BBRYF - Burberry: Good Progress Competitive Multiples

2023-09-26 00:30:47 ET

Summary

- Burberry's share price has been lacklustre recently, which is in stark contrast with its healthy trading update. Its same-store sales rose by 18% in Q1 FY24.

- These were driven by China's recovery, which more than made up for the pullback in sales from the Americas and even some softening in the European Market.

- My forecasts based on conservative revenue growth estimates indicate a competitive forward P/E, indicating further upside.

Since the last time I wrote about the British luxury fashion company Burberry (BURBY) in May, its share price has seen a small correction of 2.6%. This is hardly any movement over five months, and it's in line with what I had expected then. I was "on the fence about it short-term future of its price", clearly, other investors felt the same. But its medium-term still looked promising, prompting a Buy rating.

The company's progress since indicates that it continues in the right direction. But first, a quick recap of where the company was at when I last checked.

Quick recap

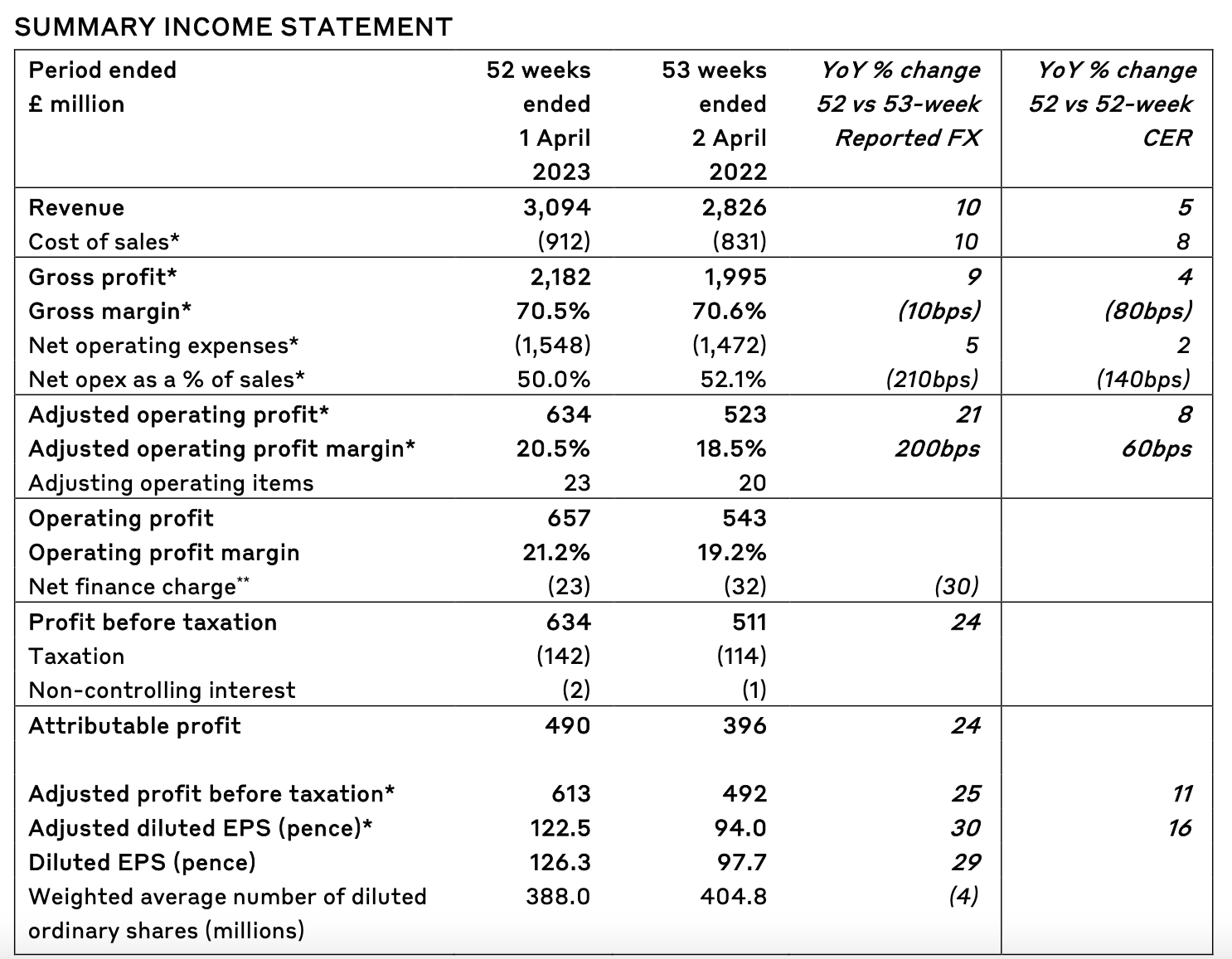

For its financial year ending April 1, 2023 (FY23), the company's same-store sales rose by 7% year-on-year [YoY], with a nice uptick to 16% in the final quarter, on China's recovery. Revenue growth in reported terms at 10% wasn't bad either, though it lagged in constant currency terms. Its operating margin pushed past 20%, notably as it actually managed to reduce operating expenses even at a time of high inflation.

