VTI - Bullish Sentiment Is Too High Going Into Recession: Sell VTI (Rating Downgrade)

2023-12-18 22:38:41 ET

Summary

- I am worried the recent spike in U.S. stocks will translate into higher short-term interest rates in the first half of 2024 and a weaker economy by the second half.

- Investor sentiment is reaching for unsustainably bullish extremes, long-term stock market valuations remain stretched, while a Dow Theory sell signal has been hit.

- A contrarian trading stance may now be the correct course of action. I am downgrading ETFs like the Vanguard Total Stock Market ETF to Sell.

I have wavered between a negative to neutral view of the U.S. stock market's immediate direction during 2023, happy to hold a hedged portfolio and lots of cash earning 5%. Mind you I have refrained from being net short the market. I do own large gold/silver bullion holdings, a few bonds, and some exposure to REITs and oil/gas. This design has allowed me to earn a decent gain on the year, following my own investment path.

What I did not foresee or participate in was the Artificial Intelligence [AI] craze move in Big Tech names, especially the Magnificent 7. In fact, I am very bearish on this group going forward, as a likely recession (credit/banking contraction is still ongoing) and remaining high short-term interest rates (as investment competition) are not factored into them properly during December. You can read a number of my articles since summertime explaining the exact logic.

Over the last week, U.S. stocks spiked again, led mostly by smaller cap names previously lagging all year. In my view, this rally almost guarantees high short-term interest rates will be the norm until a recession hits. With 4% core inflation rates well above the 2% Federal Reserve bank target, pumping the stock market to 52-week highs and the Dow Industrials to all-time highs may be bad news for the economy during 2024, not good news. If the Fed wants to keep the U.S. dollar from collapsing and inflation spiking above 4% again next year, they CANNOT lower interest rates anytime soon, definitely not the March timeframe now priced into the Fed Funds futures market.

To achieve the new soft-landing, low-inflation environment goal (which is a goalpost move vs. the banking policy explanations in 2022), I have been screaming all year the Fed needed to keep the equity market from rising. Early in the year, I even suggested increasing the margin requirement on stock borrowing to curb speculation (changing rules for the first time since the 1970s). The idea was you wanted to prevent a big jump in consumer/business equity wealth. If you honestly want lower inflation and less consumer spending, you don't pump stock prices with dovish predictions of declining short-term interest rates in 2024 with your dot plot, like was done last week by Chairman Powell . The positive "wealth effect" is now preparing to pull inflation higher, not lower.

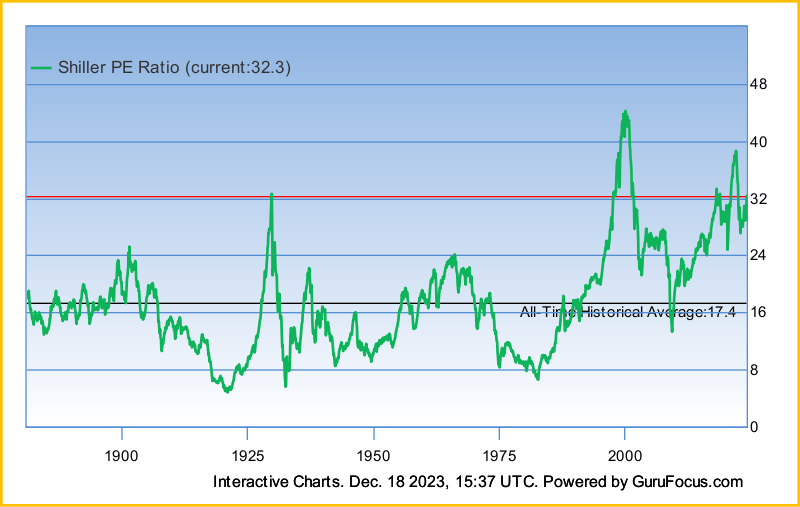

Of course, the Fed did not take my advice (they rarely do). So, we now have a stock market elevated well past its long-term worth on 10-year CAPE valuations or the value of all U.S. stocks vs. GDP output. Where do we go from here? The odds increasingly are stacked against another big upmove during 2024, unless completely irrational exuberance is the new normal from investors, while economic growth pumping by the government is approaching to prop things up into the important 2024 election cycle. Remember, both outcomes would increase the risks inflation will turn higher.

GuruFocus - Shiller CAPE P/E, Since 1880

{kind=link}

We have been teetering close to recession all year, given any type of major negative catalyst event rocking the boat too much. Luckily for the powers that be, bearish developments have been contained, like the regional bank runs of March-April, the continuing Russia/Ukraine war, escalating war in the Middle East since October, etc. The question is, will this luck run out in 2024?

