copper demand is still relatively high but has slowed especially in China.

- Supply is tight, and a cap between what is needed for the green transition and current possible copper supply exists.

- A feasible chance exists for copper to hold andeven increase from its current $4/lb price.

Investment Thesis

A potential supply shortage could be vital to supporting high copper prices in the 2020s. Essential copper-producing countries such as Chile and Peru have either flatlined their production or are on a decline, which can be a significant roadblock in the mission to meet demand in the coming years. Establishing new copper is a high-cost, time-consuming task; thus, existing copper mines and development projects are likely to play a critical role in the future of copper pricing.

In this article, we will explore the key factors set to drive demand in the coming years and the challenges seen on the supply side of the global copper market and argue for a bull case for the price of copper. We will, in future articles, analyze several copper-mining and producing companies.

Copper Plays a Leading Role in The Green Energy Transition

The transition towards clean energy requires a significant number of materials. These materials include critical minerals such as lithium, cobalt, nickel, copper, steel, cement, plastics, and aluminum. For example, copper is essential in various infrastructure technologies, including wind turbines, electric vehicle batteries, and electricity grids.

In addition, copper stands at the heart of the green transition and the advancement of emerging markets and the entire globe, making it an indispensable element. For example, the EU has recently set a goal to become a Net Zero Emissions (NZE) continent by 2050 . As a result, demand for copper is projected to increase by a CAGR of approximately 4.9% from 2022 to 2030 as clean technology deployment is expected to fire on all cylinders.

To fulfill the ambitious net-zero goals, the mining capacity for copper must expand rapidly. However, while anticipated investments will yield significant gains, they will still fall short of the global NZE Scenario requirements by 2030. Moreover, constructing new mines are lengthy and uncertain process; hence an investment of approximately USD 360-450 billion will be required , mainly over the next three years, to bridge this gap.

We have already seen the first signs of strong demand for copper. For example, the price of copper exploded after the COVID-19 lockdowns back in 2020, as the reopening of major economies and stimulus packages from world governments gave global demand a breath of fresh air. As a result, the price of copper was able to sustain a level of $8,800 - $10,300 per ton for most of 2021 and H1 2022. The question is whether these prices are sustainable in the future, and some arguments could support such a case.

In the next section, we will look at three key drivers behind the demand for copper. These include the green transition in the west, higher demand for electric vehicles and plans for sizable infrastructure projects in China and the US.

The Key Ingredient in EVs, Green Energy, and Infrastructure

Europe's NZE project is not unique in any sense of the word. The largest economies in the west are determined to decrease carbon emissions by reducing their dependence on fossil fuels and, instead, utilizing renewable energy sources such as wind turbines and solar panels. These aspirations require a tremendous amount of copper to realize.