{kind=link}

Looking forward, it targets a GBP 4 billion revenue in the medium term, which translates into a 9% annual growth up to FY26. In FY24 it expects an even higher "low double-digit growth". Burberry also expects to sustain its adjusted operating margin at 20%.

Recent progress

So far, Burberry's new creative designer Daniel Lee, certainly seems to be making his mark. Just last week, his just released latest collection received some good reviews . The big question though is, can they translate into better sales? Its numbers up to Q1 FY24, ending July 1, certainly indicate that it's on a good path.

{kind=link}

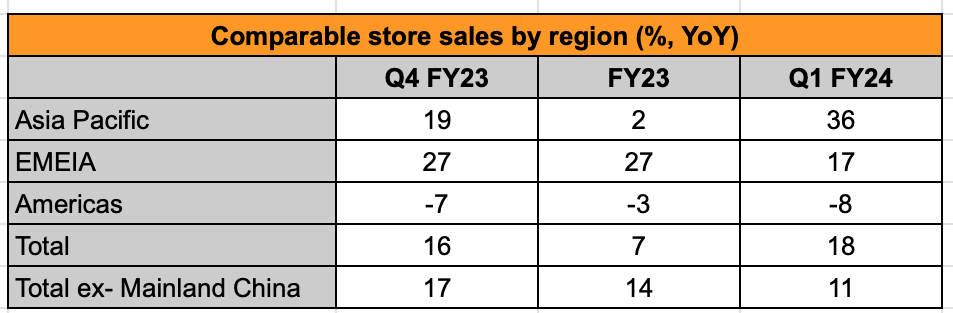

Its same store sales were up by 18% YoY, with significant support from mainland China which grew by 46%. This more than made up for the 8% decline in the Americas market, which continued the weakening trend from last year (see table below). Europe was resilient too, though it has seen a softening from FY23.

Outlook for FY24 and market multiples

Going by its forecast of "low double-digit growth" though, the next quarters are likely to show a softening in revenue growth. For the full year FY24, I have conservatively assumed no more than an 11% reported growth. I have also assumed that its net margin stays the same as in FY23 at 15.8%.

This translates into a competitive forward price-to-earnings (P/E) ratio of 13.6x. This is lower than other analysts' estimates, which give a ratio of 15.5x but it's also lower than that for the consumer discretionary sector at 15x. Even other analysts' P/E ratio isn't significantly higher than that of the sector. Considering that Burberry is a luxury brand, which can be more resilient than the average consumer stock in a slowing economy, I believe some premium is fair.

Next, consider it's trailing twelve months [TTM] GAAP P/E is at 16.3x, which is lower than the 18.3x it was at the last time I checked. Further, it's also lower than its own historical average of 23.4x .

What's holding Burberry back?

The question then is, why despite strong performance and attractive market multiples, has the Burberry stock gone nowhere in the past months?

