BURBY - Burberry: I Don't Think The Premium Is Worth It At This Time

Summary

- I look at a few consumer discretionary companies, and my favorite are the conglomerates/businesses that own a whole host of very appealing brands, like LVMH.

- Burberry is a fashion business that generates relatively small revenues of under £3B per year - but it has a not-uninteresting sales and geographic mix.

- I'm looking at Burberry and showing at what valuation I would consider the company interesting as a longer-term investment for my portfolio.

Dear readers/followers,

Almost everyone knows Burberry ( BURBY ), or has at the very least heard the name once or twice. The company is a fashion business in what they're calling "Modern British Luxury", especially with the strategy update that began in 2022 and onward. In recent history, the brand has been somewhat fragmented in its design and appeal, and they're looking to get back on point and to their roots - the "Britishness" of things, as it were. This refocused brand image, together with establishing a leather goods business, is going to bring the company's various categories to their full potential - at least, that it what the company seems to be expecting and working toward.

Let's see what the company is, what it offers, and what we can expect from investing in Burberry over the next few years.

Burberry - The company from A to Z

Burberry is a luxury brand from Great Britain that has a 160+ year history behind it, with headquarters in London. The company is most famous for its trench coats, as well as ready-to-wear, leather accessories, and footwear products. Burberry also has licensed fragrances to Coty (COTY), which also includes cosmetics, as well as Luxottica for eyewear.