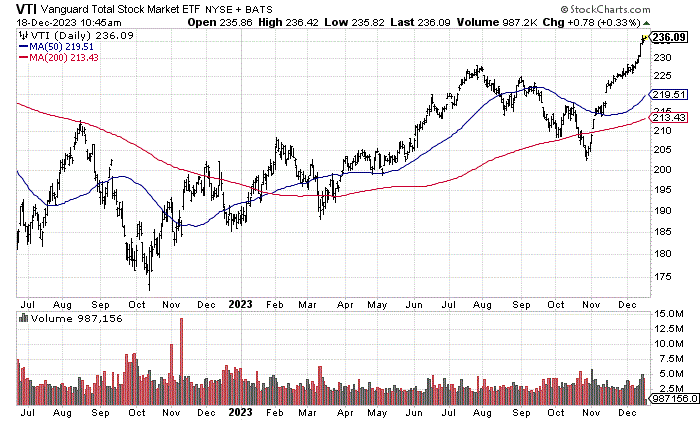

My summary is investors have discounted plenty of good news yet to play out. Let me explain the nearly euphoric investor expectation for 2024 (which will have difficulties improving from today), and why now is a smart time to take the contrarian stance, with a downgrade to ETFs like the Vanguard Total Stock Market ETF ( VTI ) from Hold to Sell. My last VTI article here correctly warned of a meaningful selloff during September and October.

StockCharts.com - Vanguard Total Stock Market ETF, 18 Months of Daily Price & Volume Changes

{kind=link}

Equity Investors Are Overly Bullish

The newest issue that is pushing my stock market view over the next 3-6 months back into bearish territory is investor sentiment has popped to unsustainable levels. Everyone has jumped back into the pool over the last 7 weeks, with a wonderful +10% to +20% upmove in most names. Everywhere I read this weekend, optimism reigns supreme in the financial media.

Gone are the prudent and balanced articles of October explaining stocks don't usually bottom until AFTER a recession. The Pollyanna sentiment of investors today is don't worry, be happy - the stock market always rises (regardless of recession risks, still high inflation and interest rates, record debts in the global economy, or a world slipping into war).

