VTI - Bulls' Hopes Fade As S&P 500 Earnings Estimates Fall

2023-10-20 11:45:12 ET

Summary

- Inflation is expected to remain high, with no rate cuts in sight, causing concern for the bulls.

- Earnings estimates for the fourth quarter are falling, raising doubts about the S&P 500's lofty valuation.

- Margin estimates for 2024 appear to be too high, suggesting potential margin compression and the need for earnings adjustments.

Yields, the dollar, and oil have soared. Inflation will likely be stuck around 3.5 to 4% for the next several months, along with no rate cuts coming anytime, and now the one thing the bulls were banking on is melting before their eyes.

Earnings estimates for the fourth quarter are falling, and the bad news is that third-quarter results have only started. It will be hard to justify the S&P 500's ETF (SP500) lofty valuation if earnings growth for the index continues to vanish, meaning the overvalued equity market will have no legs to stand on.

Estimates are Dropping

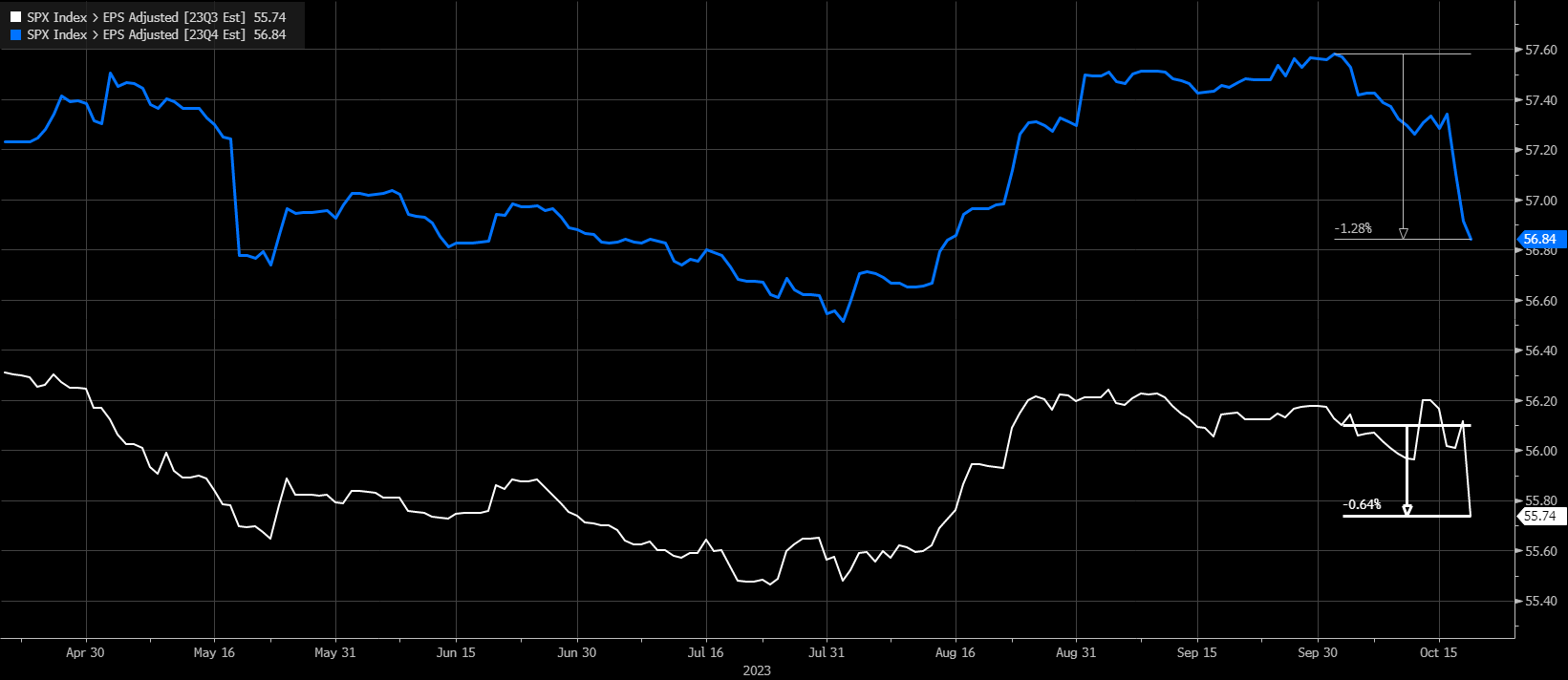

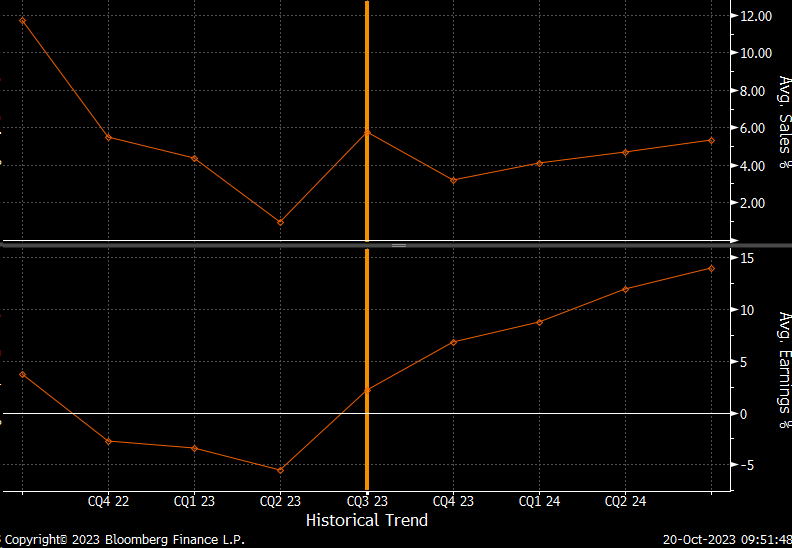

Since October 3, earnings estimates for the third quarter have fallen by 0.6%, and for the fourth quarter, they have fallen by almost 1.3%. This seems like a material drop in earnings estimates, considering that just 86 out of 499 companies in the index have reported results thus far.

{kind=link}

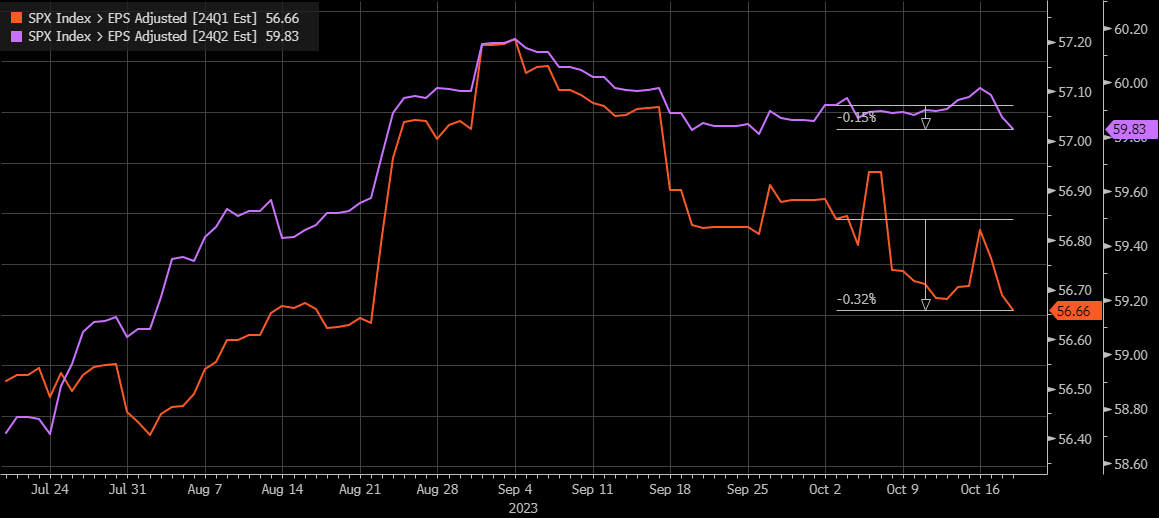

This has resulted in first-quarter 2024 earnings estimates dropping by 0.3% and second-quarter earnings estimates dropping by 0.1%. Certainly, these are not large drops at this point for 2024, but if earnings for 2024 start to trend lower with 2023 earnings estimates, that poses a serious problem for the SPDR® S&P 500 ETF Trust (SPY) and the index because this is not a cheap market.