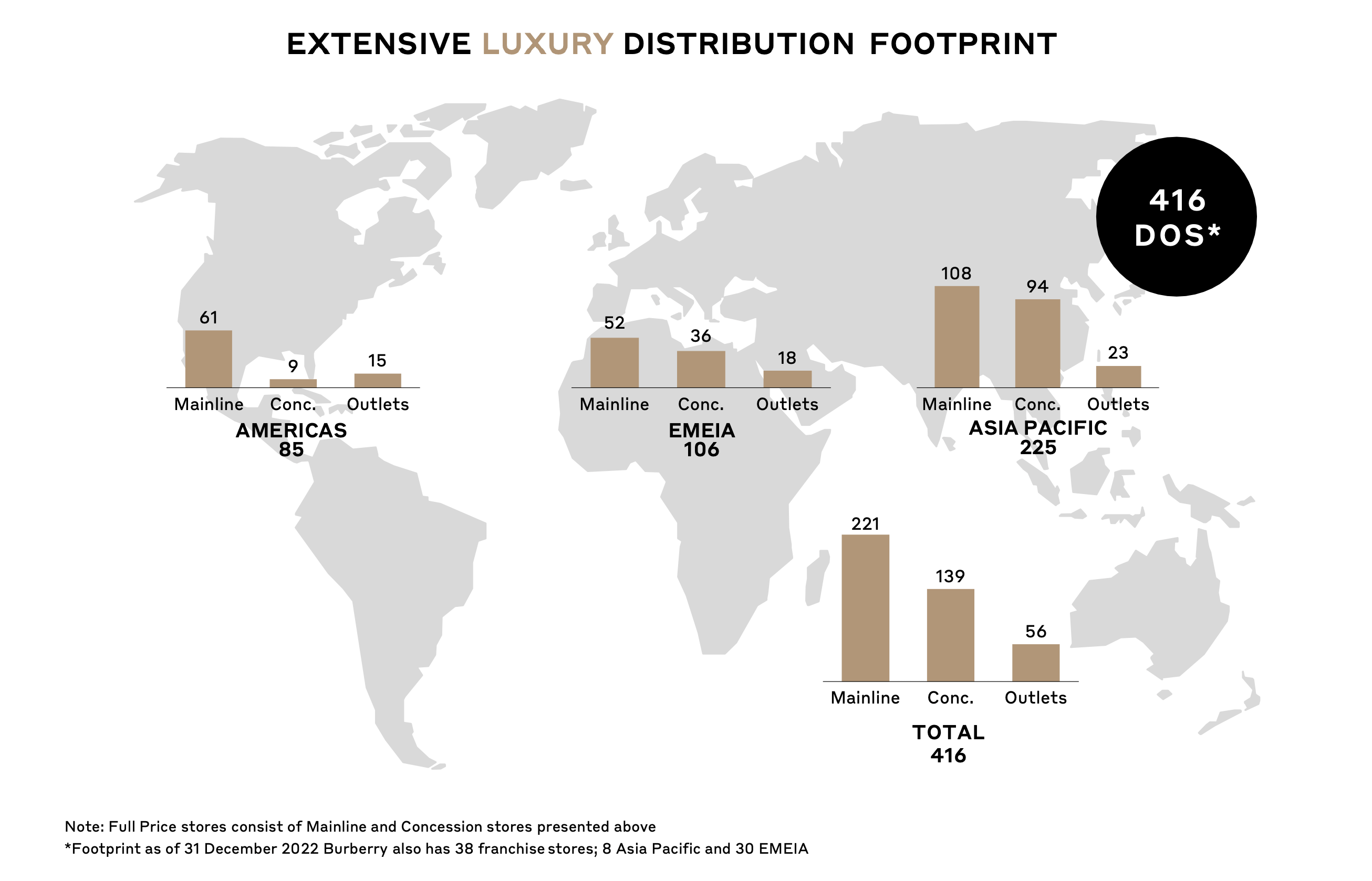

The company has over 410 locations as of today. The company has an investment-grade credit rating, and it pays a dividend of around 2%, which is somewhat higher than some of the other European luxury companies.

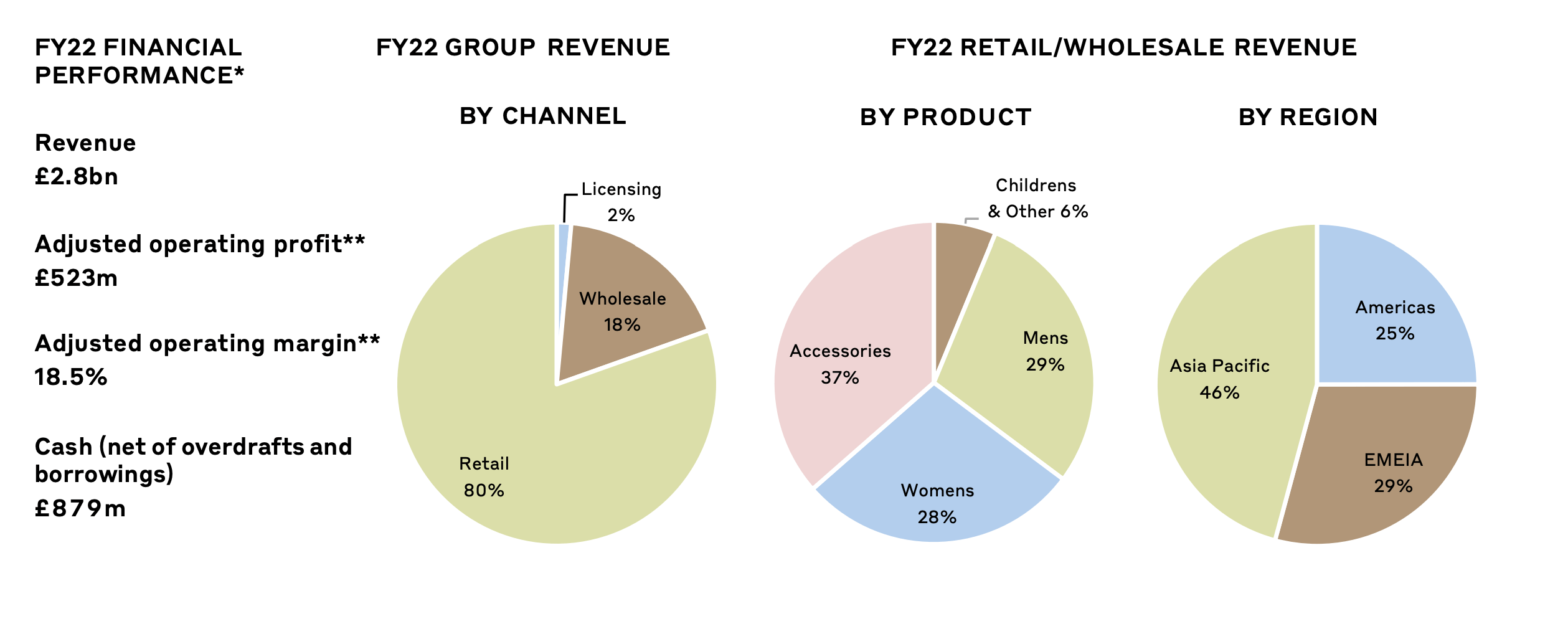

The company has an interesting sales split, with 80% retail and 18% wholesale, as well as 2% licensing. Unlike some other luxury brands, this one is very evenly split by product.

{kind=link}

The company has an impressive distribution footprint, mixing mainline, concession, and outlet stores across the world.