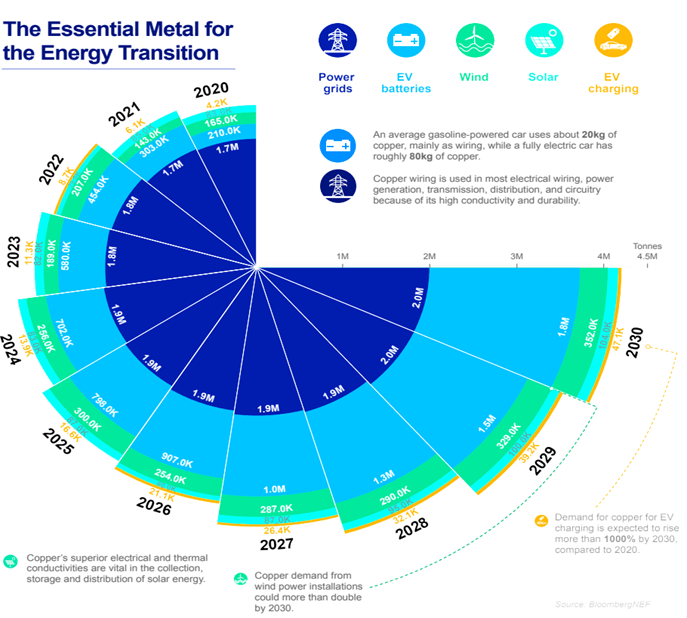

Copper's uniquely low resistivity , sets it apart as one of the finest and simplest materials for electrical conductors. Teck Resources ( TECK ) estimates that demand for EV batteries will drive the demand for copper, especially considering a fully electric vehicle uses approximately four times the amount of copper of a gas-powered car. As estimated by Teck, the projected demand for copper used in the construction of power grids, EV batteries, windmills, solar panels, and EV charging stations is presented in the image below.

Projected Copper Demand 2020-2030 (Teck Resources)

{kind=link}

The rapid shift towards clean energy globally has created a surge in demand for green technologies, leading to an increased need for copper. Renewable energy facilities, on average, require 8 to 12 times more copper than traditional power generation from fossil fuels. the supply prospects for copper in the coming years fall significantly short of the demand. Constructing new copper mines usually requires over a decade, and the recent slump in commodity prices has dampened investment enthusiasm.

According to Kate Southwell from Pala Investments, which specializes in raw materials essential for decarbonization, this shortfall will significantly affect the development of energy transition infrastructure such as EVs, wind turbines, and charging stations. Copper is indispensable in these applications, and substitution is not easy, which will likely lead to cost increases ultimately borne by OEMs and consumers.

This move is expected to boost the rapidly growing electric vehicle (EV) industry, potentially increasing its market share to as much as 20% by 2025 . The market share of EVs has been steadily growing, going from less than 3% in the first half of 2021 to around 6% in 2022. Given that this trend continues in the following years. Furthermore, it is estimated that the average electric vehicle requires around four times as much copper as a conventional internal combustion engine vehicle. In addition, renewable energy projects such as wind and solar power also require significant amounts of copper for their infrastructure.

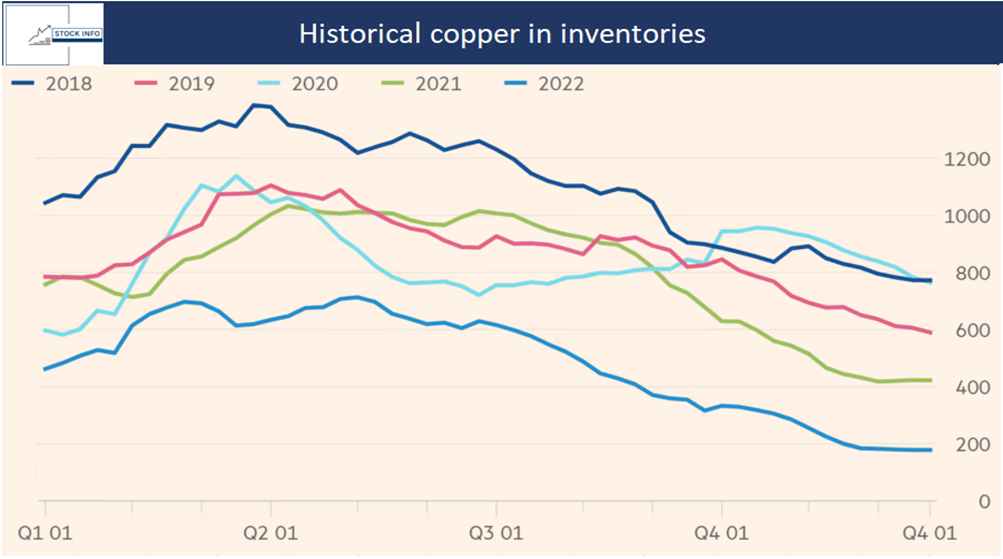

In addition, Trafigura, a commodities trader firm, warned that global copper stocks fell to dangerously low levels in October 2022, with inventories expected to cover only 2.7 days of consumption by the end of the year. Limited inventories increase the risk of a sudden price spike if traders rush to secure supplies. As can be seen in the image below, it becomes evident just how low inventories are in 2022 compared to the previous 4 years.

