BUR - Burford Has Clear Value Beyond Eton/Peterson

2023-04-21 02:09:59 ET

Summary

- Despite the recent run, Burford's shares may be inexpensive.

- Eton/Peterson is key to the stock, but more as a catalyst for revaluing the core business than the direct potential cash receipt.

- If the market sees Burford as offering sustained premium returns, a valuation above $30/share is possible, though a strong and decisive Eton/Peterson outcome may be needed for this.

I wrote a piece suggesting upside after a favorable legal ruling for UK-based litigation finance company Burford Capital ( BUR ) on March 31. Since then BUR stock has drifted up around +17% or so, but perhaps not enough.

Here's some quantification to explain why there is likely further upside for patient investors, and to work through the moving parts. I'm surprised more people haven't written about this one, as it does seem to be an interesting and non-correlated opportunity with the broader markets. It's also one where the stock has popped 55% YTD and maybe a lot of holders feel vindicated and want to sell, perhaps to reign in position sizing, but there still appears to be upside on the table. There has been a lot of focus on the Eton/Peterson judgement, which is understandable, but the real story here may be revaluing the core assets in light of a potentially strong Eton/Peterson outcome.

Context

Burford essentially buys the rights to legal cases and then invests money to fight those cases. Burford then makes money if they win the case (or settles the case positively) or eats the cost when they lose. Some of the money is Burford's own, some is managed on an AuM basis (sovereign wealth funds etc.). Some see this as a great business model, largely uncorrelated with other asset classes. However, others worry that it's opaque and unproven and returns will be unimpressive or erratic and lumpy. There was particular worry that Eton/Peterson case was occupying a large portion of Burford's assets and operations and was a risky bet. However, at the end of March Burford appeared to receive a very favorable judgement on the Eton/Peterson case ( here's Burford's take ), but there are still details to be filled in and the question of whether or not Argentina will pay or continue to fight (or maybe refuse to pay but not make any further legal challenges).

Value of the Verdict

We'll first discuss the valuation of the Eton/Peterson case as a standalone asset, then consider the remaining Burford business.

We can really boil down the legal outcome to three moving parts:

1. The YPF share priced used in the calculation of payment, at the time of the expropriation the share price was understandably volatile and so exact date used makes a big difference to outcomes.

2. Whether interest is applied and what rate is used.

3. When and if Argentina pays.

Dealing with the first 2 issues first, I calculate the following outcomes drawing on Burford's stated share of the payments (75% for Eton and 35% for Peterson) and payment values.

| Timing of compensation date and presence/absence of interest payments |

| 40 days before May 7, 2012 |

| 40 days before April 6, 2012 |

| No interest |

| $1.99B |

| $3.18B |

| With 10 year of simple 6% interest |

| $3.3B |

| $5.28B |

Then to simplify things further, I have no idea which date will be chosen so weight those 50/50 and believe there's a good chance interest will be applied (though the rate is unclear) so will weight 80/20 interest vs. no interest.

That leaves us with an expected value figure for Eton/Peterson of $3.95B. (range $2B-$5.3B). That's before considering taxes, the risk of non-payment and further delays from the legal process or the ruling be overturned.

When and If Argentina Pays

So will Argentina pay the estimated/expected $3.95B? There's some chance they simply refuse to play or win an appeal. Then if they do pay, the process may theoretically take another 1-3 years to conclude.

However, the appeals process may be unappealing to Argentina as the court may require, given the summary judgement that they need to post a bond for billions of dollars during the appeals process.

It also seems likely that Burford would pay tax on the proceeds, I'll assume 20%, though there's limited visibility.

So to take that to per share values, here it is with various probability of Argentina paying, and/or settlement outcomes, using the $3.95B value from above.

| Chance Argentina pays |

| 15% |

| 30% |

| 70% |

| Value per Burford share after 20% tax (219M s/o) |

| $2.16 |

| $4.33 |

| $10.10 |

(note since the ruling Burford's share price has risen ~$5.50/share)

Burford's Underlying Value

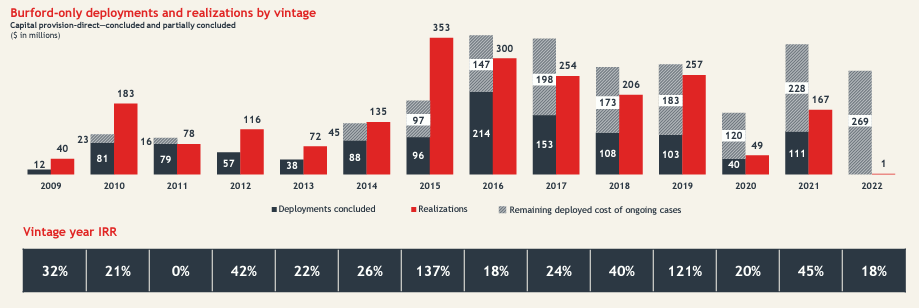

However, perhaps more fundamentally, this potential outcome does suggest Burford's business model works and management knows what they are doing. Below are Burford's estimated IRRs for vintage years from 2009 to 2022 (this excludes the recent Eton/Peterson decision). These IRRs range from 0% to 137% with a simple average by year of 40%.

{kind=link}

Let's review the valuation of the business:

- $325M in cash, marketable securities and near-term receivables

- $3.2B in Burford's own funds (directly owned)

- $3.8B in assets undermanagement in Burford funds, upon which Burford can collect fees generally under a 2% fee and 20% of performance structure

- Against that Burford has $1B in debt and $400M of minority interests

If we assume Burford earns a 5% fee on AuM each year (assuming 15% annual performance) that asset management business is worth $2.85B on a 15x multiple. And then the core business may be worth at least 2x if superior returns can be sustained. That's $4.92B also assuming minority interests are worth 2x book, which is consistent.

Thus the AuM business and the operating business combined, after taking account of net debt and minorities, may be worth $29/share before any additional Eton/Peterson receipts.

That's a really important part of thesis here. If you believe that Burford can continue to earn superior returns then the business should trade at a premium.

Then on top of that you have Eton/Peterson, which based on what we know now is worth $2/share-$10/share, though that will move (up or down) when we learn more about the exact expropriation date and interest rate relating to the judgement and Argentina's reaction to that judgement. That translates to a valuation of $31/share to $39/share.

The real takeaway here is the Eton/Peterson case matters, but what matters more is its ability to reinforce investors' conviction in the quality of the underlying business (or not). So you could say there's real upside to Burford even without the Eton/Peterson verdict, but that's not quite true as it's circular, Burford needs a strong Eton/Peterson outcome to validate the core business.

Conclusion

It appears Burford may be worth over $30/share given its ability to earn superior returns over time for both itself and clients. That's made up of roughly $22/share for the operating business, $13/share for the AuM business less -$6/share for minorities and net debt, and then plus approximately $2/share to $10/share for Peterson/Eton. That appears an attractive risk/return compared to a price of around $13/share at the time of writing.

Risks

- First off, the Eton/Peterson case is trending well but has not concluded. There's a chance that a final outcome takes another 3 years and/or that the initially favorable ruling is reversed. These are not the base case, but possible.

- Secondly, as it grows Burford will see challenges with scale. If it is proving out the litigation finance model, it is sowing the seeds of competition, and operating with billions to deploy rather than hundreds of millions may create further challenges.

- Thirdly, Burford's model requires some trust. Its assets are mostly intangible. This helps the company when things go well, but provides little protection when outcomes are poor.

For further details see:

Burford Has Clear Value Beyond Eton/Peterson