{kind=link}

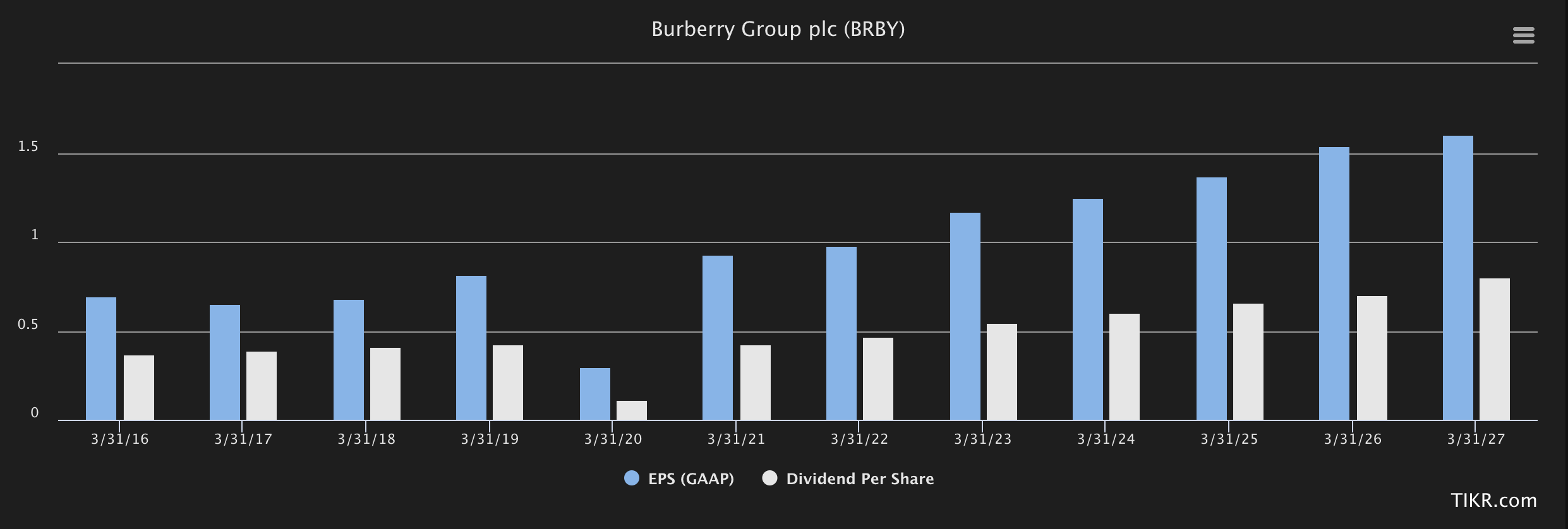

Burberry has been through a couple of pretty rough years. Earnings have been declining more or less since 2015, with single-digit and double-digit earnings declines with exceptions in 2018, with a 10% earnings increase. This turned around last year - with a 2022 adjusted EPS increase for the ADR up 23%, a clear beat here, and the current expectations are for high single-digit to low double-digit EPS growth in the near term.

The native ticker for Burberry is BRBY on LSE - and here is the positive for the company. The earnings expectations going forward from here are absolutely amazing, and something we haven't seen for several years.

{kind=link}

Some of these earnings increases are supposed to be coming from slight margin increases, and some of them are from sales volume increases. I personally believe that these forecasts are slightly more positive than we should be considering or expecting - but more on that later.

