BMBL - Bumble: No Moat Massive Dilution Make It A Sell

2023-12-01 11:34:32 ET

Summary

- Bumble, a popular dating app, has experienced a decline in its stock price since going public in 2021.

- The company's financials show mediocre cash flow for its current valuation.

- Bumble's main revenue source is its flagship app, but it faces challenges in a volatile social media market and lacks a strong competitive advantage.

Bumble ( BMBL ) is one of the best-known dating apps out there, perhaps second-best to the likes of Tinder. After working there, founder Whitney Wolfe Herd left and started Bumble in 2014 , with a mission of making the dating app experience friendlier and more appealing to women. The company went public not long ago in 2021. Since then, shares of Bumble have, well, bumbled , tumbled, and been humbled. Priced at high as $70 in early 2021, BMBL has more recently traded under $15. This fall, Herd announced that she will be stepping down as CEO, to work in the role of Executive Chair.

Bumble shows signs of a healthy company, taking into account both the titular app and its smaller holdings (the main one being Badoo). Nevertheless, I will make the case that various challenges and risks make it a poor investment and thus a SELL for current holders. These include:

- Volatility of social media

- Lack of a dating app moat

- Share dilution

Financial Data

Before getting to the qualitative aspect of this story, let's look at the financials. We'll start with Bumble's balance sheet.

{kind=link}

BMBL Q3 10Q

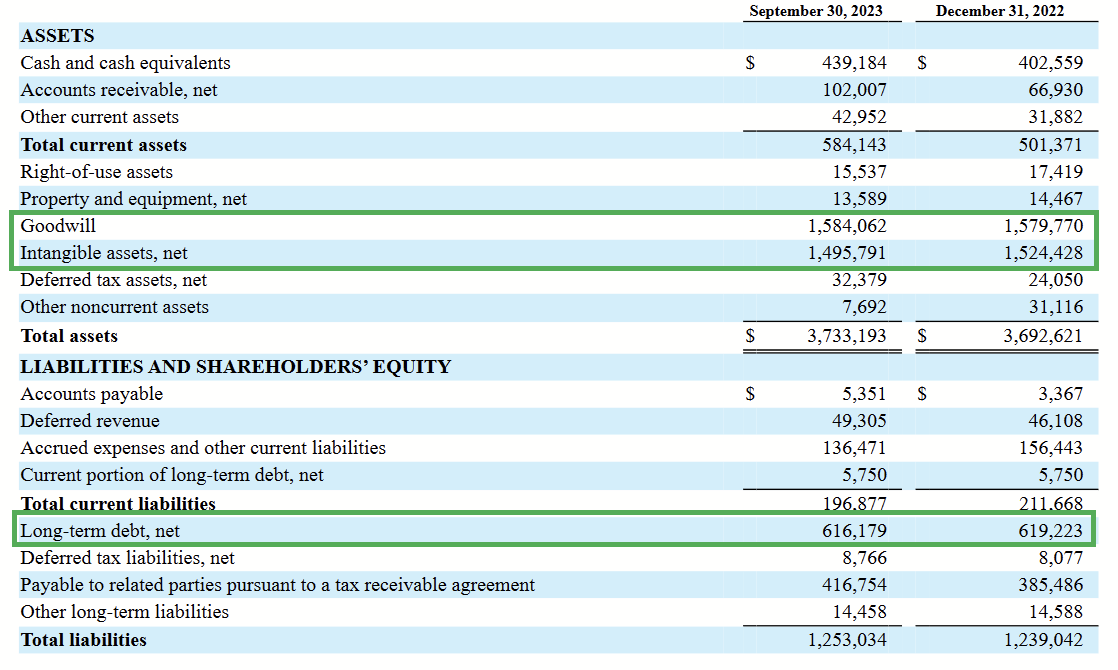

I indicated the parts that I think are important. While there are significantly more assets than liabilities, note how nearly all of these assets are intangible. Bumble has a decent amount of cash for debt repayments, but it's not a company that leaves much for shareholders in the event of a liquidation. Any workable investment thesis will require it to generate cash attractively . Let's take a look at its history there.

{kind=link}

BMBL 2022 10K

Their 10K (which I cropped for convenience) shows that their cash flows turned positive just before the IPO. Let's look at their capex for that same period.

