KIND - Bumble: Swipe Right On Growth

2023-07-25 23:26:17 ET

Summary

- Bumble is an industry leading online dating platform that has seen strong user and revenue growth since its IPO in 2021.

- BMBL operates three dating apps, Bumble, Badoo, and Fruitz, and has shown strong secular growth and brand awareness since launch.

- The company has significant international growth prospects, industry leading ARPPU metrics, and business model expansion initiatives.

- Despite stiff competition and the potential of a recession, BMBL has geographic, strategic, and new product growth plans taking shape.

- I view the current share price as undervalued, with a weighted average price target implying a 36% premium to the current share price.

Thesis

Bumble Inc. (BMBL) represents a leading online dating and social networking platform that has experienced strong user, revenue, and organic growth since it IPOed in in 2021. According to Grand View Research , the global online dating industry is a nearly $10 billion industry and is projected to grow at a compounded annual growth rate ((CAGR)) of 7.4% from 2023 to 2030. Within that, Morgan Stanley estimates that industry revenue in United States was approximately $2.6 billion in 2022.

BMBL operates three apps, Bumble, Badoo, and Fruitz and employs a freemium business model, where basic services are free and a smaller subset of users pay for subscriptions or in-app purchases to access premium features. Fruitz was acquired in January 2022 and has a Gen Z focus. In 2022, BMBL served an average of 40 million users on a monthly basis, was ranked top five grossing iOS lifestyle apps in 109 countries, and has 950 employees. The company is well-known for its core ethos, brand, and culture of ‘women-first’ and its popular Founder and CEO, Whitney Wolfe Herd.

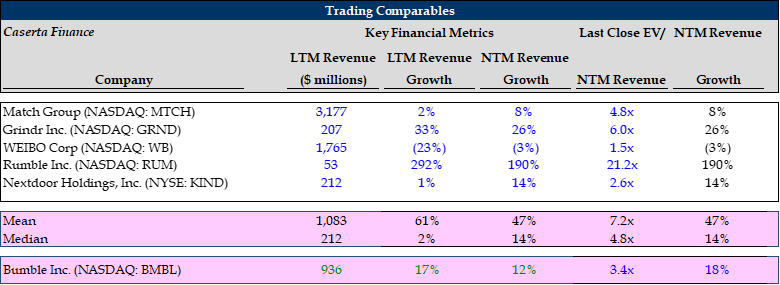

BMBL operates in a highly competitive, low-barrier to entry market that has two public company competitors, Match Group, Inc. ( MTCH ) and Grindr Inc. (GRND), and many privately held competitors who operate in the same space and have similar business models. Despite the competitiveness of the industry, I believe BMBL has entrenched itself as the number two in the space as measured by revenue, only behind MTCH (BMBL LTM revenue $936 million versus MTCH’s $3,177 million), with stronger growth revenue, user, and international growth prospects ahead.

My weighted average NTM price target for the stock is ~$29, implying a 36% premium to the current share price at the time this analysis was written. My analysis will cover various catalysts that I believe will be accretive to the current share price, including BMBL’s international growth prospects, paying user growth, ARPPU strength, and business model expansion initiatives.

International Growth Prospects

Bumble has built a sizable and growing international portion of its business over the last several years, and I believe we are in the early innings of how much further the company can expand into other regions.

According to public filings

To start, in the most recent two earnings calls, both Whitney and Tariq Shaukat, President, have acknowledged the company’s focus on expanding into Western Europe, Latin America, India, and Southeast Asia. However, the team highlighted that there is a prioritization occurring in Western Europe, Italy, the Nordics, and some parts of Central Europe because they have seen rapid growth in their data analytics. Additionally, the company launched in Spain at the end of 2022, meaning that the impacts of these regional expansions should show up in the financials in the coming quarters.

Bumble’s international growth has been growing at 11% or more on an LTM basis over the last six consecutive quarter, and represents 40% of sales. While the bulk of the remaining 60% of revenue comes from North America (primarily US and Canada), the company has plenty of open space ahead. I put together an illustrative example of how BMBL has potential to grow and scale their international presence over the course of the next 12 to 24 months.

Author's representation

In the analysis above, I estimated BMBL’s current LTM Payer base in North America and internationally using MTCH’s existing payer and revenue metrics. I was able to estimate that 50% of BMBL’s payers are international and calculated a 9% discount between MTCH’s North American and international ARPPU metrics. I then applied the 50% international payer estimate, the 9% international APRU discount, and an additional 25% discount to the difference between MTCH and BMBL’s LTM payers of 28,730, to arrive at $570 billion of upside.

Not only that, but I also found that the difference in ARPPU of 76% between MTCH and BMBL suggests that BMBL is more effective in converting users to paid and delivering more value per user than its larger peer. While I believe that BMBL’s ARPPU will likely diminish over time, I think that BMBL will continue to steal share and wallet from Tinder over time and in more geographies as it catches up to MTCH’s scale.