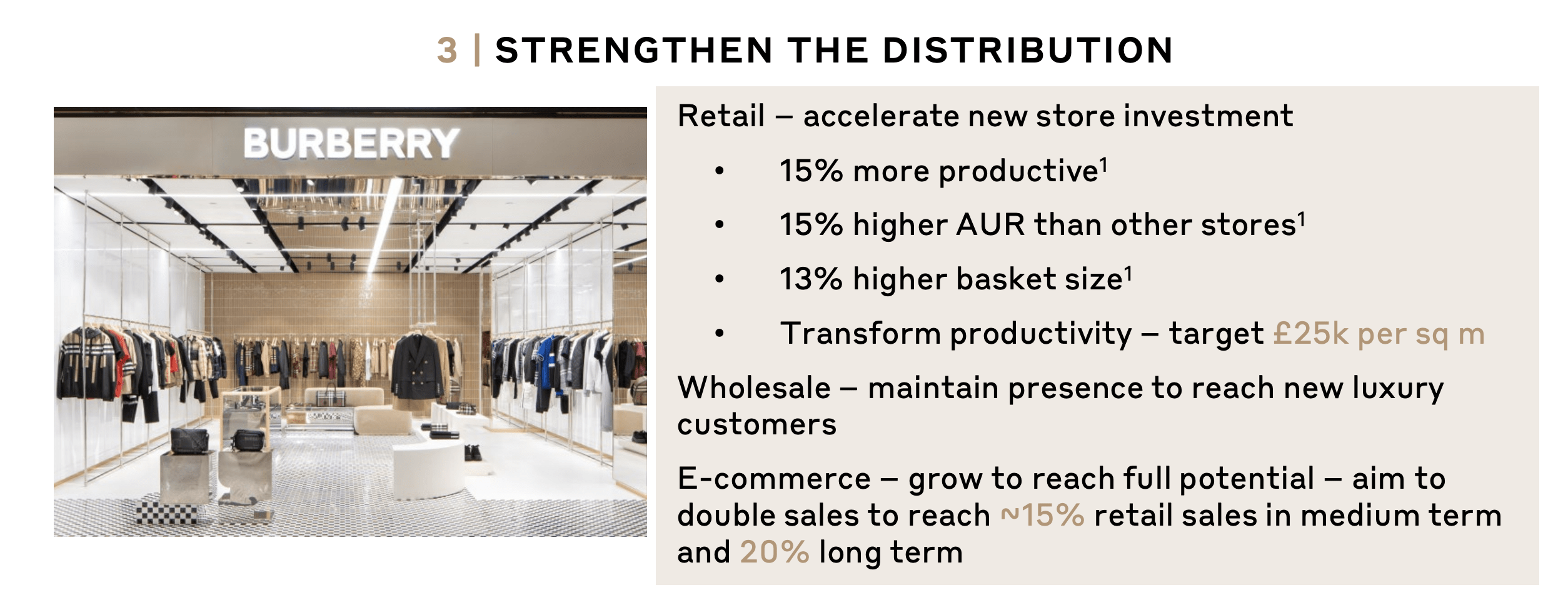

The company is making some strong moves. With the establishment of its leather goods segment, remodeling stores and upgrading the network, cleaning up wholesale, working with efficiencies, improving the clarity, and really focusing back on its roots, I think the company will see some success here.

Burberry is targeting a full £4B revenue in the medium term, and wants that 20%+ adjusted OM, which wouldn't be far from LVMH and other "better" companies in the same segment. The company expects higher sales in leather goods, shoes, and women's RTWs, as well as more outerwear sales.

All stores are going to be converted by FY26 at the latest, where the company is trying to improve productivity on a store basis, with better retail penetration and more e-commerce.

Burberry's ambition is to become a £5B brand in the long term, and they believe this can be done by focusing on its brand tradition and image.

{kind=link}

Burberry's target customer is 15-45 (men/women), and come in the form of students, working youth, Business people, Models, Artists, and Pros. The company targets an income segment from Middle income to High income, with a focus on fashion-conscious and lifestyle-oriented individuals with an appreciation for British style.

I personally am not a big fan of the style and the way Burberry is trying to achieve its goals. As I've mentioned in my LVMH ( LVMUY ) articles, I'm actually a bit of a luxury shopper, in several segments (Clothes, watches, etc). Burberry does not often appeal to me. While its core traditional products like the trenchcoats are something I could see myself wearing - especially the heritage series - the brand doesn't often resonate with me. I personally prefer to buy products from a brand where it is the "expert" in the field and tends to ignore the ancillary segments it tries to get into.

For instance, I use a Montblanc 149 Meisterstück Fountain Pen (several actually) in my personal writing, signing, and the like, but I wouldn't buy the Montblanc Fragrances, Watches, accessories, or other products. Having spoken to like-minded consumers, I will say that my stance isn't unique in my age demographic and income tier - and I'm in the 35-45 age demographic.

This doesn't mean I have anything against Burberry. I firmly believe that certain brands resonate with one's personal style, but don't at all resonate with others' styles, or suit other people. I know several people who wear and like Versace, but I would never personally wear a single Versace product - it doesn't suit my style.

Burberry is a very successful business, from a mathematical/financial perspective, and it has solid and well-working business goals. The company's current capital allocation framework looks something like this.

{kind=link}

The company wants to maintain IG, which currently calls for the leverage goal of net debt/Adjusted EBITDA to be around 0.5-1x for a TTM basis, which is very conservative and something I can get behind. Furthermore, the basic flows of how money goes from revenue to operating profit to net profit have, even during the worst of times, never gone negative as with some businesses.

Burberry averages gross margins of around 70% and operating margins of 15-18%, which is rising towards the 19-20% mark as some of these improvements take shape. During the worst years, the company has still managed a positive net income margin, which is not something that can be said for every company in this segment. (Source: Tikr.com/S&P Global)

We have a trading update for the latest quarter, which mostly confirms the company's current trajectory. Store sales were up 1% despite continued COVID-19 restrictions in the period in China. Once those effects wind down, we're likely to see significant improvements. Excluding COVID-19 impacts from China, sales are actually up 11%, with 19% of Americas Growth alone.