{kind=link}

BMBL 2022 10K

Here we see capex largely stabilizing, while operating cash flows increase, suggesting annual free cash flow could easily be around $120 million. Of course, this requires us to assume that cash for acquisitions are not part of the consideration, and why shouldn't they be? Let's look at their year-to-date cash flows for 2023.

{kind=link}

BMBL 10Q

Okay, so it's somewhat on track for that same $120m range (being three quarters in). Let's get into the story behind those cash flows then.

Operations

Bumble is the flagship app, but the assets also include BFF, Badoo, Fruitz, and Official. As such, its cash flows derive from the revenues these provide.

{kind=link}

Company Presentation

Revenue Sources

Let's use slides the company recently provided in its Q3 2023 earnings presentation.

{kind=link}

Q3 2023 Presentation

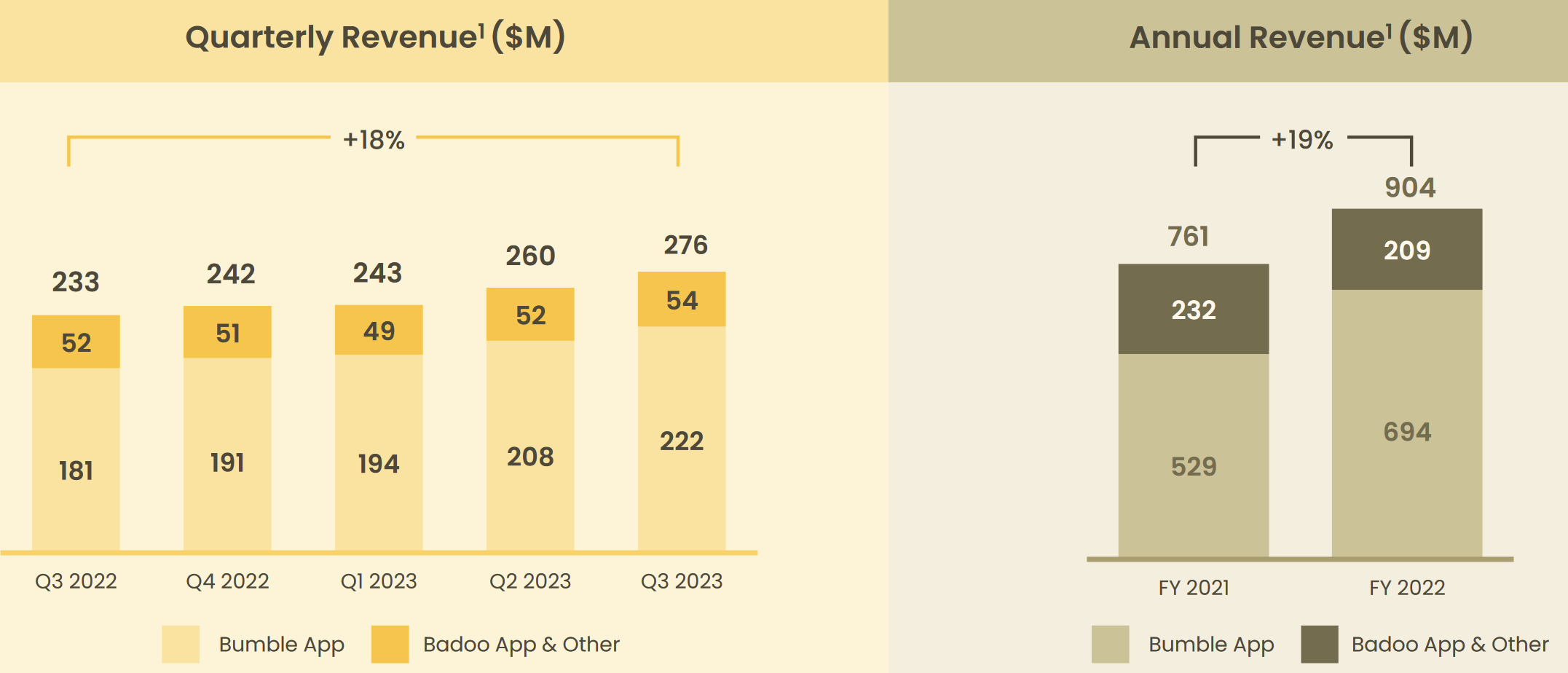

Here we see very clearly that Bumble is the dominant factor for BMBL's cash flows and where most of the growth is enjoyed. Let's look at the kinds of revenues those can generate.

