BURBY - Burberry's Interim Results: Here's What To Expect

Summary

- Quantitative accounting metrics indicate that Burberry could surprise to the upside when it releases its interim results on November 17th.

- However, China exposure and waning economic activity in the European Union provide cause for concern.

- The company's Veblen Goods status and strong brand identity are positives. Yet, we don't see enough positives to expect a flourishing interim report.

- We assign a hold rating to Burberry until further notice.

The festive season is upon us, and understandably there's much attention on retail stocks. However, in Burberry's ( BURBY ) case, investors have interim results to deal with first. The company is set to release its interim results on November 17th , and there's a lot of rumbling in the air due to the systemic influences the company recently faced.

Today's article covers various influencing variables we've noticed during the company's most recent operating cycle. In addition, a quantitative risk assessment is provided to contextualize the stock's status in the current stock market climate.

Here's a video just for effect; I thought it would be a value-add to lift everyone's spirits before the holiday season enters full flow.

Operational Analysis

Positives

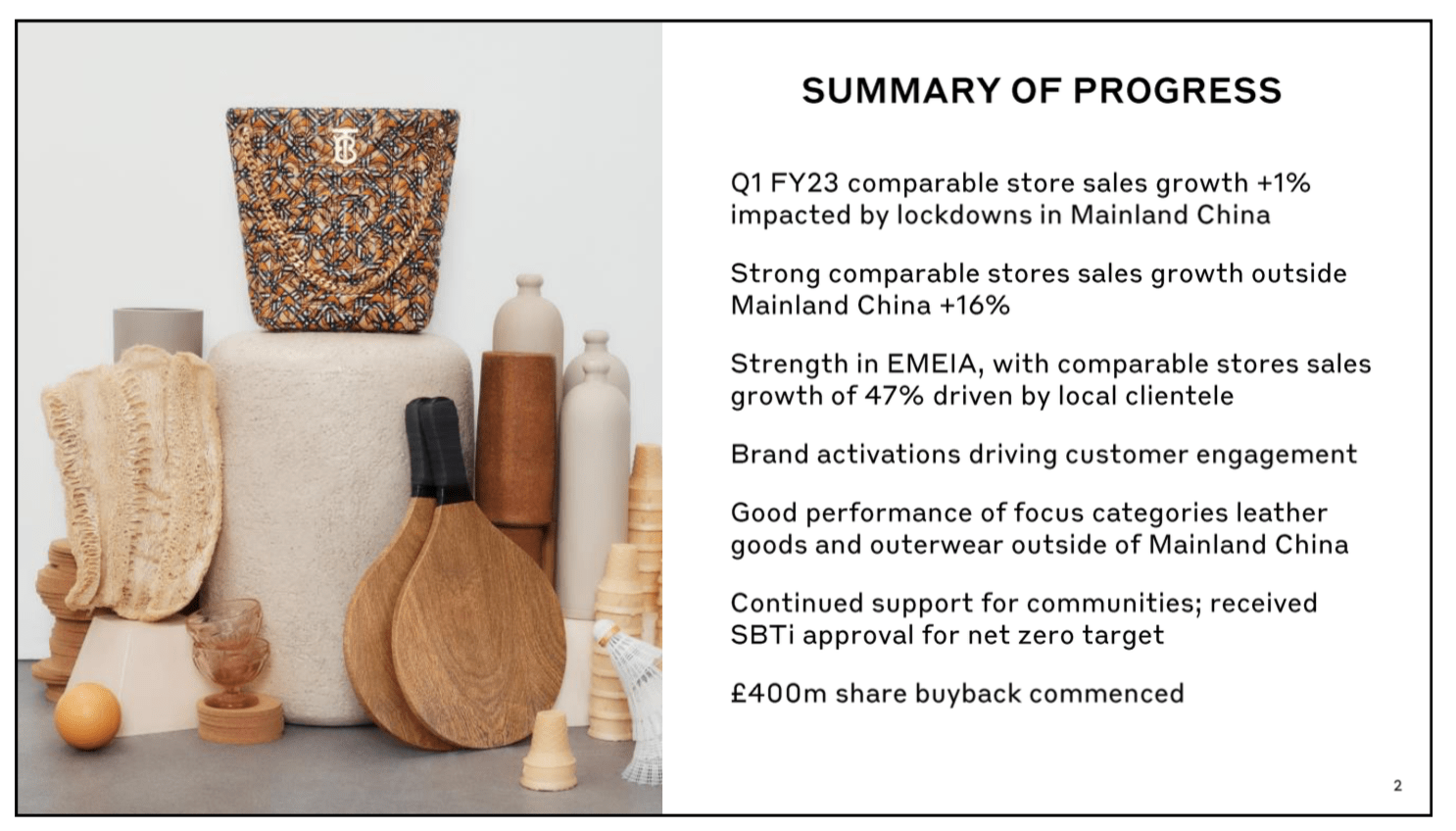

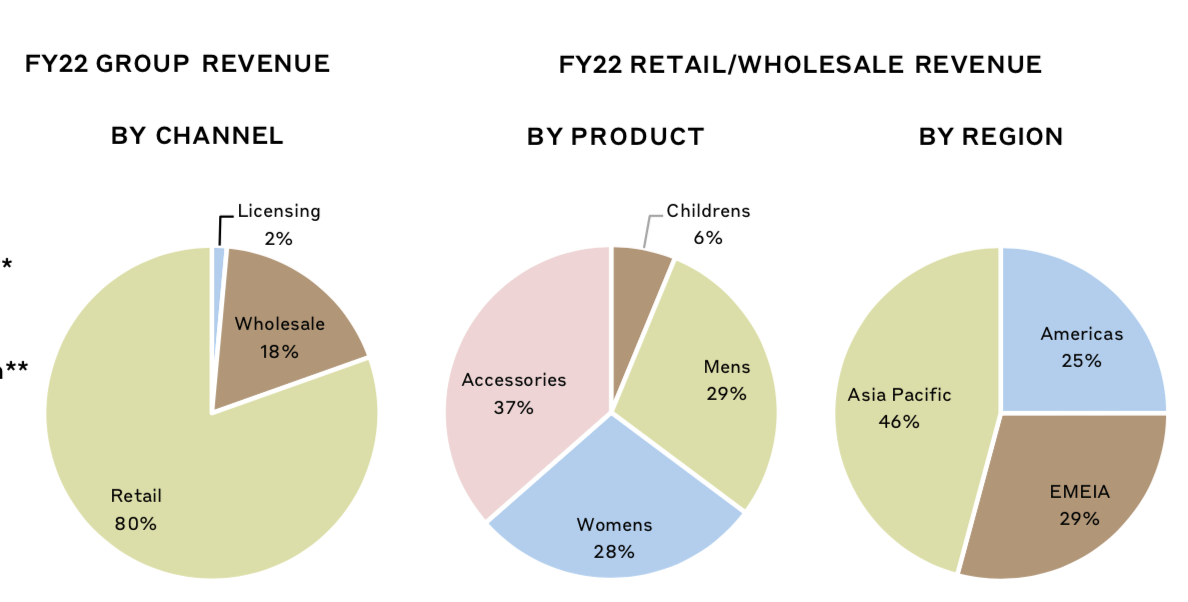

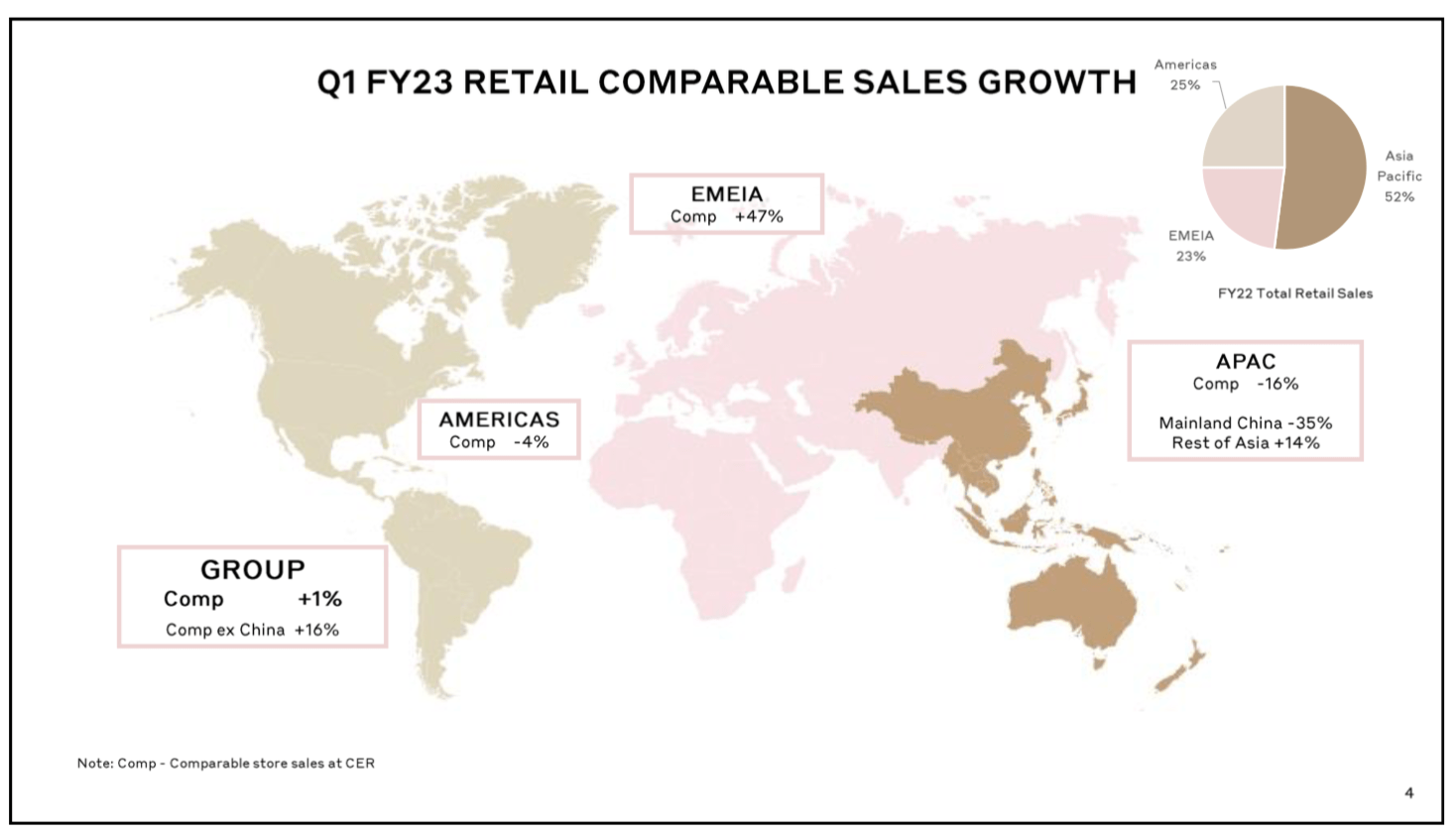

Despite the world economy being in a slight gully, Burberry managed to grow its sales considerably in the past year. According to the company's first-quarter results, it produced 16% year-over-year comparable store sales growth (China excluded and discussed later). The firm's mixture of wholesale and retail exposure allows it to serve more than one area of the supply chain. For instance, Burberry wholesales much of its Asia exposure, which is a smart move considering the differentiated marketing strategy that would be required in the region.

Burberry Investor Pack Burberry Investor Pack

{kind=link}

{kind=link}