Paying User Growth

User growth for Bumble’s flagship application has consistently been north of 31% on a quarter over quarter basis – an impressive feat as it recently crossed the 2.3 million paying user mark in 1Q23. The bad news? Badoo’s paying user base has shed users 10% on average for the last five quarters, stunting total user growth for BMBL. The chart below details BMBL’s user metrics split out by both Bumble and Badoo over the last five quarters.

Author's representation

The takeaway? BMBL’s more profitable application, Bumble (LTM ARPPU $29.37), is outpacing the lesser profitable and declining user base of Badoo (LTM ARPPU $14.59). Should the company continue to ramp Bumble’s user base from 2.3 million users closer to MTCH’s high point of 16.2 million users, the potential upside is attractive. That, coupled with turning around Badoo’s shrinking and lesser profitable user base, and the growth of its newly acquired Fruitz application, to me represents potential upside outside of its core application.

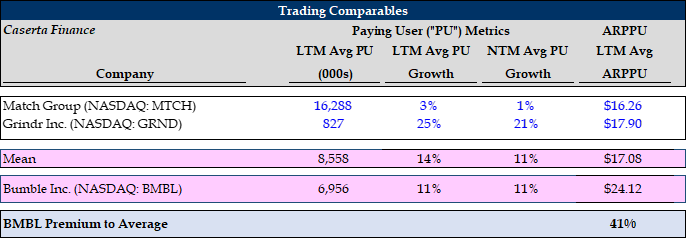

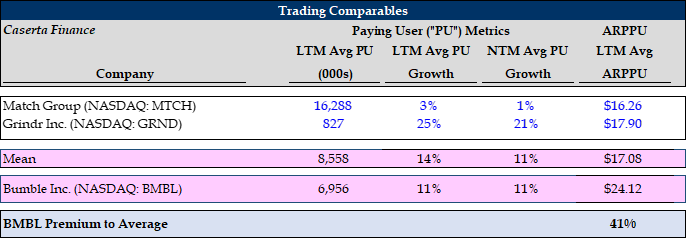

I also compared BMBL’s LTM average paying users to that of both MTCH and GRND and found that BMBL sits in the middle of the pack in terms of paying users, LTM average paying user growth, and NTM average paying user growth. What struck me most was how much higher the LTM average revenue per paying user ((ARPPU)) BMBL’s was of $24.12 relative to the median of the compset of $17.08. The difference amounts to a 41% premium that BMBL is getting above competitors and therefore, as I will show later, should be factored into its valuation.

{kind=link}

ARPPU Strength

Bumble has built, maintained, and stabilized an industry leading ARPPU of $24.12 for all brands. Despite both Bumble and Badoo experiencing declining ARPPU growth in 3Q22, company has sustained positive year-over-year total ARPPU growth in each quarter since IPO. The strength of the company’s ARPPU will certainly be tested over the next several quarters as competition continues to heat up. However, the strength in ARPPU to date across brands continues to lead the pack and should warrant highly valuations relative to competitors. The analysis below displays the ARPPU for BMBL by brand.

Author's representation

Another key point to note is the ARPPU of $27.93 for Bumble, ahead of online dating competitors MTCH, $16.26, and GRND, $17.90. The premium of 41% that BMBL has over its competitors on a per user basis is stark and, in my view, should be considered when valuing the business. More on that later. See analysis of the paying user and ARPPU metrics below for BMBL, MTCH, and GRND.

{kind=link}

Business Model Expansion

BMBL monetizes via (i) subscription offerings called Boost and Premium, which offer daily, monthly, and lifetime packages, (ii) in-app purchases including Spotlight, SuperSwipe, and the newly added Compliments, and (iii) video and banner advertising. In the latest earnings call and in recent months, BMLB has made a push to roll out new features to boost monetization and increase revenue generation pathways.

As a first step, BMBL rolled out the ‘ Compliments ’ feature in 4Q22 as a new message-before-match as another way for users to engage and potentially convert to paying users. The results of Compliments are hard to track and will be difficult to measure, though in recent news, there has been a fairly extensive amount of coverage on the success of the new feature in recent months. If the company can continue to innovate, experiment, and push new features out for users to engage with, BMBL may be poised for future growth.

Additionally, a unique competitive product that BMBL has secured the lead in, from my perspective, is Bumble BFF . There are no other highly successful and sticky platonic friendship applications that have been able to show as much promise as Bumble BFF has had to date. The exciting strategic avenues BMBL can take with expanding and monetizing on an app to find friends remains to be seen. In June, Bumble reported its plans to launch a separate BFF app to help people find friends in the U.K and select Asian markets as a pilot.