{kind=link}

Q3 2023 Presentation

{kind=link}

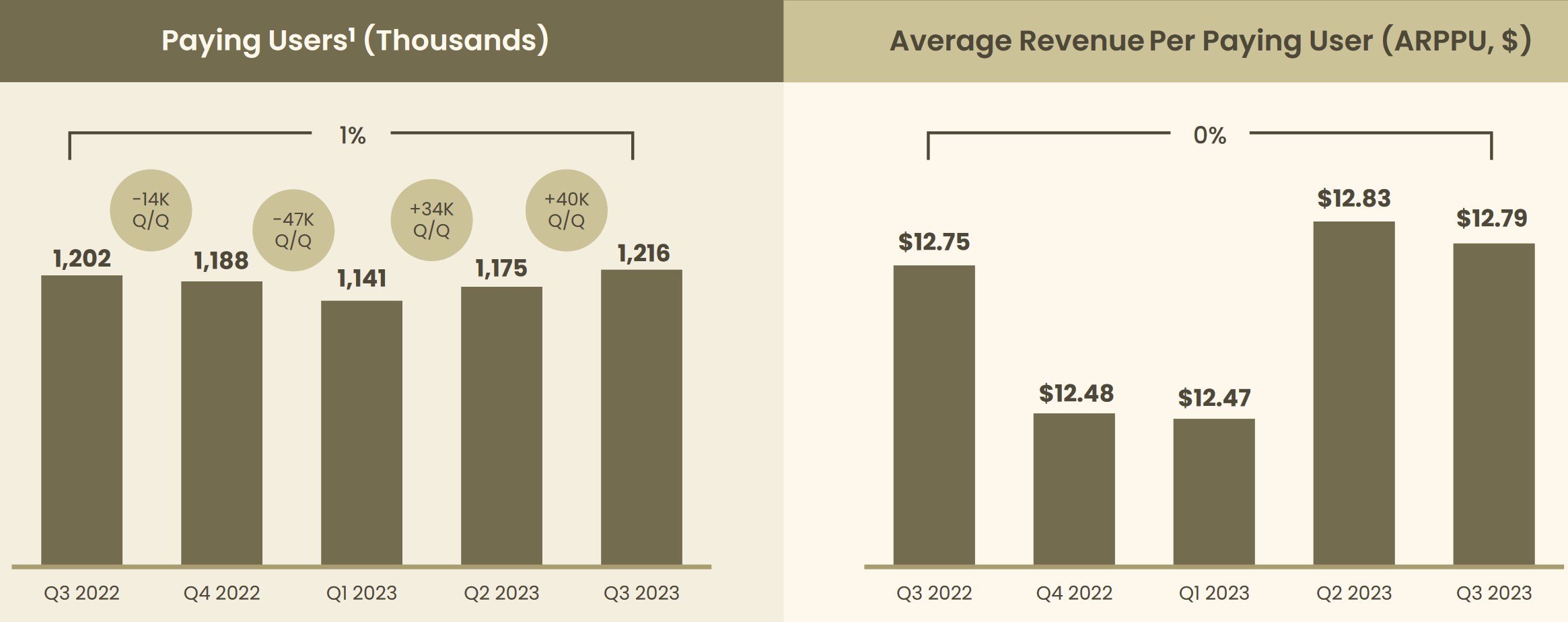

Q3 2023 Presentation

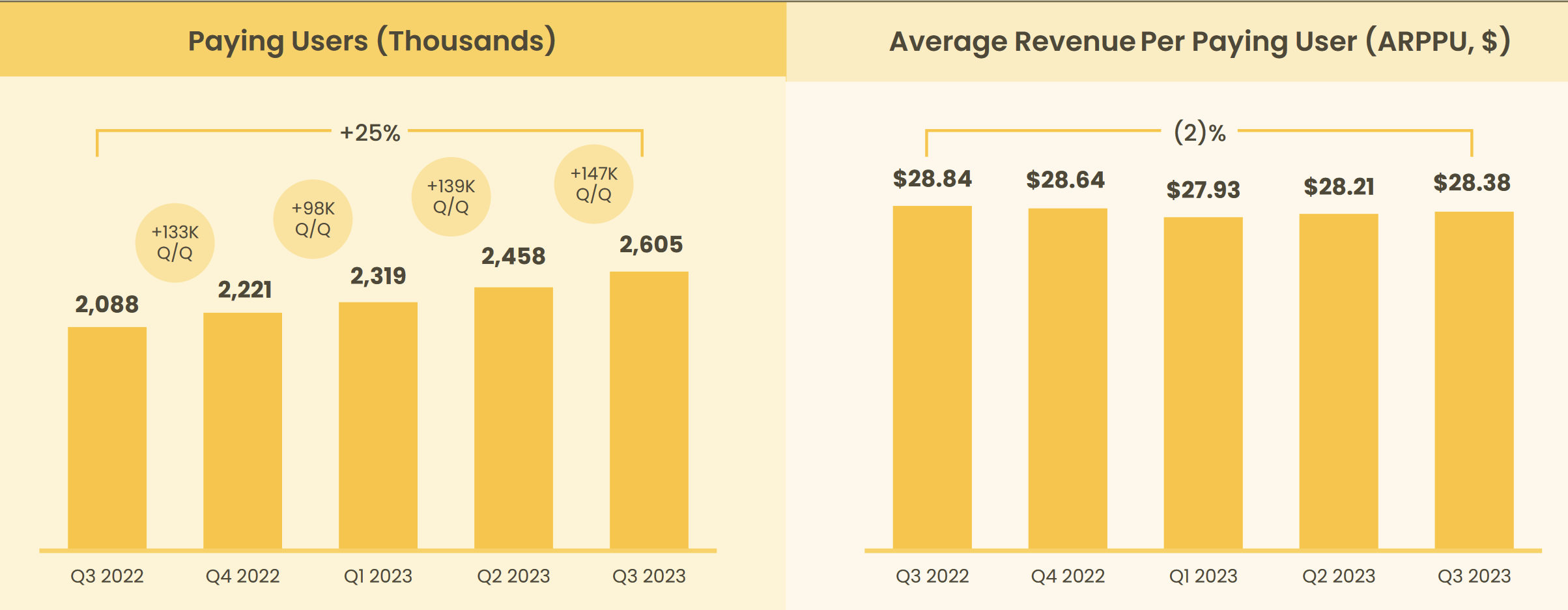

Here we can see that revenue per paying user doesn't fluctuate much. The real name of the game are the segments' abilities to grow cash generation by growing users.

{kind=link}

BMBL 2022 10K

Geographically, 60% of revenues come from North America.

Paid Subscriptions

What does a subscription on apps like these mean? Why is someone paying to use this? Well, it mostly just makes the app fully functional. You go from having a limited number of likes per day to having unlimited. You get more filters enabled to allow for better matches (which somewhat conflicts with being able to use more likes). You get more priority in other users' feeds. You get to see if someone liked you and immediately decide if you like them too (which causes a match to happen faster).

Understanding the value of a subscription is the key to understanding the cash flows of this company. This recent article provides some valuable insights on who is paying for dating app subscriptions and why. Here are some excerpts:

“When you pay, you’re going to do less work and find more dates — that’s what we’re trying to engineer,” said Mark Brooks, who has been a consultant in the dating app world from the beginning.

And:

“When we’re looking at dating apps as a group, they’re not adding new users anymore,” he said. “So if you can’t really add new users, you want to sort of optimize the ones that you’ve had.”

Age of subscribers:

Only about a third of those who use dating apps report paying for them, said Colleen McClain at the Pew Research Center.

“This is relatively more common among older users,” she said. “It’s also more common among people who are earning more money than people who are earning less.”

So we know that paid subscribers tend to be those who want to unlock more dating potential at a good price, are more often older users, and that new users aren't growing much in an industry that has been around for more than a decade now. The sexual demographic may provide better insights.

Male and Female Users

According to Emlovz , about two-thirds of Bumble's userbase is male. For an app oriented toward women, 2-1 may seem like a lot of men, but considering how they also report that Tinder's base is usually around 9-1 male-female, it's much more even.

The tricky thing here is that the true customers of dating apps like Bumble aren't women; they are men. Pew's own data show that it's men on dating apps who are disappointed by lack of engagement with female users, not vice versa.