Burberry has experienced robust sales growth in the EMEIA (Europe, Middle East, and Africa) region with 47% year-over-year comparable sales store growth.

But are there forces that could've sustained Burberry's sales growth during the past quarter?

In our opinion, there are a few noticeable influencing factors that Burberry possesses. Firstly, it has a strong brand identity, allowing it to sustain sales during trying economic times. In addition, the company targets a niche market of Veblen good buyers. Veblen goods are typically associated with less price and income elasticity as it's catered towards a market of consumers that are in the upper echelon of earners.

Negatives

The elephant in the room is China's influence on Burberry's sales. Regional same stores sales capitulated by 35% in Burberry's previous quarter, driven by the nation's zero-covid policies . There aren't any signs that China's hard line on Covid will wane anytime soon; in fact, the nation has tightened its policies more than anything else.

China isn't only a key point of sales for Burberry but also yields significant influence on the level of global input costs due to its significant presence in manufacturing and raw material exploration. Thus, Burberry's China-based headwinds are twofold.

{kind=link}

Key metrics also imply that Burberry has a few internal issues. For example, the company's total receivables have increased exponentially, indicating doubtful payments, which is extremely concerning given the firm's exposure to China and a waning EU economy .

Furthermore, Burberry's inventory turnover has been exacerbated, given rising global inflation and worrisome supply-chain issues. The inventory turnover ratio measures the cost of goods sold with respect to the average inventory. Thus, parsimoniously speaking, a rise in the ratio is bad for business.

Lastly, Burberry's pre-tax income is diminishing. This could be due to a tight labor market, general inflation, and cyclicality; either way, it's not good to see.

Quantitative Analysis

Today's quantitative risk assessment focuses on accounting-based metrics and the potential volatility investors can expect after (or before) the company releases interim results.

