CTRA - Bumbershoot Holdings 2022 Investor Letter

Summary

- Bumbershoot Holdings uses a fundamental investment strategy as a “quality over quantity” approach to identifying and evaluating great businesses. It primarily invests in small- and mid- capitalization public companies.

- Bumbershoot Holdings registered a gain of +1.2% for the full-year 2022.

- Inflation is an endemic, systemic part of our global economic system. A release-valve off a faulty monetary policy—a feature, not a glitch. Thus, need to stay invested for the long-term.

- Deflation is the true “enemy” of the Fed… and also a danger to investors as oneof the only ways to catch a permanent impairment. It is a real risk factor to growing wealth… so beware!

- Bumbershoot remains my mechanism to address these two forces… and so I’dask for the opportunity to manage aportion of your money, right alongside most of mine….

Dear Partners,

{kind=link}

Bumbershoot Holdings registered a gain of +1.2% for the full-year 2022. Given the challenging year in global markets, this result exceeded major benchmarks.

I’m not going to beat my chest for the insipid outcome of not losing your money, although I am rather proud of our result for the year. While highlighting the risks for a long time—' you have to get it right on price too’ — merely calling out the threats is different than actually navigating them. Presented with an extremely difficult market environment, we proved up to the task. While it is never fun to sit out/sit through periods of intense reflation, it is gratifying to see that discipline become rewarded.

With formalities out of the way, I’m just about ready to move to the heart of this letter, which is a fair amount lengthier than previous letters, but I hope will address the following core messages…5

- That inflation is an endemic, systemic part of our global economic system. A release-valve off a faulty monetary policy—a feature , not a glitch. Thus, need to stay invested for the long-term…

- That deflation is the true “enemy” of the Fed… and also a danger to investors as one of the only ways to catch a permanent impairment . It is a real risk factor to growing wealth … so beware!

- That Bumbershoot remains my mechanism to address these two forces… and so I’d ask for the opportunity to manage a portion of your money, right alongside most of mine…

By Month: Bumber S&P 1 Russell 2 FTSE 3 Barclay 4

| Jan-2022 |

| -2 .92 % |

| -5.26 % |

| -9 .66 % |

| 1 .08% |

| -2 .62 % |

| Feb-2022 |

| 7 .86 % |

| -3 .1 4 % |

| 0.97 % |

| -0.08% |

| -0.94 % |

| Mar-2022 |

| 8.7 9 % |

| 3 .58% |

| 1 .08% |

| 0.7 7 % |

| 0.60% |

| Apr-2022 |

| -4 .47 % |

| -8.80% |

| -9 .95% |

| 0.38% |

| -2 .39 % |

| May -2022 |

| -0.51 % |

| 0.01 % |

| 0.00% |

| 0.84 % |

| -0.82 % |

| Jun-2022 |

| -1 0.34 % |

| -8.39 % |

| -8.37 % |

| -5.7 6 % |

| -3 .85% |

| Jul-2022 |

| 4 .50% |

| 9 .1 1 % |

| 1 0.38% |

| 3 .55% |

| 2 .58% |

| Aug-2022 |

| -0.69 % |

| -4 .24 % |

| -2 .1 8% |

| -1 .88% |

| -0.38% |

| Sep-2022 |

| -6 .61 % |

| -9 .34 % |

| -9 .7 3 % |

| -5.36 % |

| -3 .94 % |

| Oct-2022 |

| 7 .35% |

| 7 .99 % |

| 1 0.94 % |

| 2 .91 % |

| 1 .86 % |

| Nov -2022 |

| -0.37 % |

| 5.38% |

| 2 .1 5% |

| - |

| 2 .89 % |

| Dec-2 022 |

| 0.61 % |

| -5.90% |

| -6 .64 % |

| - |

| -1 .25% |

I’ve teased at all these threads the past couple of years, interspersed throughout previous letters… and to me they all run a course… except they have not been fitted together. I spend a lot of time writing these notes very particularly, in order to build up my view of the world. And so, with this letter, I want to take those individual strands of observation & philosophy… and try to wrap them up into a tight bouquet…

But before I do, I’d like to just take a final moment to officially close out 2022. While it was not additive to our track record per se… it does add to our long-term record of accomplishment, as we continue to do what we had originally set out to do upon starting the fund.