PewResearch.org

Most female users are getting enough attention from men on these apps, largely due to the gender imbalance. A subscription, therefore, is a product oriented toward male users , and its value is how many more matches and dates it creates for them, which they lack.

I have to speculate a bit here, but my belief is that a subscription is only worthwhile to semi-attractive men. Attractive men are likely getting plenty of dates with the free service, so paying doesn't open any new doors for them. Other men, meanwhile, are getting zero, and paying to increase that amount by 30% (or whatever the Bumble prompt says) is still zero. If you are attractive enough to get one or two dates a month, then maybe paying to get that up to 4 or 5 is worth it.

For those reasons, whether it's Bumble or another app, only a small slice of total users are ever going to pay, and it's mainly going to be men. Those are the forces behind BMBL's current cash flows.

Valuation

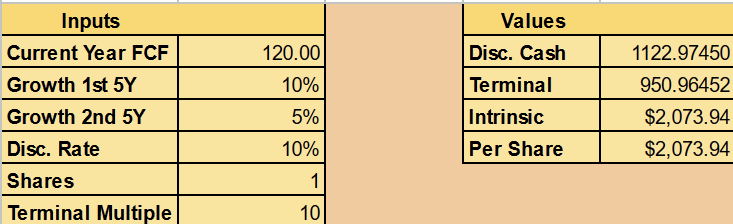

At this moment, we have enough information about the company to attempt a valuation. Let's do a Discounted Cash Flow valuation with these assumptions:

- Baseline of $120m in free cash flow per year from recent data

- 10% growth the first five years (based on recent growth trends)

- 5% growth the next five years as Bumble begins to saturate its accessible market

- A terminal multiple of 10 to allow for modest, future growth opportunities

{kind=link}

Author's display of calculation

This gets us to a fair value of just over $2 billion. The company currently trades for about $1.9 billion ( and it was over $13b before ), so maybe it's at least fairly valued for my discount rate of 10%. Yet, I believe this is a very optimistic outlook for the company. I haven't even dared to value the individual shares, just all of Bumble. Let's look at the various risks and concerns to see why I'm hesitant.

Risks

Social Media

Dating apps are part of the larger market of social media. A big part of Facebook's rise was a user's ability to list their "relationship status." Yet, as the fundamentals showed signs of age and decay, the share price got pummeled. The low barriers to entry for tech make this a danger to anybody in this space. This likely also factored into the Twitter board's decision to accept Elon's buyout last year; it relieved them of having to figure out how to create returns for holders of TWTR.

Bumble should not be seen as any different in this regard. It's very easy for the culture on a social media platform to become negative or at least become "behind the times" enough for a new player with a cooler experience to slip in and eat your lunch.