Margin Estimates Appear To Be High

{kind=link}

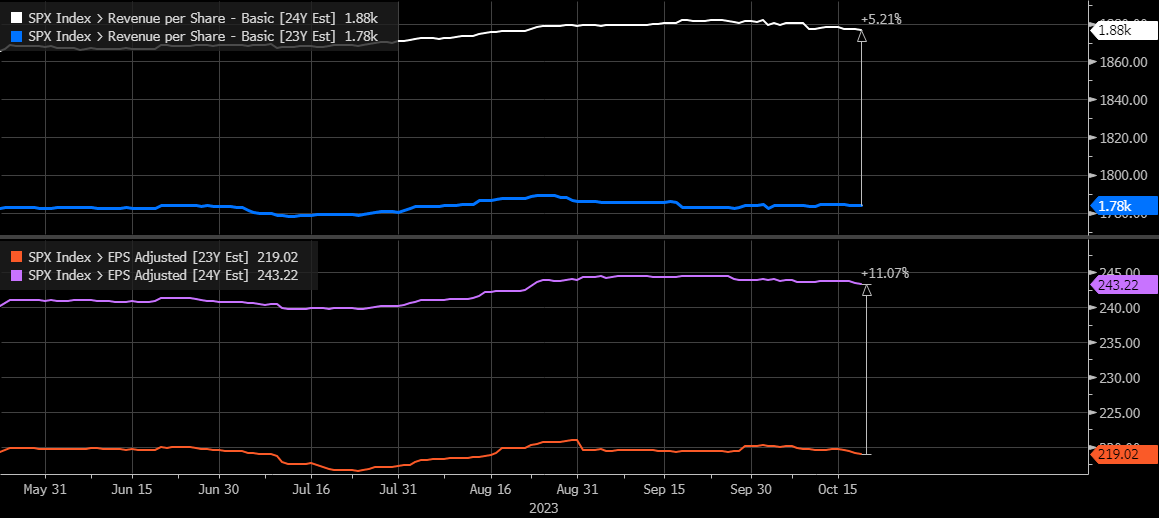

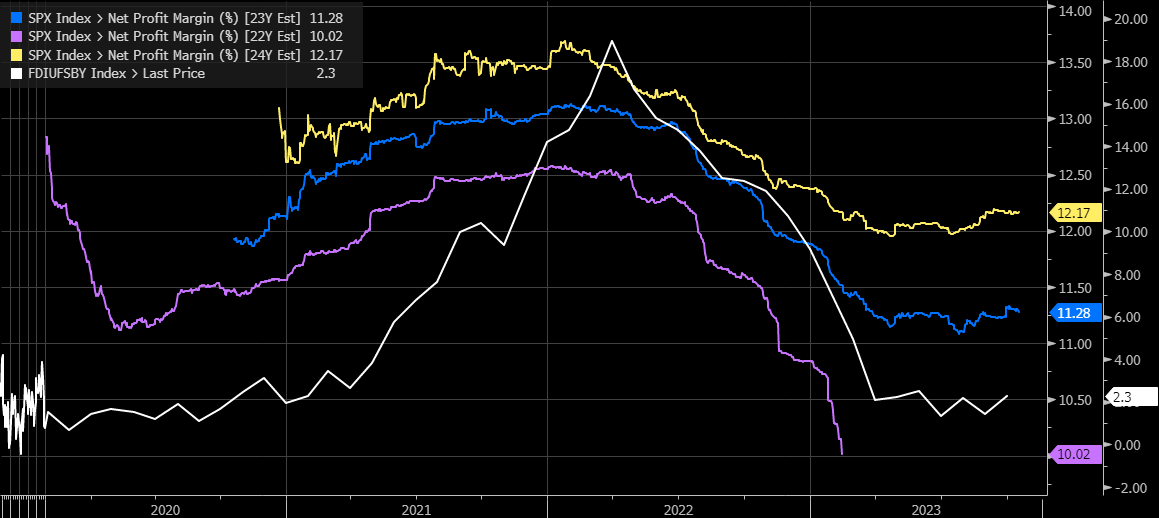

Investors and analysts expect earnings to grow in 2024 by around 11%. This seems like a stretch, given that sales are only expected to grow by 5.2%. It would suggest that earnings growth will largely come from share buybacks or margin expansion.