One of the best things I did last year was read the book Atomic Habits , by James Clear. The most impactful quote from the book was “ you do not rise to the level of your goals. You fall to the level of your systems .” We have built a process and are destined for success.

I am excited for all of what is to come!

Performance

Bumbershoot Holdings L.P. generated a positive gross return of +1.24% for the full-year 2022.

The partnership has a cumulative total gross return of +102.8% since inception in Oct-2015.

Looking more closely at performance, monthly returns showed greater volatility than in years past. This was mostly correlated to macro events such as the Russian invasion of Ukraine, lingering effects of the pandemic and key Fed decisions; as well as in part due to higher levels of portfolio concentration.

Investment activity is categorized into five segments— Core , Micro , Value , Special Situation, Discretionary — Estimated P/L contribution is as follows:

| By Category |

| By Market Cap |

| Core |

| 5.1% |

| Large |

| 2 .6 % |

| Core - Long |

| -1. 7% |

| Mid |

| -2 .3 % |

| Core - Short |

| 6. 8% |

| Small |

| 4 .7 % |

| Micro |

| -3 .8% |

| Micro |

| -3 .1 % |

| Value |

| 0.8% |

| Fx |

| -0.6 % |

| Special Situation |

| 0.1% |

| Misc |

| -0.1 % |

| Discretionary |

| -0.3% |

| Fx. |

| -0.6% |

| Misc. |

| -0.1% |

| FY-2022 |

| 1 .2% |

| FY-2022 |

| 1 .2 % |

Core category profits were boosted by short exposure. While the fund never got close to becoming positioned net negatively, even modest exposure helped to offset a challenging market environment.

On the long side of the ledger, Core gains were led by Viking Therapeutics ( VKTX ) which increased substantially following Madrigal Pharmaceutical ( MDGL ) releasing positive data on its NASH trial in Dec-2022. Ligand ( LGND ) —Viking’s former parent company which still owns ~9% of shares—was down for the year, in part due to separating OmniAb ( OABI ) into a standalone public company via a merger into a SPAC. The fund’s combined position in Viking / Ligand / OmniAb represents largest holding within the Healthcare sector.

Our holding in Intrepid Potash ( IPI ) was also a positive contributor for the year—despite its shares inexplicably being down for the full year, completing a round trip from the high-$30s to $120 and back again. While we did not sell our position, we took advantage of the massive run up in Feb-Apr as an opportunity to pull out significant equity through option hedges. We remain highly constructive about fundamentals within the ag-fertilizer industry; and a combined position in Intrepid / Nutrien ( NTR ) / CF Industries ( CF ) / Mosaic ( MOS ) still represents the largest overall weighting within the fund.

Contribution was surprisingly broad given the tenor of the year with additional gains registered in Atlas Air Worldwide ( AAWW ) , Berkshire Hathaway ( BRK.A )( BRK.B ) , First Solar ( FSLR ) , Coterra Energy ( CTRA ) , Box ( BOX ) , and KVH Industries ( KVHI ) .

Of course, not everything was up. Losses were mainly confined to positions within the Technology sector, as Alphabet ( GOOG , GOOGL ) and Micron ( MU ) accounted for a significant portion of the decline. Our position in Barrick Gold ( GOLD ) was also an appreciable detractor for the second straight year—as the (underlying) yellow metal was a surprising laggard despite the highest inflation in over 40+ years. British home improvement retailer Kingfisher ( KGFHF ) as well was a notable decliner, along with a number of other more moderate detractors.

The Micro strategy had a grisly outing primarily due to Charles & Colvard ( CTHR ) —which declined by -70% for the year. That decline was partially offset by gains in Select Energy Services ( WTTR ) and Photronics ( PLAB ) .