First, Burberry's Beneish M-Score is in the safe zone (less than -1.78). The Beneish M-Score is a parsimonious indicator of a company's accruals. To elaborate, it measures a range of income statement variables to assess whether a company has recognized its past earnings prematurely or whether it's held some of it back. According to Burberry's Beneish M-Score, the company's been conservative on its earnings recognition; therefore, its interim results could reflect a welcome surprise due to previously unrecognized items.

Also, notice the company's negative accruals, illustrating how its sound cash basis performance. However, I realized that much of the firm's cash performance is due to it depreciating and amortizing much of its costs; thus, core net income versus accrual earnings probably is similar in practice.

The metrics below indicate that Burberry is a relatively low-risk stock. For instance, the asset's Beta coefficient is lower than the broader stock market's ( usually considered 1 ), and its monthly 5% value at risk is moderate. The latter means that the stock tends to lose at least 13.40% of its value in 5% of its traded months, and the prior measures the stock's sensitivity to the broader market.

Whether good or bad, collectively, we don't anticipate a tremendous value shift after Burberry's interim results are released.

Concluding Thoughts

Burberry's interim results could be a mixed bag. The company's same-store sales growth is robust, likely due to its strong brand identity and Veblen goods status. However, the firm's exposure to China remains a risk as zero-covid policies persist. In addition, rising implications in Eurozone economies could've hindered Burberry's sales.

From a quantitative vantage point, Burberry exhibits promising accounting metrics as its Beneish M-Score reads well, and its accruals are in negative territory. However, we're unconvinced of a positive earnings report; thus, we assign a hold rating to the stock.

For further details see:

Burberry's Interim Results: Here's What To Expect