Lastly, BMBL’s foray into large-scale partnerships with large corporate brands – specifically with the new Barbie blockbuster movie – may, in my view, provide a significant boost in brand awareness. The marketing push by BMBL to partner with Barbie while boosting visibility of BMBL’s new Compliments feature may lead to outsized downloads, paying users, and revenue in the near term. That, coupled with the bigger strategic shift to partnering with larger corporations, has the potential to lead to advertising revenue that the market currently is not accounting for.

Valuation

It should be noted that the overall shakiness of the market, and specifically technology companies, puts this investment at high risk due to potential recession warnings. With that being said, all else equal, I view the stock as being undervalued today and having room to run in the short term. Specifically, I see BMBL’s international growth prospects, industry leading ARPPU, and business model expansion initiatives as catalysts for upward stock price movement ahead of expectations.

{kind=link}

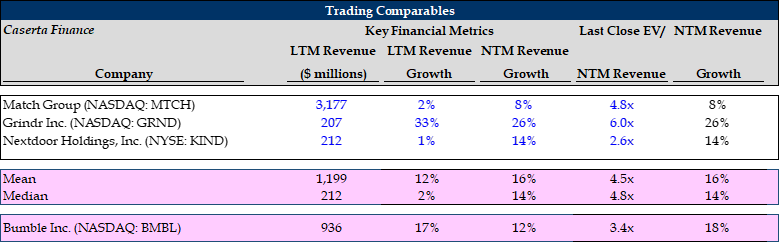

In the peer comparison table of BMBL above, I used technology companies with similar business models, user dynamics, and key metrics. However, I had to pull out WB and RUM due to their vastly disproportionate decline and growth trajectories, and as such, re-ran the comp set removing the aforementioned names and provided the table below.

{kind=link}

BMBL stands out from the peer set by having better LTM and NTM revenue growth expectations relative to both the mean and median of the comps. What’s more, the company is currently valued at 3.4x EV to NTM sales, a full multiple less than the comp set average of 4.5x. This mismatch struck me as a key point to consider when valuing BMBL, and one that supports the thesis of the name being undervalued. I chose to use EV/NTM sales because the company and some of its competitors are not yet profitable or have high fluctuations in EBITDA and FCF, eliminating and distorting other valuation methods.

Author's representation

I see 36% upside from today's share price, factoring in highly conservative downside, base, and upside scenarios. I see the company's efforts in geographic, ARPPU, and business model expansion providing tailwinds to the stock price in the short term. My proprietary weighted average price model I built is based on Paying User, ARPPU, geographic, and business line growth models as previously described. Additionally, and perhaps more importantly, I used the average EV/NTM revenue multiple in the base case and adjusted in both the upside and downside scenarios to reflect modest fluctuations in multiples. At a blended rate, the upside relative to current valuation is worth considering.

Risks

The dating industry is highly competitive, with low barriers to entry and many new products and features being constantly rolled out. As with any technology stock, the fluctuations in stock price amid market uncertainty, which we are currently facing, present further risk to this play. Below I will highlight several other potential risks.

To start, I view a slowdown in general macro environment as a catalyst that may lead to paid user declines. As cash strapped consumers watch their budget, expenses for dating will be cut alongside the costs of going on those dates which may include entertainment, food, beverage, etc. However, this risk is partly mitigated by my hypothesis that during financially difficult times or not, people will want to find matches and also may find themselves having more time on their hands to meet people if they have been laid off.

Secondarily, I see the potential for decelerating ARPPU as a threat to the thesis as more entrants, lower cost competitors, and cheaper alternatives chip away at BMBL’s lead. This risk, in my view, can be mitigated by BMBL’s extremely powerful ‘women-first’ ethos that has resonated with consumers to date.

Last, the various bets in monetization strategies may not only turn out to be a resource sink, but they may run the risk of turning off users. As the market gets saturated with online dating behemoths who are clearly attempting to monetize the users who got the company to where it is today, the risk of consumer sentiment shifting away from online dating becomes more real. However, this risk I believe is slightly lessened by BMBL’s perceived efforts in creating edgy, engaging new products and features distinct from competition.

Conclusion

BMBL has developed a strong brand and reputation as an industry leader in online dating, backed by leadership of Whitney Wolfe Herd and supported by millions worldwide. The cult-like following has led to highly profitable user metrics, a healthy balance sheet ($235M of net debt), and strong growth prospects relative to peers. Even though the company’s share price has fallen from its peak share price post-IPO of $75 per share in 2021 and competition has stiffened, I see a lift in share price in the short-term – assuming the entire market avoids a recession – fueled by BMBL’s efforts to grow internationally, maintain industry-leading ARPPU, and expand its business model through strategic partnerships and new product features.

For further details see:

Bumble: Swipe Right On Growth