Value category registered a gain primarily attributable to our investment in Adams Resources ( AE ) . In Nov-2022, the company announced the repurchase of all shares previously held by the founding family— representing 44% of total shares outstanding.

Special Situation and Discretionary categories had no significant attribution to merit discussion in detail.

In terms of exposure levels, Bumbershoot ended 2022 with 20 “positions of significance” that each represent a weighting of more than 100bps. This has remained steady in the 20-25 range, with a few always bouncing around above/below that threshold. The Core category ended the year near its targeted exposure level, while Non-Core categories remain mixed with above/below target weightings of ~5% AUM each.

Investment Outlook

In many respects, the investment outlook for this year feels surprisingly similar to last year… albeit with one major caveat.

As I wrote in last year’s letter to partners:

“The structural configuration of the economy has shifted rapidly—from one in which the Fed must do anything and everything to protect against a deflationary spiral, to one in which it is now closely monitoring the threat of runaway inflation expectations. The Fed is still very much in charge, but it has given up control . […]

Best case —it will be able to engineer this “soft landing” we’ve been hearing about for years. ‘ When you gonna drop Magnum on us already ?’ That it can raise rates / control inflation without damaging the job market, sending expansion into recession.

Worst case —it cannot… and it will need to hit the hard reset button. ‘ Flip the boardgame .’ Hike rates to crush demand-pull inflation; and give back all the gains from the expansion along with it.”

That’s still the case…

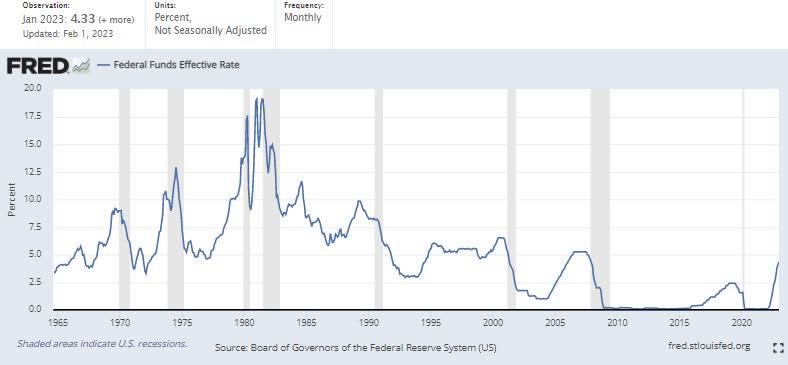

While it may not be in the same inning, it’s very much the same game. We’re still off-leash …because inflation is still an issue, but one the Fed knows to deal with by way of its unique ability to raise/lower interest rates— the special power of the Central Bank Superheroes .

And it’s doing that. Raising rates. Quickly at first, then slowly, as it ratchets closer to restrictive territory and the terminal rate of the SEP projection.

All this just to keep expectations in check. To not allow inflation to ever become permissible… lest it become embedded in people’s psych. The Devil’s Bargain 8 that cash will not be suitable as a store of value asset. That the U.S. dollar can hold to reserve status , but not as a place to park wealth.

“ If a policy of active or permissive inflation is to be a fact, then we can secure the shreds of our self- respect only by announcing the policy. We should have the decency to say to the money saver, ‘Hold still, little fish! All we intend to do is gut you .’”

—Malcolm Bryan President (1951-1965), Federal Reserve Bank of Atlanta

But this is why inflation is a filler arc to the storyline.

High inflation… sure, now that is something… But inflation is the game to the Fed .

The Fed never wants to beat inflation back too badly… because then who would it fight? It must tread lightly, especially in a world of natural 9 deflation:

“This dynamic was always positioned as a balance. The Central Bank Superheroes trying to defend against the evils of Deflationary Forces in the economy — namely demographics, globalization and technology/efficiency. And just like in the comics, in the end the superheroes always win… because even when it looks most grim… they still win (2% at a time…) through inflation—growing our way out over cycles. This was traditionally the risk. Timing of the cycles. The ebbs and flows of liquidity to the reflation trade — the equivalent of potentially being forced to bed early without having a chance to flip to the next page to find out how the story ends.”