{kind=link}

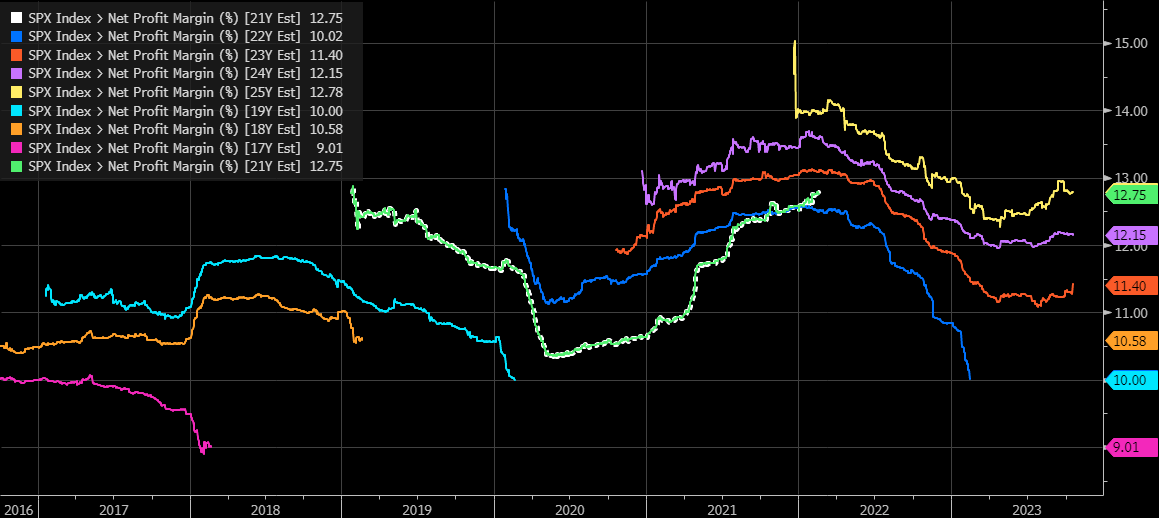

While it is tough to measure share buybacks, we can measure margins. Margins are expected to expand significantly in 2024 to 12.1%, from 11.4% in 2023 to just 10% in 2022. That is a lot of margin expansion in a category that tends to see expectations start very high and then fall over time.

{kind=link}

It seems probable that the margin expectations are too high because thus far, in the small set of the third quarter results, we have seen sales grow 5.8% and earnings grow just 2.2%. We saw the same thing in the second quarter, too, with earnings falling by 5.5% while sales grew by 0.9%, and in the first quarter, when earnings fell by 3.4% and sales grew by 4.35%. Somehow, that is expected to change in the fourth quarter, with sales growing by just 3.1% and earnings growing by 6.7%, and then accelerating in the first quarter with sales growing by 4.1% and earnings growing by 8.7%, which is exactly the opposite of the trend we have seen since the third quarter of 2022.

{kind=link}

Margins tend to follow the year-over-year change in the producer price index trade services, and trade services have shown no sign of moving higher. They have certainly leveled off, but to see margins move higher in 2023 and 2024, we would probably want to see that trade service value rising, and it isn't. It has flattened out.

{kind=link}

Too Expensive

This is likely why earnings estimates for the third and fourth quarters are coming down, based on the early rounds of data; when sales grow faster than earnings, it is a sign of margin compression. If margins are compressing, then it probably means that estimates for all of 2023 and 2024 will need to be adjusted, and there is a good chance the index either doesn't see 11% earnings growth next year or that the 11% earnings growth comes off a lower level of overall earnings in 2023.