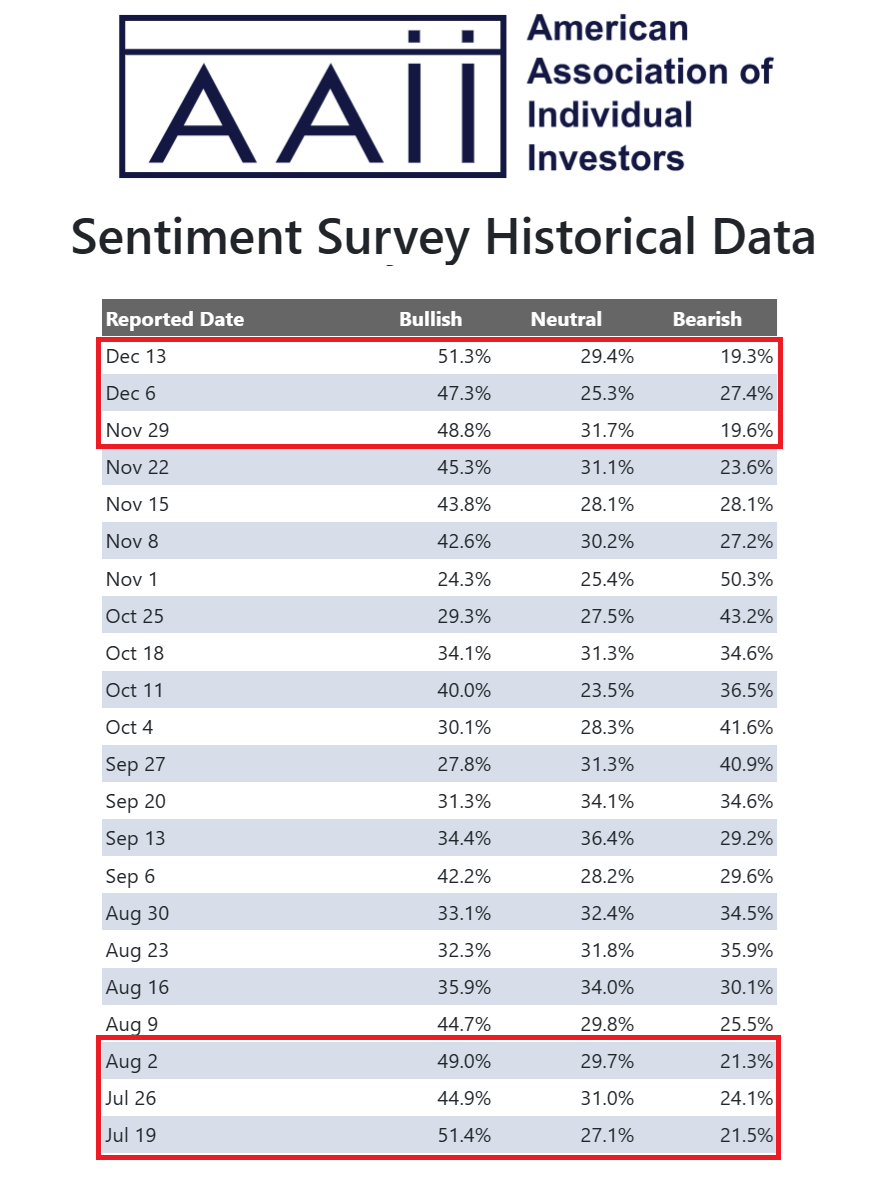

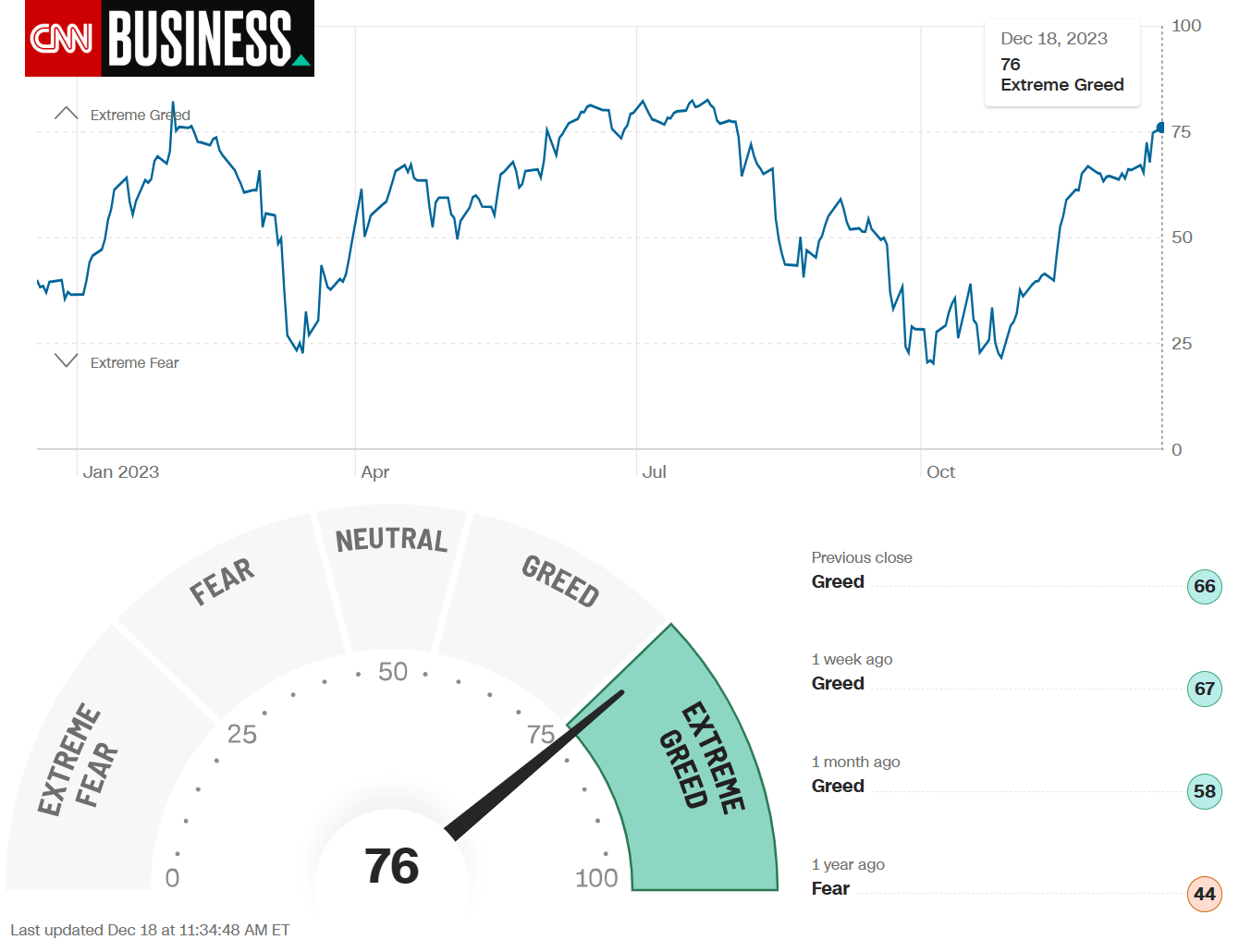

How euphoric have traders and investors become into the New Year? The last time the AAII Investor Survey reached 48%+ bulls averaged over 3 weeks, at the same time as the CNN Business Fear & Greed Index was above 75+ (out of 100) came right at the early August market peak, just before a -10% drawdown in price.