That is all normal from a risk perspective.

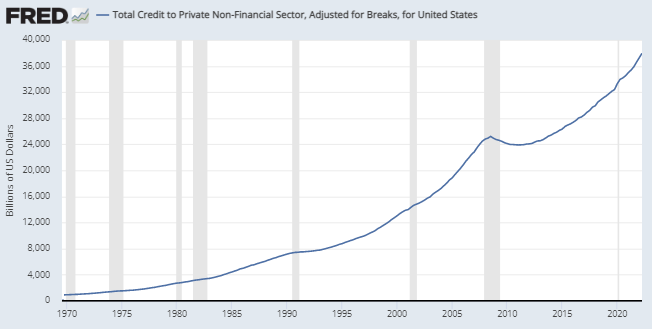

But while I’ve labeled deflationary forces as being the true enemy… the reality is that is just an outcome. The cause is of another name. Financial engineering . The Casino Economy . Perhaps most accurately, Creditism , a term coined by the well-known doomsayer , Richard Duncan. It is our entire system of debt… the house of cards… always just waiting to collapse.

Because America runs on credit .

In the absence of productivity gains… Debt is the driver of economic growth; Leverage the foundation of prosperity.

Credit is what makes the world go round …

And that’s a problem if the music ever stops.

{kind=link}

But I’m not some crazy doomsayer… I’m an optimist! Or at least a cautious one. A hopeful realist .

So, to go back to what I said last year, my view was the Fed was feeling the heat— we’re cooking with gas now ! That it was being forced to act aggressively in order to re-anchor people’s inflation expectations, before it got any further behind the ball.

That the momentum trade was officially over . The 2019-2021 playbook … done . Meme stocks … finished .

That the lower-for-longer , growth-at-all-costs , there- is-no-alternative , stonks-only-go-up , BTFD mantra… may it rest in peace .

That the excess demand… the “spillover” effect into the real economy brought about by the cartoonish increase in money supply… was finally going to be reined in.

But also to not underestimate the Fed’s desire to keep the music playing. That was the big IF… whether the expansion was set to continue. That the Fed could tap the brakes without stopping the car. If it could raise rates to control inflation without damaging the job market and flip the expansion into recession.

I felt like it could.

And we sort of got it right. So close .

The Fed hasn’t pushed too far yet. It hasn’t made any policy mistakes it can’t come back from. Even from his interview yesterday, Jerome Powell remarked that the disinflationary process has begun… while labor is still very strong.

The only thing that didn’t happen is consensus . Stocks never got any credit for the cycle continuing in terms of multiple expansion. The view shifted towards a hard landing being the final outcome more likely than not… at least until the past month or so.

But in either case, the reality is we just don’t know yet. The story is still being written. So, that outlook is still largely intact…

Except for the one major caveat that I alluded to at the outset… which is that I’m a lot more nervous about it.

…but what’s to be nervous about? I’m a realist… and I really know that we need inflation over the long-term.

Death, taxes… and inflation . It’s an inevitable!

“I don't know what business will do next month or next year. I bought my first stock in April of 1942. I was 11 years old. Pearl Harbor had happened 3-4 months earlier. We were losing the war… I mean, you want to talk about bad outlook for the country. Now nobody thought we were going to lose the war, but at that time we were getting clobbered in the Pacific [...] and it was a good time to buy stocks. I bought stocks after 9-11 […] in 1987 after the big crash in the fall. The country is not going away. The plants aren't going to go away. People aren't going away. The talents aren't going to go away. The country will grow in value over time – now who gets it is another question – but it will grow in value; and if it grows in value, businesses will grow in value. So, it is a terrible mistake to buy or sell stocks based on what you think business is going to do next month or even next year.”