Historical Copper In Inventories (Stock Info with Financial Times)

{kind=link}

In addition, there have been indications that the demand for copper may be decelerating, as evidenced by the companies by country's recent exportation of copper to LME depots as of early march 2023. Nevertheless, this could only be a temporary phenomenon because of China's slower-than-expected rebound in domestic demand.

According to sources familiar with the matter, Chinese copper smelters have been ramping up production to take advantage of the favorable export environment. Reportedly, the government has loosened export restrictions to boost economic growth. The surge in copper exports from China could significantly impact the global markets, particularly copper prices.

However, the move could also have negative consequences for Chinese manufacturers, who may see a rise in the cost of importing copper because of the increased exports. In addition, it could also exacerbate tensions with other major copper-producing nations, such as Chile and Peru, which could see a decline in demand for their copper exports due to the unexpected exports from China. In short, according to the Bloomberg article, copper inventories are prominent in China but thin everywhere else, and Chinese demand has been weak enough to let Chinese smelters export their goods to the western inventory sites.

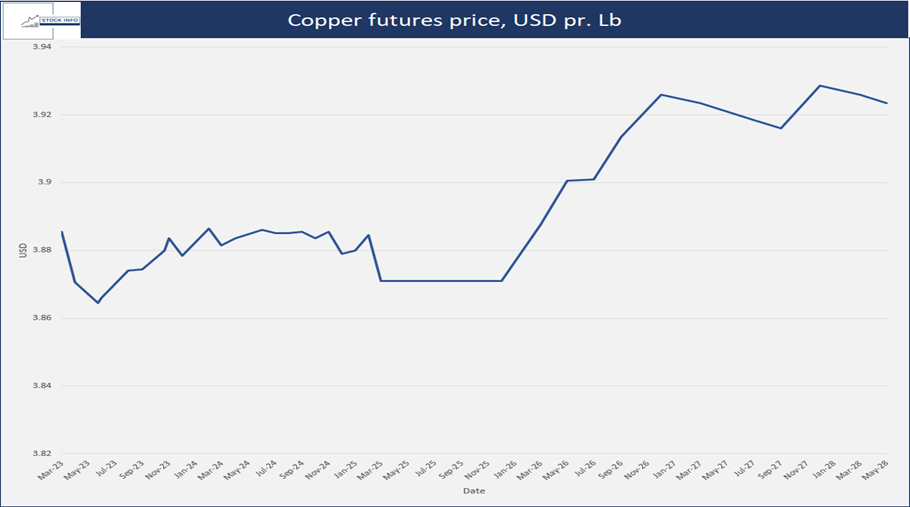

Looking at how the market currently prices copper, shown in the chart below, it is now pricing in decline in copper prices until around the beginning of Q3 2023; whereafter it starts to increase again. Furthermore, in H2 2025, the market prices copper at around the same as May 2023, but then increases sharply from 2026 and beyond.

{kind=link}

A great opportunity may lie in the likely mismatch between futures pricing and global inventories. The fact global inventories currently sit at around 3 days' worth of inventory could mean, that an unexpected rise in demand could push the price of the futures up quite significantly. We, therefore, advise investors looking for an opportunity to enter the copper market to observe global inventory data closely.

Tightness on the supply side.

As the world embraces electric vehicles, renewable energy, and other green technologies, the global copper industry has witnessed an unprecedented surge in demand. As a result, there has been a significant increase in the number of greenfield copper projects worldwide, which are expected to contribute to the growing demand for copper.

Greenfield projects refer to new mining projects developed from scratch, as opposed to brownfield projects, which are expansions or upgrades of existing mines. According to industry experts, greenfield copper projects are essential to meet the growing demand for copper, which is expected to rise by around 2.5% per year over the next decade.