Broad luxury weakness further

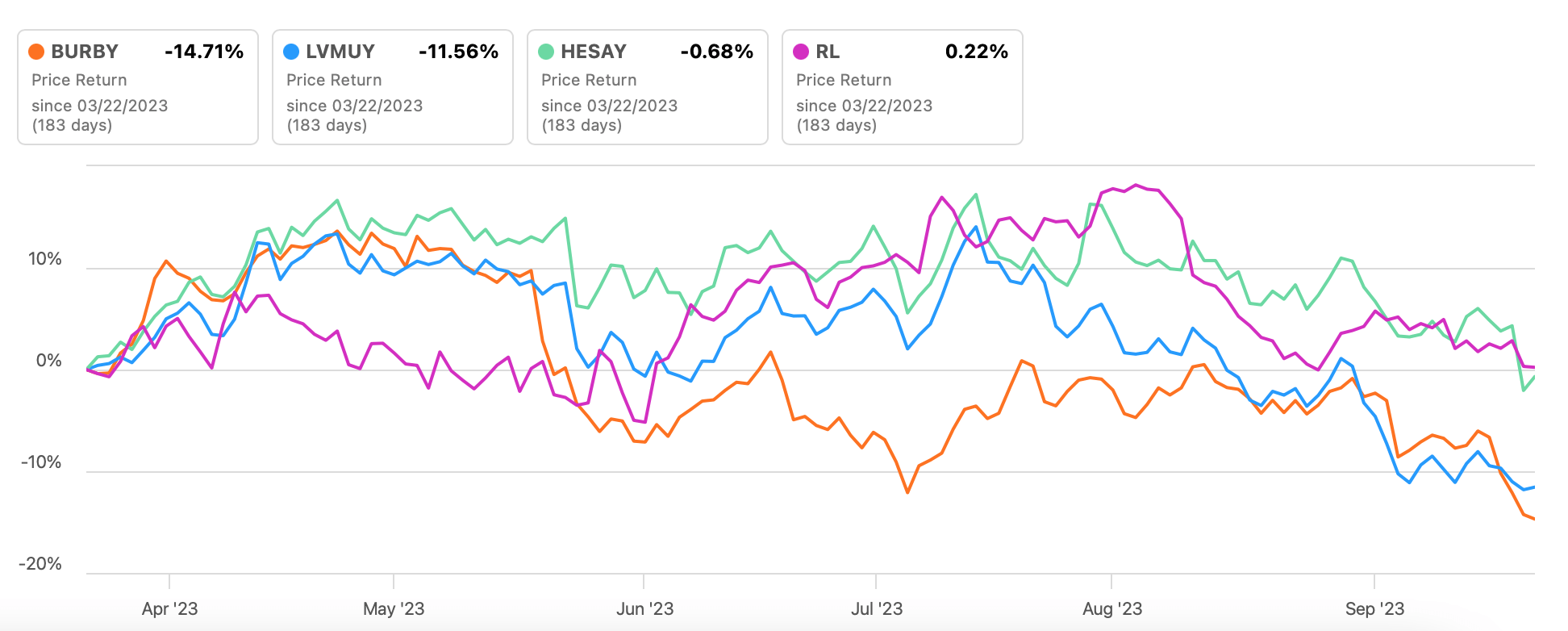

The stock needs to be seen in the context of the larger luxury set. The chart below shows the performance of high-end luxury fashion companies like Hermès (HESAY) and LVMH Moët Hennessy (LVMUY) and the affordable luxury company Ralph Lauren ( RL ) on the other hand. Burberry sits somewhere between this spectrum.

{kind=link}

All the stocks have been lacklustre over the past six months. Burberry has actually performed the worst of the lot, which is in stark contrast with its financial performance, though LVMH comes close.

US and EU markets can weaken

I believe that macroeconomic uncertainty is holding them back. The US market has been weak this year, which is evident from shrinking luxury sales in the market across companies. With growth expected to be weak next year too, the trend can continue. While the US isn't typically the biggest market for luxury companies, it still has a substantial share. For Burberry, for example, the Americas have a share of 24% as of FY23 (see Page 24 of the link).

Additionally, the European market while still quite strong, is softening too, as evident from Burberry's latest numbers. It could slow down further according to economic growth forecasts. The European Commission has revised down both 2023 and 2024 growth projections for the EU economy to 0.8% (Previous: 1%) and 1.4% (Previous: 1.7%) recently.

The China wild card

But the biggest risk is a slowdown in the big China market. There are already concerns about it, with some even wondering if it's a " ticking time bomb ". These questions arise from its weak real estate sector, relatively subdued industrial production trends and its deflation.

At the same time, it needs to be noted that its overall growth is still strong. In Q2 2023, it grew by a healthy 6.3% , accelerating from the quarter before. So it can well continue to support luxury demand in the coming months.

What next?

There are definite risks to the Burberry stock right now, going by investor diffidence about the luxury sector as such. At the same time, its own financial performance is looking good so far, with a boost from Chinese consumers.

Its outlook for FY24 also looks reasonable, even factoring in possible softening in the next quarters. And with its operating margin already having touched its medium-term target in FY23, it looks good profit wise as well. In fact, with the continued decline in inflation and its own ability to restrict expenses, its margins may well expand now.

At the same time, its market multiples don't look bad either. My FY24 estimates indicate that its forward P/E is actually lower than that for the consumer discretionary sector. Typically, I'd expect a premium on a luxury stock like Burberry considering that the segment tends to be more resilient than the average consumer stock in slowdowns. It's TTM P/E is lower than the historical average too.

The stock may continue to stay weak in the short term, but I think it's still a good time to buy it with the medium term in mind. If anything, its recent progress only confirms my earlier rating. I'm reiterating a Buy on Burberry.

For further details see:

Burberry: Good Progress, Competitive Multiples