—Warren Buffett

It turns out… it’s ALWAYS a good time to buy stocks; and Inflation is what allows quotes like that to exist. It is how investors in Bumbershoot will hopefully be able to marvel, in much the same way, when they look back on their investment 30-40 years from now…

Everyone knows they need to be invested for the long- term. But it’s not as easy as sitting back and chuckling, “ Oh, what a life! ” That’s why he’s Warren Buffett!

The part nobody ever mentions about quotes like that is you have to avoid a lot of idiotic maneuvers to be able to pull it off. Because anything that could cause a permanent impairment might set you.

It kind of reminds me of Nike’s old “ Golf’s Not Hard! ” ad campaign with Tiger Woods. It’s always a good time to buy stocks if … you have a long time-horizon… and some modest skill at stock selection… and can manage position sizing… and never have a liquidity event.

Because if you just compound a bunch of numbers… it is going to be a big number eventually.

But if you multiply in just one measly zero somewhere in the middle… then the whole thing is always ZERO.

So don’t worry about everything that can go right . Worry about not losing. Worry about catastrophe risk.

One of the easiest ways to lose… to multiply in a zero… to permanently impair an asset—through bankruptcy, restructuring, or dilution—is to have a liquidity crisis . A period of distress… which can most easily be caused by a severe short-term contraction/deflation.

And that’s why I’m nervous about it. Because the Fed has been the offset. The motor to a reflationary pump. So, if it is off now… then how is risk on?

Well, that doesn’t matter! Nobody believes the Fed will actually be able to keep rates at 5% for any significant period. And frankly I don’t believe it either! There’s no recent precedent to it doing so… and it’d be a disaster. But you need to really listen . That’s why it’s the risk.

Go back to the Nov-2022 FOMC Press Conference:

“You can think about our tightening program as really addressing three questions […]

On the first question—how fast to tighten policy— it’s been important that we move expeditiously… and we have clearly done so. […] It’s a historically fast pace, and that’s certainly appropriate given the persistence and strength in inflation and the low level from which we started.

So now we come to the second question, which is how high to raise our policy rate. And we’re saying that we’d raise that rate to a level that’s sufficiently restrictive to bring inflation to our 2 percent target over time […] because that really does become the important question […] and that’s why we say that ongoing rate increases will be appropriate. […] That level is very uncertain, though, and I would say we’re going to find it over time. […] with the lags between policy and economic activity, there’s a lot of uncertainty […] So I would say, as we come closer to that level, move more into restrictive territory, the question of speed becomes less important than the second and third questions. And that’s why […] it will become appropriate to slow the pace of increases. So that time is coming […]

To be clear, let me say again that the question of when to moderate the pace of increases is now much less important than the question of how high to raise rates and how long to keep monetary policy restricted, which really will be our principal.”

—Jerome PowellFOMC Press Conference – Nov-2022

This needs to be the key focus… How fast…? How high…? How long …?

And it’s that final question I’m particularly focused on. Because that’s the one that’s going to break people.

The first question was already answered… really fast . The fastest rate cycle in history. That’s because it was starting off from the bottom—levels of unprecedented accommodation. Inflation was also already really high when it started to hike. The Fed needed to move fast… and it did.

But as it ratchets now, into the lower end of restrictive territory and nearer to the terminal rate, investors are starting to make a lot of noise about the second quest. How high is closing in on an answer. But people really need to be asking how long .10

Because the Fed has a task. It is on a mission to bring inflation back to its 2% target; and it isn’t going to cut rates unless something breaks. Although the definition of breaking might be subjective.

The Fed has a dual mandate and only a dual mandate.

It made that clear in its remarks a couple of weeks ago on its evolving views of that issue. That after a decade of trying to expand its goals in highly politicized areas it “ should ‘stick to [its] knitting’ and not wander off to pursue perceived social benefits that are not tightly linked to our statutory goals and authorities .”

As Powell reiterated just yesterday, “ accountability is to the legislature .” To deliver on that mandate to the Senate and the House. Not to the people of the United States; and definitely not to you (or your portfolio).