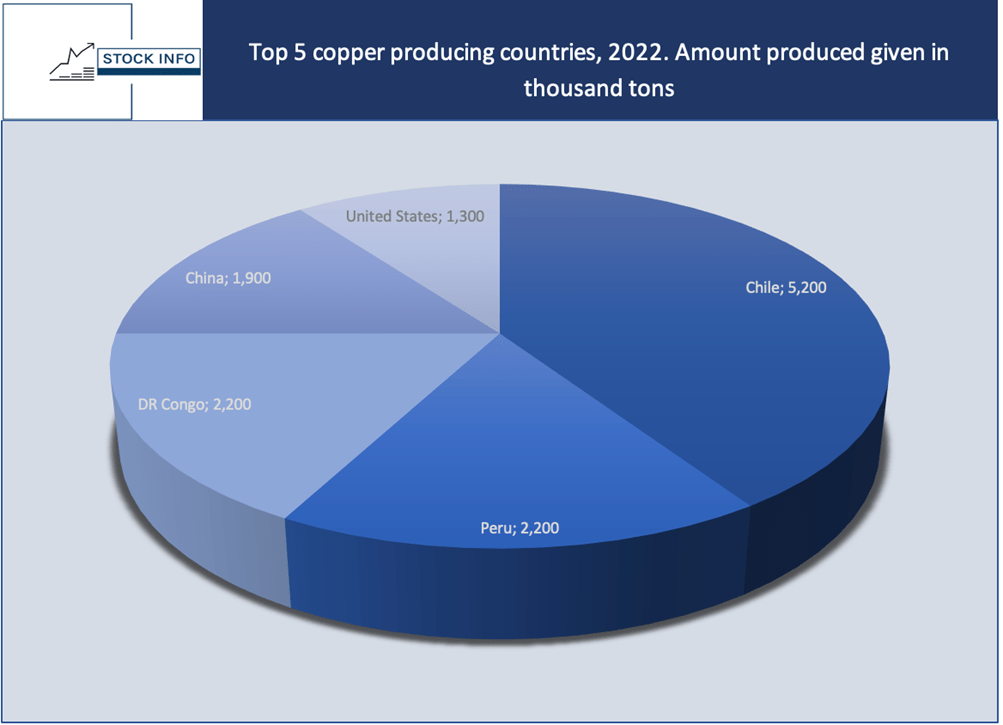

As of 2022, Peru and Chile were the top two copper-producing nations in the world, producing 5.2 and 2.2 million tons of copper, as seen in the chart below.

Top 5 Copper Producing Countries (Stock Info)

{kind=link}

Chile and Peru accounted for approximately 27% of global copper production in 2022; hence copper production is heavily concentrated in these two nations. However, south American copper producers face many challenges in the current regional political climate. This includes widespread protests in Peru, the risk of an increase in the tax rate for copper producers in the South American region, and various environmental regulations, which all pose a threat to their operations and hence possibly profits.