{kind=link}

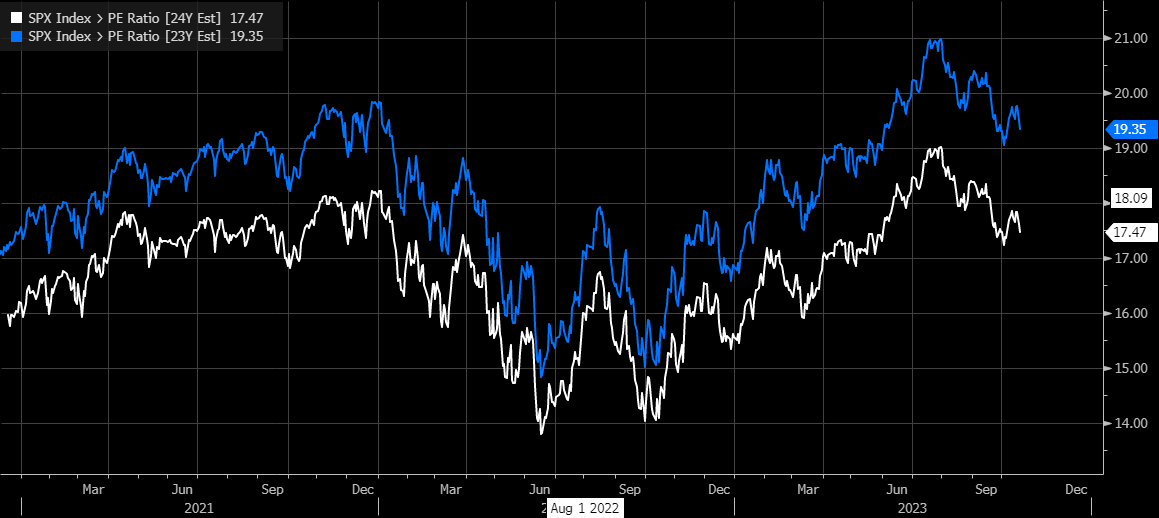

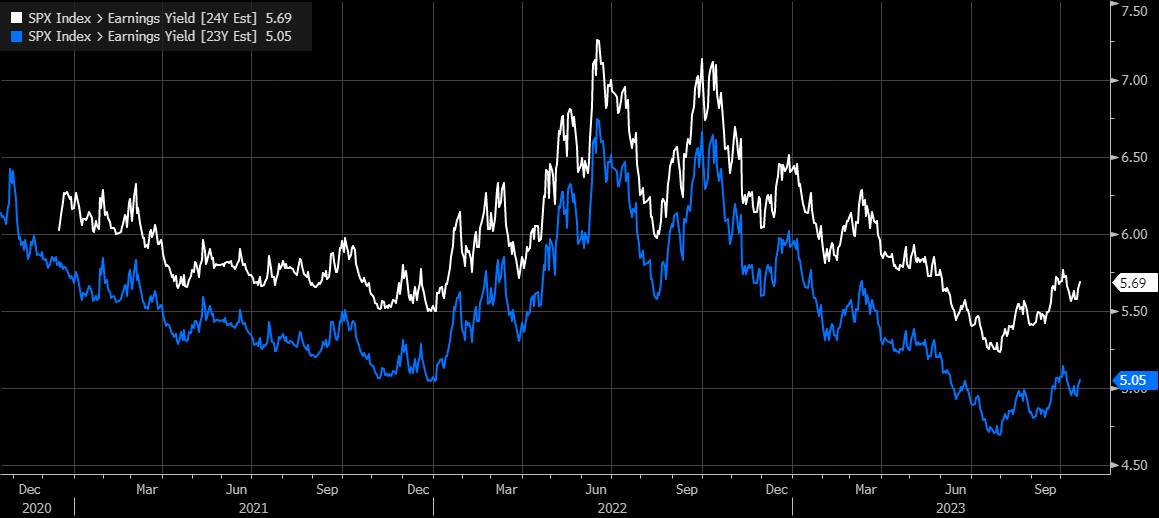

Why would an investor pay 19.3 times 2023 earnings estimates, or 17.5 times 2024 earnings estimates, when the 2-year Treasury rate is paying a "risk-free" rate of 5.1%, or the 10-year Treasury pays almost 5%, compared to the earnings yield of the S&P 500 of 5.05% in 2023 or 5.69% in 2024. It doesn't make much sense, especially when the risk is that earnings estimates may be too high and need to be adjusted lower, meaning the earning yields go higher and the SPY drops.

{kind=link}

If earnings estimates for the third and fourth quarters continue to sink, the S&P 500 ETF will sink with them because there will be nothing left of the bull narrative to support stock prices.

For further details see:

Bulls' Hopes Fade As S&P 500 Earnings Estimates Fall