Deliverance might take the start of a new rate cycle…

{kind=link}

The Fed is just doing its job . It’s late and fixing a crisis of its own making… but it is doing it. Fairly admirably, if truth be told.

Taking responsibility for inflation… full stop. And yea, maximum employment too. Although on that one may actually be looking to see it cool off a bit more. But so, inflation and employment… just lay it down at the feet of the Fed.

Can’t ask them for a lot more than that.

The Fed is kicking the rest of it—like climate change or racial equality… or distribution of wealth—back to the fiscal side of the house, to let the Federal government pick up the baton and sort it out.

That’s kind of a dicey game. Because it looks like it is being fumbled…

I’m not looking to make this letter at all political since its across both sides of the aisle—but America needs to take a fundamental redesign to the political strategies and economic policies that have brought us here. The globalization, deregulation & economic restructuring that has failed average Americans fairly spectacularly. That has led to corrosion of our social fabric. Wrought upsurges in violence, alienation, isolation, loneliness. Increased homelessness and financial insecurity, while decreasing life expectancy for the first time in history; and in general, fostering a deep-rooted anxiety for the future. Policies leading to a breakdown of the natural world. And perhaps worst of all… the underutilization of our talents… robbing people of their full potential.

The Fed doesn’t want all that smoke .

But without fiscal support… it doesn’t have an option. Because if it does its job in isolation, then something is bound to break. And credibility might break with it.

I made a half-joke in last year’s letter that “ You shall not crucify mankind on a cross of T-Bills .” It was my favorite part of the letter as a play on William Jennings Bryan’s famous Cross of Gold speech.

Because that’s really what it would’ve been in my eyes were it to happen. An execution of the consumer and the middle-class. For the salvation of money, power, and status quo. At the redemption of bondholders.

That was the joke . You can’t do that…

Heroes are supposed to fight for the common man…

But what if superheroes aren’t always the ‘ good side’ ? Even with the noblest intentions… what if they’re just flawed, dangerous vigilantes with their own agenda?

Price stability … to the benefit of all!

Inflation as an everyman problem… except for it isn’t. It isn’t about rent increasing or gas prices going up. It is about the erosion of wealth . Just like any other commodity, wealth has a storage cost. Need already to have amassed it first though, in order to be so lucky as to watch it fade away.

For the vast majority of people, the issue of inflation is in reality a short-term discomfort. The constriction of financial freedom.

As fortunately for most people, the most valuable asset they own is a near-perfect pass-through on inflation over time. Themselves . The best way to protect against inflation is to improve your own earnings power.

The Fed ought to let people rediscover that …

Never meet your heroes…

“There are two ideas of government. There are those who believe that if you just legislate to make the well-to-do prosperous, that their prosperity will leak through on those below. The Democratic idea has been that if you legislate to make the masses prosperous their prosperity will find its way up and through every class that rests upon it.”

—William Jennings Bryan

If this whole outlook has seemed a little confusing or contradictory… it’s because it can be. The investment picture is in a fuzzy place.

Needing to stay steadfast for the long-term— inflation . But also avoid permanent loss short-term— deflation .

Bumbershoot remains my mechanism to address these opposing forces. To grow wealth over time through any cycle or situation.

Connecting this back to the cartoon on the first page— A Bug’s Life took its direction from the Aesop’s fable The Ant and the Grasshopper .

The moral of that story is to always be prepared. So, what is Bumbershoot doing to be prepared?

While I’ve spent a lot of time talking about the Fed and macro factors, interest rates and catastrophe risk.

I spend a lot more time thinking about great, durable businesses… to own for the long term and benefit from the inevitable inflation…

And in that regard, I plan to stay the course…

I am very positive on the companies we own. Feel great about our portfolio prospects. Think we’re exceedingly well positioned to take advantage of any opportunities that might arise.

While we’re at a size where we can be nimble and react quickly to things if situations were to change… I don’t see that as being necessary right now.

Great businesses will be able to maintain or even grow purchasing power through the ability to increase price over time without loss of market share or volume.