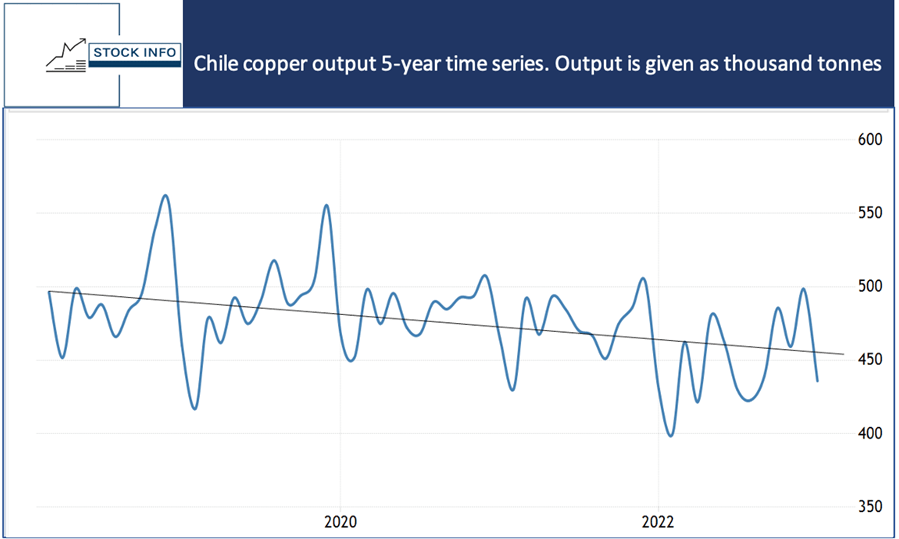

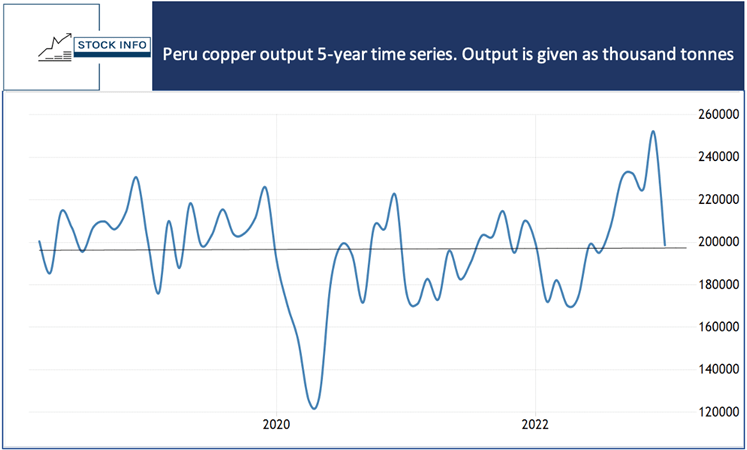

As a result, these risk factors have started to present themselves in the countries' output, either on a declining trend or trending flat, as shown in the charts below.

Chile Copper Output Over The Last 5 Years (Stock Info) Peru Copper Output Over The Last 5 Years (Stock Info)

{kind=link}

{kind=link}

There are still several new greenfield copper projects being developed worldwide, with the most significant project being the Quellaveco copper mine in Peru , developed by Anglo-American ( AAUKF ) and Mitsubishi ( MSBHF ). The mine is expected to produce 300,000 tonnes of copper annually, making it one of the world's largest.

Other notable greenfield copper projects include the Kamoa-Kakula project, which is a joint venture between Ivanhoe Mines ( IVPAF ), Zijin Mining Group ( ZIJMF ) in the Democratic Republic of Congo, which is expected to produce 800,000 tonnes of copper per year, and the Oyu Tolgoi mine from Rio Tinto ( RIO ) in Mongolia, which is expected to produce 560,000 tonnes of copper per year. These projects and several others are expected to increase global copper production over the next decade significantly.

However, greenfield projects are not without their challenges. For example, developing a new mine from scratch can be complex and costly, requiring significant investment and a range of technical expertise. In addition, greenfield projects often face environmental and social challenges, such as land use conflicts and opposition from local communities. Below you can see an image of the Rosemont Greenfield Mining Project by Tetra Tech ( TTEK )

Rosemont Greenfield Mining Project (Tetra Tech Investor Presentation)

{kind=link}

Mining companies are increasingly adopting sustainable and responsible practices to address these challenges, such as minimizing their environmental footprint and engaging with local communities. The International Copper Association ((ICA)) has also developed a sustainable copper program to promote responsible mining practices and sustainable development in the copper industry.

Despite the challenges, the outlook for greenfield copper projects is positive. This is because they are essential to meeting the growing demand for copper in the coming years. In addition, developing these projects is expected to create significant economic benefits for the countries where they are located, including job creation and increased investment.