Dating App Moat

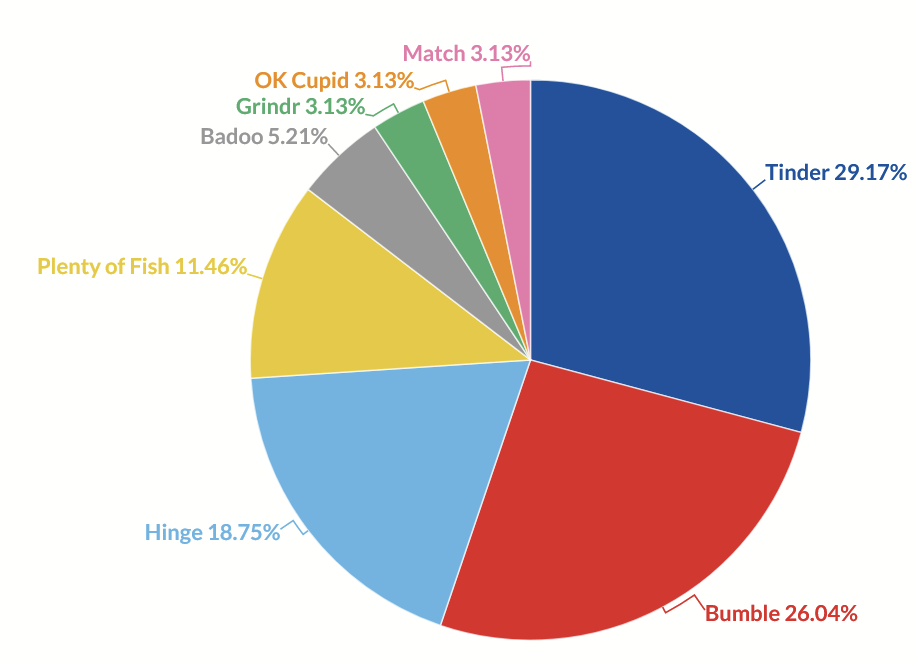

A "moat" in investing is a source of earnings for a business that can stand the test of time. It's a bit abstract, to be sure. With BMBL in particular we have to see where it falls in this dating app space. BusinessOfApps indicates that Bumble and Badoo account for about 31% of the US dating market share. They provide a handy graph here.

{kind=link}

BusinessofApps.com

You might think that Bumble + Badoo = More Than Tinder, but you'd be wrong. Match Group is the parent company of Tinder, Hinge, Plenty of Fish, OK Cupid, and (of course) Match. To the extent that dating apps can have a moat, it clearly belongs to Match Group. I find this concerning because Bumble's founder thinks they have a moat. Let's review what Herd had to say in the Q3 earnings call :

Yes. So I -- you know what, this is such a big piece of my excitement going into this step forward into the Executive Chair role. I am -- in my heart and in my skill set, I'm a marketer. I'm a brander. This is such a super power of ours and the unique brand that we have built up over the years.

And so we've said this once, we'll say it again. We have such a durable moat. And we really have loyalty with customers, with women that have never been seen before in any dating-related category. You don't really see dating app hats walking around the street.

And so the fact that we have a beloved community that want our merchandise, they want to integrate us into their wedding, they are proud of us, this is where we shine. And I'm going to put so much love, attention and care into this in 2024, take our brand to the next level, take our mission to the next level, create that evangelized beloved fandom around Bumble and Bumble for Friends.

While some nifty merchandise sales are a nice addition to cash flows and a form of free marketing, these are not a moat for a company whose primary operation is helping people find dates. I'm 32. When I was in college, Tinder was the main dating app that people were using. All these years later, Tinder has not been knocked off its rock. That's a moat.

Marketing isn't. Does anyone think Tinder even needs marketing? It's cute that Bumble has merchandise popping up at weddings, but who is the main customer in the wedding industry? Women. They planned it with their friends at slumber parties as girls. Who is the main customer on a dating app? Again, it's men , not women, and Bumble trying to be the friendliest dating app for women doesn't change this. If we can't be sure of a moat, can we be sure that there will be any cash flows in ten years for today's owners?

Dilution

A big influence on a single share's intrinsic value is not just cash flow but dilution. BMBL is huge victim of that. Let's look at the amount of stock-based compensation going on the last few years:

{kind=link}

BMBL 10K

These amounts are rivaling the company's free cash flow. Year-to-date for 2023 is a similar story.

BMBL 10Q

Total shares outstanding of BMBL have risen from 129.7m at the end of 2022 to 138m today. That's over 6%, and it could end up being 8% for the whole year.

{kind=link}

Fidelity.com

With BMBL constantly declining since the IPO, this also means that the rate of dilution from share-based compensation is picking up. To get the same level of value from a lower share price requires the employer to give up more shares. This can have a runaway effect where sufficient dilution drives the price down even further and requires even more dilution.

This rate of dilution competes with what I believe to be optimistic estimates of growth. Even if the cash flows do grow between 10% and 5% over the next decade, it's effectively zero from this. If the cash flows fail to grow at all, then it's a long-term loss for individual shareholders.

Conclusion

Bumble is an excellent company by many measures. It successfully defied Tinder with its women-driven team and mission statement, capturing almost a third of the dating app market in the U.S. and maturing into a cash-flow-positive operation. Herd's company has probably also helped thousands of people find their own true love.

With that said, shares of BMBL have declined in value significantly since the honeymoon of the IPO. The chaotic and cutthroat nature of the dating app market and the social media industry broadly make its future cash flows uncertain, and even optimistic growth assumptions make its current valuation of $1.9 billion dubious.

I could have given more reasons about the grim prospects here, but these should be enough for any responsible investor. BMBL is not a buy, and for folks that currently hold it and care about long-term returns, it's an easy SELL.

For further details see:

Bumble: No Moat, Massive Dilution Make It A Sell