Several of the company's lines, including handbags, RTW for women, and dresses/knitwear continue to perform very well. The company also targets to have 65 new stores completed in the new look in 2023 alone.

Due to continued high sales growth trends and positive signals, the company seems to see no reason to expect anything except continued positive high-single-digit revenue growth with good margin progression.

Most of the analysts following Burberry missed out on this margin and eps expansion. The reason for this missing out was simple. Burberry has communicated growing targets for some time now, without really pushing through in terms of share price - but for the past 2 months, we're up over 20% in a very short time.

I personally didn't invest in Burberry either at the time but got my eyes on the company when a reader pointed them out to me about a month back or so. Looking at the valuation now makes me wish I had paid closer attention to this undervalued opportunity.

The positive part?

I don't think this was the last opportunity - not even close - and I believe better prices will be coming back.

Burberry Valuation - Difficult today, but might be interesting in the future

I'm a firm believer in that a company follows similar trends as we've seen historically. Any belief that a company has reached a "new paradigm" in terms of its valuation trends usually turns out to be false. Case in point, Burberry.

Burberry Valuation (F.A.S.T graphs)

{kind=link}

Up and down - not unusual exactly, but interesting to see the downright predictability (if not timing) of this pattern. Up to around 21-25x, down to 15x. This makes the "right time" to buy this company a fairly easy exercise. The issue lies now - we could be entering a bit of a growth period for Burberry not seen since the late beginning of the 2000's, which could see the company's valuation remain stretched for some time.

The current valuation targets for Burberry from S&P Global are already being exceeded as I'm writing this article. 22 analysts follow the native LSE ticker, and only one of them is at a "BUY" recommendation, with all the rest either at "SELL", "HOLD" or equivalent passive or negative rating. The range here starts at £17.3, and goes to £28 with an average of £22 - the current native is at £24.5. So even the analysts consider this one stretched.

Peers exist in the form of the luxury apparel companies we've come to know and love - Dior, Richemont (CFRUY), Moncler, VF Cop (VFC), and others. Burberry already trades at a 3x revenue multiple. That's twice the level of Adidas (ADDYY) and on the level of Kering (PPRUY), which I don't believe is justified here. It's in fact higher than Swatch, which does luxury watches - again, I don't see it justified here.

You'd have to discount the company to an 11-12% risk-free rate and a terminal growth rate of almost 6% to get a DCF price that implies anything above £26 is acceptable here. And I don't think that's really valid here, for a few reasons. First of all, analyst accuracy - it's not good. The analysts miss targets by 25-40% either negatively or positively, and they have a tendency of overestimating where Burberry goes.

Secondly, I don't see these targets as being conservative enough. Yes, we have an upside of around 13% annually or nearly 30% in 3 years, but that's really only above 21.5x P/E. At 15x, you're losing 8.3% of your money even with dividends considered, and at anything below 16.5x P/E, you're pretty much-losing money in this investment, if we see a correction as a result of lower earnings, challenges, or sales issues.

The luxury segment is notoriously difficult even for the most established brands. The reason I'm willing to invest so much money in LVMH is that the company is world-leading and owns not one, not even a dozen, but dozens of market-leading and world-leading premium brands in various segments. This gives me safety in such an investment.

Burberry, I believe, does not offer the same. For that reason, I'm not willing to give the company the same sort of premium I do to LVMH or similar companies.

I choose to allow a 16-18x P/E for Burberry - that caps the upside at around 5% annualized, which is below my target return for an investment, especially being as volatile as it is, and being in consumer discretionary.

For that reason, I give Burberry the following thesis for 2023.

Thesis

- Burberry is an impressive luxury company with a worldwide sales profile. It plays in segments similar to LVMH, Kering, VFC, and other companies I own stock. But I have elected, at this time, to not invest in Burberry due to valuation issues with the company trading at over 20x P/E normalized, while essentially being a very volatile investment historical, without some of the fundamentals that would justify a better upside here.

- For that reason, I would call Burberry a "HOLD" here until the valuation improves - either through significantly better earnings or due to a correction, which often happens for Burberry despite growing earnings.

- My PT on the company is £19 for the native to begin with - and we'll continue coverage from this initial article from here on out.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

Because the company is neither cheap nor has a good upside based on a conservative valuation, Burberry only fulfills 3 out of 5 of my criteria. At this time, that's not good enough.

For further details see:

Burberry: I Don't Think The Premium Is Worth It At This Time