Thus, the global demand for copper is increasing rapidly, driven by the adoption of green technologies such as electric vehicles and renewable energy. Developing greenfield copper projects is critical to meeting this demand, and several significant projects are currently in action worldwide.

To sum up, regarding the supply-demand dynamics we see in the copper market today, we believe that significant tailwinds exist for copper that can push the price higher than it currently sits at or provide a comfortable level of support. According to S&P Global's ( SPGI ) estimates, the global copper supply will fall short by 1.6 million tonnes in 2035, and the shortfall will start to become significant during this decade. In a worst-case scenario, the deficit may increase to 9.9 million tonnes in 2035 . Although market analysts hold different opinions on future prices, supply, and demand, there is a consensus that the supply shortage will emerge around 2026. We, therefore, see a strong bull case for copper in the coming years.

Major Players Who Could Stand to Benefit

Although several companies with exposure to copper production in Chile and Peru, we identify three companies with the potential to benefit from the supply-demand gap in the coming years.

The first one is Teck Resources ( TECK ), which ended 2022 with $7.23B in EBITDA and forecasts their revenues upwards of $11.57B in 2023 alone and around $2.9B in free cash flow. This would mean they currently trade at roughly 7x the projected free cash flow. Furthermore, TECK aims to return 30% of its free cash flow to shareholders and may consider a special dividend, but the author believes that TECK Resources will prioritize share repurchases over dividends. This makes them an attractive investment opportunity under current market conditions.

Secondly is Freeport-McMoRan ( FCX ), which generated $1.6B in free cash flows in 2022. The company plans to create approximately $7.2B in operating cash flows in 2023 with a targeted copper price of $4/lb. The company plans to spend $3.4B on capital expenditures in 2023 and has the potential to return cash to shareholders while still investing in new copper capacity. FCX's variable dividend payout and discretionary capital spending provide financial flexibility, and the company has the potential to benefit from higher copper prices in the future, with a potential adjusted EBITDA of up to $15 billion if copper prices rise to $5/lb, which is entirely possible given future dynamics on the copper market.

The third is a small junior mining company, AbraSilver Resources ( ABRA:CA ). ABRA's appeal lies in their up-and-coming copper mining projects, La Coipita and the Arcas project, which we discussed HERE . Both mining sites are located in Argentina on the border with Chile, in a region with proven high-quality copper. They have already reported the results of initial drillings in La Coipita, which showed extensive deposits of high-grade copper. Based on their presentation from March 2023, the company currently sits at a market capitalization of around C$162M with approximately C$15M in cash. While their size is minuscule compared to other players on the market, their ongoing projects make them highly interesting, given the tight the copper market supply is estimated to be.

Concluding Remarks

In conclusion, the global copper market is facing potential supply shortages, as key copper-producing countries such as Chile and Peru are either flatlining production or on a decline. Establishing new copper mines is a high-cost and time-consuming task, and therefore, existing copper mines and development projects are likely to play a crucial role in the future of copper pricing. The transition towards clean energy and emerging markets are set to drive up demand for copper for the foreseeable future. For the EU and other modernized nations to fulfill their ambitious net-zero emission goals, the mining capacity for copper must expand rapidly, and an investment of approximately USD 360-450 billion will be required over the next three years. The market currently prices copper in decline until the beginning of Q3 2023, when it starts to increase again.

However, several risk factors may affect copper production in South America, such as political instability, tax rate increase, and environmental regulations. Despite market analysts holding different opinions on future prices, supply, and demand, there is a consensus that a supply shortage will emerge around 2026. Therefore, we believe copper has a strong bull case in the coming years, with TECK, FCX, and ABRA having the potential to capitalize on these market dynamics.

For further details see:

Bullish Outlook For Copper: Navigating Asymmetric Supply-Demand Dynamics In The Future