AAII Investor Sentiment Survey, Since July 19th, 2023, Author Reference Points CNN Business - Fear & Greed Index, December 18th, 2023

{kind=link}

{kind=link}

The next instance was way back in November 2021, as the Big Tech stocks reached their zenith, and only weeks before a -30% market decline erupted during most of 2022. You can review the last two occurrences of investor extremes in bullishness below, marked with green arrows.

YCharts - S&P 500 Price Changes Daily, Since October 2021, Author Reference Points

Final Thoughts

Another bearish factor to consider is we have now officially entered a Dow Theory sell signal with the Dow Industrials at 52-week and all-time highs, while the Transports and Utilities are lagging badly. This non-confirmation has been especially pronounced since the August peak in many individual stocks.

YCharts - Dow Industrials vs. Transports & Utilities, Price Change, Since August 1st, 2023

My analysis of sentiment is everyone wanting to get back into stocks from cash has largely made that move going into January 2024. We either get an extended breather for price over several months or the start of another bear market like 2022 is at hand.

The latest 7-week jump in stock quotes represents the sharpest percentage gain over an equivalent span since April-May 2020, coming off the pandemic panic bottom. Are we really going to start a new multi-year bull market from a clearly overvalued point historically, or is another equity drop actually dead ahead? That's the judgement you need to make for yourself.

The typical stock market trading cycle pattern is prices peak right before or after a recession appears. Equity prices continue to slide for a while, even after the Fed starts lowering interest rates. Then, at the depths of economic contraction and consumer spending pullbacks, excessive investor fear pushes money into gold/silver hedges first. You experience a period of months or longer of rising monetary metal values as easy Fed policy begins to get some footing, while investor fear shoots to 5 or 10-year highs. Then, the equity market starts to rise again in anticipation of an upturn in economic demand and better corporate profitability.

We have not even had the recession yet during 2022-23 (contrary to what 20 and 30-somethings believe), but everyone is celebrating its demise and the next upswing in the economy. Is such an abnormal outcome possible? Theoretically, the answer is maybe. However, with so many geopolitical troubles in America and overseas, the Treasury spending and debt/deficit mess not sustainable for very long, and consumers feeling the pinch of higher interest rates, any unexpected negative news event could cause a cascade of problems for both the economy and stock market pricing.

Betting on another +10% or +20% of upside in American stocks kind of requires a sentiment extreme similar to the bubble territory of the late 1990s or 1920s. Plus, nothing can go wrong in the world, the Fed can lower interest rates with still stubbornly high inflation without collapsing the dollar's exchange value, and foreign investors won't care about an extra $2 trillion in Treasury debt being added annually (which can never be repaid in constant dollar value). That's too much for me to swallow. You have to IGNORE the three foundations of past stock market booms are lacking: low inflation/interest rates, high levels of corporate profitability, and relative geopolitical calm around the world. You are gambling skies will turn brighter in 2024, not darken further.

If you are fully invested now, I would whittle back my holdings in regular ETFs like the Vanguard Total Stock Market index product. For aggressive traders, selling VTI with the intention to buy it back at lower quotes sometime during 2024 makes plenty of sense to me. The same goes for other broadly diversified U.S. index ETFs. Given a -10% to -15% market tank in January or February, and the real-world ability (excuse) for the Fed to actually lower interest rates, a better entry for new capital might present itself soon.

Heaven forbid, if the wheels fall off the economy during 2024, stock market losses of -20% to -50% will be commonplace. Generating a "guaranteed" 5% sitting in cash, with the 100% "guaranteed" return of your upfront capital remains an intelligent risk-reward place to wait out a world in turmoil and U.S. economy awash with debt. At least that's the way I see today's big macroeconomic picture.

I will still be writing individual company articles, for names holding above-average odds for outperformance of the major U.S. indexes. And, I will own many of them with smaller position sizes and macroeconomic hedges against a significant market meltdown. I do not recommend general net-short portfolio weightings, given the high margin interest expense backdrop currently, and the cost for put options in a normal range historically. Stay diversified. Own assets outside of the stock market, including gold/silver and some bonds and cash to survive another trading year.

I remain a firm believer you need to have 10% to 20% of your portfolio parked in gold/silver bullion plus a variety of related mining concerns. Expanding geopolitical stresses and the lack of spending restraint in Washington DC (requiring future money printing) dictate as much. That's the conservative approach to navigate the long-term overvalued market setup going into 2024.

Thanks for reading. Please consider this article a first step in your due diligence process. Consulting with a registered and experienced investment advisor is recommended before making any trade.

For further details see:

Bullish Sentiment Is Too High Going Into Recession: Sell VTI (Rating Downgrade)