Regardless of the economy, interest rates or currency.

I’ve often said that there is too much money chasing far fewer durable profits. Even if money supply were to contract further… that is still true. Great businesses are hard to find.

Marketing

Whoa…! New Section Alert… !!

Instead of just a throwaway line in the Administrative segment, it felt like this ought to be separated into its own section.

Because I want to do something that I haven’t officially done since starting the firm: ask for your money .

I sent out the fund’s initial Letter to Potential Partners back in Sep-2015.

I said at that time, investing is not a science and there is no precise formula for a “great business.” While the characteristics may be simple to list—secular growth, barriers to entry, scalable operations, reinvestment opportunities, quality management—they are typically significantly more difficult to evaluate in practice. It is oftentimes the subtle nuances of a business that build up into the critical components needed to support and differentiate the investment thesis.

I explained why I felt uniquely positioned to do this:

“I can point to my past experience and sizable body of published work as proof of concept, but early- stage partners should understand they are largely buying in to that belief. I have a deep intensity to make this partnership a success and to prove out the strategy over time through our returns.”

Essentially, to just hold the faith…

Hope is never a great investment strategy … but after a number of years, I can say this “proof-of-concept” has turned to a reality. With a track record since 2015, we have accomplished the mission that I set out to do in offering people an alternative in asset management.

Learning to dance with two left feet !

-- -- -- --

A handful of years, though, is hardly a career, as our long-term track record is only just starting to be built. The jury remains out on where we will ultimately land with respect to my favorite investment analogy:

“Ability to repeatedly find idiosyncratic risk/reward […] through fundamental research is the unicorn of active management. It is the proof of market inefficiency; and it is worth its weight in gold.

The problem for most active managers stems from only being a horse with a party hat on, casting a favorable shadow in the right light for a couple of years.

My own classification will be borne out in the years to come.”

I can’t say for certain…

But I am increasingly confident that we are building a process that is both scalable and repeatable at higher amounts of capital under management.

So, as we get ready to take the next steps forward… I’d like you to be part of it—to build and grow together.

I’ll be setting up meetings in the next few months for anyone interested in learning more… and any support to help intro the fund to new capital partners is always greatly appreciated.

Administrative

While I’ve often joked in this section about the small changes to report on—an updated Wordpress account; Administrator fees going up—this upcoming year may actually be poised for significant change…

You’ll notice that I very often use the collective “we” in talking about our partnership… that’s because I really do look at it as a team… as a partnership . But at least on the investment side, the reality is it’s just me…

While there is no “ I ” in Bumbershoot … there is one in Bumberings … the NY- LLC which acts as investment manager & General Partner of the fund; and for which I am both the managing and sole member.

That is a lot… especially as we reach a certain size and prepare to take additional steps forward.

And so, I’ve recently begun to evaluate additions to the firm. I’m looking to hopefully expand in 2023 with one new member that can help build scale/infrastructure, with the goal of that person becoming a partner.

I will have more to say on this process as it evolves.

Taxes

The partnership’s form Schedule K-1 that reports each partner’s share of income/losses for the 2022 tax year is being prepared by our administrator. Copies will be sent to each individual LP once available.

This year was mixed from a tax perspective, as our tax burden will reflect a moderately higher gain than our stated increase in investment accounts. This is due to the nature of gains for the year—particularly our short exposure and hedging activity.

As reminder, we successfully implemented a “ Master- Feeder ” structure over the course of 2019 to be able to more efficiently pass back long-term gains in our Core holdings. While this had minimal effect in 2019-2020 and then a significant positive/deferred effect in 2021 (as we were able to “benefit” from a tax perspective on unrealized losses that were laid out in short positions in the Master account that we could recognize due to mark-to-market accounting), that effect was partially reversed in 2022, as losses were harvested back into realized/unrealized gains (on our short exposure).

I’ll wait on the final tally from our administrator, but I still expect to see an efficient/advantageous tax strategy moving forward. For existing partners, with a sizable (and hopefully increasing) level of gains embedded in our Core investments (held in the Feeder account…)— those gains will also ultimately become taxable upon being realized at some point in the future, however, that event is deferred and consequent tax-effect long- term in nature.

Summary

This letter has been long enough, so to leave off, I just want to restate the objective of Bumbershoot Holdings remains on maximizing long-term returns.

That focus centers around our ‘ quality over quantity’ philosophy to investing, which relies on fundamental analysis. Patience and discipline are the underpinning for our success.

I take the responsibility of managing a portion of your money extremely seriously and am grateful to have an incredible investor base that has acted like permanent capital since I started the fund. I continue to have the vast majority of my personal net worth co-invested in the partnership and am proud of everything we have accomplished.

We’re only just getting started…

I can’t wait to see where we go from here…

Sincerely,

Jason Ursaner, Managing Member, Bumbershoot Holdings

Footnotes

3 FTSE 100 Index -- https://www.ftserussell.com/products/indices/uk 4 BarclayHedge Hedge Fund Index -- http://www.barclayhedge.com/research/indices/ghs/Hedge 5 As a middle child, I don’t mind being a good Milford Man — neither seen nor heard… unless there is something I ought to say… I feel like I have something to say now… so I’m seizing the opportunity to do so -- https://arresteddevelopment.fandom.../wiki/...Milford_man 6 Collection of artworks from A Bug’s Life -- https://characterdesignreferences.com/art-of-animation- 1/a-bugs-life 7 “It’s not a bug, it’s a feature is an acknowledgment, half comic, half tragic, of the ambiguity that has always haunted computer programming.” -- https://www.wired.com/story/its-not-a-bug-its-a-feature/ 8 “I memorized one definition of ‘money’ from an economic textbook way back in 1966: ‘A medium of exchange and a store of value,’ it said. Well, yes, I suppose, although it failed miserably in the latter capacity in subsequent years.” -- https://www.pimco.com/en-us/insights/economic-and- market-commentary/investment-outlook/devils-bargain 9 “An aging population puts persistent downward pressure on the price level, real interest rates, and output. A novel feature of our theory is that it also recognizes the reactions of government policy. The central bank responds to falling prices by reducing its policy nominal interest rate, and the fiscal authority responds by allowing the public debt–gross domestic product ratio to rise.” -- https://www.atlantafed.org/.../research/publications/wp/2 022/09/29/12--why-aging-induces-deflation-and-secular- stagnation.pdf 10 And no… “ wen pivot ?” doesn’t count. 11 “Cross of Gold” -- http://historymatters.gmu.edu/d/5354/ |

| LEGAL DISCLAIMER This letter is provided on a confidential basis and is for informational purposes only. All market prices, data, and other information are not warranted for completeness or accuracy and are subject to change without notice. All performance figures are estimated and unaudited. Any opinions and estimates constitute a “best efforts” judgment and should be regarded as preliminary and for illustrative purposes. As of the publication date of this letter, Jason Ursaner, Bumbershoot Holdings LP, Bumberings LLC, and its affiliates (collectively “Bumbershoot”) may own, or have sold short, stock and/or options in companies covered herein; and stand to realize gains if the price of their issues change. Following the publication of this letter, Bumbershoot may transact in the securities of the companies mentioned. Content of this report represents the opinions of Bumbershoot. All information has been obtained from sources believed to be accurate and reliable, however, such information is presented “as is” without warranty of any kind—express or implied. No representation is made as to the accuracy, timeliness, or completeness of any such information. All expressions of opinion are subject to change without notice; and Bumbershoot does not undertake to supplement and/or update this report or any information contained herein. Any investment involves substantial risks, including, but not limited to: price volatility, inadequate liquidity, and the potential for complete loss of principal. This document does not in any way constitute an offer or solicitation of an offer to buy or sell any investment of security for any company discussed herein. Investors should conduct independent due diligence, in assistance from professional financial, legal, and tax experts, prior to making any investment decision. |

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Bumbershoot Holdings 2022 Investor Letter